Paper-like Films Market Size

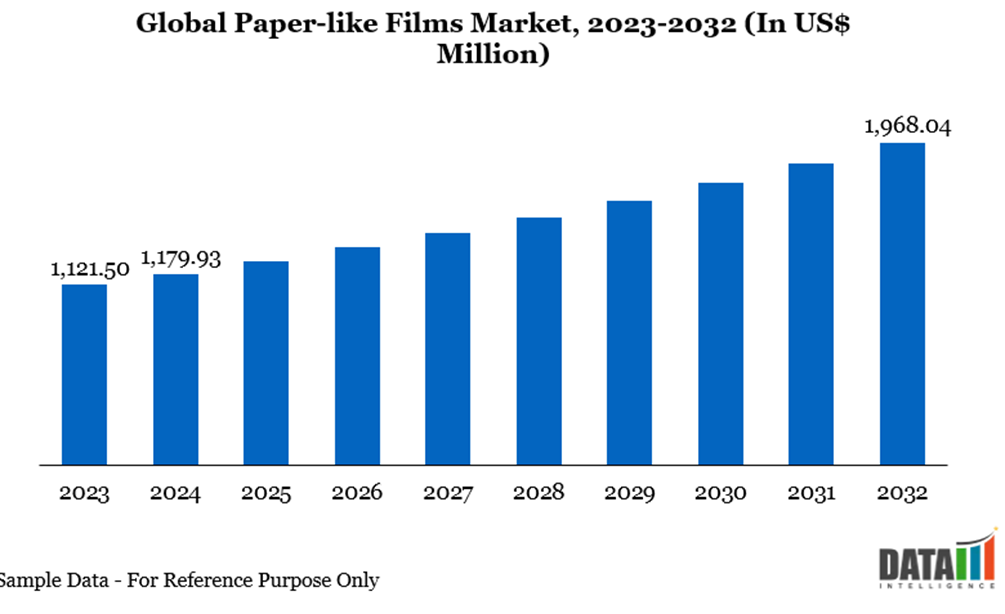

The global paper-like films market reached US$1,179.93 million in 2024 and is expected to reach US$1,968.04 million by 2032, growing at a CAGR of 6.8% during the forecast period 2025-2032. This growth is justified by the rising preference for sustainable and recyclable packaging materials, increasing regulatory emphasis on reducing plastic waste, and the expanding application of paper-like films in food, personal care, and e-commerce sectors.

