India Aluminium Extrusion Market Size & Forecast

The India Aluminium Extrusion market reached US$ 2.60 billion in 2025 and is expected to reach US$ 9.77 billion by 2035, growing with a CAGR of 14.1% during the forecast period 2026-2035. India’s aluminium extrusion industry has evolved from a domestic manufacturing base into an export oriented and technology advanced sector supported by automation, sustainability initiatives and expanding applications across automotive, aerospace, renewable energy, transport, construction and electronics industries. Indian producers have strengthened global presence through investments in CNC enabled extrusion systems advanced die design automated handling and precision finishing technologies while improving compliance with ISO IATF RoHS and REACH standards enabling expansion across North America Europe Southeast Asia and the Middle East. Growth is supported by strong aluminium production capacity competitive labor smart manufacturing adoption and government initiatives such as Make in India.

Companies are investing in research and development lightweight alloys energy efficient production and customized solutions alongside increasing focus on ESG compliance recycling emissions reduction and green manufacturing practices. The sector has an installed capacity of about 4.2 million tonnes per annum across more than 450 companies with nearly 90 percent MSME driven but operates at 1.2 to 1.3 million tonnes showing underutilization. West Asia conflict disrupted supply chains scrap LPG PNG cutting output by 40 50 reducing utilization to 30 35 raising costs by 25, straining liquidity Industry response focuses on diversification renewable energy integration and resilient supply chains.

Key Takeaways

- Pipes and tubes represented the fastest-growing sub-segment under hollow profiles, expected to grow at a CAGR of 16.9%, due to accelerating demand from HVAC, fluid transport, EV cooling systems, and industrial infrastructure.

- 6000 series alloy dominated the market with more than 74% share in 2025, supported by its extensive use in architectural systems, transportation, and structural applications due to superior strength-to-weight ratio and corrosion resistance.

- Powder coating and PVDF coating segments are expected to witness accelerated growth, registering CAGRs of 16.1% and 18.7%, respectively. PVDF coating remains the fastest-growing finishing category due to rising adoption in premium façade systems, commercial buildings, and weather-resistant architectural applications.

- Building and construction remained the largest end-use sector with a market size of US$ 1.43 billion in 2025, contributing more than 55% of total market revenue. The segment is forecast to reach US$ 3.54 billion by 2033, supported by urbanization, commercial real estate development, smart cities, and green building initiatives.

India Aluminium Extrusion Industry Trends and Strategic Insight

- The Indian aluminium extrusion industry is moving towards electrification and lightweighting through the replacement of steel components in the auto and rail industries with aluminum extrusions. Hindalco Industries Ltd and Jindal Aluminium have invested in their capacities in anticipation of demand growth for aluminum extrusions that offer superior performance.

- Integrated extrusion service providers that combine machining, anodizing, powder coating, and fabricating services have grown in popularity as buyers seek readily available engineered components. Manufacturers, including Maan Aluminium Ltd. and GAL Aluminium, are focusing on improving their value-added capabilities to enhance competitiveness.

- The expansion of renewables and infrastructure projects in India has increased applications for aluminium extrusions in applications requiring corrosion and wear resistance. This has widened applications beyond conventional uses in construction.

- An increase in dependence on imported products in sectors requiring high precision and stringent environmental, social, and corporate governance standards is forcing producers to invest in advanced materials and sustainable manufacturing processes.

India Aluminium Extrusion Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 2.60 Billion | |

| 2035 Projected Market Size | US$ 9.77 Billion | |

| CAGR (2026-2035) | 14.1% | |

| By Type | Solid Profiles, Hollow Profiles, Semi-Hollow Profiles | |

| By Form | Standard Shapes and Profiles, Custom Shapes and Profiles | |

| By Alloy Grade | 1000 Series, 3000 Series, 5000 Series, 6000 Series, 7000 Series, Other Grades | |

| By Finishing | Mill Finish, Anodized, Powder Coating, PVDF Coating, Others | |

| By Recycled Content | Primary Aluminium, Secondary Aluminium | |

| By Size | Less than 10mm, 10mm to 100mm, 100mm to 300mm, More than 300mm | |

| By Production Area | Locally Produced, Imported | |

| By End Use Industry | Building and Construction, Automotive and Transportation, Electronics, Machinery, Energy and Electrical, Medical and Scientific, Others | |

| By Region | Asia-Pacific | India |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Disruption Analysis

