Potassium Sulfate Fertilizer Market Overview

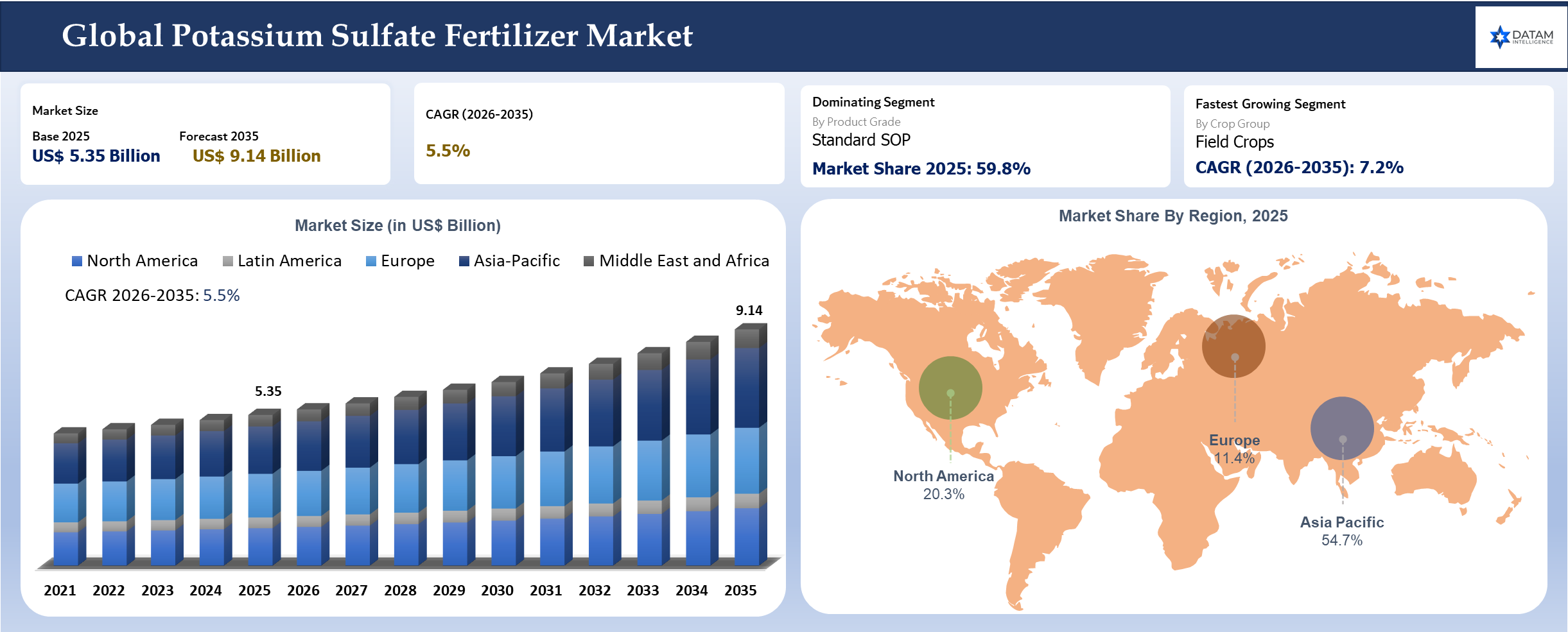

The global potassium sulfate fertilizer market reached US$ 5.35 billion in 2025 and is expected to reach US$ 9.14 billion by 2035, growing with a CAGR of 5.5% during the forecast period 2026-2035. SOP fertilizer demand comes from chloride-sensitive crops that need potassium and sulfur without the quality risk linked to chloride-heavy potash. Fruits, vegetables, potatoes, tobacco, tea, coffee, tree nuts, berries, grapes, citrus and greenhouse crops account for the most defensible demand because output value depends on color, firmness, sugar formation, storage life, taste and export acceptance.

The water-soluble SOP is now being more widely used in drip fertigation, sprinkler fertigation, hydroponics, and greenhouses. It is applied by farmers during blooming, setting, enlargement of fruits, and pre-harvesting periods when there is an increased need for potassium and sometimes not enough nitrogen. Insolubility, rapid dissolution, and suitability to irrigation equipment are crucial factors influencing buyers in this class.

Granular SOP continues to be significant in field fruits, potatoes, tree nuts, tobacco, and plantations. Bulk buyers prefer it for broadcast application, basal placement, band placement and top dressing. Product quality depends on granule strength, uniform spreading, low dusting and dependable chloride control.

SOP pricing remains above MOP because production is more limited and input costs are higher. Adoption is therefore concentrated in crops where the grower can recover the premium through better quality, lower salinity stress, stronger shelf life or higher crop grade realization.

