Point-of-Care Ultrasound Market Size and Trends

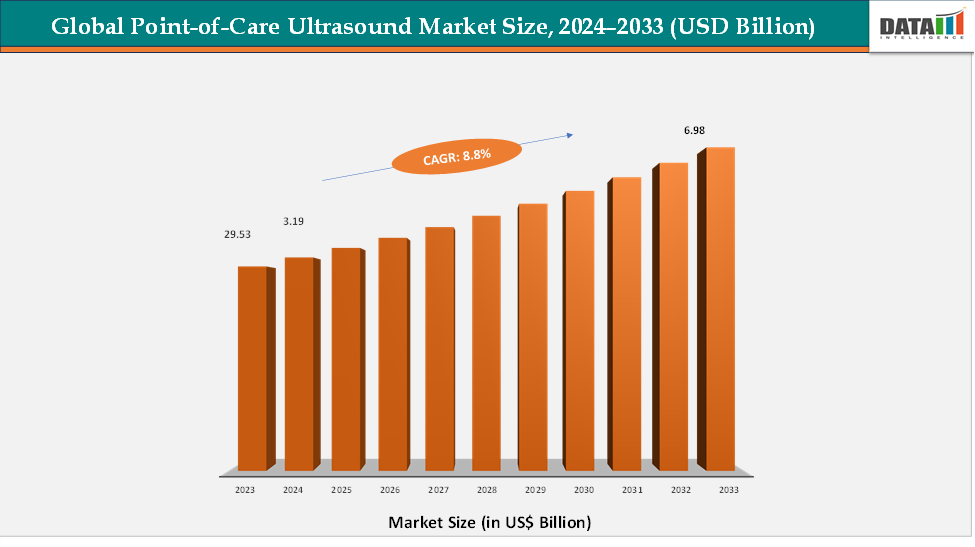

The global point-of-care ultrasound market reached US$ 2.35 billion in 2025 and is expected to reach US$ 4.60 billion by 2033, growing at a CAGR of 8.8% during the forecast period 2026–2033. The global portable ultrasound market is witnessing strong growth, driven by the increasing demand for rapid, accurate, and point-of-care imaging solutions across hospitals, clinics, and remote healthcare settings. Portable ultrasound devices provide real-time, high-resolution imaging that supports faster diagnosis, improved clinical decision-making, and enhanced patient outcomes. Technological innovations such as AI-assisted imaging, wireless connectivity, handheld form factors, and cloud-based data integration are improving diagnostic precision, ease of use, and workflow efficiency. Rising prevalence of chronic diseases, expanding adoption of bedside and emergency imaging, and growing healthcare infrastructure in emerging economies are further fueling market adoption. Additionally, the integration of portable ultrasound into telemedicine and homecare services is creating new opportunities, establishing these devices as essential tools in modern healthcare and driving long-term market expansion.

Key Market highlights

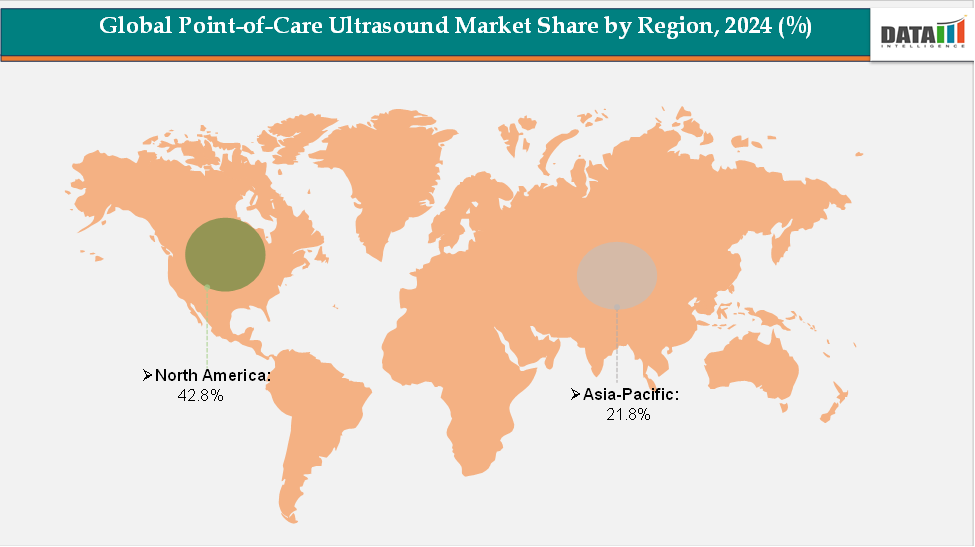

- North America leads the point-of-care ultrasound market, accounting for approximately 42.8% of global revenue, supported by high diagnostic testing volumes, advanced healthcare infrastructure, and the strong presence of key ultrasound device manufacturers.

