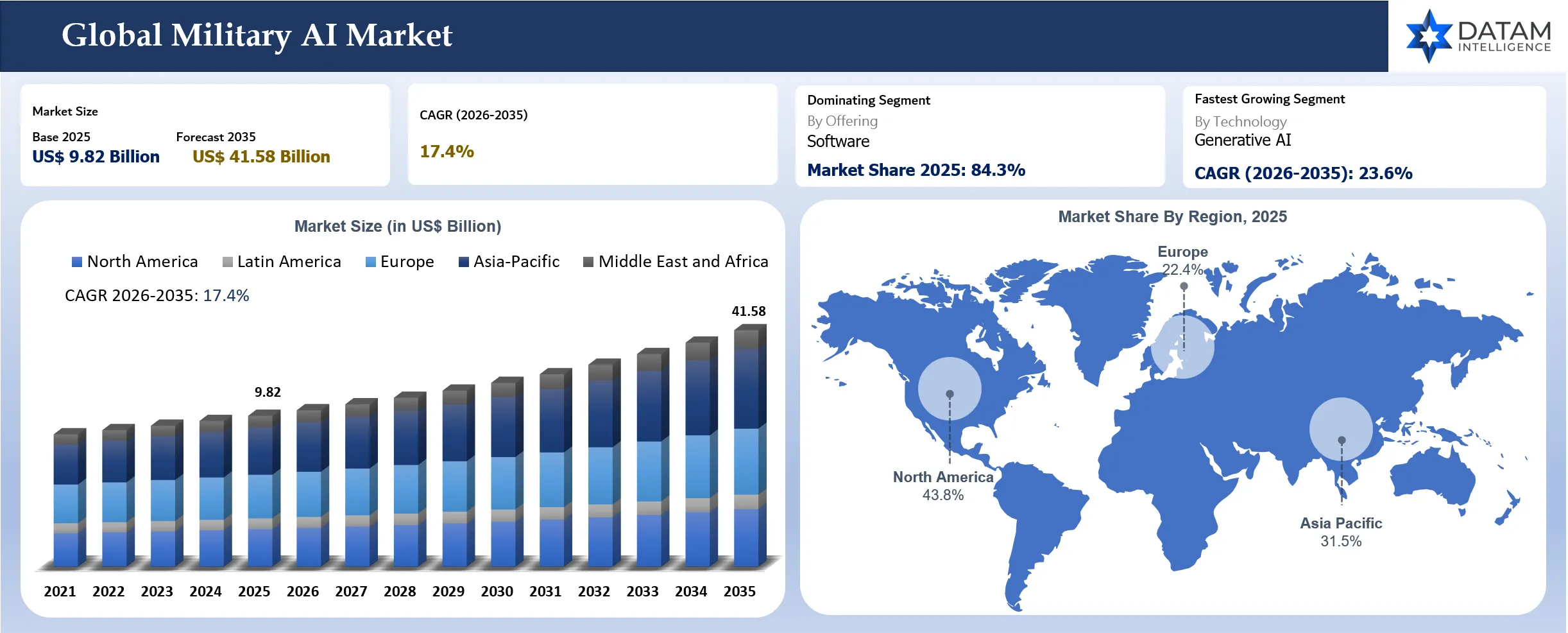

Military AI Market Size

The global military AI market reached US$ 9.82 Billion in 2025 and is expected to reach US$ 41.58 Billion by 2035, growing at a CAGR of 17.4% during 2026 to 2035. Demand has moved well beyond research labs and image-recognition pilots. Defense buyers now look for mission software, autonomous platforms, tactical edge processing, sensor fusion, EW support, cyber defense, and decision support that can work inside classified networks with limited connectivity.

Defense ministries are moving away from stand-alone algorithms and toward operational systems that combine data infrastructure, model governance, secure compute, training pipelines, human-machine interfaces, and rugged hardware. Spending is strongest across ISR exploitation, command decision support, uncrewed teaming, counter-drone workflows, predictive maintenance, cyber defense, and simulation. Buyers now ask whether a solution can improve after field feedback instead of judging it only by lab accuracy.