Paper-like Films Industry Trends and Strategic Insights

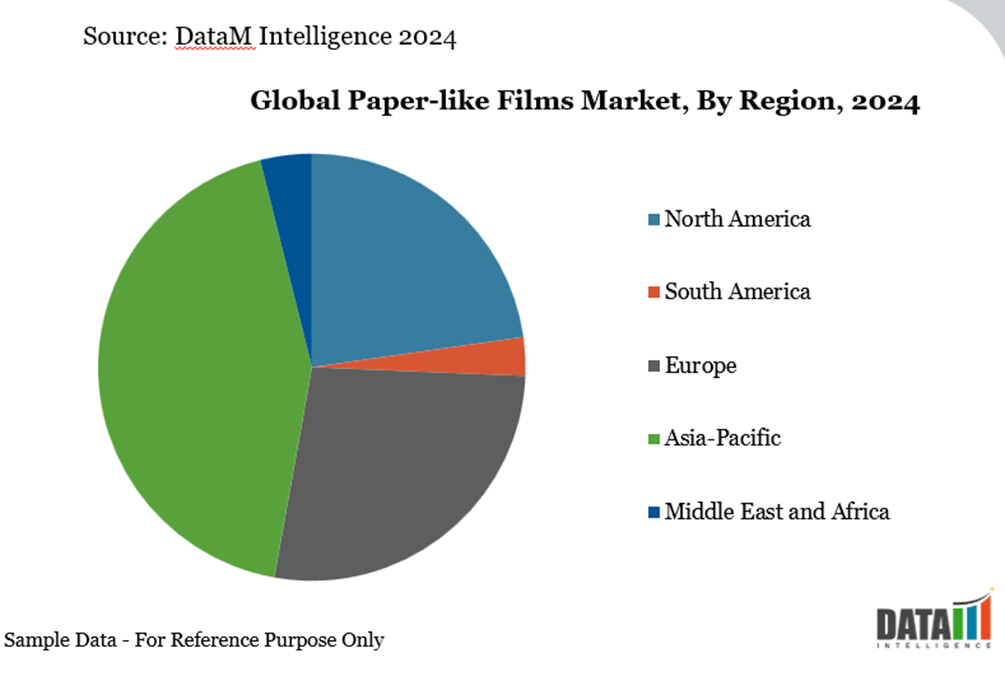

The Asia-Pacific region emerged as the dominant market in the market, capturing the largest revenue share of 42.96% in 2024.

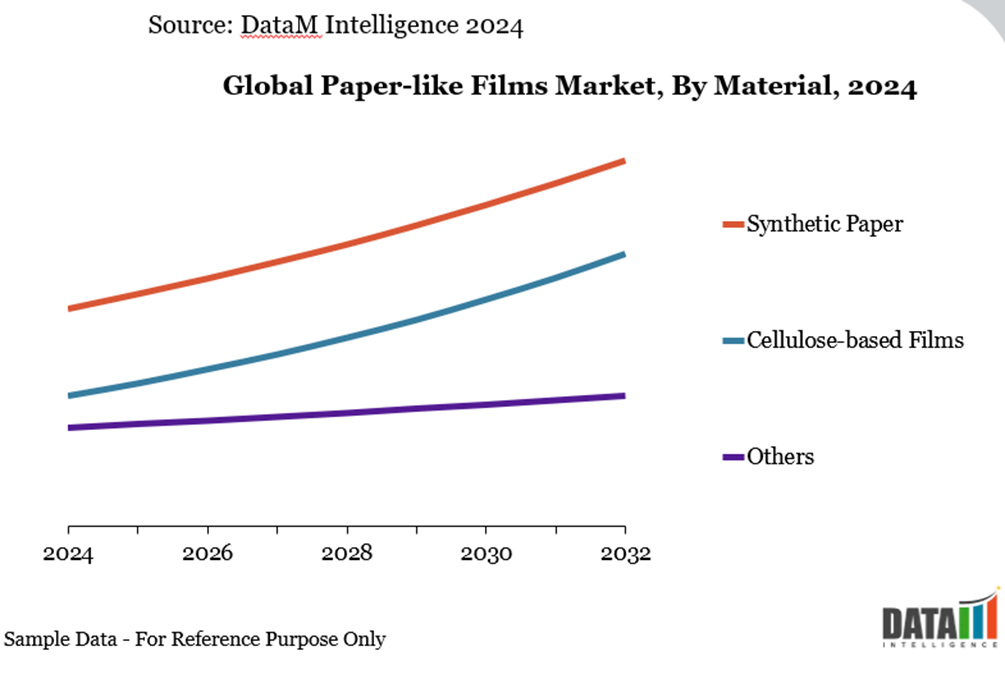

By material, the synthetic paper segment is projected to experience the largest market, registering a significant 58.38% in 2024.

Global Paper-like Films Market Size and Future Outlook

2024 Market Size: US$1,179.93 Million

2032 Projected Market Size: US$1,968.04 million

CAGR (2025-2032): 6.8%

Largest Market: Asia-Pacific

Fastest Market: Asia-Pacific

Market Scope

Metrics | Details |

By Material | Synthetic Paper, Cellulose-based Films, Others |

By Type | Up to 50 microns, 50–150 microns, Above 150 microns |

By Application | Packaging & Labeling, Consumer Electronics, Printing & Publishing, Stationery & Education, Others |

By End-User | Food & Beverages, Electronics & IT, Retail & Consumer Goods, Education & Publishing, Others |

By Region | North America, South America, Europe, Asia-Pacific, Middle East and Africa |

Report Insights Covered

| Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth |

Market Dynamics

Growing Demand for Sustainable Materials

The global market for paper-like films is growing steadily, driven by rising demand for ecologically friendly alternatives and cost-effective packaging solutions. As per the data from the International Trade Centre (ITC), the global packaging industry alone has seen a compound annual growth rate (CAGR) of 4.1% between 2020 and 2025, boosting demand for sustainable materials. This shift is further supported by increasing consumer preference for recyclable and biodegradable options, positioning paper-like films as a viable substitute for conventional plastic-based packaging across multiple industries.