Potassium Sulfate Fertilizer Industry Trends and Strategic Insights

- Water soluble SOP is strongest in fertigation, greenhouse vegetables, berries, hydroponics and export horticulture.

- Granular SOP remains the main field-applied grade for fruits, potatoes, tree nuts, tobacco and plantation crops.

- Low chloride positioning is the main premium lever because chloride-sensitive crops face quality and salinity risks from MOP.

- Mannheim process supports large-scale SOP availability, while brine and mineral-based routes strengthen resource-backed supply positioning.

- Distributor availability, crop-specific guidance and product solubility determine supplier strength more than broad fertilizer portfolio size.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 5.35 Billion | |

| 2035 Projected Market Size | US$ 9.14 Billion | |

| CAGR (2026-2035) | 5.5% | |

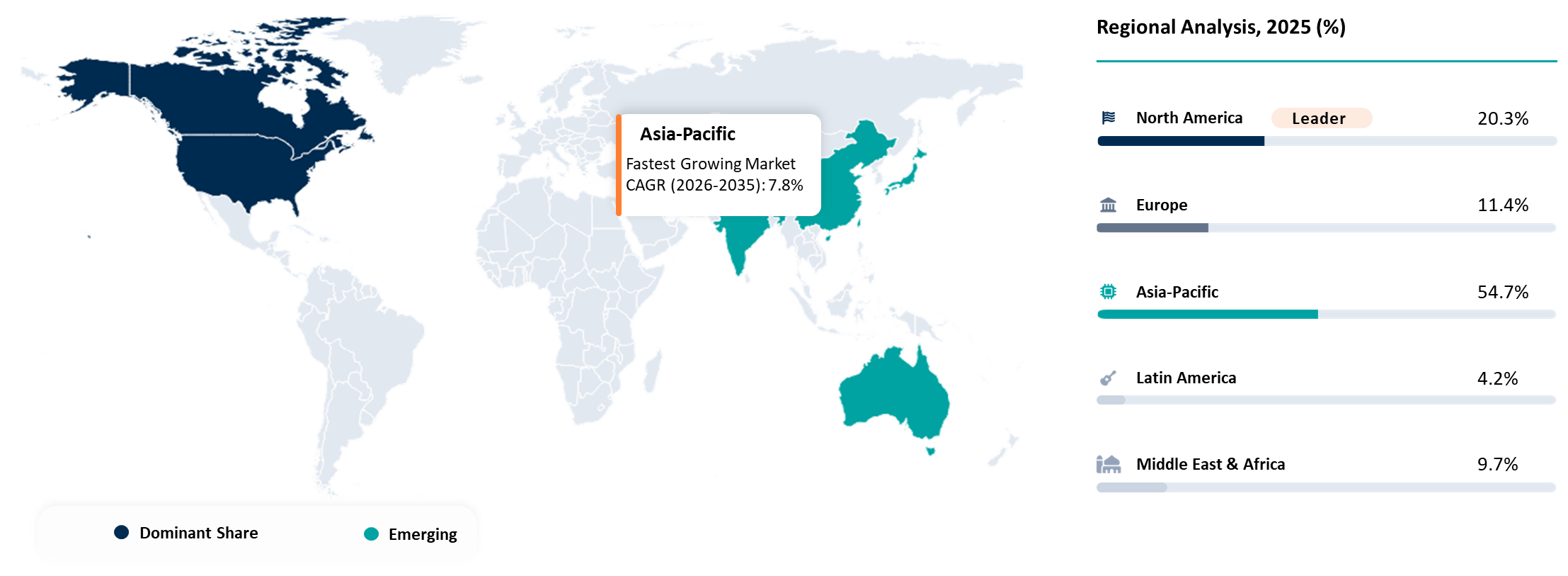

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Product Grade | Standard SOP, Granular SOP, Water Soluble SOP, Low Chloride SOP, High Purity SOP, Organic Compliant SOP, Industrial Grade SOP, Fertigation Grade SOP, Foliar Grade SOP and Others. | |

| By Form | Powder, Granules, Crystals, Fine Crystalline, Liquid SOP Solutions and Others. | |

| By Production Route | Mannheim Process, Sulfate Brine Recovery, Solar Evaporation, Double Decomposition Process, Natural Mineral Processing, Glaserite Process, Langbeinite Processing and Others. | |

| By Crop Group | Fruits, Vegetables, Tree Nuts, Plantation Crops, Field Crops, Ornamental Crops and Others. | |

| By Application Method | Soil Application, Fertigation, Foliar Application, Hydroponic Application and Others. | |

| By Farming System | Open Field Farming, Protected Cultivation, Organic Farming, Precision Farming and Others. | |

| By Distribution Channel | Direct Sales, Distributor Network, Online Agricultural Input Platforms, Greenhouse Input Specialists and Others. | |

