Global Natural Gas Engine Market Size

The Natural Gas Engine Market is estimated to reach USD 5.99 Billion in 2025 and is projected to grow to USD 10.65 Billion by 2035, registering steady growth at a CAGR of 5.9% during the forecast period from 2026 to 2035.

The global natural gas engine market is expanding steadily as industries, utilities and transport fleets worldwide pursue cleaner, more flexible energy solutions. As of 2024, natural gas provided about 23% of total global primary energy consumption, with demand continuing to rise due to its lower carbon intensity compared with coal and oil. Global natural gas production reached nearly 4.1 trillion cubic meters, up by over 2% from the previous year, supported by capacity expansion in the US, Russia and Qatar. This steady supply is fueling broader use of natural gas engines across distributed power generation, combined heat and power (CHP), industrial operations and heavy-duty transportation.

In power generation, natural gas engines are increasingly deployed for on-site and backup applications. More than 70 GW of global installed CHP capacity now operates on reciprocating gas engines, reflecting their high efficiency (often exceeding 45–48%) and flexible load response. National energy programs in the US, Japan and several EU countries encourage the use of gas-based distributed power to enhance grid reliability and reduce carbon emissions. The US Energy Information Administration (EIA) notes that gas-fired reciprocating engines contributed to over 15% of new distributed energy capacity additions in 2024, emphasizing their role in modern energy systems. In transportation, demand is accelerating due to stricter emission norms and cost advantages over diesel.

Globally, there are over 30 million natural gas vehicles (NGVs) in operation, consuming roughly 75 billion cubic meters of gas annually. Major adoption is seen in China, India and parts of Europe where governments provide tax incentives and infrastructure support for CNG and LNG vehicles. Technological advances, such as high-compression spark-ignited engines and hybrid systems capable of running on renewable natural gas (RNG) or hydrogen blends, are further enhancing efficiency and reducing lifecycle emissions.

Natural Gas Engine Market Industry Trends and Strategic Insights

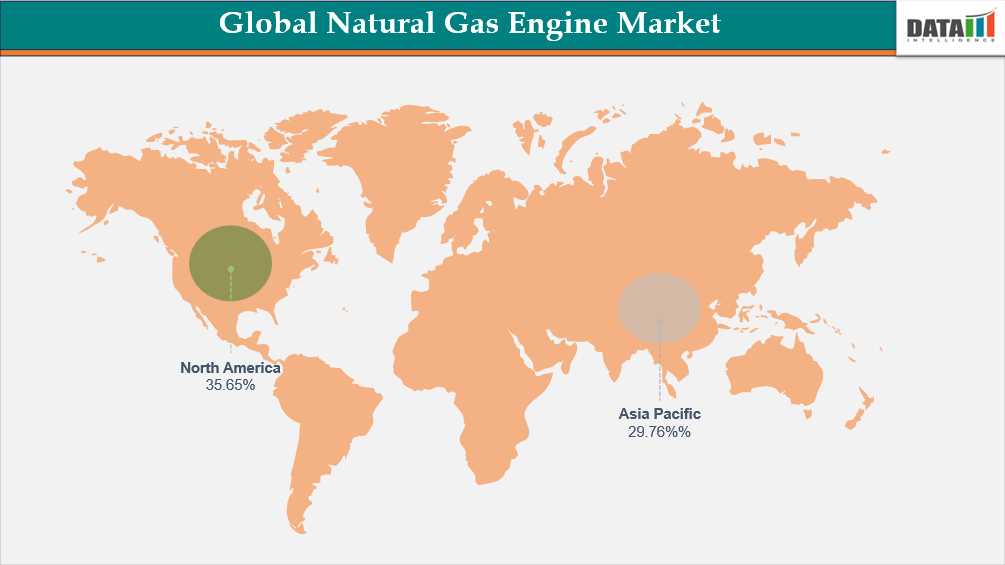

- North America leads the global natural gas engine market, capturing the largest revenue share of 35.65% in 2024.

- By engine type segment, spark-ignited engines led the global natural gas engine market, capturing the largest revenue share of 41.23% in 2024.