Shift Toward Electrification, Lightweighting, and High-Performance Material Engineering Reshaping India Aluminium Extrusion Landscape

The key disruptor for the Indian market for aluminum extrusions is the quick move towards electrification and light weighting in the transportation sector (automobiles and rail industry) as well as industrial engineering. Conventional designs using steel alloys are slowly making way for extrusions made of aluminium which offer better energy efficiency and higher performance in terms of reduced emissions. Simply put, conventional commodity-based extrusions are being taken out by more sophisticated extrusions tailored for specific applications that need special alloy compositions and tighter controls.

Also, the fast-growing adoption of renewable energy infrastructure, electric vehicle ecosystem, and advanced manufacturing sector is creating new demand dynamics and enhancing the complexity demands for extrusion products. Examples of applications include mounting structures in solar energy generation systems, battery cases in electric vehicles, and industrial automation machines, among others. In response, aluminum extrusion producers are adopting integration into value-adding processes like machining, anodizing, powder coating, and assembling instead of just producing extrusions. In addition, increasing dependence on imports for precision extrusions and environmental, social, and governance (ESG) compliance among consumers have compelled domestic producers to invest in automation and alloy development technologies, among others.

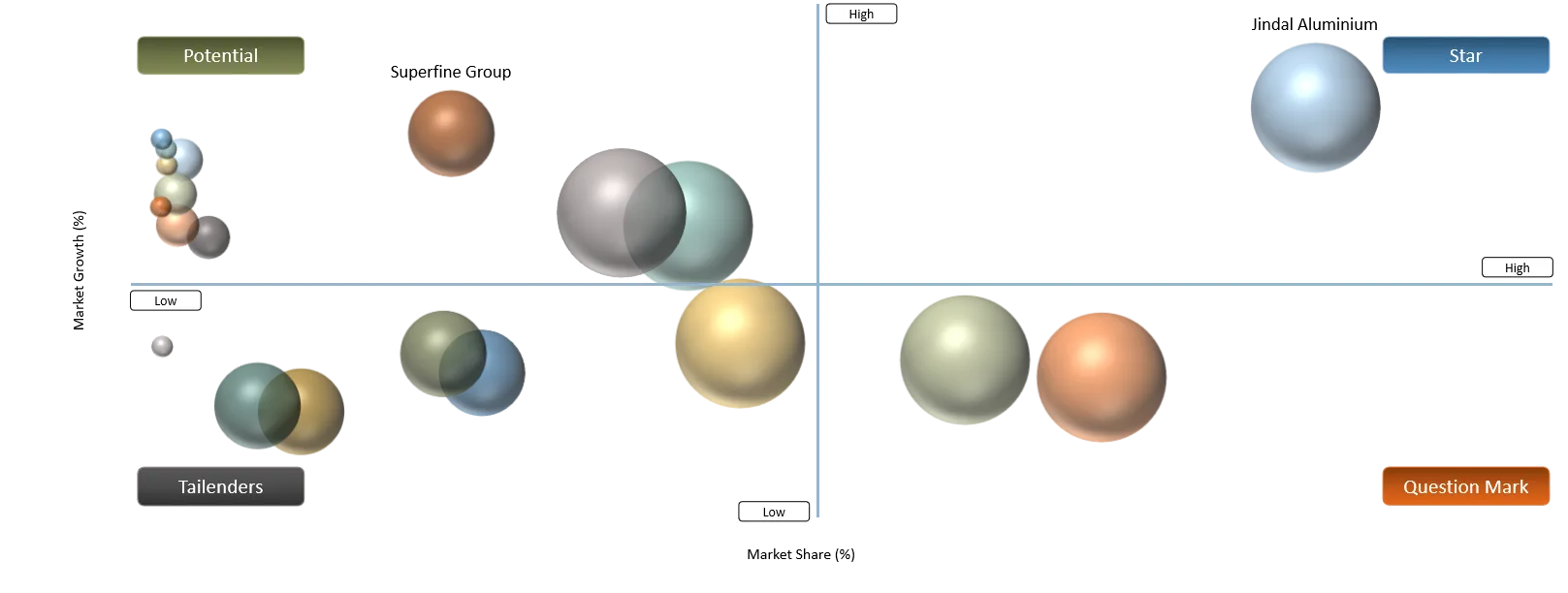

BCG Matrix: Company Evaluation

Hindalco Industries Ltd and Jindal Aluminium are stars as both have been able to establish dominance in the aluminium extrusion business of India due to their massive scale operations, upstream support, and aggressive entry into areas of value addition and engineering of precision components. Both firms are making substantial investments in smelting capacity augmentation, downstream flat rolled products, and high-precision extrusions to capitalize on rapidly growing demand from the electric vehicles, electronics, and infrastructure industries.