| By End-User | Growers, Channel and Institutional Buyers and Others. | |

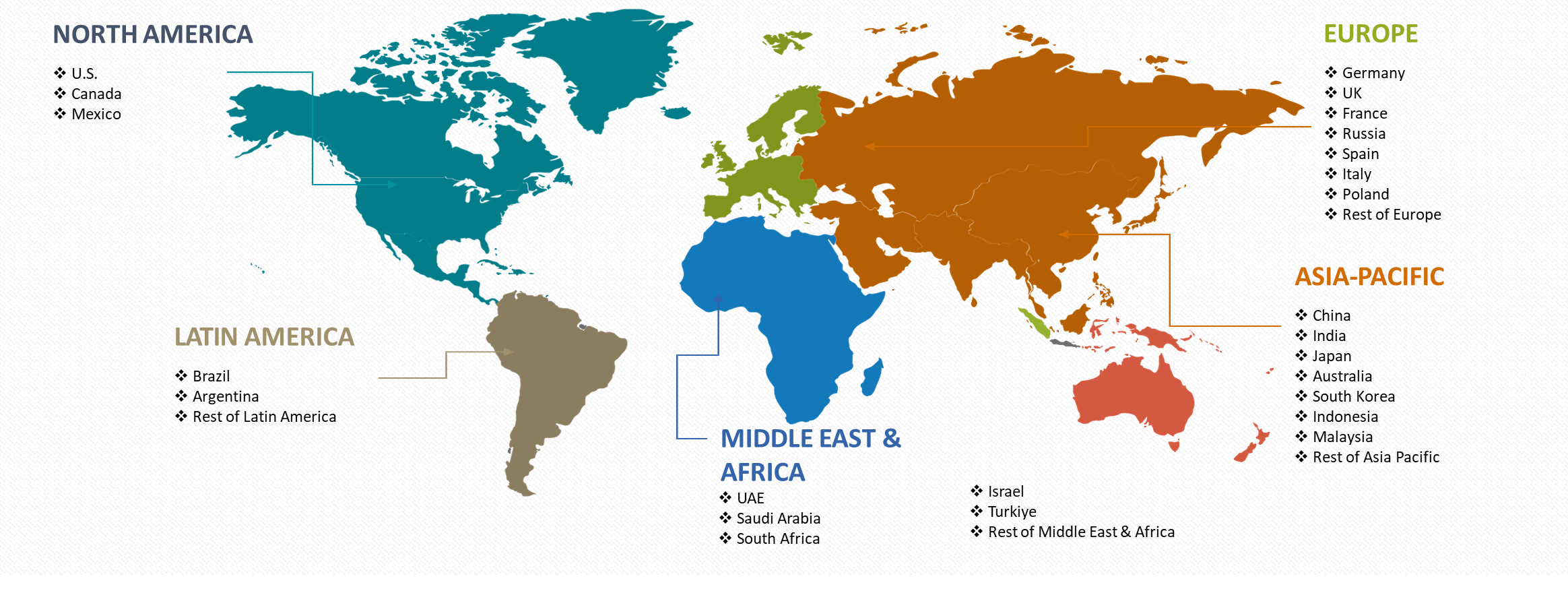

| By Region | North America | USA, Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

AI Impact

AI-Enabled Fertigation Planning Improves SOP Timing and Crop-Stage Nutrition

Artificial intelligence can assist in SOP usage with respect to the nutrient requirement by the plant at different stages. Soil tests, water quality, tissue testing, EC, weather data, and yield mapping can provide information about situations where SOP would be preferred over MOP. High-value crops farmers can utilize SOP at different stages of growth where the need for potassium and sensitivity to chloride will be high.

The artificial intelligence system can help in optimizing fertigation with the use of soluble SOP. Farmers using greenhouses and drip irrigation systems can monitor parameters such as pH levels, EC, water flow, frequency of irrigation, and nutrient uptake more often than conventional farmers.

Supplier planning also improves through demand forecasting. SOP purchases are seasonal and often linked to crop calendars. Dealers need stock before citrus, grape, berry, potato, nut and vegetable application windows. Better forecasting reduces stockouts in import-dependent markets and limits excess inventory after peak application periods.

Agronomists can use AI models to compare SOP, MOP, potassium nitrate and NPK blends across crop stage, chloride tolerance, nitrogen requirement and water salinity. Better recommendation tools can protect SOP pricing because the product is linked to a specific crop need rather than only to potassium content.

Disruption Analysis

Fertigation Growth and Chloride Management Reshape SOP Fertilizer Demand

With fertigation and greenhouse cultivation, there has been an increase in demand for SOP due to its use in soluble nutrition programs rather than in bulk soil applications. Clean crystalline and water-soluble forms of SOP are required by crops such as berries, tomatoes, cucumbers, peppers, flowers, and hydroponic plants. Suppliers who produce consistent grades of crystalline and water-soluble SOP have greater access to professional farmers.

