Pleuropulmonary Blastoma Treatment Market Size & Industry Outlook

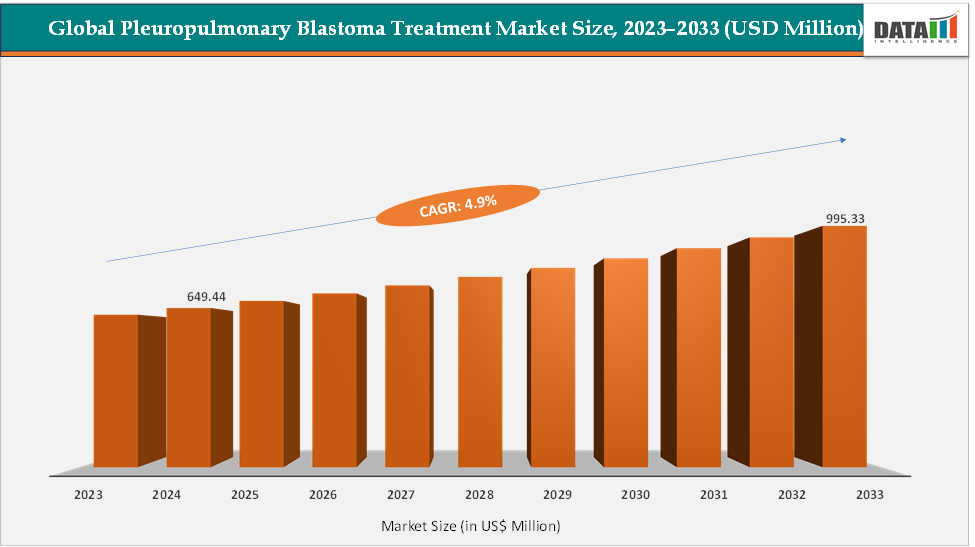

The global pleuropulmonary blastoma treatment market size reached US$ 649.44 Million in 2025 and is expected to reach US$ 995.33 Million by 2033, growing at a CAGR of 4.90% during the forecast period 2026-2033.

The pleuropulmonary blastoma treatment market focuses on therapeutic approaches for managing pleuropulmonary blastoma (PPB), a rare and aggressive pediatric lung cancer primarily affecting infants and young children. The market is niche but evolving, driven by increasing awareness of rare pediatric cancers, advancements in diagnostic technologies, and the growing adoption of multimodal treatment approaches including surgery, chemotherapy, and targeted therapies. Early diagnosis remains critical, as treatment outcomes vary significantly based on disease stage and histological type.

Market growth is supported by ongoing research into genetic factors such as DICER1 mutations, which are associated with PPB, enabling improved risk assessment and personalized treatment strategies. Additionally, increasing investments in rare disease research, supportive regulatory frameworks such as orphan drug designations, and collaborations between research institutions and pharmaceutical companies are contributing to pipeline development. Although challenges such as limited patient population and lack of standardized treatment protocols persist, the market is expected to grow steadily with advancements in precision medicine and pediatric oncology care.

Key Market Highlights

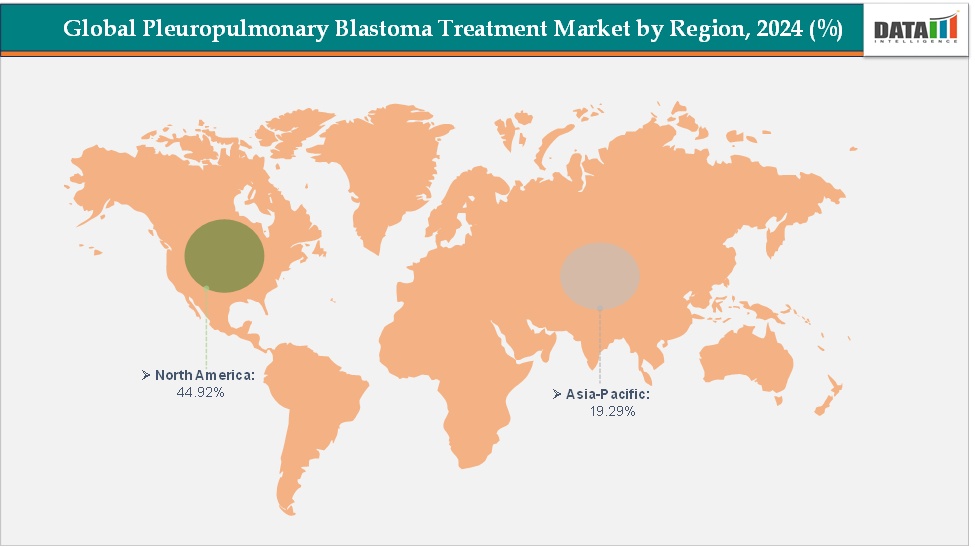

- North America dominates the pleuropulmonary blastoma treatment market with the largest revenue share of 44.92% in 2024.

