Low-Grade Glioma Market Size& Industry Outlook

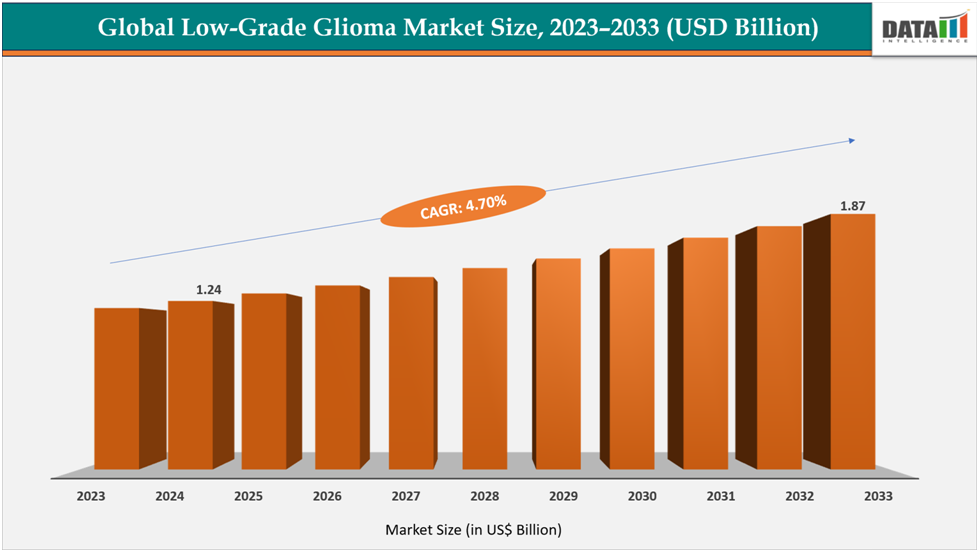

The global low-grade glioma market size reached US$1.24Billion in 2024 from US$1.12 Billion in 2023 and is expected to reach US$ 1.87Billion by 2033, growing at a CAGR of 4.7%during the forecast period 2025-2033.

The market is expanding rapidly, driven by advancements in targeted therapies, rising incidence, and technological integration. Therapies such as Temozolomide (Temodar), Lomustine (Gleostine), and emerging targeted therapies like IDH inhibitors and BRAF-targeted agents exemplify regulatory-approved innovations currently shaping the low-grade glioma treatment landscape. These treatments enable disease progression control, personalized therapy based on molecular profiling, and improved survival outcomes, addressing previously unmet clinical needs. The market’s growth trajectory is reinforced by increasing adoption of combination regimens, advancements in precision oncology, and ongoing clinical development of novel agents, positioning therapeutics as the cornerstone of next-generation low-grade glioma care and a key driver of improved patient outcomes.

Key Market Highlights

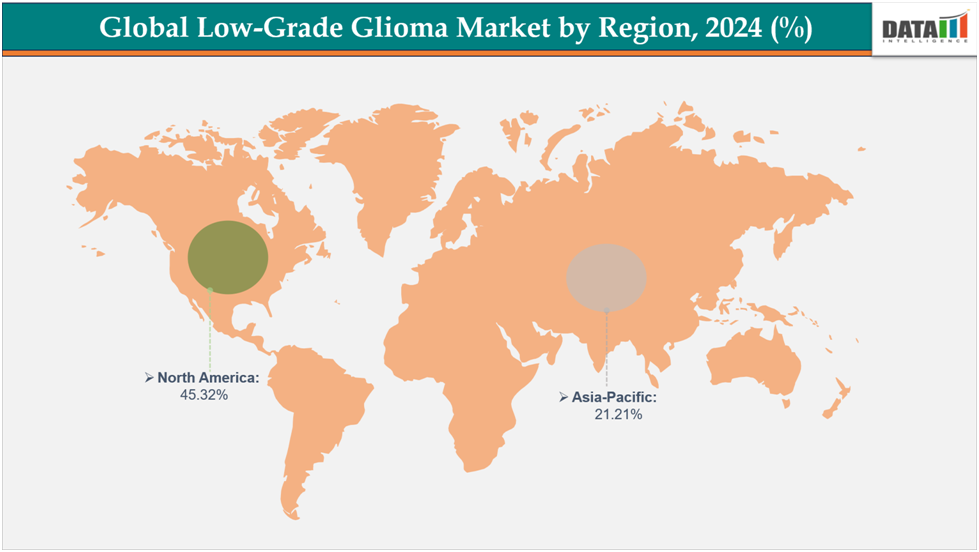

- North America dominates the Low-Grade Glioma market with the largest revenue share of 45.32% in 2024.

- The Asia Pacific is the fastest-growing region and is expected to grow at the fastest CAGR of 5.27% over the forecast period.