Potassium fertilizers are being affected by changes in chloride management among high-value farmers. Although MOP is cheaper than SOP, farmers who grow tobacco, potatoes, grapes, citrus, berries, tea, and coffee have more potential risks due to chlorides.

Production route volatility is affecting buyer preference. Mannheim producers depend on potassium chloride, sulfuric acid and energy cost. Brine and mineral-based producers depend on resource access, recovery economics and regional logistics. Import-dependent countries face price and availability pressure during peak crop seasons. Sustainable and organic farming are creating smaller premium pockets. Organic compliant SOP, low carbon SOP and naturally derived SOP grades are gaining attention in Europe, North America and export horticulture. Buyers in these pockets need documentation, source transparency and retailer-acceptable input claims.

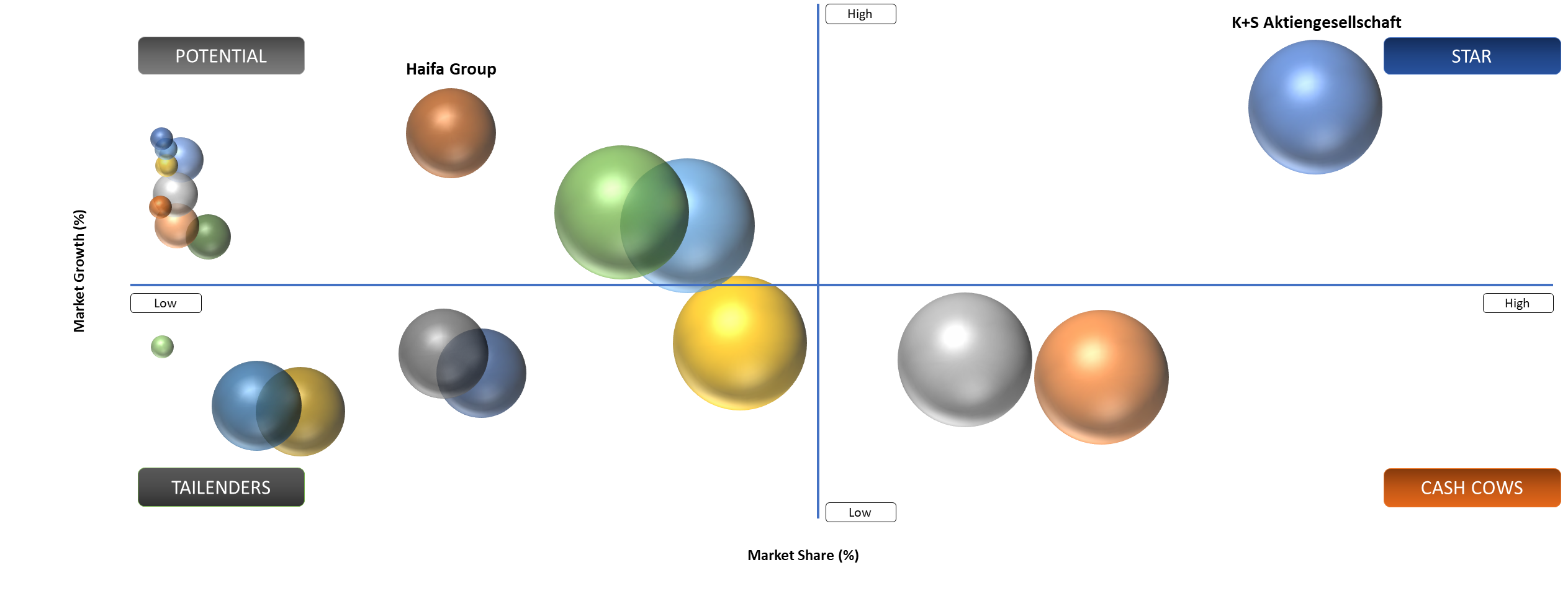

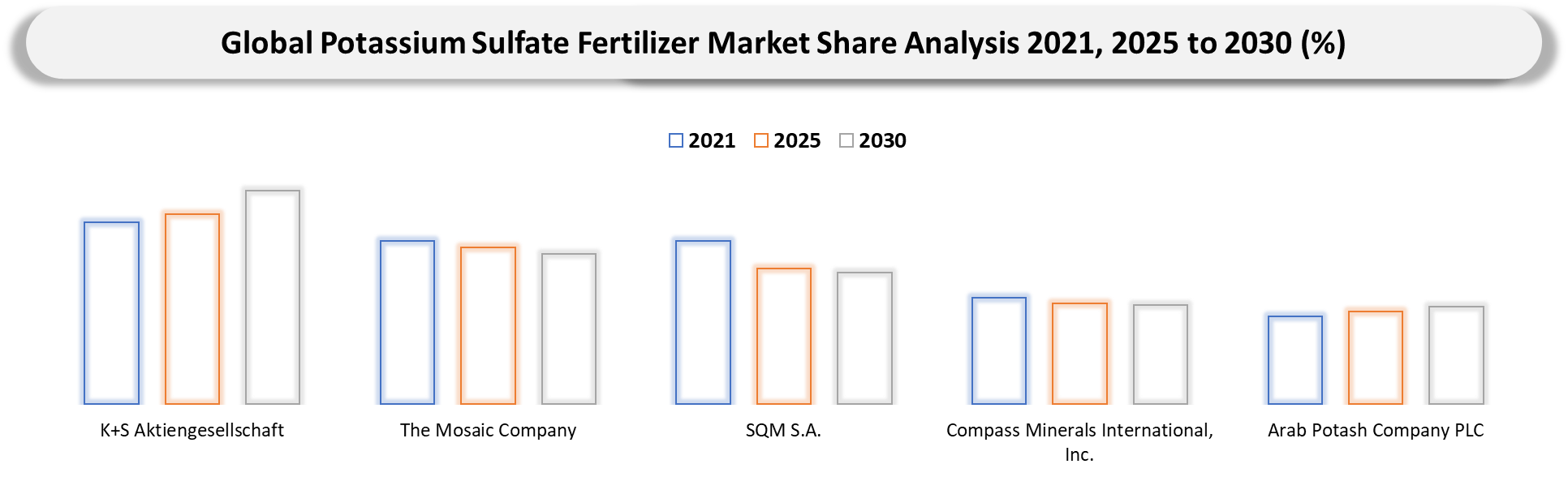

BCG Matrix: Company Evaluation

Stars include K+S Aktiengesellschaft and Compass Minerals International, Inc. K+S has SOP relevance through soluble SOP products used in fertigation, fruit and vegetable crops and chloride-sensitive applications. Compass Minerals has strong positioning through Potassium Plus, which targets premium crops requiring potassium and sulfur with low chloride exposure. Both companies have clear SOP product identity, grower-facing positioning and repeat demand from specialty crop programs.

Cash Cows include SQM S.A. and The Mosaic Company. SQM has long-standing strength in specialty plant nutrition and potassium-based fertilizers. Mosaic has strong crop nutrition reach and agronomic visibility, although its strength is broader than dedicated SOP leadership. Both companies benefit from established customer access, distributor relationships and recurring fertilizer demand.

Potential players include Tessenderlo Group and Haifa Group. Tessenderlo has relevance through soluble and granular potassium sulfate offerings. Haifa Group has strong positioning in water soluble potassium sulfate for Nutrigation and specialty crop programs. Growth potential is concentrated in fertigation, greenhouse crops, export horticulture and chloride-sensitive crop programs.

Tailenders include fragmented regional SOP suppliers and fertilizer blenders that compete mainly on price and short-term availability. Weakness appears where suppliers lack soluble-grade consistency, crop-specific technical support, low chloride credibility and dependable regional stock.