Question Mark firms such as Century Extrusions Limited, Maan Aluminium Ltd., Banco Aluminium Private Limited, and GAL Aluminium are considered because while increasing their capacities and modernizing their extrusion technology, they are under pressure from integrated companies and experience price fluctuations due to their commodity nature. Potential competitors would be the Superfine Group, Alom Group, Valcoindia, Padmawati Extrusion, Global Aluminium, Eleanor Industries Pvt. Ltd., Gloria Aluminium India Pvt Ltd, Bimal Aluminiums Private Limited, SNALCO, and Sudal Industries Limited that target regional markets for construction, electric, and industrial goods but are moving towards custom profiles. Finally, Tailenders are represented by small fragmented companies with low capacity, limited automation, and no penetration in advanced automotive and electronics sectors.

Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

Rising Adoption of Lightweight Materials in EVs and Transportation | 5.4% | Automotive OEMs, EV manufacturers, railway and commercial vehicle segments in India and global markets | EV battery enclosures, chassis systems, motor housings, thermal management systems | Accelerates substitution of steel with aluminium extrusions, improving energy efficiency, range extension, and structural performance in mobility applications |

Rapid Growth in Construction and Urban Infrastructure Development | 4.8% | Urban housing projects, smart cities, commercial real estate developers, and public infrastructure programs | Window frames, façades, architectural profiles, structural glazing systems | Drives large-scale consumption of standard aluminium extrusions in building and construction applications, supporting volume growth |

Expansion of Renewable Energy and Power Infrastructure | 4.6% | Solar power developers, wind energy projects, and transmission infrastructure networks | Solar panel frames, mounting structures, inverter housings, electrical enclosures | Strengthens demand for corrosion-resistant and durable aluminium profiles in renewable energy installations and grid modernization |

Rapid Expansion of Solar Energy Infrastructure | 4.5% | Utility-scale solar parks, distributed rooftop solar systems, and industrial renewable installations across India and global markets | Solar module frames, mounting structures, inverter housings, support systems | Significantly increases demand for corrosion-resistant, lightweight aluminium extrusions, supporting long-term structural and installation efficiency in solar deployment |

Rising Adoption of Lightweight Materials in EVs and Transportation

India’s rapid electric vehicle adoption is creating strong structural demand for aluminium extrusion products as OEMs focus on lightweighting to improve efficiency and extend driving range. EV batteries contribute nearly 20–30% of total vehicle weight, making weight reduction a key design priority across platforms. Aluminium is increasingly preferred due to its high strength-to-weight ratio, corrosion resistance, recyclability and thermal performance. Extruded aluminium is widely used in battery enclosures, chassis structures, crash systems, motor housings, thermal management systems and Body-in-White applications. A 10% reduction in vehicle weight can improve EV efficiency by around 6–8%, further accelerating material substitution. Automotive suppliers are expanding investments in aluminium based engineered components to meet evolving EV design requirements.

India’s EV market expansion is further reinforcing long-term extrusion demand across mobility segments. Electric two-wheeler sales reached about 1.2 million units in 2025, while passenger EV sales grew nearly 77% to around 177,000 units. Government incentives, localization policies and rising domestic manufacturing are strengthening aluminium integration across EVs, buses, commercial vehicles and rail mobility systems. This shift is increasing demand for precision engineered extrusion solutions with advanced machining and finishing capabilities. Companies are scaling capabilities in battery housings and motor casings where thermal efficiency and structural strength are critical. Overall, the transition to electric mobility is positioning aluminium extrusion as a core material driver in India’s automotive transformation.