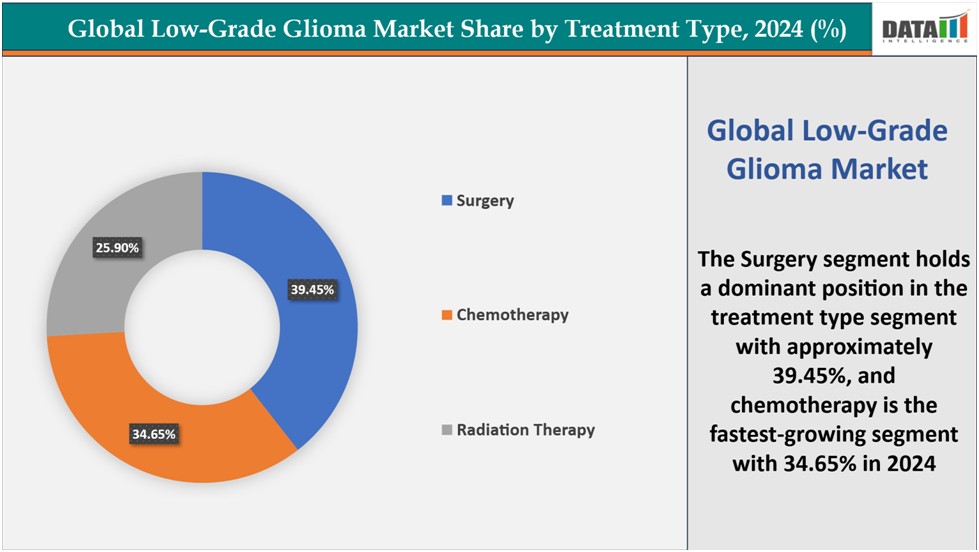

- Based on treatment type, the surgery segment led the market with the largest revenue share of 39.45% in 2024.

- The major market players in the Low-Grade Glioma market are Day One Biopharmaceuticals, AnHeart Therapeutics, Beigene, SpringWorks Therapeutics, Servier, Helsinn Healthcare SA, Eli Lilly and Company, Hoffmann-La Roche, Novartis AG, Merck & Co.Inc.

Market Dynamics

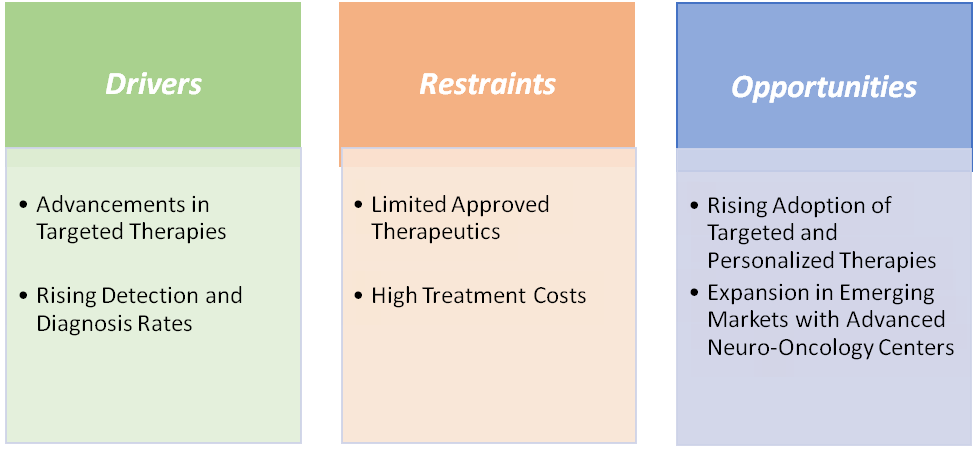

Drivers: Rising adoption of targeted therapies and precision medicine is significantly driving the Low-Grade Glioma market growth

The rising adoption of targeted therapies and precision medicine is one of the most powerful drivers fueling the growth of the Low-Grade Glioma therapeutics market, as these treatments enable personalized interventions, improved progression control, and better survival outcomes. According to the American Brain Tumor Association, gliomas account for nearly 80% of malignant primary brain tumors in adults, with low-grade gliomas representing a significant portion of newly diagnosed cases each year.

Such statistics highlight the urgent need for therapies that address specific genetic mutations and molecular subtypes, such as IDH1/IDH2 mutations, BRAF alterations, and 1p/19q co-deletions, which influence disease progression and therapeutic response. Approved drugs like Temozolomide (Temodar), Lomustine (Gleostine), and emerging agents such as Ivosidenib, Dabrafenib, and Trametinib exemplify innovations already in use, providing clinicians with tools for personalized chemotherapy, targeted inhibition, and combination regimens.