White Space Opportunities

White-space opportunity is strongest where the current market offer remains too broad for the problem the buyer is actually trying to solve inside the potassium sulfate fertilizer market. A large part of the market still packages value at a category level even though revenue is shifting toward narrower use cases with stronger consequences for quality uptime route stability or premium output. Suppliers that design propositions around those exact pain points can create defensible share faster than vendors pushing average-market language.

Mid-market and retrofit environments remain under-served across many of these markets. Large flagship projects receive the most attention while a meaningful pool of profitable demand sits inside existing assets regional operators and buyers that need practical upgrades rather than full replacement. Better modularity, stronger advisory support and lower implementation friction can unlock value that is still poorly captured.

Service layers offer another open opportunity. Buyers increasingly want lower risk clearer validation and stronger lifetime economics rather than just a product transaction. Testing support optimization training modernization traceability and co-development can therefore generate stickier revenue than one-time selling in many of these segments.

Geographic localization is still weak in many offers. Country-level operating conditions differ more than many vendors admit. Players that localize specification strategy without fragmenting their platform will gain more share in the next phase of market development.

Market Dynamics

Rising Use of SOP in Chloride-Sensitive and Fertigation-Intensive Crops

SOP demand is increasing in fruits, vegetables, potatoes, tobacco, tea, coffee, tree nuts and greenhouse crops because these crops need potassium without added chloride. MOP remains cheaper, but chloride can affect crop quality, root performance, sugar formation, storage life and salinity balance in sensitive crops.

High-value horticulture supports stronger SOP use because potassium affects fruit size, color, firmness, sugar content and stress tolerance. Sulfur also supports protein synthesis, enzyme activity and crop quality. Growers selling into export markets, processors and premium retail channels can justify SOP when better crop grade offsets the fertilizer premium.