According to research by the US Environmental Protection Agency (EPA), packaging waste contributes significantly to global pollution, with over 70 million tons of packaging materials ending up in landfills each year. This alarming statistic is pushing brands and manufacturers to adopt paper-like films to meet both regulatory requirements and sustainability goals. As industries like food & beverages, retail, and consumer goods embrace eco-friendly packaging, the demand for paper-like films is expected to accelerate, shaping the future of sustainable material adoption.

Segment Analysis

The global paper-like films market is segmented based on material, thickness, application, end-user and region.

Synthetic Paper Leads the Global Paper-like Films Market Due to Superior Durability and Growing Sustainability Innovations

Synthetic paper, a robust, tear- and water-resistant material derived from synthetic polymers such as high-density polyethylene or biaxially oriented polypropylene, has established a considerable presence in the label-making, packaging and specialized printing industries.

HDPE variations, which are valued for their durability and print quality, are particularly popular and widely used in industrial applications. Recent corporate developments are increasingly focused on sustainability. In May 2023, Arjobex America introduced r-Polyart, a synthetic paper containing 30% post-consumer recycled HDPE, which is designed to provide the same water- and tear-resistant performance as conventional Polyart but with better environmental credentials and is recyclable after use.

At the same time, DuPont announced intentions to increase its production capacity for Tyvek synthetic paper, intending to fulfill increased demand in packaging and labeling, particularly in durable, sustainable contexts.

Market signals indicate that synthetic paper is gaining traction. In terms of production, PE-based synthetic paper benefits from scalable manufacturing, but it has raw material and energy limits. Film-based synthetic paper manufacture, which is popular for polyethylene variations, frequently relies on polymer resins, which account for 60-70% of expenses, with worldwide resin price changes adding instability.

Cellulose-Based Films Drive Fastest Growth in the Global Paper-like Films Market Owing to Rising Demand for Compostable and Renewable Packaging Solutions

Cellulose-based films are emerging as the fastest-growing segment in the global paper-like films market, driven by the surge in demand for fully biodegradable and compostable materials. These films, derived from renewable resources like wood pulp and cotton linters, are increasingly favored for their excellent printability, transparency, and eco-friendly profile, making them a preferred choice in food packaging and labeling applications. The growing regulatory push for plastic-free packaging further accelerates adoption, especially in Europe and North America.

Recent developments underscore this momentum. In September 2023, Futamura celebrated the opening of a new state-of-the-art cellulose film production line at its Wigton plant, designed to boost capacity for its flagship NatureFlex compostable films by 25%. This strategic investment highlights the company’s commitment to addressing rising global demand for sustainable packaging. Similarly, industry players like Taghleef Industries have also launched bio-based cellulose films targeting personal care and food packaging. These advancements position cellulose-based films as a critical driver of growth in the paper-like films market.

Geographical Penetration

Asia-Pacific Dominates Global Paper-like Films Market Due to Expanding Packaging Demand and Strong Manufacturing Capabilities

Asia-Pacific paper-like films market is quickly developing as the area strives for sustainable alternatives to plastics. Innovations in material science are critical to this transformation. For example, Indian researchers have developed biodegradable films from waste streams such as sewage sludge and eggshells, which not only improve tensile strength and barrier qualities but also provide soil-friendly breakdown benefits. Such developments underscore the growing importance of circular economy practices, with Asia-Pacific academic institutions and enterprises establishing themselves as early adopters of next-generation paper-like films.