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

Surge in Low-Cost Imports from China and ASEAN Countries | 5.2% | Domestic pricing pressure and capacity utilization | Construction extrusions, automotive profiles, industrial components | Weakens domestic producer margins, reduces capacity utilization, and intensifies price competition across standard extrusion segments |

High Energy Costs and Raw Material Price Volatility | 4.6% | Production cost structure and conversion efficiency | Aluminium billet melting, extrusion pressing, thermal processing | Increases overall manufacturing cost base, reduces global competitiveness, and compresses profitability for MSME manufacturers |

Heavy Dependence on MSME-Driven Fragmented Industry Structure | 4.3% | Operational scalability and technology adoption | Small-scale extrusion units, customized profiles, local fabrication demand | Limits automation adoption, restricts economies of scale, and reduces ability to compete with large integrated global producers |

Rising Logistics Costs and Supply Chain Inefficiencies | 4.0% | Input sourcing and distribution efficiency | Raw aluminium transport, export shipments, domestic supply chains | Increases landed cost of finished products and reduces price competitiveness in export and domestic markets |

Surge in Low-Cost Imports from China and ASEAN Countries

India’s aluminium extrusion industry is facing rising competitive pressure from low-cost imports, especially from China and ASEAN countries such as Vietnam and Malaysia under Free Trade Agreements. These zero-duty imports are entering at significantly lower prices, impacting domestic players across construction, industrial, transportation, and engineering applications. Indian producers face structural disadvantages due to higher raw material duties of around 8.25%, elevated energy costs, and rising conversion expenses. In contrast, Chinese manufacturers benefit from integrated production systems, lower financing costs, and strong government support, enabling aggressive export pricing. This cost gap is weakening the competitiveness of Indian producers in both domestic and export markets, particularly in price-sensitive extrusion segments.

Import surges are also leading to significant underutilization of India’s 3.5 million tonnes annual extrusion capacity, with effective use near 2 million tonnes. A large portion of domestic demand is increasingly met through imports, reducing expansion potential and compressing margins across the value chain. MSME-dominated producers are most affected due to rising scrap prices, LPG and PNG costs, logistics inflation, and global trade disruptions during 2025 to 2026. Concerns over weak quality enforcement and transshipment under FTAs are further intensifying competitive pressures on domestic manufacturers. Industry bodies such as ALEMAI are pushing for stricter Rules of Origin, BIS compliance, safeguard measures, and FTA reassessment to restore competitiveness.

Segment Analysis

The India aluminium extrusion market is segmented based on type, form, alloy grade, finishing, recycled content, size, production area, end use industry, and region.

Expansion of High-Strength, Corrosion-Resistant Series Alloys Driving Structural and Precision Engineering Applications

The 6000 series segment dominates the India aluminium extrusion market owing to its strong combination of strength, corrosion resistance, machinability, and surface finishing properties. These alloys are extensively used across architectural profiles, automotive components, electronics enclosures, industrial structures, and consumer durable applications where lightweight performance and precision engineering are critical.

In August 2025, Hindalco Industries announced an investment of nearly ₹586 crore to establish an aluminium extrusion facility in Andhra Pradesh for manufacturing Apple iPhone chassis and enclosure components. Smartphone frames and precision electronics casings widely utilize 6000 series aluminium alloys due to their superior anodizing quality, structural strength, lightweight properties, and precision machinability, for instance, smartphone average selling prices reached a record USD 294 during Q3 2025, growing 13.7% year-over-year. India’s smartphone market is witnessing increasing premiumization, which is driving higher demand for advanced device specifications and high-quality aluminium enclosure materials. With the country’s smartphone user base reaching nearly 659 million users, accounting for around 47.1% of the population, manufacturers are increasingly focusing on lightweight metal frames and precision-engineered casings for premium devices. This shows the increasing adoption of 6000 series alloy due to their strength, lightweight properties, and superior surface finishing capabilities.

Geographical Penetration

Infrastructure-Led Growth and Downstream Integration Accelerating Value-Added Aluminum Extrusion Demand in India

India aluminium extrusion market is witnessing steady expansion, driven by rising demand from construction, power distribution, automotive lightweighting, railways, and industrial applications. Growth is further supported by rapid infrastructure development, increasing electrification projects, and a structural shift toward high-performance, value-added aluminium products within the domestic manufacturing ecosystem.