Drip irrigation and greenhouse farming are increasing demand for water soluble SOP. Growers apply soluble SOP during flowering, fruit development and pre-harvest stages when potassium demand is high. Expansion of berries, greenhouse vegetables, hydroponics and flower cultivation supports demand for high purity soluble grades. Salinity pressure in irrigated agriculture is adding another growth layer. Farms using saline water or farming in dry regions need potassium sources that do not add more chloride to the root zone. SOP fits these conditions better than MOP when crop sensitivity and water quality risks are high.

Higher SOP Cost and Continued MOP Substitution

SOP adoption remains restricted by its higher price compared with MOP. Broadacre growers and price-sensitive farmers continue using MOP or NPK blends when crop value does not justify the SOP premium. Dedicated SOP use is strongest only were chloride sensitivity, salinity risk or crop quality can offset the added cost.

Supply availability also limits adoption. SOP supply is narrower than conventional potash supply and many countries depend on imports. Dealers may not stock enough soluble or granular SOP before peak crop stages. Growers may switch to MOP, potassium nitrate or blended fertilizers when SOP is unavailable at the required time.

The levels of grower awareness vary greatly. Farmers usually choose potassium fertilizers based on their nutrient content and prices. Inadequate awareness of chloride tolerance, salinity of water, suitability for fertigation, and crop-specific potassium needs prevent the shift from MOP to SOP.

In addition, alternative specialty fertilizers pose another obstacle for SOP usage. The choice of potassium nitrate is justified when crops require not only potassium but also nitrate-nitrogen. Meanwhile, if a grower needs several nutrients in a single fertilizer, he will go for the NPK combination.

Segmentation Analysis

Water Soluble SOP Gains Share in Fertigation and Greenhouse Nutrition

Standard SOP serves open-field fruits, vegetables, potatoes, tobacco, tea, coffee and plantation crops where growers need chloride-free potassium and sulfur without the higher cost of fully refined soluble grades. Buyers usually select standard SOP when crop sensitivity to chloride is clear but application is still managed through conventional fertilizer programs.

Granular SOP is used in orchards, potato farms, tree nut plantations, tobacco fields and plantation crops. Demand is linked to bulk handling, spreader compatibility, uniform granule size, low dusting and dependable field distribution. Growers prefer this grade when SOP is applied through broadcast spreading, basal placement, band placement or top dressing.

Water soluble SOP is used in drip fertigation, sprinkler fertigation, hydroponics and greenhouse dosing. Demand comes from greenhouse vegetables, berries, grapes, flowers and high-value fruit crops where fast dissolution, low insoluble matter and irrigation-line compatibility directly affect nutrient delivery. Growers apply soluble SOP during flowering, fruit sizing and pre-harvest stages when potassium demand rises and additional chloride or nitrogen is not preferred.

Low chloride SOP serves tobacco, potatoes, grapes, berries, citrus, tea, coffee and greenhouse vegetables where chloride accumulation can affect quality, root health, storage performance or market grade. High purity SOP is used in fertigation and specialty crop programs where insoluble matter, tank mixing and irrigation-system cleanliness influence product selection.

Powder and crystalline SOP are used in soluble fertilizer production, fertigation tanks and specialty nutrient blends. Granular formats are used in field application and distributor-led sales. Fine crystalline grades are preferred where fast dissolution and clean tank mixing are required.

Mannheim process SOP supports large-scale commercial supply and consistent industrial output. Sulfate brine recovery and solar evaporation support resource-backed supply where brine assets are available. Double decomposition and natural mineral processing support regional production where suitable raw materials and conversion economics are favorable.

Crop demand is strongest in fruits, vegetables, tree nuts, potatoes, tobacco, tea, coffee, greenhouse crops and ornamentals. Fruits and vegetables lead value demand because color, sugar content, firmness and shelf life affect price realization. Tree nuts and potatoes support granular SOP use, while greenhouse vegetables, berries and flowers support soluble SOP demand.

Direct sales are stronger with large farms, greenhouse operators and commercial horticulture groups. Distributor networks, fertilizer dealers and cooperatives dominate granular SOP movement. Greenhouse input specialists and agrochemical retailers are stronger in soluble SOP and specialty nutrition programs. Online agricultural platforms remain small but useful for specialty product discovery.

Geographical Penetration

Asia-Pacific Leads Through SOP Production, Horticulture Acreage and Fertigation Growth

Asia-Pacific has the most strategic role in the fertilizer industry due to its high area under fruit and vegetable farming, fertilizer usage, increased protected cropping, and indigenous SOP production. China has the leading role in Asia-Pacific due to its production of SOPs, high horticulture, and efficient fertilizer distribution. Chinese SOP output also affects export availability and price movement in import-dependent markets.