Natural Gas Engine Market Scope

| Metrics | Details |

| By Engine Type | Spark Ignited Engines, Dual-Fuel Engines, Internal Combustion Engines, Microturbines, Others |

| By Power Output | 0.5 MW – 5 MW, 6 MW – 10 MW, 10 MW Above |

| By Horsepower Range | Up to 1000 HP, 1001 HP – 2000 HP, Above 2000 HP |

| By Application | Power Generation / Cogeneration, Industrial Mechanical Drive, Natural Gas Gensets, Decentralized Energy Generation, Others |

| By End Consumer | Utilities, Oil & Gas, Wastewater Treatment Plants, Hospitals, Marine, Others |

| By Region | North America, South America, Europe, Asia-Pacific, Middle East and Africa |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth |

For More Detailed Information, Request for Sample

Key Takeaways

- The natural gas engine market is experiencing steady expansion driven by rising demand for low-emission power generation, distributed energy systems, and industrial decarbonization initiatives.

- Spark-ignited engines dominate the market due to their high efficiency, lower emissions, fast start-up capability, and strong suitability for CHP (combined heat and power) and decentralized energy applications.

- Power generation and industrial mechanical drive applications account for the majority of demand, supported by increasing energy security concerns and grid reliability needs.

- Asia-Pacific is emerging as the fastest-growing region due to rapid industrialization, infrastructure expansion, and increasing adoption of cleaner fuel alternatives.

- North America leads the market due to abundant natural gas supply, strong pipeline infrastructure, and favorable regulatory frameworks supporting gas-based power generation.

- Growing LNG exports, data center energy demand, and distributed generation investments are strengthening long-term market fundamentals.

- Increasing focus on reducing carbon emissions is positioning natural gas engines as a transitional technology between diesel-based systems and renewable energy solutions.

Analyst Viewpoint

The natural gas engine market is evolving from a conventional industrial power segment into a strategic pillar of the global energy transition. Historically driven by cost efficiency and fuel availability, the market is now increasingly influenced by decarbonization mandates, grid flexibility requirements, and distributed energy expansion.

A major structural shift is the growing role of natural gas engines in decentralized energy systems, where industries, utilities, and commercial facilities deploy localized generation to reduce dependency on centralized grids. This trend is accelerating alongside rising electricity demand from data centers, manufacturing hubs, and electrification initiatives.

Technological advancements in dual-fuel engines, high-efficiency combustion systems, and emissions control technologies are improving performance and regulatory compliance. At the same time, integration with renewable natural gas (RNG) and hydrogen blending is expanding long-term sustainability potential.

In the future, the market is expected to transition toward hybrid energy ecosystems, where natural gas engines operate alongside renewables, storage systems, and digital grid management platforms. Companies that integrate efficiency, flexibility, and low-carbon operation capabilities will gain competitive advantage.

Market Dynamics

Increasing Demand for Low-Emission Transportation Alternatives

The rising demand for low-emission transportation alternatives is one of the most significant factors driving the global natural gas engine market. As countries intensify efforts to decarbonize the transport sector, which accounts for nearly 24% of global CO₂ emissions, natural gas engines are emerging as a key transitional technology bridging the gap between conventional diesel engines and full electrification.

Liquefied natural gas (LNG) and compressed natural gas (CNG) vehicles offer 20–25% lower CO₂ emissions and up to 90% reduction in particulate matter and nitrogen oxides (NOx) compared to traditional diesel vehicles. This environmental advantage is accelerating adoption in heavy-duty trucking, municipal fleets and public transport systems, especially in regions with established gas infrastructure.

In North America, the number of natural gas-powered vehicles exceeds 175,000 units, with more than 1,200 fueling stations across the US and Canada. The US Department of Energy’s Clean Cities program reports that heavy-duty CNG and LNG trucks are being rapidly adopted by logistics and waste management companies to comply with tightening emission mandates and to reduce operating costs. In Europe, natural gas vehicles (NGVs) surpassed 1.4 million units in 2024, with strong growth in Italy, Germany and Spain driven by Euro VI emission standards and tax incentives promoting biomethane use.