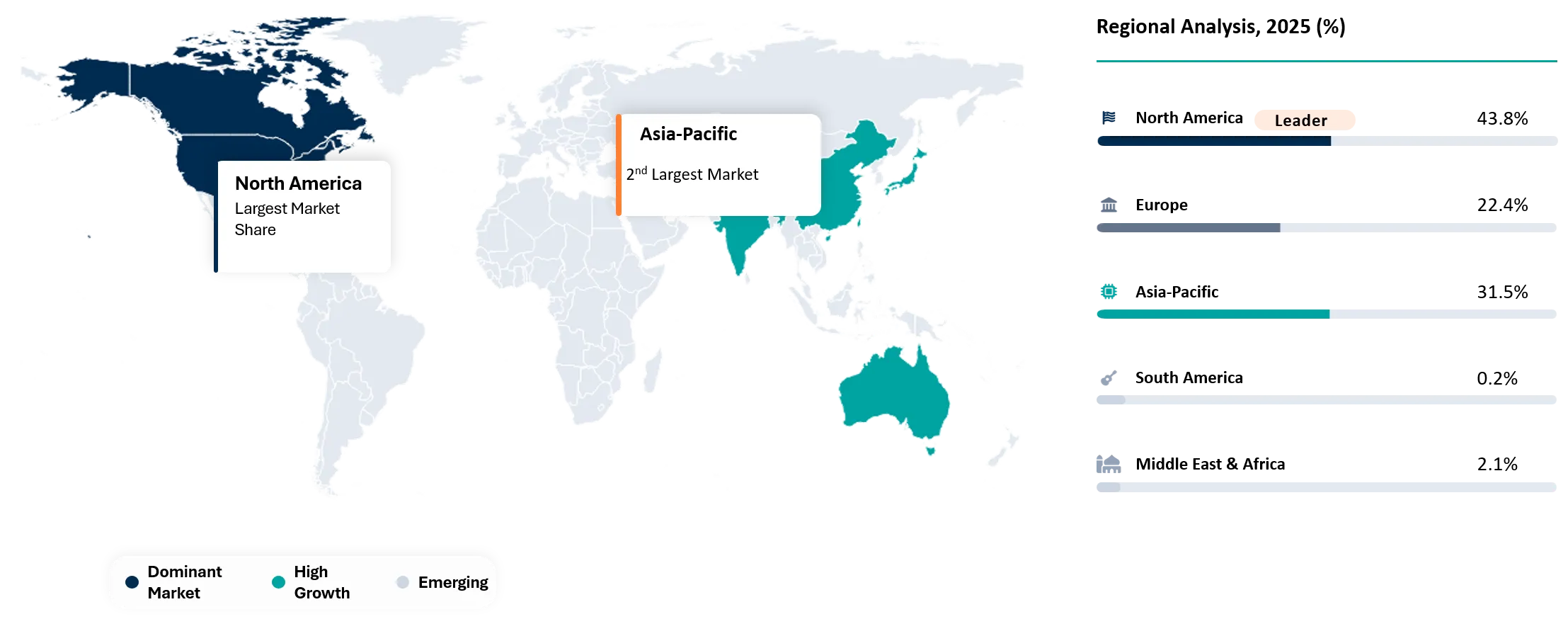

North America remains the largest region because U.S. defense software budgets, CDAO-led adoption, replicator-style autonomy programs, and a deep venture-backed supplier base keep demand active. Europe is moving faster as NATO interoperability, Ukraine battlefield lessons, and sovereign technology policies push allied governments toward domestic autonomy and AI-enabled defense suppliers. Competitive strength will depend on accredited deployment pathways, classified data handling, model traceability, edge performance, legacy C2 integration and proof from live exercises.

Latest Investment Activity and Partnerships In Military AI and Defense Technology

Military AI and defense technology investment accelerated sharply in 2026, with DataM Intelligence reporting more than US$ 14.6 billion invested across 107 venture rounds in military, national security and law enforcement categories during the first five months of 2026. Large disclosed rounds from Anduril Industries, Shield AI, Saronic Technologies, True Anomaly, Sierra Space and Vast accounted for a major share of the disclosed funding momentum.

- Anduril Industries raised US$5.0 billion in Series H funding in May 2026 at a reported US$61.0 billion valuation, supporting autonomous defense systems, AI command and control, drones and scaled defense manufacturing.

- Shield AI announced US$2.0 billion in financing in March 2026, including US$1.5 billion Series G funding and US$500 million preferred equity, at a US$12.7 billion post-money valuation to scale aircraft autonomy, simulation software and Hivemind-enabled defense platforms.

- Saronic Technologies announced US$1.75 billion Series D funding in March 2026 at a US$9.25 billion valuation to accelerate autonomous maritime platforms, unmanned naval vessels and shipbuilding capacity.

- True Anomaly raised US$650 million in Series D financing in April 2026 at a reported US$2.2 billion valuation to support space security, autonomous spacecraft and national-security space systems.

- Sierra Space closed US$550 million in Series C funding in March 2026 at a reported US$8.0 billion valuation to expand defense-tech space systems, national-security space infrastructure and production capacity.

- Vast raised US$500 million in March 2026, including US$300 million Series A equity and US$200 million debt, to accelerate Haven space station production and government-linked space infrastructure opportunities.

- Havoc AI raised US$100 million in Series A funding in May 2026 to scale all-domain collaborative autonomy for defense and commercial mission environments.

- Picogrid raised US$45 million in Series A funding in May 2026 to build an open integration layer connecting military sensors, autonomous platforms, AI tools and command-and-control systems.

- BAE Systems and Scale AI announced a 2026 strategic relationship to accelerate agentic AI capabilities for mission environments and operational platforms.

- RTX and Shield AI announced a 2025 partnership to integrate Hivemind into selected RTX defense products including loitering munitions and sensors.

Military AI Market Scope

| Metrics | Details | |

| Market Size In 2025 | US$ 9.82 Billion | |

| Market Size By 2035 | US$ 41.58 Billion | |

| CAGR During 2026 To 2035 | 17.4% | |

| Largest Region In 2025 | North America, 43.8% market share in 2025 | |

| Fastest Growing Region | Europe, 17.9% CAGR between 2026 and 2035 | |

| Key Regional Shift | Europe is expected to increase from 22.4% market share in 2025 to 27.5% market share by 2035 | |

| Leading Offering | Software | |

| Fastest Growing Offering | Services | |

| Leading Technology | Computer Vision | |

| Fastest Growing Technology | Generative AI | |

| Leading Platform | Airborne | |

| Fastest Growing Platform | Naval | |

| Leading Application | ISR | |

| Fastest Growing Application | C-UAS | |

| Market Maturity | Early Growth Stage | |

| Key Buying Question | Which AI stack can be trusted, accredited and updated at mission speed inside classified and contested environments? | |

| By Offering | Software, Hardware, Services | |

| By Technology | ML (Machine Learning), Computer Vision, NLP (Natural Language Processing), Edge AI, Generative AI, Sensor Fusion, Swarm Intelligence, Reinforcement Learning, Predictive Analytics | |

| By Platform | Airborne, Land, Naval, Space, Cyber, Multi-Domain | |

| By Application | ISR (Intelligence, Surveillance and Reconnaissance), C2 (Command and Control), Autonomous Systems, Target Recognition, Cybersecurity, Simulation and Training, Logistics, Predictive Maintenance, EW (Electronic Warfare), C-UAS (Counter Unmanned Aircraft Systems) | |

| By Deployment | Cloud, On-Premise, Edge Tactical AI, Hybrid Secure Cloud | |

| By Operator | Army, Navy, Air Force, Space Forces, Intelligence Agencies, Homeland Security | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Key Takeaways

- North America led with 43.8% share in 2025 as U.S. programs absorbed commercial autonomy, data platforms and battlefield software faster than most allied markets.

- Europe is the fastest-growing region as NATO digital transformation, EU defense funding and Ukraine-driven operational learning accelerate sovereign AI and autonomous systems demand.

- Software is the largest offering because value sits in data integration, model orchestration, autonomy control, AI-assisted workflows and classified deployment environments.

- Services are growing fastest because defense customers need data preparation, accreditation support, red teaming, model monitoring, mission engineering and legacy system integration.

- Computer vision leads adoption because ISR exploitation, target recognition, full-motion video analysis and counter-drone detection are immediate operational needs.