- Asia-Pacific is the fastest-growing regional market, holding about 21.8% of the share, driven by expanding healthcare access, rising prevalence of chronic and infectious diseases, and increasing investments in portable and point-of-care imaging technologies across countries such as China, India, Japan, and South Korea.

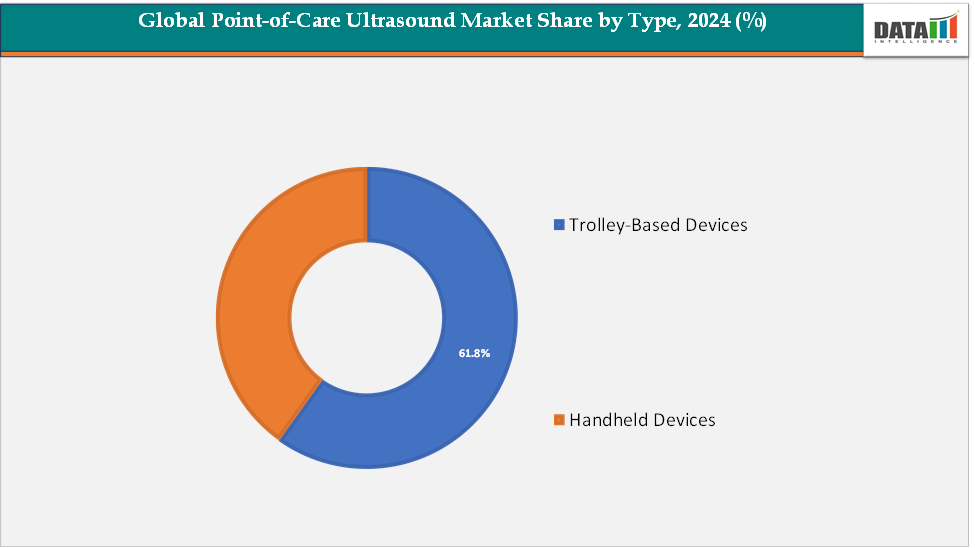

- Trolley-Based Devices remain the dominant product segment, contributing around 61.7% of global revenue. Their widespread adoption in hospitals and diagnostic centers, owing to portability, versatility, and ability to support multi-department imaging needs, underscores their crucial role in driving market growth.

Market Size & Forecast

- 2025 Market Size: US$ 2.35 billion

- 2033 Projected Market Size: US$ 4.60 billion

- CAGR (2026–2033): 8.8%

- North America: Largest market in 2024

- Asia Pacific: Fastest-growing market

Market Dynamics

Driver: Rising Demand for Rapid Diagnostics

The rising demand for rapid diagnostics is a key driver of the portable ultrasound market, as healthcare providers increasingly prioritize timely, bedside imaging to support immediate clinical decision-making. Point-of-care ultrasound enables quick assessment of critical conditions such as trauma, cardiac emergencies, and obstetric complications, reducing the need for patient transfers to radiology departments and shortening diagnosis times from hours to minutes.

For instance, studies indicate that the use of portable ultrasound in emergency and critical care settings can reduce patient turnaround time by up to 30–40% while improving diagnostic accuracy for conditions like internal bleeding and heart failure. Additionally, the growing prevalence of chronic diseases, including cardiovascular disorders and diabetes-related complications, has amplified the need for frequent, rapid imaging to monitor disease progression and guide interventions. By delivering real-time, high-resolution imaging at the patient’s bedside, portable ultrasound devices effectively meet this demand, enabling faster treatment, improving patient outcomes, and alleviating pressure on overburdened healthcare systems, particularly in high-volume hospitals and remote care settings.

Restraint: High Capital and Maintenance Costs

High initial costs of point-of-care ultrasound devices can limit adoption, especially among small clinics, outpatient centers, and low-resource healthcare settings. The expense of advanced systems, combined with ongoing maintenance and training requirements, may delay purchases and restrict market penetration despite the clinical benefits and growing demand for rapid diagnostics.

For more details on this report, Request for Sample

Segmentation Analysis

The global point-of-care ultrasound market is segmented by type, application, and end-user, and region.

Product Type: The trolley-based devices segment is estimated to have 61.7% of the point-of-care ultrasound market share.

The trolley-based devices segment is expected to dominate the portable ultrasound market due to its versatility, robustness, and suitability for multi-department clinical use. These systems are widely adopted in hospitals and large diagnostic centers, where high patient volumes and diverse imaging needs require reliable, full-featured machines. Trolley-based devices provide superior image quality and support complex diagnostic procedures, including cardiac, abdominal, and musculoskeletal imaging. Their adaptability across emergency rooms, intensive care units, and surgical suites makes them indispensable in institutional settings, contributing significantly to market revenue and establishing their dominance in the global portable ultrasound landscape.

The handheld devices segment is estimated to have 38.3% of the point-of-care ultrasound market share.