Global Natural Gas Engine Market, Segmentation Analysis

The global natural gas engine market is segmented based on engine type, power output, horsepower range, application, end-user and region.

Spark-Ignited Engines Lead Market with 41.23% Share Driven by efficiency, low emissions, and versatile applications.

The global demand for spark-ignited (SI) natural gas engines is steadily expanding as industries and utilities accelerate their transition to cleaner and more flexible energy systems. Natural gas consumption worldwide rose by nearly 2.7% in 2024, reaching its highest level to date, driven by its availability, cost competitiveness and lower carbon intensity compared to coal and oil. This surge in gas use supports increasing deployment of SI engines, which are widely applied in distributed power generation, combined heat and power (CHP) systems and commercial fleet operations due to their quick start-up capabilities, high efficiency and relatively low maintenance requirements.

In distributed generation, SI engines are increasingly preferred for small- and mid-scale projects that require dependable power and heat supply near consumption sites. Governments in North America, Europe and Asia-Pacific are promoting CHP installations as part of energy-efficiency and grid-resilience programs. In US, over 80 GW of installed CHP capacity currently uses reciprocating gas engines, while Europe continues to add smaller decentralized systems supported by clean energy subsidies. These policies enhance the adoption of SI gas engines, which provide rapid response and high thermal efficiency compared to gas turbines at lower loads.

Dual-Fuel Engines Growing Driven by Fuel Flexibility and Lower Operational Costs in Industrial and Marine Applications

Dual-fuel engines are gaining traction in the global natural gas engine market due to their ability to operate on both gas and diesel, offering significant fuel flexibility. They help reduce operational costs and emissions, making them attractive for industrial, marine, and power generation applications. Investments are increasing as manufacturers innovate to improve efficiency and meet stricter environmental regulations. This trend reflects the broader shift toward versatile and cleaner energy solutions worldwide.

Natural Gas Engine Market, Geographical Penetration

DOMINATING MARKET:

North America Leads Natural Gas Engine Market with 35.65% Share Driven by Robust Gas Infrastructure and Supportive Clean Energy Policies

North America holds the largest share in the global natural gas engine market due to its abundant natural gas reserves and well-developed infrastructure for extraction, distribution, and storage. The region’s strong focus on reducing emissions and adopting cleaner energy solutions has driven demand for natural gas engines across industrial, transportation, and power generation sectors. Supportive government policies and incentives further encourage the use of natural gas technologies. Additionally, the presence of major engine manufacturers and advanced R&D capabilities strengthens North America’s market dominance.

US Natural Gas Engine Market Outlook

The US holds a major share in the global natural gas engine market due to its abundant gas resources and robust production and distribution infrastructure. Stationary gas-engine applications, including distributed generation and industrial cogeneration, are growing as utilities and large energy users seek flexible assets to complement renewables. Natural gas-fired power contributes over 43% of US electricity generation while accounting for a similar share of CO₂ emissions, highlighting its critical role in the energy mix. Rising regulatory scrutiny, with 2022 gas-system emissions at 209.7 million metric tons CO₂-equivalent, is driving cleaner and more efficient engine adoption. EPA initiatives, such as new CO₂ limits and published emission factors for gas engines, further support upgrades, retrofits, and market growth.

Canada Natural Gas Engine Market Trends

Canada holds a strong position in the natural gas engine market due to its sizable natural gas reserves and well-developed energy infrastructure. The country is increasingly adopting stationary gas-engine applications, such as distributed generation and industrial cogeneration, to support reliable and flexible power, especially in remote and industrial regions. Natural gas plays a key role in Canada’s energy mix, offering lower emissions compared to other fossil fuels and aiding the transition toward cleaner energy. Government policies and incentives promoting reduced greenhouse gas emissions encourage the deployment of efficient natural gas engines. Additionally, ongoing investments in engine technology and maintenance support a growing market for both new installations and retrofits.

FASTEST GROWING MARKET:

Asia-Pacific’s Natural Gas Engine Market Driven by Industrial Growth and Supportive Policies

The Asia-Pacific region holds a significant share in the global natural gas engine market. Rapid industrialization and urbanization have increased the demand for efficient energy solutions. Supportive government policies and incentives for cleaner fuel adoption further boost growth. Additionally, expanding power generation and transportation sectors contribute to higher natural gas engine deployment.