In 2025, Hindalco Industries expanded its downstream aluminium presence through initiatives in wire, cable, and infrastructure-linked aluminium solutions. The company’s planned setup activities in India further highlight its focus on strengthening value-added aluminium manufacturing capabilities, with extrusion and fabrication playing a key role in meeting electrical, construction, and industrial demand. The Indian aluminium extrusion market is therefore evolving through increasing downstream integration, rising infrastructure-led consumption, and growing adoption of engineered aluminium solutions, positioning the country as an emerging hub for high-value extrusion-based manufacturing within the Asia-Pacific region.

Competitive Landscape

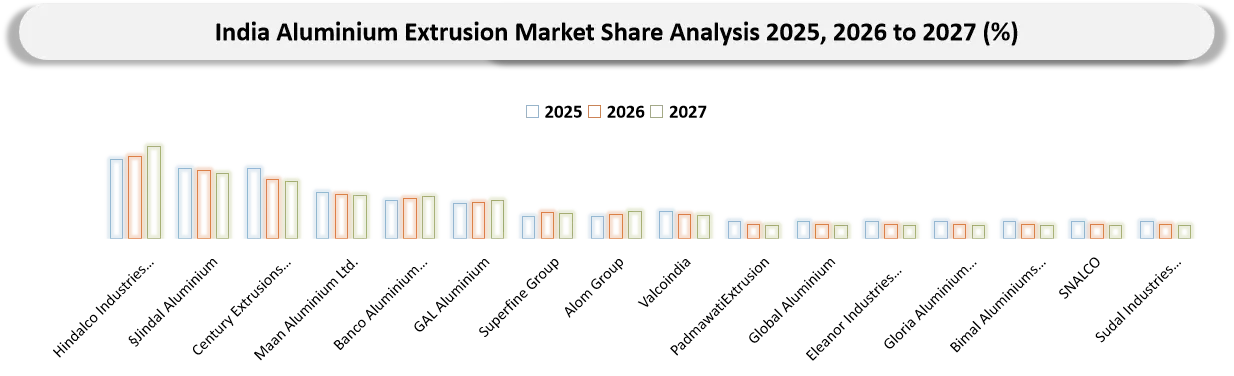

Key players include Hindalco Industries Ltd, Jindal Aluminium, Century Extrusions Limited, Maan Aluminium Ltd., Banco Aluminium Private Limited, GAL Aluminium, Superfine Group, Alom Group, Valcoindia, Padmawati Extrusion, Global Aluminium, Eleanor Industries Pvt. Ltd., Gloria Aluminium India Pvt Ltd, Bimal Aluminiums Private Limited, SNALCO, Sudal Industries Limited.

Key Developments

- January 2026: Hindalco Industries Ltd. announced an investment of ₹21,000 crore for aluminium smelter expansion in Odisha and commissioned flat rolled products (FRP) and battery foil facilities, strengthening its downstream aluminium ecosystem for EV batteries, packaging, and advanced industrial applications.

- August 2025: Hindalco Industries Ltd. announced plans to establish an integrated aluminium facility in Kuppam, Andhra Pradesh with an investment of ₹586 crore for manufacturing aluminium used in smartphone chassis and enclosures, supporting India’s electronics manufacturing ecosystem and expanding precision extrusion capabilities.

- July 2025: Hindalco Industries Ltd. unveiled a new corporate identity as part of its transformational strategy focused on advanced manufacturing, sustainability, and engineered materials, aligning with expansion into high-value downstream aluminium applications across mobility and infrastructure sectors.

- March 2025: Hindalco Industries Ltd. announced a ₹45,000 crore investment plan across aluminium and copper businesses to expand upstream and downstream capacity, accelerating growth in value-added aluminium products, extrusion-linked applications, and strategic industrial sectors in India.

- March 2025: Jindal Aluminium upgraded its Bhiwadi extrusion facility with advanced technologies and invested nearly ₹300 crore to modernize operations, increasing total extrusion capacity by 40% to 1,50,000 TPA and strengthening engineered aluminium production capabilities.

- March 2025: Maan Aluminium Ltd. acquired 13,117 square meters of leasehold land in Devas Industrial Area, Madhya Pradesh for approximately INR 8.75 crore to expand extrusion manufacturing and value-added processing, following the commissioning of a new line that doubled capacity to 24,000 tonnes annually.

