India Semiconductor Manufacturing Market Size

The India semiconductor manufacturing market reached US$59.78 billion and is expected to reach US$161.40 billion by 2035, growing at a CAGR of 10.42% during the forecast period 2026–2035. The India semiconductor manufacturing market is experiencing strong growth, driven by rising domestic demand for electronic devices, government initiatives to boost local chip production, and the increasing adoption of cutting-edge technologies such as 5G, IoT, and electric vehicles. Expansion in the consumer electronics sector, along with growth in automotive electronics, industrial automation, and data centers, is fueling the need for high-performance semiconductors. Supportive policies, including the production-linked lncentive (PLI) scheme for semiconductors and display manufacturing, are attracting both domestic and global investments. Furthermore, advancements in fabrication techniques, packaging solutions, and chip design are improving efficiency and output quality, further accelerating the market’s growth.

Key Takeaways

- The market is expected to expand from US$59.78 billion in 2025 to US$161.40 billion by 2035, creating substantial opportunities across fabrication, packaging, testing, and semiconductor materials.

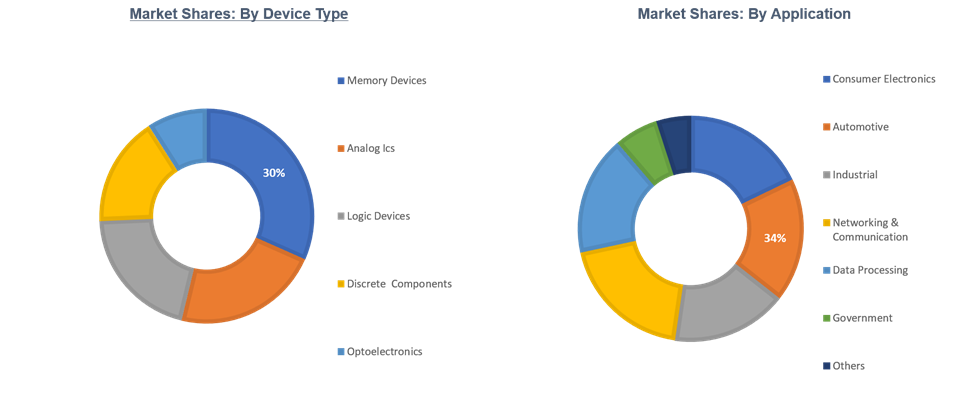

- Memory devices account for approximately 30% of market demand, reflecting the growing importance of data-intensive applications and connected devices.

- India's electronics industry is projected to generate demand exceeding US$240 billion by 2030, creating a strong downstream market for locally manufactured chips.

- Semiconductor demand from electric vehicles, telecom infrastructure, defense modernization, and cloud data centers is becoming increasingly important alongside consumer electronics.

- Government incentives, including semiconductor-focused production-linked incentive programs, continue to attract domestic and international investment into manufacturing facilities.

- Advanced packaging demand is expected to grow as India strengthens its OSAT capabilities and seeks greater participation across the semiconductor value chain.

- Limited advanced fabrication capacity remains a strategic challenge, highlighting opportunities for technology transfer, equipment suppliers, and manufacturing partnerships.

Market Scope

| Metrics | Details |

| Market Size (2025) | US$59.78 Billion* |

| Market Size (2035) | US$161.40 Billion* |

| CAGR (2026-2035) | 10.42% |

| Historic Years | 2023-2024 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Segments Covered | Device Type, Application, Manufacturing Process |

| Leading Device Segment | Memory Devices |

For more details on this report, Request for Sample

Market Dynamics

Semiconductors are increasingly becoming the foundation of India's digital economy. Every smartphone, connected vehicle, industrial automation system, telecom network, defense platform, and cloud computing facility depends on advanced semiconductor components. As demand rises across these sectors, policymakers and industry stakeholders are placing greater emphasis on building domestic manufacturing capabilities.

The India Electronics and Semiconductor Association estimates that the country's semiconductor market could increase from approximately US$52 billion in 2024 to more than US$103 billion by 2030. This expansion is creating favorable conditions for investments across wafer fabrication, assembly and testing facilities, semiconductor materials, equipment, and chip design services.

Unlike previous growth cycles that were heavily dependent on imports, the current phase is characterized by efforts to localize critical manufacturing processes and improve supply chain resilience.

Growth Drivers Reshaping India's Semiconductor Manufacturing Landscape

Electronics Consumption Continues to Expand

India remains one of the world's largest and fastest-growing electronics markets. Smartphones, laptops, tablets, wearables, smart appliances, and connected devices continue to penetrate both urban and semi-urban markets.

According to industry data, smartphone shipments reached 151 million units, reinforcing the scale of semiconductor demand generated by consumer electronics alone. Every device requires memory chips, processors, sensors, analog integrated circuits, and power management components, supporting sustained manufacturing demand.

5G, IoT and Edge Computing Accelerate Chip Requirements

Telecommunications operators are expanding 5G infrastructure across the country, increasing demand for networking processors, RF semiconductors, memory solutions, and communication chips.

At the same time, IoT deployments across manufacturing, logistics, utilities, healthcare, and smart city projects are creating new semiconductor consumption patterns. These applications require reliable, low-power, and highly integrated semiconductor solutions capable of supporting real-time connectivity.

Electric Vehicles Create New Semiconductor Demand Centers

India's automotive sector is becoming a significant semiconductor consumer. Electric vehicles require substantially higher semiconductor content compared with traditional vehicles due to battery management systems, power electronics, sensors, infotainment systems, and advanced driver-assistance features.