By enabling precision-targeted intervention, reduced tumor progression, and optimized treatment planning, these therapeutics directly address the clinical needs of LGG patients while improving quality of life and potentially reducing hospital visits. As molecular diagnostics and targeted therapy adoption continue to expand globally, the demand for personalized and precision-guided LGG therapeutics is expected to accelerate, driving overall market growth.

Restraints: Limited approved therapeutics and high treatment costs are major restraints hampering the growth of the Low-Grade Glioma market

The Low-Grade Glioma therapeutics market faces significant restraints due to the limited number of FDA-approved drugs and the high costs associated with targeted therapies and precision medicine. While therapies like Temozolomide (Temodar), Lomustine (Gleostine), and emerging IDH or BRAF inhibitors offer clinical benefits, the slow pace of approvals and high R&D costs restrict accessibility, particularly in emerging markets.

For instance, targeted therapies for IDH-mutant LGG can cost tens of thousands of dollars per treatment cycle, placing a substantial financial burden on patients and healthcare systems. Many insurance providers and public health programs offer limited reimbursement, which reduces patient access and adoption.

Such financial and regulatory barriers not only limit widespread utilization but also slow market expansion despite the clinical importance of personalized treatment strategies. The combination of high costs, limited treatment diversity, and reimbursement challenges acts as a significant restraint on overall market growth, especially in regions with constrained healthcare infrastructure.

For more details on this report – Request for Sample

Segmentation Analysis

The global Low-Grade Glioma market is segmented based on drug type, treatment modality, route of administration, and distribution channel.

Treatment Type:

The surgery segment is dominating the Low-Grade Glioma market with a 39.45% share in 2024

The surgery segment is dominating the Low-Grade Glioma market, accounting for approximately 39.45% of the market share in 2024. Surgical resection remains the first-line treatment for LGG patients, offering the most effective means to physically remove tumors, alleviate intracranial pressure, and improve long-term survival outcomes. Unlike chemotherapy or radiation, which primarily manage tumor progression, surgical interventions provide immediate and tangible clinical benefits, particularly when combined with molecular profiling to guide the extent of resection.

Advances in neuronavigation, intraoperative MRI, and awake craniotomy techniques have significantly enhanced surgical precision, minimizing neurological deficits and improving postoperative quality of life. Studies indicate that complete resection can achieve a median overall survival rate of 82% at five years, compared to 54% with initial biopsy. Furthermore, the extent of resection (EOR) is a critical factor; patients undergoing surgeries with higher EORs, particularly those utilizing advanced intraoperative mapping protocols, have shown improved survival rates and functional outcomes.

The critical role of surgery in LGG management, coupled with increasing adoption in specialized neuro-oncology centers worldwide, reinforces its dominance in the market and underscores its central position in standard-of-care treatment protocols.

The chemotherapy segment are fastest-growing in the Low-Grade Glioma market with a 34.65% share in 2024

The chemotherapy segment is the fastest-growing in the Low-Grade Glioma market, accounting for approximately 34.65% of the market share in 2024. This growth is driven by the increasing adoption of adjunctive and combination chemotherapy regimens following surgical resection, particularly in cases where complete tumor removal is not feasible. Drugs such as Temozolomide (Temodar), Lomustine (Gleostine), and emerging targeted agents like Ivosidenib and Dabrafenib are increasingly used to control tumor progression, delay malignant transformation, and improve patient survival.

The rise in molecular profiling and personalized therapy approaches has further fueled chemotherapy adoption, allowing clinicians to tailor treatments based on tumor genetics, such as IDH1/IDH2 mutations or 1p/19q co-deletion status, thereby improving efficacy and minimizing unnecessary toxicity. Additionally, clinical studies indicate that chemotherapy combined with radiation therapy significantly improves progression-free survival rates in LGG patients, reinforcing its growing role in standard treatment protocols. The combination of enhanced drug efficacy, expanding therapeutic pipelines, and greater clinician confidence in chemotherapy regimens positions this segment as the fastest-growing within the LGG therapeutics market.

Geographical Analysis

North America is expected to dominate the global Low-Grade Glioma market with a 45.32% in 2024

North America stands as the dominant region in the Low-Grade Glioma market, primarily due to the presence of major market players, advanced healthcare infrastructure, strong regulatory frameworks, and high adoption of precision oncology and targeted therapies. The region benefits from widespread availability of surgical facilities, specialized neuro-oncology centers, and molecular diagnostic platforms, enabling early detection and personalized treatment for LGG patients. Coupled with advancements in neuron avigation, intraoperative MRI, and targeted chemotherapeutics, North America continues to lead in innovation, adoption, and revenue generation in the low grade glioma market.

US Low-Grade Glioma Market Trends

The US FDA’s proactive role in approving and fast-tracking innovative low grade glioma therapies ensures patient access to cutting-edge treatments. Approved drugs such as Temozolomide, Lomustine, Ivosidenib, Trametinib, and Dabrafenib are widely used, highlighting the region’s focus on personalized chemotherapy and targeted therapy solutions. Advanced surgical interventions combined with molecular profiling have further improved clinical outcomes, making the US a global benchmark for LGG management.

