Hospital Robotics (Logistics and Pharmacy) Market Overview

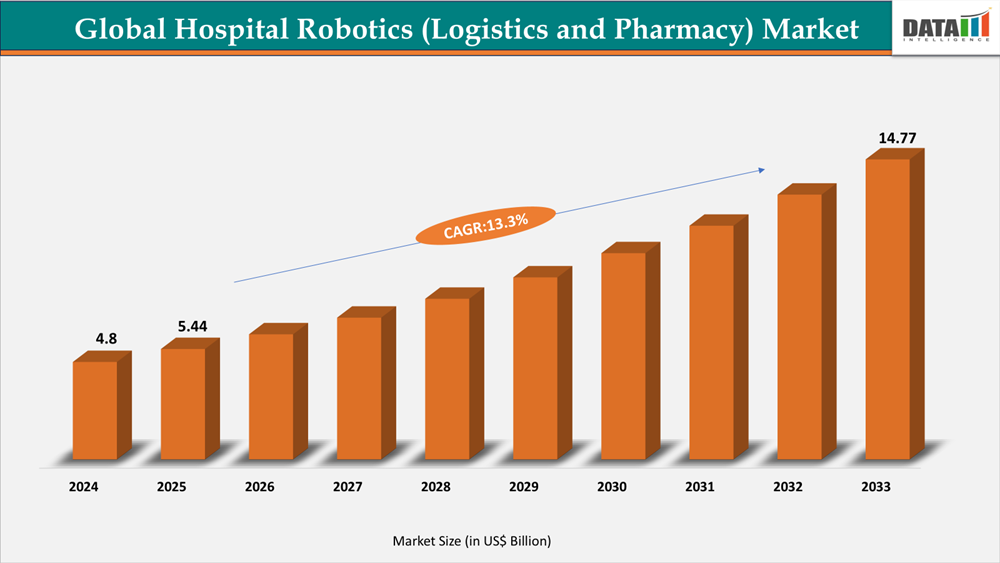

The global Hospital Robotics (Logistics and Pharmacy) Market reached US$4.8Billion in 2024, rising to US$5.44 Billion in 2025 and is expected to reach US$14.77 Billion by 2033, growing at a CAGR of 13.3% from 2026 to 2033. The global growth of the hospital robotics (logistics and pharmacy) market is influenced by the increasing workload within hospitals, the complexity of medications, and the continued shortage of healthcare workers. With the growing number of people aged over 65 years due to population aging and increases in chronic illnesses, hospital admissions and outpatient visits to hospitals continue to increase, resulting in high levels of operational pressure placed on both the pharmacy and logistics departments of hospitals.

Medications safety is one of the biggest reasons for automating processes in hospitals today. According to the WHO, medication errors account for approximately US$42 billion in lost revenue to the world’s healthcare systems each year; this accounts for close to 1% of the total expenditure on healthcare throughout the world. A majority of the errors related to medications occur during the dispensing and administration of medications, encouraging hospitals to implement pharmacy robotics like Automated Dispensing Machines (ADM) and robotic compounding systems. Studies indicate that the introduction of automation has led to a 30 to 50% decrease in medication distribution errors thus improving both safety and compliance of the medication process.

On the logistics front, hospitals handle hundreds to thousands of internal transit activities every day. Autonomous mobile robots (AMRs) are rapidly being used to transport prescriptions, test samples, and supplies, lowering manual workload by 60-70% in some circumstances and allowing staff to focus on patient care. Long-term demographic and workforce dynamics contribute to growth. By 2050, one in every six individuals worldwide will be beyond the age of 65, which will increase hospitalization and prescription volumes. At the same time, the WHO predicts a global shortage of 10 million healthcare personnel by 2030, increasing the need for automation. Overall, patient safety, operational efficiency, aging populations, and labor restrictions are driving hospital robotics adoption, putting the market on track for long-term growth.