India Paper-like Films Market Outlook

India is experiencing significant growth in the paper-like films market, fueled by the country’s booming packaging sector and increased focus on sustainability. Rising demand for recyclable and eco-friendly materials across food, retail, and e-commerce sectors has accelerated the adoption of synthetic and cellulose-based films. For instance, in March 2022, Cosmo Films Limited, a global leader in packaging films, announced an expansion by setting up a new CPP film production line at Aurangabad with an annual rated capacity of 25,000 MT, involving an investment of about US$15.98 million (₹140 crores). This move aligns with the company’s commitment to sustainability, promoting monolayer CPP and BOPP structures as preferred recyclable solutions for future packaging needs.

China Paper-like Films Market Trends

China is also emerging as a major growth hub for the paper-like films market, supported by strong manufacturing capabilities and increasing sustainability regulations. The country’s rapidly expanding e-commerce sector and government policies targeting plastic reduction are driving demand for eco-friendly films.

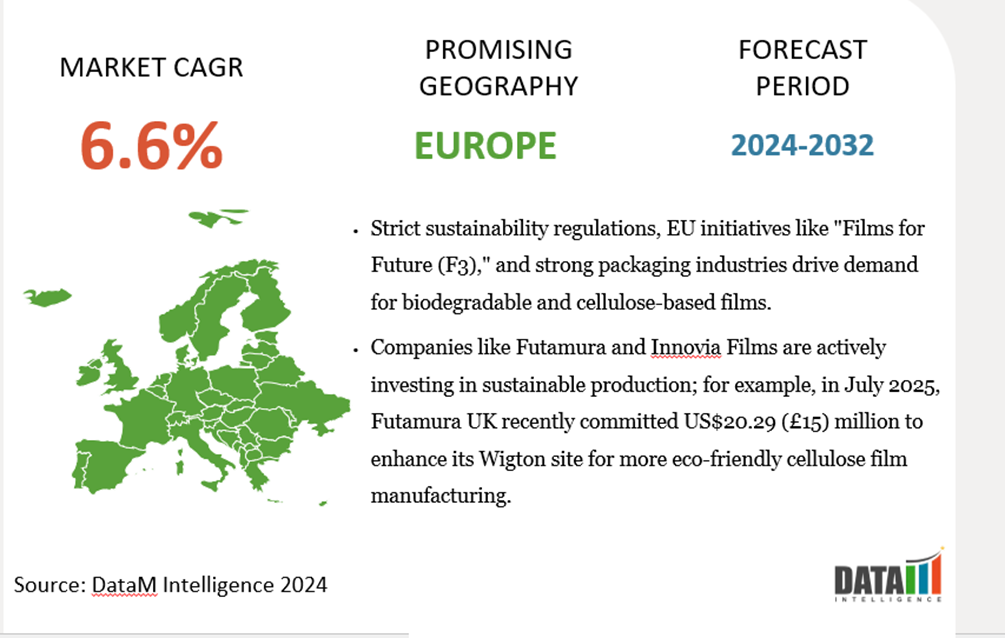

Europe Holds a Significant Share Due to Strict Sustainability Regulations and Strong Demand for Eco-Friendly Packaging Solutions

Europe holds a significant share in the global paper-like films market, primarily driven by stringent environmental regulations and the EU’s push for reducing single-use plastics. The growing demand for sustainable and recyclable packaging solutions in food, beverage, and retail sectors further supports this trend. Leading companies in the region, such as Futamura and Innovia Films, are actively investing in biodegradable and compostable film production. Additionally, increasing consumer awareness and strong adoption of eco-friendly materials across industries position Europe as a key contributor to market growth.

Germany Paper-like Films Market Insights

Germany holds a significant share in the global paper-like films market due to its strong packaging industry, advanced manufacturing capabilities, and commitment to sustainability. The country is actively promoting the use of recyclable and biodegradable materials to comply with EU environmental regulations. Notably, the EU-funded "Films for Future (F3)" initiative—launched in 2022—involves German firms such as Leipa Group GmbH and Kelheim Fibres GmbH, aiming to develop transparent, biodegradable cellulose-based films aligned with the EU’s Packaging Directive. These efforts, combined with growing consumer demand for eco-friendly solutions, solidify Germany’s position as a key market leader in Europe.