High patient awareness, supportive reimbursement policies, and the presence of leading market players such as F. Hoffmann-La Roche Ltd, Novocure, Medtronic, Bristol Myers Squibb, and Day One Biopharmaceuticals further strengthen North America’s dominance, establishing the region as a clear leader in innovation, treatment adoption, and revenue generation for Low-Grade Glioma therapeutics.

The Asia Pacific region is the fastest-growing region in the global Low-Grade Gliomamarket, with a CAGR of 5.27% in 2024

The Asia Pacific region is emerging as the fastest-growing market for Low-Grade Glioma, driven by its large population base, rising prevalence of brain tumors, expanding access to advanced healthcare, and increasing government investments in oncology care. Countries such as China, India, and Japan are witnessing rapid growth in the adoption of advanced surgical techniques, molecular diagnostics, and targeted chemotherapy regimens, supported by improvements in hospital infrastructure and specialized cancer centers.

Japan continues to lead in neuro-oncology innovations, with widespread use of precision-guided surgical systems, proton therapy, and targeted drug therapies tailored for glioma management. In China, government-backed initiatives such as the Healthy China 2030 plan and rising approvals for novel oncology drugs have accelerated access to modern treatments for LGG patients. Similarly, India’s National Cancer Control Programme and increasing collaborations with global pharma and biotech players are expanding clinical trial activities and patient access to next-generation therapies.

The region is also benefiting from partnerships between local and global biopharmaceutical companies, which are focused on delivering cost-effective, patient-centric glioma treatments. For example, several ongoing clinical trials across China, Japan, and South Korea are evaluating targeted therapies and immuno-oncology drugs for gliomas, paving the way for rapid innovation and adoption. With a growing patient pool, supportive government policies, and accelerating healthcare digitization, the Asia Pacific is set to outpace other regions in the Low-Grade Glioma market growth over the forecast period.

Europe Low-Grade Glioma Market Trends

In Europe, the Low-Grade Glioma market is witnessing steady growth, supported by a robust regulatory framework, high clinical trial activity, and well-established neuro-oncology centers. The European Medicines Agency (EMA) and the European Union’s strong oncology-focused regulations ensure that innovative therapies, including targeted drugs, molecular diagnostics, and advanced radiotherapy techniques, reach patients with greater safety and compliance standards. The region’s aging population—where more than 20% of Europeans are aged over 65— is contributing to a rising incidence of brain tumors, thereby fueling demand for early diagnosis and effective treatment strategies.

Europe is at the forefront of personalized medicine in glioma care, with widespread adoption of molecular profiling to guide treatment decisions. Major oncology centers in Germany, France, and the UK are integrating proton therapy, intraoperative MRI, and neuronavigation systems, ensuring safer and more precise surgical outcomes. Additionally, pan-European collaborative research initiatives, such as the European Organisation for Research and Treatment of Cancer (EORTC), are driving innovation in glioma trials and improving access to novel therapies.

The region also benefits from strong reimbursement policies and government-backed cancer plans, including France’s Plan Cancer and the UK’s NHS Cancer Strategy, which prioritize expanding patient access to cutting-edge oncology treatments. With a combination of advanced infrastructure, cross-border research collaborations, and increasing emphasis on precision oncology, Europe remains one of the most progressive regions for Low-Grade Glioma market development.

Competitive Landscape

Top companies in the Low-Grade Glioma market includeDay One Biopharmaceuticals, AnHeart Therapeutics, Beigene, Spring Works Therapeutics, Servier, Helsinn Healthcare SA, Eli Lilly and Company, Hoffmann-La Roche, Novartis AG, Merck & Co.Inc, among others.

Market Scope

| Metrics | Details | |

| CAGR | 4.70% | |

| Market Size Available for Years | 2022-2033 | |

| Estimation Forecast Period | 2025-2033 | |

| Revenue Units | Value (US$ Bn) | |

| Segments Covered | Drug Type | Trametinib, Dabrafenib, Ivosidenib, Mirdametinib |

| Treatment Type | Surgery, Chemotherapy, Radiation Therapy | |

| Route of Administration | Oral & Topical | |

| Distribution Channel | Hospital Pharmacies, Retail Pharmacies, Online Pharmacies | |

| Regions Covered | North America, Europe, Asia-Pacific, South America and the Middle East & Africa | |

The global Low-Grade Glioma market report delivers a detailed analysis with 70 key tables, more than 62visually impactful figures, and 159 pages of expert insights, providing a complete view of the market landscape.

Suggestions for Related Report

For more pharmaceuticals-related reports, please click here