Key Procurement Priorities and Buyer Evaluation Criteria

- Construction and architectural procurement remains highly fragmented, with buyers across doors, windows, glazing systems, curtain walls, and partitions primarily influenced by price competitiveness, availability, credit terms, and regional distribution strength rather than advanced engineering specifications.

- Industrial buyers are increasingly shifting toward suppliers offering integrated value-added capabilities, with preference for extrusion companies providing CNC machining, anodizing, powder coating, fabrication, welding, and assembly under a single supply ecosystem to reduce outsourcing dependency and improve lead-time efficiency.

- Procurement in high-precision sectors continues to be shaped by import dependency, particularly in aerospace, defence, semiconductor infrastructure, and advanced electronics, where buyers prioritize ultra-precision tolerances, specialized alloy availability, and advanced fabrication capabilities that are not fully met by domestic supply chains.

- Sustainability and ESG compliance are emerging as critical procurement filters, with global OEMs and export-oriented manufacturers increasingly evaluating suppliers based on recycled aluminium usage, low-carbon production processes, traceability systems, and compliance with international environmental and quality standards.

- Supply chain resilience has become a major selection criterion, with buyers prioritizing suppliers demonstrating strong operational continuity amid raw material volatility, energy price fluctuations, and logistics disruptions, alongside preference for backward-integrated manufacturers with stable long-term production capability.

DMI Insights & Strategic Recommendations

- Prioritize Expansion into High-Value Extrusion Segments: Increasing focus on automotive-grade, solar-grade, industrial-grade, and precision-engineered extrusion products is expected to improve profitability and reduce exposure to low-margin commodity segments. Expansion into customized fabrication, machining, anodizing, and downstream finishing capabilities can strengthen participation across advanced industrial applications.

- Strengthen Positioning Across Renewable Energy and EV Supply Chains: Rapid growth in solar energy infrastructure, battery storage, EV manufacturing, and transmission networks is creating sustained long-term demand for advanced aluminium extrusion solutions. Greater alignment with applications such as solar module frames, mounting structures, battery enclosures, lightweight structural systems, and thermal management components can strengthen long-term market positioning.

- Accelerate Technology Modernization and Operational Efficiency: Investments in automation, advanced extrusion presses, precision tooling systems, and energy-efficient manufacturing technologies are becoming increasingly important for improving conversion efficiency, dimensional accuracy, alloy consistency, and operational competitiveness. Adoption of smart manufacturing and digital process monitoring systems can further improve productivity and quality performance.

- Increase Penetration into Advanced Manufacturing Ecosystems: Limited penetration into aerospace, semiconductor, electronics, defense, and high-performance industrial ecosystems remains a key structural gap for the domestic extrusion industry. Strengthening certification-driven manufacturing capabilities, advanced alloy development, and tight-tolerance extrusion capabilities can improve integration into global high-value supply chains.

Target Audience 2026

- Construction & Infrastructure Developers: Real estate developers, EPC contractors, and infrastructure companies using aluminium extrusions in doors, windows, façades, curtain walls, and structural systems.

- Automotive & EV Manufacturers: OEMs and tier suppliers adopting lightweight aluminium extrusions for EV chassis, battery enclosures, crash structures, and thermal management systems.

- Electrical & Power Sector Companies: Power transmission, distribution, and renewable energy firms using aluminium extrusions in solar mounting structures, grid systems, and electrical components.

- Industrial & Engineering Manufacturers: Machinery, automation, and equipment manufacturers integrating extruded aluminium profiles for frames, enclosures, and structural applications.

- Electronics & Consumer Device Manufacturers: Companies using precision aluminium extrusions for smartphone frames, device casings, heat sinks, and high-end electronic housings.

- Aerospace, Defence & Railways: Organizations requiring high-strength, lightweight, and precision-engineered aluminium extrusions for transport, structural, and mission-critical applications.

- Government & Urban Development Bodies: Public sector agencies driving demand through infrastructure development, smart cities, metro projects, and industrial corridor initiatives.

- Investors & Private Equity Firms: Stakeholders tracking expansion in downstream aluminium, EV-linked materials, and value-added extrusion manufacturing ecosystems.

Suggestions for Related Report