- C-UAS is the fastest-growing application because low-cost drones have become a daily burden for air bases, ships, logistics hubs and forward units.

- Procurement is moving from experimentation to fieldable intelligent mass across attritable air systems, autonomous surface vessels, edge AI kits and AI-enabled battle networks.

Why Does This Report Matter In 2026?

Budget and doctrine are converging around autonomy. SIPRI reported world military expenditure of US$2.718 trillion in 2024 with the steepest annual increase since at least 1988. Large defense budgets are no longer flowing only into conventional platforms. A larger share is being redirected toward software-defined force multipliers that shorten sensing, decision and response timelines.

Operational lessons from Ukraine, the Red Sea, the Gulf region and Indo-Pacific deterrence planning have changed buyer behavior. Forces now treat small uncrewed systems, AI-assisted ISR and counter-drone automation as operational necessities instead of experimental tools. Mission teams want systems that can train in simulation, deploy at the edge, and improve after every exercise or engagement cycle.

Supplier power is shifting as well. Established primes still control major platform integration, classified programs and support networks. Venture-backed companies are gaining influence where speed, modularity and software ownership matter. Leading vendors are forming partnerships that combine prime contractor accreditation with startup autonomy stacks and commercial development velocity.

Strategic Indicators For Military AI

High Regulation Impact

Regulation impact is high because defense buyers must balance faster autonomy with rules on human judgment, international humanitarian law, data rights, export controls and classified cybersecurity. NATO’s revised AI strategy emphasizes safe and responsible adoption. The U.S. Department of Defense also requires responsible, equitable, traceable, reliable and governable AI principles. Compliance slows uncontrolled deployment but favors suppliers with model documentation, audit trails, test evidence and clear human-machine control design. Systems linked to targeting, electronic attack or autonomous movement face the toughest scrutiny. Maintenance and logistics tools can move faster, but programs still need secure data access, cyber approval and lifecycle monitoring before enterprise adoption.

High Investment Activity

Investment activity is unusually high because defense technology has moved from a niche venture category into a large-scale capital formation theme. Crunchbase data shows more than US$ 14.6 billion invested across 107 venture rounds in military, national security and law enforcement categories during the first five months of 2026, already surpassing the previous full-year record. Large disclosed rounds from Anduril Industries, Shield AI, Saronic Technologies, True Anomaly, Sierra Space and Vast show that capital is concentrating around autonomy, AI-enabled command workflows, space security, maritime robotics and defense manufacturing.

Funding is not only moving into software dashboards. Venture and strategic investors are backing vertically integrated defense companies that combine AI software, mission autonomy, rugged hardware, manufacturing capacity and platform-level deployment. Anduril’s US$ 5.0 billion Series H, Shield AI’s US$ 2.0 billion financing and Saronic’s US$ 1.75 billion Series D indicate that investors are prioritizing companies able to convert AI into deployable defense systems rather than standalone algorithms.

Capital intensity is rising across space and maritime defense as well. True Anomaly, Sierra Space and Vast show that national-security space infrastructure is becoming a major investment pillar, while Saronic highlights the shift toward autonomous shipbuilding and unmanned maritime operations. The market is therefore developing two supplier models: software-first companies that embed AI into command, simulation and integration workflows and hardware-software companies that deliver autonomous platforms with built-in mission intelligence.

Supply Chain Disruption

Supply disruption now reaches beyond semiconductors into secure compute, sensors, inertial navigation components, RF components, propulsion, batteries and qualified manufacturing capacity. Defense AI systems need GPUs, edge accelerators, rugged processors and secure storage that meet export and cybersecurity conditions. Naval autonomy and attritable aircraft also depend on engines, composite structures and test ranges. Program timelines can slip when commercial chips change generation faster than defense certification cycles. Suppliers with modular hardware abstraction, multiple compute options and long-term component roadmaps can reduce buyer risk. Local manufacturing mandates and allied content rules are likely to shape vendor selection through 2035.

Pricing Volatility

Pricing volatility is shaped by GPU availability, classified integration labor, model validation cost, test range access and the gap between prototype and fielded unit economics. Defense customers often see attractive pilot pricing before lifecycle cost rises through cybersecurity hardening, red teaming, integration, operator training and sustainment. Attritable systems create another pricing challenge. Buyers want low unit cost while expecting survivability, autonomous navigation, secure communications and EW resilience. Vendors that separate recurring software cost from expendable hardware cost will have stronger negotiating power. Procurement teams will increasingly compare cost per mission effect instead of cost per platform.

Procurement Pressure

Procurement pressure is rising because commanders want rapid deployment while acquisition offices require evidence, cybersecurity approval and sustainment planning. AI solutions must fit contract vehicles, data rights rules, classified network policies and operator training timelines. Long buying cycles can make models stale before deployment. Governments are responding through rapid capability offices, framework contracts and modular open systems approaches. Vendors still need to prove that field updates will not create uncontrolled mission risk. Buying teams will reward suppliers that provide continuous testing, auditable model release notes, system safety cases and integration support without forcing full platform replacement.

New Technology Adoption

Technology adoption is strongest in computer vision, edge inference, sensor fusion, simulation, autonomous navigation, AI-assisted C2, counter-drone workflows and predictive sustainment. Generative AI is entering defense through staff work, intelligence summarization, training content, software engineering and decision support rather than fully autonomous lethal action. Edge AI matters because communications-denied operations require local perception and mission execution. Simulation is becoming a certification layer because developers can test thousands of scenarios before live trials. The most durable opportunity sits in mixed autonomy where humans supervise multiple systems while algorithms handle sensing, routing, prioritization and operator workload reduction.

Regional Expansion Opportunity

Regional expansion opportunity is strongest in Europe and allied Indo-Pacific markets. European governments need sovereign systems that reduce reliance on foreign-controlled data and model stacks. Poland, Germany, France, the Nordics and the Baltic region are raising demand for drones, counter-drone systems, air defense decision support and battlefield software. Japan, Australia, South Korea and India are investing in maritime awareness, space resilience, cyber defense and autonomous systems built for contested regional environments. Suppliers entering these markets need local partnerships, export approval, data localization and interoperability with national command architectures instead of a simple U.S. style sales model.