The demand from China has its backing in terms of vegetables, fruits, tea, tobacco, potatoes, and greenhouse crops. The water-soluble SOP has started to acquire increasing importance in the realm of protected cultivation and fertigation for growing vegetables, whereas the granular SOP still holds its significance in the case of open field crop programs.

India offers one of the strongest growth opportunities in Asia-Pacific. Grapes, pomegranates, bananas, potatoes, tea, coffee, vegetables and protected cultivation crops support SOP demand. Drip irrigation expansion in horticulture improves the case for water soluble SOP because growers can apply potassium during crop stages linked to flowering, fruit development and quality improvement. Price sensitivity remains a restraint because many growers still compare SOP against MOP and NPK blends rather than against crop-grade improvement.

Japan, South Korea and Australia represent more developed premium-use pockets. Japan and South Korea support demand through protected cultivation, vegetables, fruits and high-value horticulture where input quality and crop appearance matter. Australia has SOP relevance in almonds, grapes, citrus, vegetables and irrigated agriculture, especially were salinity management and water quality influence potassium fertilizer choice.

Southeast Asia generates demand for SOP due to its plantation crops, fruits, vegetables, coffee, and export-oriented horticulture. Potassium fertilizers are used in Southeast Asia by countries like Vietnam, Thailand, Indonesia, and the Philippines in their tropical crops. The use of SOP is dependent on the cost and availability of dealers, and also on the value of crops planted.

North America Benefits from Specialty Crops, Salinity Management and Established SOP Brands

There is stable SOP demand in North America driven by specialty crops, tree nuts, fruits, vegetables and potatoes. United States is the dominant region owing to specialty crop production, reliance on irrigation and soil salinity issues. Compass Minerals increases SOP profile in North America through Potassium Plus that is marketed as a source of potassium and sulfur nutrients with minimal chloride content. There is a strong SOP demand in regions where there is potassium requirement for crop quality without using MOP that has higher chloride content. Major crops benefiting from SOP use include tree nuts, grapes, citrus, potatoes and vegetables.

The demand for water soluble SOP is driven by its suitability in fertigation for valuable crops as well as for controlled nutrient program. Growers utilize soluble potassium fertilizers through drip irrigation in orchards, vineyards, vegetables and greenhouses when crop timing and nutrient interaction with water is significant. The demand for granular SOP continues in field applied crops through fertilizer distributors and agricultural distributors.

Canada contributes demand through potatoes, greenhouse vegetables, fruits and specialty agriculture, although overall SOP consumption is smaller than the U.S. Greenhouse production in Canada supports soluble fertilizer use, while field crop use remains more price-sensitive. Mexico adds demand through export vegetables, berries, avocados, citrus and protected cultivation, especially in regions supplying the U.S. retail and foodservice markets.

Europe Supports Premium SOP Demand Through Greenhouse Farming, Potatoes, Fruits and Compliance-Led Agriculture

Europe has strong premium SOP demand because growers place high value on soluble inputs, low chloride fertilizers, documented product quality and efficient nutrient management. Greenhouse vegetables, berries, potatoes, grapes ornamentals and organic farming support steady SOP use. Environmental constraints and increased regulation on the inputs sector can aid in creating demand for low-chloride fertilizers.

Western Europe is crucial for greenhouse vegetables and ornamentals, potatoes, and horticulture. Countries like the Netherlands, Spain, France, Germany, Belgium, and Italy are significant demand centers. Spain and Italy are driving the SOP market in fruits, vegetables, grapes, citrus, and greenhouse crops. The Netherlands and Belgium drive soluble fertilizers demand from greenhouse vegetables and flowers.

Eastern Europe offers growth in potatoes, vegetables orchards and expanding modern farming systems. Adoption is more mixed because price sensitivity remains higher than in Western Europe. SOP gains traction where growers serve export markets or where crop quality, storage performance and chloride sensitivity are clearly linked to returns.

Organic and sustainable agriculture strengthen SOP’s European positioning. Organic compliant SOP and lower footprint SOP products can attract premium buyers in certified production, greenhouse systems and retailer-driven supply chains. Growers need input documentation origin clarity and compatibility with certification requirements, especially in premium fruits, vegetables and horticulture.

European demand is also supported by strong technical distribution. Specialized fertilizer distributors, greenhouse supply companies, and agronomic advisors aid in positioning SOP based on the developmental stage of crops, irrigation method, and the tolerance level to chloride. The supplier's competitive edge is determined by factors such as the quality of the soluble grade, certification documents, and regional availability besides the pricing.

Competitive Landscape

SOP Competition Is Led by Product Purity, Chloride Control and Crop Support

- K+S, Compass Minerals, SQM, Mosaic, Tessenderlo, Haifa, ICL, Yara, Arab Potash, Van Iperen and Cinis compete through SOP availability, specialty plant nutrition portfolios, soluble-grade quality and crop-specific positioning. Strong competitors have a defined role in chloride-free potassium, water soluble SOP, granular SOP, low chloride crop programs or sustainable SOP supply.