- The Asia Pacific is the fastest-growing region and is expected to grow at the fastest CAGR of 5.9% over the forecast period.

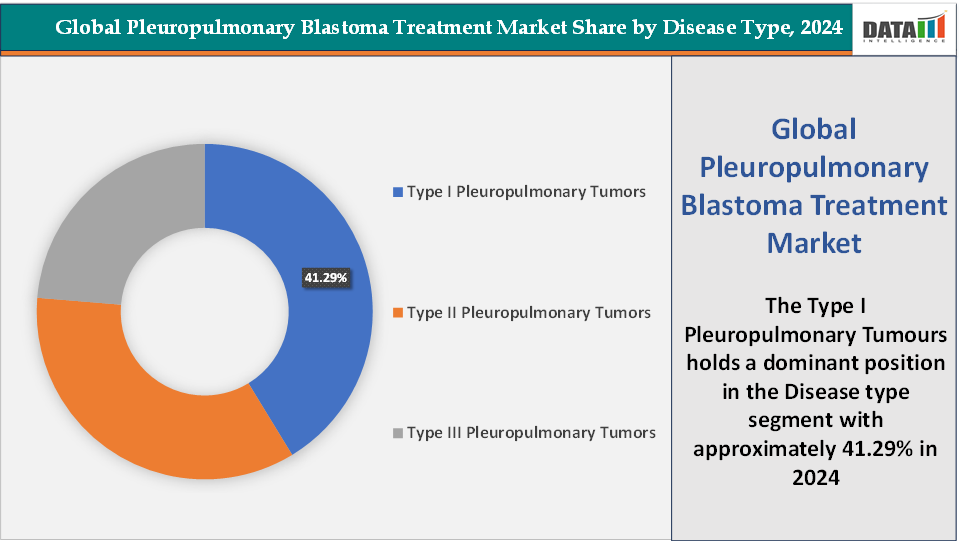

- Based on disease type, the type I pleuropulmonary tumors segment led the market with the largest revenue share of 41.29% in 2024.

- The major market players in the pleuropulmonary blastoma treatment market are Merck & Co., Inc., Pfizer Inc., Baxter, and Eli Lilly and Company, among others

Market Dynamics

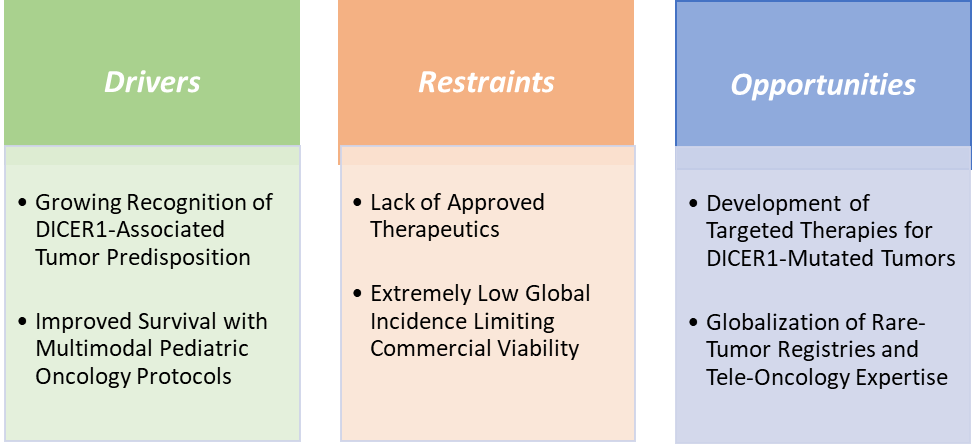

Drivers: Growing recognition of DICER1-associated tumour predisposition is significantly driving the pleuropulmonary blastoma treatment market growth

Growing recognition of DICER1-associated tumor predisposition is significantly accelerating growth in the Pleuropulmonary Blastoma (PPB) treatment market because it is transforming how early detection, diagnosis, and family-level risk management are approached. As more clinicians adopt routine genetic testing for children presenting with lung cysts or unusual thoracic masses, PPB is identified earlier often at Type I, when outcomes are better and intervention rates increase. This broader use of DICER1 testing also triggers cascade testing among family members, expanding the population requiring surveillance imaging, genetic counseling and ongoing specialist follow-up, all of which increase healthcare utilization.