Government Policy Support

Government policy support is rising through defense innovation units, NATO digital transformation, the European Defence Fund, U.S. Replicator-style procurement and national defense industrial strategies. Policy support is not unconditional. Programs increasingly require responsible AI governance, interoperability and supply chain resilience. Public funding is also bringing non-traditional suppliers into defense ecosystems and reducing dependence on a small group of incumbents. The market is becoming more open but still tightly controlled. Vendors that understand both software scaling and defense compliance will be better positioned than companies that treat military sales as standard enterprise software expansion.

New Product Launches

- March 2026: Thales launched SkyDefender as an AI-enabled air and missile defense architecture that combines sensors, effectors and C2 software for multi-layer protection against drones, missiles and complex aerial threats.

- April 2025: Shield AI unveiled a V-BAT block upgrade with Hivemind autonomy, SATCOM capability and a heavy-fuel engine configuration for tougher maritime and expeditionary operating conditions.

- April 2025: True Anomaly announced Jackal for geosynchronous orbit and cislunar space as a maneuverable autonomous spacecraft designed for space superiority missions and payload-flexible operations.

- March 2025: Leonardo DRS introduced the AIP (Artificial Intelligence Processor) product line for rugged battlefield computing, real-time tactical processing and integration into Army ground vehicle fleets.

- December 2024: Helsing unveiled HX-2 as an AI-enabled strike drone integrated with the Altra reconnaissance-strike software platform for coordinated ISR and strike workflows.

AI Impact Analysis

AI is changing defense value creation by moving intelligence from centralized analysis cells to distributed mission layers. Computer vision now screens video feeds, radar tracks and satellite images at a scale human teams cannot sustain. Sensor fusion tools combine imagery, signals, acoustic inputs and platform telemetry into a common operational picture. Decision aids prioritize alerts and give operators more time for judgment instead of manual data sorting.

Generative AI is creating a second impact layer in staff workflows and intelligence analysis. Secure models can summarize reports, draft plans, compare courses of action and support software development. Military adoption will move slower than commercial adoption because hallucination, data leakage and prompt-injection risk carry greater consequences in classified environments. Value will come from controlled models grounded in authoritative data and supervised by trained operators.

Autonomy is the most commercially important impact area. AI-enabled navigation, perception and mission planning allow one operator to supervise more platforms. Attritable aircraft, autonomous surface vessels, robotic ground systems and space vehicles become more useful when they can adapt to GPS denial, jamming and sensor uncertainty. Strong suppliers will prove performance in degraded conditions instead of relying on clean test environments. AI also affects maintenance and readiness. Predictive analytics can forecast component failure and improve aircraft, vehicle and ship availability. Digital twins and simulation reduce test burden and support training. Defense buyers will favor solutions that connect with existing maintenance systems and produce explainable recommendations instead of black-box risk scores.

Disruption Analysis

The most important disruption is the shift from exquisite platform scarcity to intelligent mass. Low-cost drones, autonomous boats and software-defined payloads are forcing militaries to think in distributed effects. High-end aircraft, ships and missiles remain essential, but commanders increasingly need large numbers of lower-cost systems that can sense, deceive, jam, relay or strike under human oversight. A second disruption is the rise of neo-primes. Companies such as Anduril, Shield AI, Saronic, Helsing and True Anomaly are attracting capital because they build faster than the traditional defense cycle. They are not replacing every prime contractor role. The related real impact is pressure on incumbents to partner, adopt open architectures and shorten development loops.

A third disruption is the move toward data-centric defense procurement. Model performance depends on quality data, labeling, scenario libraries and operational feedback. Governments with clean mission data and secure developer access can improve faster. Governments that keep data siloed will struggle to scale AI despite large budgets. Regulatory scrutiny could also disrupt commercialization. Civil society concern around algorithmic targeting and autonomy will remain intense. Suppliers need human-control design, traceability and auditability as core product features. Companies that treat compliance as a late-stage documentation task will face slower approvals.