Global Hospital Robotics (Logistics and Pharmacy) Market Industry Trends and Strategic Insights

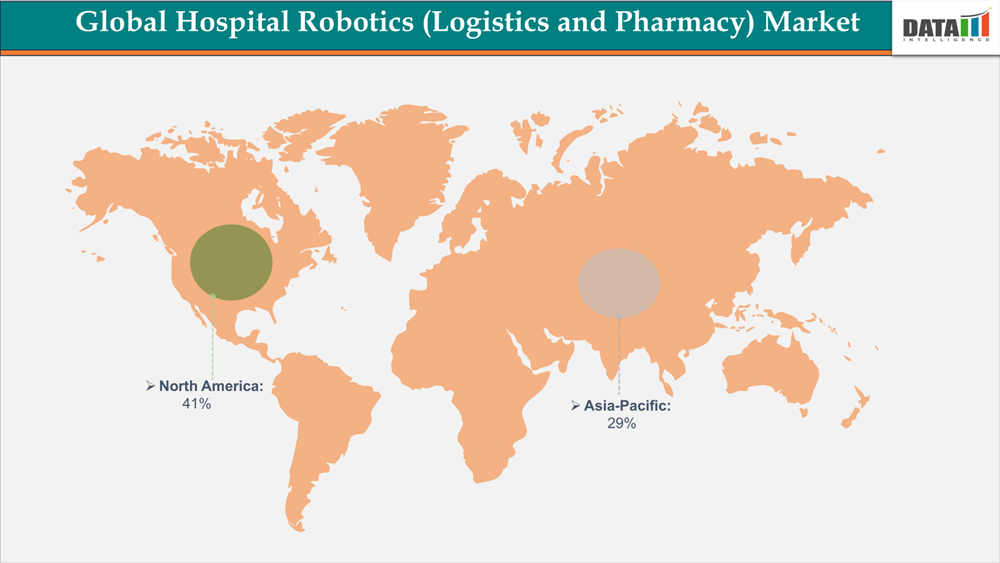

- North America leads the global hospital robotics (logistics and pharmacy) market, capturing the largest revenue share of 41% in 2025.

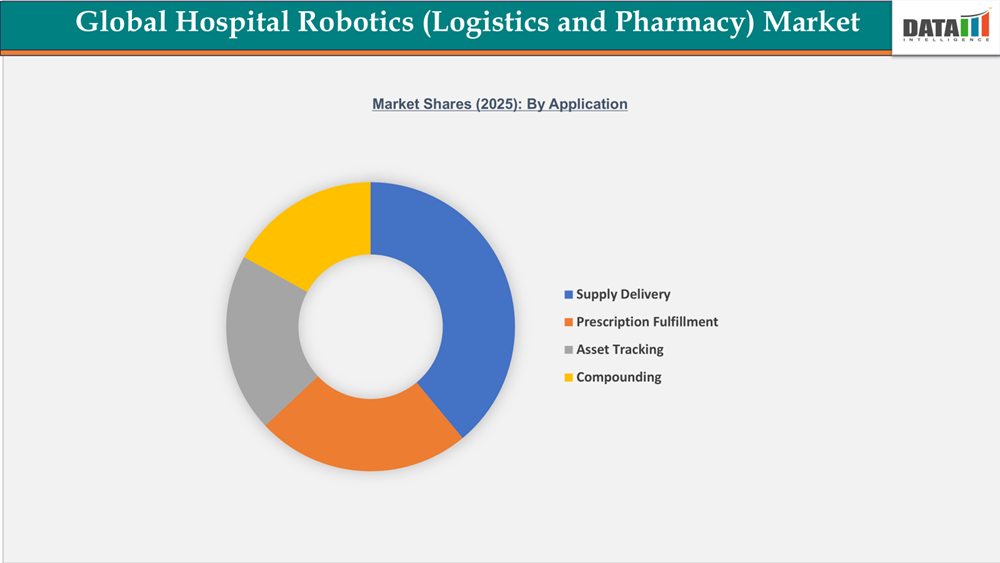

- By application segment, supply delivery led the global hospital robotics (logistics and Pharmacy) market, capturing the largest revenue share of 39% in 2025.