Additionally, heightened understanding of DICER1 biology has encouraged research into targeted and precision therapies, creating new opportunities for biopharmaceutical companies to pursue orphan-drug pathways. Pediatric oncology networks and rare-tumour registries increasingly incorporate DICER1 screening as standard practice, which raises demand for molecular diagnostics, NGS panels, and specialized pediatric oncology services. Altogether, this rising clinical and research focus on DICER1 not only boosts current treatment volumes but also stimulates innovation in future PPB-specific therapeutic options, thereby strongly driving market growth.

Restraints: Lack of approved therapeutics are hampering the growth of the market

The lack of approved, PPB-specific therapeutics significantly hampers market growth because current management relies almost entirely on older, generic chemotherapy regimens such as vincristine, cyclophosphamide, ifosfamide, and doxorubicin. These legacy drugs offer limited commercial differentiation and low revenue potential, discouraging pharmaceutical companies from investing in targeted R&D for such a rare tumor.

Without dedicated therapies, clinicians must use extrapolated protocols from other pediatric sarcomas, which limits innovation and slows the transition to precision medicine. The absence of approved targeted agents also means no premium-priced products or novel mechanisms are entering the market, keeping overall market value relatively stagnant. Furthermore, the ultra-rare incidence of PPB makes it difficult to conduct large-scale trials needed for regulatory approval, creating a cycle where low commercial return further delays drug development. As a result, the market remains dependent on supportive care and conventional cytotoxic drugs, restricting both technological advancement and overall market expansion.

For more details on this report – Request for Sample

Pleuropulmonary Blastoma Treatment Market, Segment Analysis

The global pleuropulmonary blastoma treatment market is segmented based on disease type, treatment type, end-user, and region.

Disease Type: The type I pleuropulmonary tumors segment is dominating in the pleuropulmonary blastoma treatment market with a 41.29% share in 2024

Type I pleuropulmonary tumors dominate the PPB treatment market primarily because they represent the most frequently diagnosed form due to rising awareness, early imaging, and proactive DICER1 genetic screening. These cystic lesions often present in infancy and are now detected earlier through prenatal ultrasounds or early-life chest imaging, significantly increasing the number of Type I cases entering the treatment pathway compared with more advanced Type II and III tumors.

Their management typically involves surgical intervention, which is performed in a high percentage of cases, driving substantial utilization of pediatric thoracic surgery services. Additionally, early detection of Type I disease prompts close long-term surveillance and follow-up imaging to monitor progression to Type II or III, further increasing healthcare engagement and spending.

Because outcomes for Type I PPB are generally favorable when treated promptly, clinicians prioritize early and aggressive management, making this segment more active in terms of procedures, diagnostics, genetic counseling, and multidisciplinary care. As more hospitals adopt DICER1 screening protocols and rare-tumour registries expand, the identification of Type I cases continues to rise, reinforcing its dominant share within the PPB treatment market.

Pleuropulmonary Blastoma Treatment Market, Geographical Analysis

North America is dominating the global pleuropulmonary blastoma treatment market with a 44.92% in 2024

North America dominates the global PPB treatment market due to its well-established pediatric oncology infrastructure, widespread use of advanced diagnostics such as DICER1 genetic testing, and strong integration of multidisciplinary care in leading children’s hospitals. The region benefits from higher awareness of rare pediatric cancers, enabling earlier detection and more frequent identification of Type I PPB cases. Additionally, North America hosts major rare-tumour registries, clinical-trial networks, and research funding mechanisms that support ongoing innovation and ensure broad access to specialized treatment options.

US Pleuropulmonary Blastoma Treatment Market Trends

The United States dominates the global PPB treatment market because it has the most advanced pediatric oncology ecosystem, supported by leading institutions such as St. Jude Children’s Research Hospital, Dana-Farber/Boston Children’s, and Texas Children’s Hospital, which routinely manage rare tumours like PPB. The US also has widespread access to DICER1 genetic testing, enabling earlier detection of cystic lung lesions and increasing the identification of Type I PPB cases compared with most other regions. Robust insurance coverage, specialized thoracic surgery capabilities, and standardized multimodal treatment protocols further strengthen patient access to comprehensive care.

In addition, the US hosts major rare-disease and pediatric cancer registries, which improve clinical decision-making and contribute to higher diagnosis and treatment rates. Strong federal and private research funding promotes the discovery of PPB-related biology and the development of experimental therapies, attracting industry interest despite the disease’s rarity. Overall, the combination of clinical expertise, infrastructure, technology adoption, and research leadership positions the US as the primary driver of the global PPB treatment market.