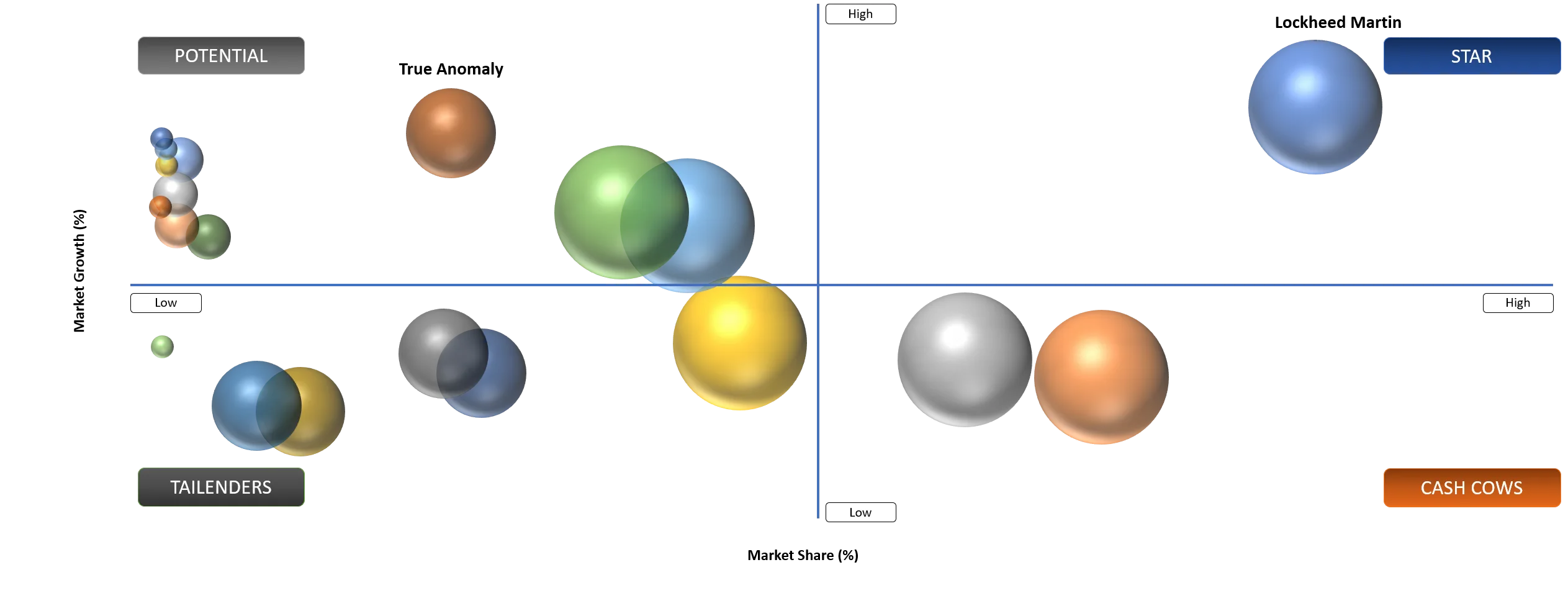

BCG Matrix: Company Evaluation

Star

Star players include Anduril Industries, Inc., Shield AI, Inc., Palantir Technologies Inc., Helsing GmbH, Saronic Technologies, RTX Corporation, Lockheed Martin Corporation, Northrop Grumman Corporation, BAE Systems plc and Thales S.A. The related strength comes from mission software, autonomy platforms, integration capability, government trust, classified program access and active product deployment. Stars are especially visible in AI-enabled ISR, autonomous aircraft, tactical edge software, counter-drone workflows, space defense and air defense decision support. Buyers view these companies as credible because they combine product maturity with operational testing, partner ecosystems or prime-level support capacity.

Potential

Potential companies include True Anomaly, Inc., Sierra Space Corporation, Vast Space LLC, HavocAI Inc., Picogrid, Inc., Saab AB, Leonardo S.p.A., Elbit Systems Ltd., General Atomics and L3Harris Technologies, Inc. Growth depends on converting specialized technical positions into scalable defense programs. Space domain awareness, autonomous maritime systems, tactical mesh infrastructure, rugged edge computing, AI-assisted fighter systems and robotic autonomy create strong upside. Near-term challenge is not technology visibility alone. Each company must prove repeatable production, mission integration, export readiness and sustainment models that can meet large government buying cycles.

Military AI Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact | Demand Concentration | Impacted Use Case | Strategic Impact |

Replicator-Style Programs Pull Autonomy Into Formal Procurement | High | U.S., Europe and Indo-Pacific Allies | Autonomous Systems and C2 | Accelerates field procurement of attritable autonomy |

Contested ISR Needs Faster Edge Target Recognition | High | North America, Europe, Israel and Asia-Pacific | ISR and Target Recognition | Expands computer vision and edge AI spending |

AI Battle Networks Reduce Operator Load Across Domains | Medium To High | Global Allied Forces | Multi-Domain Operations | Supports integrated battle networks and operator workload reduction |

Driver: Replicator-Style Programs Pull Autonomy Into Formal Procurement

Replicator-style procurement has changed the speed expectation for autonomous systems. The U.S. approach to accelerating all-domain attritable autonomous capabilities shows that defense buyers want systems fielded in useful quantities instead of showcased as isolated prototypes. Similar thinking is spreading through allied programs where mass, lower-cost survivability and rapid updates matter more than traditional platform perfection.

The driver is grounded in battlefield reality. Drone saturation, missile inventory limits and maritime surveillance gaps have created a need for distributed systems that operate across air, surface, subsurface, land and space domains. AI is central because humans cannot manually control every asset in a dense operational environment. Autonomy, mission planning and sensor fusion become the control layer that turns many small systems into coordinated effects.

Suppliers benefit when they prove operational readiness through exercises, not slideware. Procurement teams ask for ruggedness, communications-denied performance, cyber hardening, open interfaces and training support. Companies that deliver both autonomy software and mission hardware can capture larger contract value, while software-only vendors can scale through prime partnerships and platform integration.

The main commercial implication is a shift from pilot budgets to program budgets. Once a defense organization creates inventory targets for autonomous platforms or AI-enabled workflows, funding moves from innovation offices to procurement and sustainment accounts. Such movement creates longer revenue visibility for vendors that can survive certification, security review and field support obligations.

Restraint Impact Analysis

| Restraint | Drag On Market Growth | Primary Impact Area | Impacted Use Case | Strategic Impact |

Classified Data Access Slows Model Validation | High | Model Development and Accreditation | ISR, C2 and Target Recognition | Raises validation cost and slows deployment |

Human Control Rules Delay Autonomous Strike Approvals | High | Autonomous Strike and EW | Autonomous Systems | Limits full automation and requires human oversight design |

Restraint: Classified Data Access Slows Model Validation

Model performance depends on access to mission data, but sensitive defense data is hard to share. Imagery, signals, electronic order-of-battle information, mission logs and platform telemetry may sit inside classified environments with strict access controls. Commercial AI developers often have strong model talent but limited ability to train and validate on the data that matters most in operations.

Data access constraints create hidden cost. Vendors need secure facilities, cleared staff, compliant development environments and approved data pipelines. Government teams need labeling standards, audit trails and release processes. Programs can lose momentum when technical teams cannot move data quickly enough to test model behavior across real threat conditions.

The restraint favors incumbents and well-funded startups that can build secure infrastructure. Small vendors may have excellent algorithms but struggle to obtain accreditation and customer data access. Buyers can reduce friction through synthetic data, simulation environments and controlled challenge datasets. Real-world validation remains essential for mission-critical use cases where false positives and false negatives carry operational risk.

Commercial impact appears in longer sales cycles and higher integration services revenue. Customers may buy a tool only after extensive red teaming and validation. Vendors that package compliance, data engineering and model monitoring into the offer will reduce buyer uncertainty and shorten repeat deployments.

Segment Analysis

AI-Enabled ISR Is Becoming the Command Layer of the Modern Kill Chain

ISR is the most visible demand pocket because defense forces are overwhelmed by data from drones, satellites, radar, acoustic sensors, cyber feeds and open-source inputs. The operational problem is no longer collection alone. The bottleneck is turning data into trustworthy decisions at mission speed. AI-enabled ISR helps teams detect objects, classify patterns, flag anomalies and prioritize human review.