- Granular SOP competition depends on bulk supply, granule strength, low dust, dealer reach and price stability. Water soluble SOP competition depends on dissolution speed, insoluble matter, fertigation compatibility, purity and technical guidance. Low chloride SOP competition depends on product consistency and proven fit for chloride-sensitive crops.

- Broad fertilizer companies use dealer networks and agronomic reach to move SOP into existing accounts. Specialty nutrition suppliers gain advantage in greenhouse, hydroponic and export crop programs where growers require dosing guidance, tank-mix compatibility and crop-stage recommendations.

- Price competition is strongest in standard and bulk granular SOP. Premium competition is stronger in water soluble SOP, high purity SOP, low chloride SOP organic compliant SOP and lower carbon SOP. Suppliers with regional stock availability and agronomic support can defend pricing better than suppliers selling only on nutrient analysis.

Key Developments

- May 2026: SQM S.A. maintained specialty plant nutrition relevance through potassium-based fertilizer solutions used in high-value agriculture and fertigation programs.

- March 2026: Compass Minerals International, Inc. continued to support premium crop nutrition through Potassium Plus, with demand linked to tree nuts, fruits, vegetables and low chloride potassium programs.

- January 2026: K+S Aktiengesellschaft expanded SOP visibility through soluble and specialty plant nutrition products used in fertigation, fruits, vegetables and chloride-sensitive crops.

- November 2025: Haifa Group strengthened water soluble SOP positioning through Nutrigation programs for greenhouse vegetables, fruits, flowers and specialty crops.

- September 2025: Tessenderlo Group supported SOP demand through soluble and granular potassium sulfate products used in fertigation, horticulture and soil-applied potassium programs.

- July 2025: The Mosaic Company remained active in crop nutrition education and potassium fertilizer positioning, including sulfate of potash awareness for chloride-sensitive crops.

- February 2025: ICL Group Ltd. continued to serve specialty fertilizer and water-soluble plant nutrition demand where fertigation and hydroponics require clean potassium sulfate.

- October 2024: Van Iperen International and Cinis Fertilizer AB gained visibility in water soluble and lower footprint SOP positioning for fertigation and specialty crop nutrition.

- August 2024: Arab Potash Company PLC remained relevant through potassium resource access and regional fertilizer supply strength, with SOP opportunity linked to specialty crop demand.

- June 2024: Yara International ASA supported professional grower demand through specialty and water-soluble fertilizer offerings used in fertigation and high-value crop nutrition.

DMI Opinion

According to DataM, the potassium sulfate fertilizer market will reward precision more than breadth over the next cycle. Buyers are not short of alternatives. Buyers are short of suppliers that can prove why a specific solution is the right one under a defined operating constraint. Markets of this kind rarely reward generic category language for long because the customer can see where failure really happens.

Strong long-term positions will belong to companies that combine technical credibility commercial patience and execution quality. Technical credibility gets the supplier onto the shortlist. Commercial patience keeps the supplier close to the customer through testing validation or planning cycles. Execution quality turns that first decision into repeat business and stronger pricing power.

Premium value is also likely to migrate toward subsegments that still look narrow today. Smaller segments with higher switching barriers or stronger visibility around failure often shape margin more than large segments built on easy substitution. Companies that understand those pockets early can create a more durable market position than volume-led competitors.

As per our analysis, the next phase of competition will be decided by who best understands field reality. Product strength will continue to matter. Commercial winners will be the companies that can translate that strength into a lower-risk decision for the buyer.

Why Choose DataM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

Target Audience

- Manufacturers and OEMs: Companies producing systems materials ingredients or components linked to potassium sulfate fertilizer market and evaluating product strategy expansion priorities and competitive positioning.

- Distributors and Channel Partners: Firms managing regional sales specification support dealer networks or value-added services in this market.

- Asset Owners and Commercial Buyers: Operators processors building owners utilities farms or industrial users procuring solutions based on lifecycle economics uptime quality or compliance needs.

- Engineering and Technical Teams: Consultants plant managers formulation experts project developers or maintenance leads responsible for validating performance and implementation fit.

- Investors and Private Equity Firms: Financial stakeholders assessing margin structure consolidation potential and growth pockets in premium or underpenetrated subsegments.

- Government Regulators and Standards Bodies: Institutions shaping safety environmental trade building agricultural or quality frameworks that affect demand formation.

- Technology and Service Providers: Companies offering analytics testing retrofit support digital tools or system-integration capabilities that complement the core market.

- Strategic Procurement and Supply Chain Leaders: Decision-makers monitoring sourcing resilience feedstock risk regional supply concentration and long-term supplier reliability.