As EV adoption expands, automotive-grade semiconductors are expected to become an increasingly important growth category for domestic manufacturers.

Supply Chain and Manufacturing Ecosystem Analysis

Building a Domestic Semiconductor Supply Chain

The India semiconductor manufacturing supply chain extends across semiconductor design, wafer fabrication, assembly, testing, packaging, materials supply, equipment procurement, and electronics manufacturing.

A growing ecosystem of chip designers, electronic manufacturing service providers, component suppliers, and packaging facilities is supporting the industry's development. However, several critical stages remain dependent on international suppliers, particularly in advanced fabrication technologies and specialized semiconductor equipment.

Wafer Capacity Trends

India's wafer manufacturing capacity remains limited compared with established semiconductor hubs. The country's current strategy focuses on attracting large-scale fabrication investments while simultaneously strengthening assembly, testing, packaging, and design capabilities.

Increasing wafer capacity is expected to become a priority as domestic electronics demand rises and semiconductor supply chain security gains strategic importance.

Materials and Equipment Bottlenecks

Semiconductor manufacturing requires consistent access to high-purity silicon wafers, specialty chemicals, process gases, lithography systems, deposition equipment, and advanced manufacturing tools.

The availability of these materials and technologies remains a challenge for scaling domestic production. Long procurement cycles, high capital requirements, and technology access constraints continue to influence project timelines and manufacturing economics.

Advanced Packaging Demand and Node Migration Trends

As semiconductor complexity increases, advanced packaging is emerging as a critical area of investment. Packaging technologies are becoming increasingly important for improving performance, reducing power consumption, and enabling heterogeneous integration.

India's developing OSAT ecosystem is expected to benefit from rising demand for advanced packaging services as global semiconductor companies diversify manufacturing footprints.

Node migration trends are also influencing manufacturing strategies. While leading-edge nodes attract significant attention globally, substantial demand continues to exist for mature-node semiconductors used in automotive, industrial automation, telecommunications, and power electronics applications. This creates opportunities for India to establish manufacturing capabilities that align with domestic demand patterns.

Market Segmentation Analysis

The India semiconductor manufacturing market is segmented based on device type, application, manufacturing process, and region.

Source: DataM Intelligence

Device Type:The memory devices segment is estimated to have 30% of the semiconductor manufacturing market share.

The memory devices segment is projected to hold a substantial share of the India semiconductor manufacturing market. This segment is expected to lead the market owing to its crucial role in data storage and processing across diverse applications, including smartphones, laptops, tablets, servers, and industrial systems. Memory chips such as DRAM and NAND are vital for enhancing device performance, supporting high-speed computing, and ensuring efficient data management.

Their adaptability, compatibility with various electronic platforms, and consistent demand across consumer and enterprise applications make them a preferred choice for manufacturers. Memory devices are also key components in emerging technologies like 5G, Internet of Things (IoT), and electric vehicles, which rely on high-capacity, reliable storage to operate effectively.

Owing to their essential role in powering electronic devices and their widespread application across multiple sectors, the memory devices segment continues to dominate the market. Despite innovations in logic, analog, and specialized chips, the indispensable nature of memory devices in modern electronics ensures their sustained market leadership.

Key Players

The major players in the semiconductor manufacturing market include Micron Technology, Inc., Vedanta Resources Limited, Sahasra, MosChip Technologies, Applied Materials, Inc., among others.

Micron Technology, Inc.: Micron Technology, Inc. is a prominent player in the endotracheal tube market, specializing in securement solutions that enhance patient safety and comfort during mechanical ventilation. Their flagship product line, AnchorFast, offers a range of oral endotracheal tube fasteners designed to prevent complications such as lip ulcers, tube occlusions, and accidental extubation.

Key Developments

June 2026: India accelerated investments in domestic semiconductor manufacturing infrastructure through government-backed initiatives, supporting the establishment of advanced fabrication facilities, packaging units, and semiconductor supply chain development.

May 2026: The United States strengthened semiconductor cooperation with India through technology partnerships, investment initiatives, and supply chain collaboration, supporting India's ambitions to become a major semiconductor manufacturing hub.

April 2026: Leading semiconductor companies expanded investments in wafer fabrication, assembly, testing, marking, and packaging (ATMP/OSAT) facilities across India, strengthening domestic chip production capabilities.

March 2026: Semiconductor equipment and materials suppliers increased investments in India's semiconductor ecosystem, supporting the development of local manufacturing capacity and advanced electronics production.

February 2026: Industry participants accelerated research, workforce development, and skill-building initiatives focused on semiconductor design, manufacturing, and process engineering to address growing industry demand.

January 2026: The Government of India expanded semiconductor incentive programs and infrastructure development initiatives, encouraging domestic and international investments in chip manufacturing, advanced packaging, and electronics value chain expansion.

Target Audience

- Semiconductor Manufacturers

- Foundries and OSAT Providers

- Electronics OEMs

- Automotive Manufacturers

- Telecom Infrastructure Companies

- Defense Electronics Suppliers

- Data Center Operators

- Technology Investors

- Venture Capital Firms

- Semiconductor Equipment Providers

- Materials Suppliers

- Government Agencies

- Corporate Strategy Teams

- Procurement and Supply Chain Executives

Suggestions for Related Report

For more semiconductor manufacturing-related reports, please click here