Computer vision dominates current ISR workflows. Full-motion video exploitation, satellite image screening, change detection, maritime vessel recognition and counter-drone tracking are natural fit areas because image and sensor data arrive continuously. Tools that reduce analyst burden without removing human judgment are easier to adopt than systems that claim fully autonomous targeting.

Edge processing is reshaping ISR deployment. Drones, ground sensors and ships cannot always stream high-bandwidth data to cloud systems. Edge AI compresses the decision cycle by processing data near the sensor. Tactical systems must run on rugged hardware, tolerate heat and vibration and keep functioning during jamming or intermittent links. Generative AI adds value after detection. Intelligence teams can use controlled models to summarize feeds, connect events, draft briefs and compare hypotheses. Defense-grade generative tools must be grounded in approved data and constrained by clear permissions. The greatest risk is an eloquent system that produces confident but unsupported conclusions.

Commercial winners in ISR will combine detection accuracy, workflow integration and evidence traceability. A useful system must show why it flagged an object, what data supported the alert and how confident the model is. Such evidence gives commanders confidence to act while keeping accountability inside the human chain of command. Procurement teams also evaluate interoperability. ISR tools must connect with C2 systems, geospatial platforms, mission planning software and allied data standards. Vendors that lock customers into isolated dashboards will lose ground to modular platforms that improve the existing operational picture.

Computer Vision For ISR and Target Recognition

Computer vision remains the foundation for AI-enabled ISR because cameras, EOIR sensors, radar imagery and satellite feeds create enormous review loads. Algorithms can identify vehicles, vessels, air defense systems, launchers, drones and unusual movement patterns faster than manual teams. Human analysts still decide meaning and action, but automation reduces time spent on empty frames and routine screening.

Military computer vision differs from commercial object recognition. Adversaries use camouflage, decoys, smoke, clutter, weather, night operations and electronic deception. Models must handle low-resolution data and unfamiliar conditions. Training requires diverse examples and operational feedback from exercises or live deployments. Synthetic data helps but cannot replace field validation.

Buyers prefer computer vision systems that explain detections with overlays, confidence scores and source metadata. Analyst trust improves when the tool shows a traceable chain from raw data to alert. Vendors that support rapid retraining after new enemy tactics appear will outperform static model suppliers. The strongest growth will come from linking computer vision to action workflows. A detection becomes more valuable when connected to routing, cueing, track management, fire support review, electronic warfare response or counter-drone engagement. Such integration raises switching cost and makes AI part of the mission system rather than a plug-in analytics feature.

Edge Tactical AI For Contested Operations

Edge tactical AI is gaining priority because contested forces cannot rely on clean cloud connectivity. Datalinks may be jammed, satellites may be unavailable and latency may be unacceptable. Edge systems allow drones, vehicles, sensors and command posts to process data locally and continue operating under degraded conditions.

Hardware constraints define the economics. Rugged edge compute must balance power draw, heat, size, weight and cybersecurity. High-performance GPUs can be difficult to place on small drones or battery-powered sensors. Vendors that optimize models for smaller processors and support multiple chip options can reduce supply and lifecycle risk.

Edge deployment also changes update governance. A model deployed on a tactical platform may need quick updates after a threat changes, but every update must be verified for safety and cyber integrity. Defense customers need release management, rollback capability and audit logs. Model operations become a sustainment function rather than a one-time software installation.

Revenue opportunity is strong because edge AI connects software, hardware and services. Suppliers can sell rugged compute units, autonomy modules, model integration, training and long-term sustainment. Customers will compare vendors based on mission reliability under stress rather than theoretical benchmark performance.

Geographical Penetration

North American Military AI Market Trends

North America led the market with a 43.8% share in 2025 because the U.S. defense ecosystem combines the world’s largest defense budget, advanced commercial AI suppliers, strong venture capital and established prime contractors. The U.S. Department of Defense’s 2023 Data, Analytics and AI Adoption Strategy created clearer enterprise direction around decision advantage, data quality and scaled use across warfighting and business functions.

The U.S. is also the most important country for rapid autonomy procurement. Replicator-style programs, CDAO activity, DIU engagement and service-level experiments are pulling autonomy into practical fielding. Demand is strongest in ISR, autonomous aircraft, counter-drone systems, maritime autonomy, space defense and secure AI platforms for classified use. U.S. buyers are also creating more opportunities for non-traditional suppliers through rapid contracting vehicles.

Canada’s market is smaller but strategically relevant for NORAD modernization, Arctic surveillance, cyber defense and allied data sharing. Canadian defense organizations are likely to prioritize AI-enabled domain awareness, maritime monitoring and secure cloud adoption. Local industry opportunities will depend on partnerships with U.S. and European suppliers instead of large domestic platform programs alone.

Mexico plays a more limited role in military AI but has relevance in border security, public safety, maritime monitoring and infrastructure protection. Adoption will be selective and more closely tied to homeland security and surveillance applications than high-end combat autonomy. Suppliers entering Mexico need to account for budget limits and public sensitivity around AI surveillance.

U.S. Military AI Market Landscape

The U.S. is the decisive demand center because it combines mission need, budget scale and a supplier ecosystem that includes both primes and defense technology startups. The FY 2026 DoD budget request highlighted a major topline increase and continued emphasis on advanced capabilities. AI adoption benefits from broader U.S. efforts in software acquisition, data strategy and autonomy programs. Operational priorities are clear. The U.S. needs AI-enabled ISR for global sensing, autonomy for Indo-Pacific deterrence, C-UAS for base defense, cyber AI for network defense and predictive maintenance for readiness. Strong vendors solve one of two problems: they reduce operator workload inside a mission workflow or allow a smaller force to control more autonomous assets.

Procurement risk remains meaningful. Responsible AI principles, classified data handling, cybersecurity accreditation and congressional oversight create a demanding path to scale. U.S. buyers increasingly expect explainability, human oversight, test evidence and open architecture. Vendors that fit these requirements without slowing product iteration will earn the largest programs. The U.S. also shapes the global market through export permissions and allied interoperability. A system adopted by U.S. forces gains credibility with allies, but export controls can restrict scale. Companies that design exportable variants and partner with allied manufacturers can expand faster while staying inside policy constraints.