The Asia Pacific region is the fastest-growing region in the global pleuropulmonary blastoma treatment market, with a CAGR of 5.9% in 2024

The Asia–Pacific region is emerging as the fastest-growing market for pleuropulmonary blastoma (PPB) treatment due to a combination of rapidly improving healthcare infrastructure, expanding access to advanced diagnostics, and growing awareness of rare pediatric cancers. Many countries in the region, including China, India, Japan, South Korea, and Singapore, are making significant investments in next-generation sequencing (NGS), hereditary cancer testing, and pediatric oncology programs, which are leading to increased identification of DICER1 mutations and earlier detection of Type I PPB cases.

As genetic-testing costs continue to fall and government-backed precision-medicine initiatives expand, more children with unexplained lung cysts or thoracic abnormalities are being screened, resulting in higher diagnosis and treatment rates. Meanwhile, Asia–Pacific hospitals are strengthening their pediatric thoracic surgery capabilities and adopting standardized multimodal treatment protocols previously limited to Western centers. The region is also becoming a rising hub for clinical trials in rare tumours due to its large population base, improving regulatory efficiency, and lower trial-execution costs, encouraging global biopharma companies to include Asian sites in PPB-related research.

Europe Pleuropulmonary Blastoma Treatment Market Trends

Europe is experiencing steady growth in the Pleuropulmonary Blastoma (PPB) treatment market due to its highly structured pediatric oncology ecosystem, strong rare-disease policies, and expanding access to advanced molecular diagnostics. The region benefits from well-established collaborative networks such as SIOP Europe and various national rare-tumour registries, which improve early diagnosis, harmonize treatment protocols, and facilitate data sharing across countries. Widespread adoption of DICER1 genetic testing, particularly in the UK, Germany, France, and the Nordics, has increased detection of PPB-associated lung cysts, enabling earlier intervention and contributing to higher treatment volumes.

Europe’s robust healthcare reimbursement frameworks ensure that complex pediatric thoracic surgeries, multimodal chemotherapy regimens, and long-term surveillance are accessible across major tertiary care centers. Additionally, the region’s strong regulatory incentives for orphan drugs encourage research into novel therapies for ultrarare pediatric cancers, drawing participation from academic centers and biotech companies. Growing investment in pediatric precision medicine programs, coupled with improved cross-border healthcare access under EU regulations, further bolsters patient referrals and treatment uptake. Collectively, these factors make Europe a key contributor to the global expansion of PPB treatment services and innovation.

Key Players

Top companies in the pleuropulmonary blastoma treatment market include Merck & Co., Inc., Pfizer Inc., Eli Lilly and Company, Baxter International Inc., F. Hoffmann-La Roche Ltd, Novartis AG, Bristol-Myers Squibb, Company, Johnson & Johnson, AbbVie Inc., Amgen Inc. among others

Key Developments

- In August 2025, the Phase III ARAR2331 clinical trial initiated active patient recruitment to assess treatment approaches involving surgery alone or combined with chemotherapy across Types I, II, and III pleuropulmonary blastoma. This study represents one of the first large-scale collaborative interventional efforts focused on optimizing and standardizing treatment protocols for this rare pediatric cancer.

- In March 2025, a case series on pleuropulmonary blastoma with brain metastasis emphasized the use of multidisciplinary treatment strategies, including surgery, chemotherapy, and radiotherapy, for pediatric patients with central nervous system involvement, highlighting the evolving clinical approaches for managing advanced stages of the disease.

Market Scope

| Metrics | Details | |

| CAGR | 4.9% | |

| Market Size Available for Years | 2023-2033 | |

| Estimation Forecast Period | 2026-2033 | |

| Revenue Units | Value (US$ Mn) | |

| Segments Covered | Disease Type | Type I Pleuropulmonary Tumors, Type II Pleuropulmonary Tumors, and Type III Pleuropulmonary Tumors |

| Treatment Type | Chemotherapy, Radiation Therapy, Targeted Therapy, and Others | |

| End-User | Hospitals, Specialty Clinics, Academic and Research Institutes, and Others | |

| Regions Covered | North America, Europe, Asia-Pacific, South America and the Middle East & Africa | |

The global pleuropulmonary blastoma treatment market report delivers a detailed analysis with 44 key tables, more than 48 visually impactful figures, and 159 pages of expert insights, providing a complete view of the market landscape.

Suggestions for Related Report

For more pharmaceuticals-related reports, please click here