Handheld devices are the fastest-growing segment in the portable ultrasound market, driven by their compact size, ease of use, and growing adoption in point-of-care and remote healthcare settings. These devices enable clinicians to perform quick bedside assessments, facilitate telemedicine consultations, and support home care and rural diagnostics where traditional equipment is impractical. The integration of wireless connectivity, smartphone compatibility, and AI-assisted imaging enhances usability and diagnostic accuracy, making handheld systems increasingly attractive for emergency care, outpatient clinics, and field applications. Rising demand for flexible, low-cost imaging solutions and the shift toward decentralized healthcare delivery are propelling the rapid growth of handheld ultrasound devices globally.

Geographical Analysis

The North America point-of-care ultrasound market was valued at 42.8% market share in 2024

North America leads the portable ultrasound market, accounting for the largest share of global revenue, driven by advanced healthcare infrastructure, high adoption of point-of-care imaging, and strong presence of major ultrasound device manufacturers such as GE Healthcare, Philips, and Fujifilm Sonosite. The region’s emphasis on rapid diagnostics in emergency, critical care, and obstetric settings, coupled with substantial investments in healthcare technology and ongoing training programs for clinicians, has accelerated the adoption of both trolley-based and handheld ultrasound systems. High patient volumes, well-established reimbursement policies, and a focus on improving clinical workflow efficiency further reinforce North America’s dominant position in the portable ultrasound market.

The Europe Point-of-Care Ultrasound market was valued at 20.9% market share in 2024

Europe holds a significant position in the portable ultrasound market, supported by well-established healthcare systems, strong regulatory frameworks, and widespread adoption of advanced imaging technologies. The region’s focus on enhancing patient outcomes through early diagnosis and efficient care, along with high penetration of both trolley-based and handheld ultrasound devices in hospitals and specialty clinics, sustains steady market demand. Additionally, Europe benefits from technological collaborations, R&D initiatives, and increasing use of AI-enabled imaging solutions, which further reinforce its critical role in the global portable ultrasound market.

The Asia-Pacific Point-of-Care Ultrasound market was valued at 21.8% market share in 2024

Asia-Pacific is the fastest-growing region in the portable ultrasound market, propelled by expanding healthcare access, rising prevalence of chronic and acute diseases, and increasing government and private sector investments in diagnostic imaging infrastructure. Countries such as China, India, Japan, and South Korea are witnessing rapid adoption of portable and handheld ultrasound devices to address the growing demand for point-of-care diagnostics in hospitals, clinics, and rural healthcare settings. The combination of rising awareness, improving affordability, and integration of telemedicine platforms is driving accelerated growth in the APAC market, positioning the region as a key area for future expansion.

Competitive Landscape

The major players in the Point-of-Care Ultrasound market include GE HealthCare, Shenzhen Mindray Bio-Medical Electronics Co., Ltd., FUJIFILM Sonosite, Inc., Canon Medical Systems Corporation, BenQ Medical Technology Corp., DrSono, Butterfly Network, Inc., Clarius, Konica Minolta, Inc., CHISON Medical Technologies Co., Ltd., among others.

Key Developments:

- 2026: Increasing focus on AI-integrated point-of-care ultrasound devices, enabling faster diagnosis and automated image interpretation, particularly in emergency and maternal care settings, improving accessibility in low-resource and rural environments.

- 2026: Butterfly Network received regulatory clearance for an AI-powered ultrasound tool for pregnancy assessment, enhancing rapid bedside diagnostics and expanding global access to prenatal imaging solutions.

- 2026: Growing adoption of portable and handheld ultrasound systems, driven by demand for real-time bedside imaging in ambulances, emergency departments, and remote healthcare facilities.

- 2025: Rising implementation of point-of-care ultrasound in emergency and critical care, with hospitals increasingly deploying rapid diagnostic tools such as eFAST for trauma assessment and immediate clinical decision-making.

- 2025: Expansion of AI-enabled imaging and automation technologies, allowing non-specialists to perform ultrasound scans efficiently, reducing dependency on radiology departments and improving workflow efficiency.

- 2025: Increasing demand for cost-effective and non-invasive diagnostic solutions, supported by growing prevalence of chronic diseases and the need for rapid, bedside diagnostics across healthcare systems.

Market Scope

| Metrics | Details | |

| CAGR | 8.8% | |

| Market Size Available for Years | 2025-2033 | |

| Estimation Forecast Period | 2026-2033 | |

| Revenue Units | Value (US$ Bn) | |

| Segments Covered | Type | Trolley-Based Devices, Handheld Devices |

| Application | Diagnostic, Therapeutic | |

| End-User | Hospitals, Clinics, Ambulatory Surgical Centers, Others | |

| Regions Covered | North America, Europe, Asia-Pacific, South America, and the Middle East & Africa | |

The global point-of-care ultrasound market report delivers a detailed analysis with 70 key tables, more than 66 visually impactful figures, and 195 pages of expert insights, providing a complete view of the market landscape.

Suggestions for Related Report

For more medical device-related reports, please click here