Europe Military AI Market Outlook

Europe is the fastest-growing region because defense spending, Ukraine lessons and sovereignty concerns are reshaping procurement. NATO’s revised AI strategy emphasizes safe and responsible adoption while building an ecosystem with industry, academia and non-traditional suppliers. The European Defence Fund supports collaborative defense technologies and gives smaller firms a route into multinational programs.

Germany, France, the UK, Italy, Poland and Nordic countries are important buyers. Demand is focused on air defense, counter-drone systems, battlefield software, autonomous aircraft, electronic warfare, cyber defense and AI-enabled training. European customers often require local data control and industrial participation. Suppliers must adapt to national security review and export controls inside Europe.

Ukraine has become a live learning environment for drone warfare, electronic warfare adaptation and software-defined tactics. European suppliers are absorbing lessons around jamming resistance, fast update cycles, unit-level autonomy and low-cost scalable systems. Such learning is likely to influence procurement specifications across NATO members for the next decade. European competition is strengthening. Helsing has become a prominent software-defined defense company and works across AI strike drones, reconnaissance-strike software and fighter AI collaboration. Thales, Leonardo, BAE Systems and Saab are integrating AI into established defense platforms. The region will reward suppliers that combine sovereign control, interoperability and rapid field testing.

Asia-Pacific Military AI Market Analysis

Asia-Pacific demand is shaped by maritime competition, air defense needs, border surveillance, cyber threats and domestic defense industrial policies. China, India, Japan, Australia and South Korea are the most important countries. Regional buyers want AI-enabled ISR, autonomous maritime systems, space surveillance, electronic warfare and decision support for complex air and sea environments.

China has large state-backed AI and defense capability, but foreign supplier access is limited. Commercial opportunity for outside vendors is stronger in allied and partner markets such as Japan, Australia, India and South Korea. Export controls and strategic alignment will shape which technologies can move across borders.

India is a high-potential market because it combines large military modernization needs with domestic manufacturing and digital capability. Demand is likely around border surveillance, autonomous drones, predictive maintenance, cyber defense, electronic warfare and naval domain awareness. Local partnership, technology transfer and Make in India alignment will be central to market entry. Australia, Japan and South Korea are investing in advanced deterrence, maritime surveillance and allied interoperability. Japan deserves separate attention because it needs AI-enabled maritime domain awareness, air defense support, space security and unmanned systems that can operate across island chains and contested sea lanes. Japanese buyers emphasize reliability, documentation and integration with U.S. alliance systems.

Japan Military AI Market Growth

Japan is a high-value market where AI adoption is tied to regional deterrence, maritime monitoring and air defense. The country faces large surveillance demands across surrounding waters and airspace. AI-enabled sensor fusion can help operators manage radar, satellite, maritime patrol and drone feeds with faster prioritization. Japan’s industrial base is likely to favor trusted partnerships and controlled technology transfer. Domestic primes and electronics suppliers can play a strong role in integrating AI into command systems, unmanned platforms and maintenance workflows. Foreign vendors need local partnership and clear cybersecurity alignment.

Space and cyber are also important. Japan’s dependence on secure communications, satellite services and resilient logistics creates opportunity for AI-assisted anomaly detection, orbital awareness and cyber defense. Solutions must meet high expectations for safety, reliability and documentation. Public trust matters in Japan. Autonomous strike systems may face stronger political scrutiny than defensive sensing, maintenance and cyber applications. Suppliers should lead with human-centered decision support and defensive resilience before pushing more sensitive autonomy propositions.

Middle East and Africa Military AI Market Outlook

Middle East demand is shaped by air defense, drone threats, border security, maritime chokepoints and protection of energy infrastructure. UAE, Saudi Arabia and Israel are key markets. Israel has advanced AI-enabled defense technologies and a deep operational feedback loop from active security conditions. Gulf buyers are investing in C-UAS, surveillance, cyber defense and autonomous systems to protect critical assets. UAE is a particularly important adoption market because it combines defense modernization, local industrial strategy and a willingness to partner internationally. AI-enabled border security, maritime monitoring, air defense C2 and unmanned systems fit national priorities. Data sovereignty and local integration will affect supplier selection.

Saudi Arabia is investing heavily in defense localization and high-end systems. Military AI opportunities include air defense, predictive maintenance, training simulation, cyber defense and autonomous surveillance. Vendors need local partnerships and long-term industrial participation instead of transactional sales. Africa remains selective and budget-constrained. Demand is strongest in border security, counter-insurgency surveillance, maritime monitoring and infrastructure protection. Adoption will focus on affordable ISR, drones, analytics and training instead of complex autonomous combat systems.

Military AI Competitive Landscape

- Competition is split between defense primes, AI-native software firms, autonomy platform companies, space security startups, maritime robotics suppliers and rugged edge hardware providers.

- Primes retain advantages in classified programs, platform integration, compliance, sustainment and international sales channels.

- AI-native suppliers gain share when buyers need rapid iteration, modern software architecture and mission tools that improve after field feedback.

- Autonomy platform companies compete on complete mission systems that combine hardware, perception, navigation, edge compute, communications and operator interfaces.

- Partnerships are becoming central because few suppliers can cover autonomy software, sensors, weapons, cyber hardening, manufacturing and accreditation alone.

- Competitive benchmarking should track model governance, data rights, open architecture, field evidence, production capacity, exportability and ability to operate without reliable communications.

Company List

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- BAE Systems plc

- Thales S.A.

- L3Harris Technologies, Inc.

- General Atomics

- Elbit Systems Ltd.

- Saab AB

- Leonardo S.p.A.

- Anduril Industries, Inc.

- Shield AI, Inc.

- Saronic Technologies

- True Anomaly, Inc.

- Sierra Space Corporation

- Vast Space LLC

- HavocAI Inc.

- Picogrid, Inc.

- Palantir Technologies Inc.

- Helsing GmbH

- RTX Corporation

Company Coverage Preview

Anduril Industries, Inc. is the largest modern defense technology company associated with the military AI market and is positioned as the leading neo-prime. The company built its advantage around Lattice, a software platform that connects sensors, autonomous systems and command workflows across missions. Anduril has also expanded into hardware such as Ghost, Barracuda, Dive-XL, Menace and C-UAS systems. The combination gives the company control over both the mission software layer and selected autonomous platforms.