India Natural Gas Engine Market Insights

India presents significant opportunities in the natural gas engine market, with potential investments worth US$67 billion as the share of natural gas in the energy mix is projected to rise from 6.7% to 15% by 2030 (Invest India). The country is witnessing increasing demand for cleaner and efficient energy solutions across the power generation, industrial, and transportation sectors. Supportive government policies, including incentives for gas-based infrastructure and the adoption of alternative fuels, are driving market growth. Rapid urbanization, coupled with the expansion of the gas pipeline network, further strengthens the market outlook for natural gas engines in India.

China Natural Gas Engine Market Industry Growth

According to the IEA, natural gas accounted for 7.9% of China’s total energy supply in 2023, highlighting its increasing role in the country’s energy mix. The total natural gas supply, including production and imports minus exports or storage, reached 13,349,463 units. This growing reliance on natural gas is driving demand for natural gas engines across power generation, industrial, and transportation sectors. Supportive government policies promoting cleaner fuels and low-emission technologies further enhance market growth in China.

Regulatory Analysis

Natural gas engines used in stationary and distributed generation applications are regulated primarily through emission standards that define allowable limits of NOx, CO, NMHC/VOC, formaldehyde, and methane slip. In the United States, the key regulation is EPA New Source Performance Standards (NSPS) for Stationary Spark-Ignition Engines (40 CFR Part 60, Subpart JJJJ), which mandates NOx limits of 1.0 g/bhp-hr for lean-burn engines and 2.0 g/bhp-hr for rich-burn units. California’s CARB Distributed Generation (DG) Certification Program is even stricter, requiring NOx levels as low as 0.07 lb/MWh, pushing OEMs to offer advanced lean-burn combustion and catalyst-based aftertreatment.

In Europe, the Medium Combustion Plant Directive (MCPD – Directive 2015/2193/EU) governs natural gas engines in the 1–50 MWth category. It sets explicit NOx limits of 190 mg/Nm³ for new gas-fired engines and requires compliance with CO and formaldehyde thresholds. Additionally, the EU Stage V regulation affects mobile and smaller modular gas-engine systems, driving adoption of low-sulfur fuels, oxidation catalysts and closed-loop lambda-control systems. Europe is also drafting methane-slip reduction targets, which directly impact natural gas engine design and combustion optimization.

In Asia, China’s GB 13271-2014 and associated regional standards impose NOx limits ranging from 50–150 mg/m³ for gas-fired distributed energy systems, significantly influencing OEM exports to the region. India regulates stationary gas engines under CPCB-II norms, focusing on NOx and CO emissions, and favoring natural gas engines over diesel for urban and industrial applications. Japan mandates compliance with the Air Pollution Control Law, with strict NOx thresholds for CHP installations used in commercial and industrial facilities.

Additionally, Global renewable gas policies such as the US Renewable Fuel Standard (RFS), California’s Low Carbon Fuel Standard (LCFS), and the EU’s Renewable Energy Directive (RED II), provide financial and compliance-driven incentives for the use of biogas and renewable natural gas (RNG). These regulatory frameworks are pushing manufacturers to design engines with higher methane-number tolerance, enhanced corrosion resistance and materials compatible with variable biogas compositions.

Competitive Landscape

- The global natural gas engine market is moderately consolidated, with competition centered on efficiency, emissions performance, and digital engine optimization.

- Key players such as Cummins Inc., Caterpillar, Wärtsilä and Rolls-Royce plc dominate the market through strong R&D capabilities and diversified application portfolios.

- Manufacturers are increasingly focusing on fuel-flexible and low-emission technologies, including biogas/RNG compatibility and hydrogen-ready designs, in response to tightening environmental regulations and evolving customer sustainability requirements.

- Strategic partnerships, localized production, and long-term service models are shaping competitive dynamics, particularly in Asia-Pacific and North America, as companies expand capacity and target growing demand in industrial CHP and distributed generation applications.