UK Paper-like Films Industry Growth

The UK holds a notable share in the global paper-like films market, driven by innovation in sustainable and biodegradable packaging solutions. British firms are increasingly adopting cellulose-based and eco-friendly films for food and specialty packaging. Government initiatives and collaborations with EU-funded projects further support research and commercialization of advanced paper-like films. Growing consumer preference for recyclable and compostable alternatives also strengthens the UK’s market presence.

Sustainability Analysis

Traditional wood-pulp paper production is resource-intensive and contributes to deforestation, whereas synthetic paper offers longer life cycles, durability, and recyclability within existing PE and PP waste streams. Incorporating recycled materials, such as Arjobex’s r-Polyart made from 30% post-consumer HDPE, further reduces carbon footprints while maintaining performance.

European and Japanese producers are exploring bio-based PE resins from renewable sources like sugarcane ethanol, and regulatory frameworks such as the EU Single-Use Plastics Directive encourage mono-material, recyclable solutions. Innovations in solvent-free inks, digital printing, and recyclable coatings demonstrate that synthetic paper effectively integrates performance with sustainability, making it a key solution for food labeling, pharmaceuticals, and durable tags in global packaging markets.

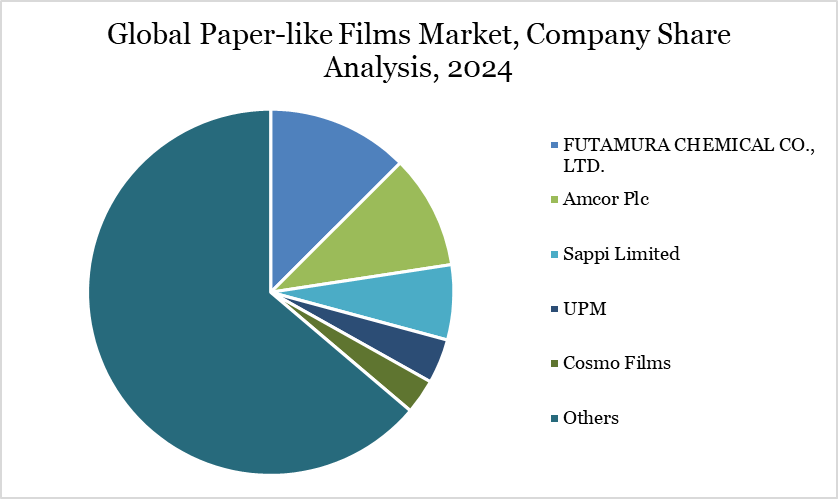

Competitive Landscape

The competitive landscape of the global paper-like films market is characterized by a mix of established polymer producers, specialty film manufacturers and regional players expanding into sustainable materials.

Companies such as FUTAMURA CHEMICAL CO.,LTD., Amcor Plc, Sappi Limited, UPM and Cosmo Films lead in synthetic paper innovations, offering durable, recyclable solutions tailored for packaging, labeling and printing.

Competition is intensifying as regional converters in Asia-Pacific invest in lower-cost production capacities to serve local e-commerce and food packaging demand, while European firms emphasize compliance with EU recyclability regulations.

Partnerships with printing technology companies and packaging converters are becoming a strategic differentiator in response to sustainability-driven market shifts.

Key Developments

In March 2025, VTT Technical Research Centre of Finland invested US$1.76 (€1.5) million into its CelluloseFilms pilot facility. This expansion is designed to scale up the production of renewable cellulose alternatives, particularly for replacing plastic films in food packaging.

Why Choose DataM?

Data-Driven Insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. This approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. This personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. These insights complement and go beyond what is typically available in generic databases.

Target Audience 2024

Manufacturers/ Buyers

Industry Investors/Investment Bankers

Research Professionals

Emerging Companies

Suggestions for Related Report