Anduril reached its dominant position by matching software speed with production scale. Its strategy differs from traditional integration models because it builds productized systems ahead of slow bespoke requirements and then adapts those systems for government missions. Large funding rounds, rapid hiring, manufacturing investment and high-profile U.S. and allied contracts have helped it compete for programs once held mainly by long-established primes.

The company’s USP is the combination of open-architecture mission software, deployable autonomous hardware, rapid iteration and venture-backed manufacturing capacity. Buyers value its ability to bring a working system to exercises quickly and refine it through operational feedback. Competitive risk remains high because defense accreditation, sustainment and international export rules are demanding. Even so, Anduril has become a benchmark for software-defined defense suppliers challenging the procurement rhythm of the incumbent industrial base.

Recent Developments

- May 2026: Anduril Industries raised US$5.0 billion in Series H funding at a reported US$61.0 billion valuation, supporting autonomous defense systems, AI command and control, drones and scaled defense manufacturing.

- May 2026: Havoc AI raised US$100 million in Series A funding to scale all-domain collaborative autonomy for defense and commercial mission environments.

- April 2026: True Anomaly raised US$650 million in Series D financing at a reported US$2.2 billion valuation to support space security, autonomous spacecraft and national-security space systems.

- March 2026: Shield AI announced US$2.0 billion in financing, including US$1.5 billion Series G funding and US$500 million preferred equity, at a US$12.7 billion post-money valuation to scale aircraft autonomy, simulation software and Hivemind-enabled defense platforms.

- March 2026: Saronic Technologies announced US$1.75 billion Series D funding at a US$9.25 billion valuation to accelerate autonomous maritime platforms, unmanned naval vessels and shipbuilding capacity.

- March 2026: Sierra Space closed US$550 million in Series C funding at a reported US$8.0 billion valuation to expand defense-tech space systems, national-security space infrastructure and production capacity.

- March 2026: Vast raised US$500 million, including US$300 million Series A equity and US$200 million debt, to accelerate Haven space station production and government-linked space infrastructure opportunities.

- May 2026: Picogrid raised US$45 million in Series A funding to build an open integration layer connecting military sensors, autonomous platforms, AI tools and command-and-control systems.

- March 2026: BAE Systems and Scale AI announced a strategic relationship to accelerate agentic AI capabilities for mission environments and operational platforms.

Major Pain Points

- Classified mission data is hard to access, label and move across development environments.

- AI models can perform well in demonstrations but degrade under smoke, weather, decoys, jamming or unfamiliar terrain.

- Government buyers want rapid deployment but still require cybersecurity, accreditation and safety evidence.

- Human oversight expectations differ across countries and slow cross-border product standardization.

- Hardware supply chains for GPUs, edge processors, sensors and secure communications remain exposed to shortages and export controls.

- Small startups often lack cleared staff, secure facilities and sustainment capacity for major programs.

- Primes often move slower than software-native customers expect, creating integration friction.

- Operators may distrust alerts when systems cannot explain why a target, vessel or anomaly was flagged.

- Autonomous platform pricing can rise sharply once payloads, encrypted datalinks, training and support are included.

- Procurement teams struggle to compare software license value against hardware unit cost and mission effect.

Analyst View and Opinion

- The strongest growth will come from fieldable mission systems rather than isolated algorithms.

- Computer vision and sensor fusion will remain the practical adoption base, while generative AI will grow through controlled decision support and staff workflows.

- Autonomy will create the largest valuation upside because it changes force structure and operator-to-platform ratios.

- Human oversight will remain a product design requirement, not a policy afterthought.

- Startups will keep winning attention, but primes will remain vital for accreditation, platform integration and international sustainment.

- European suppliers are becoming more competitive because sovereignty, Ukraine lessons and NATO interoperability are reshaping buying criteria.

- C-UAS workflows will grow faster than many offensive autonomy applications because defensive urgency is immediate and easier to justify politically.

- Vendors that own data pipelines, simulation environments and post-deployment model monitoring will create deeper customer lock-in.

- Defense AI winners will look less like generic AI companies and more like mission engineering firms with software, hardware and compliance discipline.

Military AI Target Audience

| Industry | Who Should Buy This Report? | Reason To Buy This Report |

| Defense Ministries and Procurement Agencies | Program Managers, Acquisition Teams, Digital Transformation Leaders | Evaluate AI-enabled capability roadmaps, sourcing models and vendor readiness |

| Armed Forces Commands | ISR Leaders, C2 Teams, Autonomy Cells, Training Commands | Understand practical adoption areas across ISR, autonomy, C-UAS and predictive readiness |

| Defense Primes | Strategy Teams, Product Leaders, Partnership Teams | Identify partnership opportunities with AI-native startups and edge compute suppliers |

| Defense Technology Startups | Founders, Product Teams, Business Development Leaders | Benchmark procurement barriers, customer pain points and scale pathways |

| Investors | Venture Capital, Growth Equity, Defense Funds | Assess funding themes, valuation drivers and technology areas with program-scale potential |

| System Integrators | Mission Engineering and Secure Cloud Teams | Map integration needs across classified networks, edge deployment and legacy C2 systems |

| Cybersecurity Providers | Product Managers, Government Sales Teams | Understand demand for AI-assisted cyber defense and secure model operations |

| Policy and Advisory Firms | Defense Consultants, Market Entry Teams | Support market entry, partner mapping and responsible AI strategy |

What DataM Uniquely Provides:

- DataM separates defense AI demand into mission software, autonomy hardware, integration services, edge compute and secure deployment models.

- DataM maps adoption by technology, platform, deployment and operator type instead of treating AI as one broad budget line.

- DataM benchmarks startups and primes together, making it easier to compare neo-prime momentum against established contractor advantages.

- DataM evaluates procurement barriers including classified data, model validation, responsible AI, export controls and sustainment readiness.

- DataM tracks venture funding, defense partnerships, product launches and policy shifts that affect near-term buying cycles.

- DataM connects regional demand to ground realities such as NATO interoperability, Indo-Pacific deterrence, C-UAS pressure and maritime autonomy.

- DataM supports pricing discussions by separating software licenses, hardware, integration, training, sustainment and mission-effect economics.

- DataM provides company-level coverage with official product references and market-sizing feasibility aligned with defense procurement structures.