Key Developments

- June 2026 – Cummins expanding high-efficiency natural gas engine portfolio

Cummins Inc. advanced development of next-generation natural gas engines focused on lower emissions, improved fuel efficiency, and enhanced performance for heavy-duty transportation and power generation applications. - May 2026 – Caterpillar strengthening gas-powered power generation solutions

Caterpillar expanded its natural gas engine systems for distributed energy and backup power applications, supporting growing demand for cleaner and more reliable on-site energy solutions. - April 2026 – Wärtsilä advancing hybrid and gas-based power technologies

Wärtsilä enhanced flexible engine platforms integrating natural gas with hybrid energy systems, supporting grid stability and renewable energy integration in industrial and utility sectors. - April–June 2026 – Rising adoption of cleaner fuel engines in industrial applications

Companies such as Rolls-Royce plc continued investments in high-efficiency gas engines designed for marine, power generation, and industrial use, driven by stricter emission regulations and decarbonization goals.

Investment & Funding Landscape

The investment and funding landscape for natural gas engines is expanding as both private and public capital flows into cleaner combustion technologies within the broader natural gas sector, with venture rounds and major OEM investments supporting capacity growth and innovation. Market reports show increasing capital expenditures and strategic investments by engine manufacturers to scale production and meet rising global demand for lower‑emission power and transport solutions.

| Company | Investment/Funding | Year | Details | |

| Chevron | US$1 Billion Funding | February, 2025 | US energy major Chevron is set to invest $1 billion in India to establish its largest engineering and innovation excellence centre (ENGINE) in Bengaluru, aimed at supporting global operations and energy projects. The facility will focus on advanced engineering, digital modelling, AI-driven subsurface analysis, predictive maintenance, and carbon capture solutions, while creating 600 jobs by the end of 2025. | |

What Sets This Global Natural Gas Engine Market Intelligence Report Apart

- Latest Data & Forecasts – Comprehensive, up-to-date insights and projections through 2032. Coverage includes global value by engine type, power output, horsepower range, application, end-user segments. Scenario forecasts with region-level splits (North America, Europe, Asia-Pacific, South America, Middle East and Africa) and sensitivity to factors such as regulatory reclassification and raw-material costs.

- Regulatory Intelligence – Actionable analysis of regulatory frameworks that materially affect Natural Gas Engine commercialization, revenue by country, allowable label claims, permitted doses, import/export controls and advertising restrictions.

- Competitive Benchmarking – Standardized profiling and benchmarking of leading pharma and nutraceutical players, contract manufacturers and e-commerce specialists active in the market.

- Geographic & Emerging Market Coverage – Region-by-region market sizing, growth drivers, reimbursement dynamics, cultural/consumer behavior and mrket access considerations. Focus on high-growth or regulatory-uncertain markets.

- Actionable Strategies – Identify opportunities for launching innovative products, while leveraging strategic partnerships and supply chain integration for maximum ROI.

- Pricing & Cost Analysis – In-depth assessment of price trends, raw material costs and sustainability-driven cost efficiencies across regional markets.

- Expert Analysis – Insights from industry experts such as clinical sleep specialists, regulatory affairs professionals and key manufacturing companies.

Investment Hotspots & White Space Opportunities

The natural gas engine market offers strong investment potential across energy infrastructure, distributed generation, and clean transition technologies.

High-Growth Investment Areas

•High-efficiency spark-ignited gas engines

• Dual-fuel and flexible fuel engine systems

• CHP and cogeneration power plants

• Distributed energy generation systems

• Gas genset manufacturing and deployment

• Industrial backup power systems

• LNG-based power infrastructure

• Data center power generation systems

White Space Opportunities

• Hydrogen-ready natural gas engines

• AI-optimized distributed energy systems

• Carbon capture-integrated gas engine systems

• Renewable natural gas (RNG)-powered engine platforms

• Hybrid gas + battery microgrid systems

• Smart grid-connected engine ecosystems

• Low-emission retrofit engine technologies

• Digital twin-based engine performance optimization

The strongest value creation opportunity lies in decarbonized natural gas engines integrated with digital energy management systems, enabling flexible and low-carbon distributed power solutions.