pharmacy)

Global Hospital Robotics (Logistics and Pharmacy) Market Size and Future Outlook

- 2025 Market Size: US$4.8 Billion

- 2033 Projected Market Size: US$14.77 Billion

- CAGR (2026–2033): 13.3%

- Dominating Market: North America

- Fastest Growing Market: Asia-Pacific

Market Dynamics

Expansion of Centralized Pharmacy & Distribution Models

The expansion of centralized pharmacy and distribution models is a major driver in both the hospital robotics such as logistics and pharmacy businesses. Large healthcare networks are increasingly centralizing pharmaceutical distribution and supply chain activities to serve many hospitals or satellite clinics. In pharmacy, robotic dispensing, packaging, and compounding systems allow for high-volume, standardized, and error-free pharmaceutical manufacturing from a central location. In logistics, autonomous mobile robots facilitate the effective internal delivery of medications and medical supplies across departments and facilities. This centralized paradigm enhances cost efficiency, inventory control, and operational consistency throughout healthcare institutions.

Complex IT Integration with Legacy Systems

One of the main obstacles preventing the widespread use of hospital robotics such as logistics and pharmacy is the intricate IT interface with legacy systems. The electronic health records (EHRs), inventory platforms, and hospital information systems (HIS) used by many healthcare facilities are antiquated and were not built to communicate with automated dispensing devices or mobile, autonomous robots. Task scheduling, elevator access, and real-time inventory tracking in logistics depend on smooth integration, whereas robotic systems in pharmacies need to work in tandem with prescription, barcode, and medicine administration software. Problems with integration may cause delays in workflow, longer implementation times, and more expensive customization.

Segmentation Analysis

The Global Hospital Robotics (Logistics and Pharmacy) Market is segmented based on type of robot, functionality, technology, end-user, application, deployment model, hospital size and region.

Rising Demand for Autonomous Supply Delivery Robots Driven by Operational Efficiency and Smart Hospital Adoption

The rising demand for delivery robots in healthcare is driven by hospitals’ need to improve their operations and the transition to smart hospitals. Hospitals use autonomous mobile robots (AMRs) to help with logistics in a hospital by getting medications, lab specimens, sterile instruments, linens, and other supplies delivered to the correct location faster and with less need for a manual workforce to transport items throughout the facility. In the pharmacy department, AMRs provide a secure and traceable method for delivering dispensed medications from either central or robotic pharmacies to nursing stations and critical care units. As hospitals begin to implement digital workflow systems and real-time tracking technology, autonomous delivery robots will continue to play a key role in the coordination of data-driven hospital operations.

3 Fastest Growing Use Cases

Autonomous Supply Delivery Robots

Autonomous supply delivery robots are gaining fast adoption because hospitals manage constant internal movement across medicines, samples, sterile items and supplies. Large hospitals face the highest pressure because manual transport consumes staff time and creates delivery inconsistency. Robot fleets are moving from limited pilots into broader use across pharmacy, laboratories, storage areas and wards. Growth is strongest where robots connect with elevators, access controls, route planning systems and real time dashboards. The market direction is clear, hospitals will scale delivery automation across repeatable routes where utilization is high and workflow disruption is low. Vendors with reliable navigation and fast implementation will capture the highest share.

Pharmacy Automation and Medication Handling

Pharmacy automation is expanding rapidly as hospitals place greater focus on medication safety and controlled workflow execution. Automated dispensing, robotic compounding, medication packaging and pharmacy to ward delivery are becoming core investment areas. Centralized pharmacy models are increasing the need for accurate, traceable and scalable medication handling. The market is shifting toward integrated systems that connect pharmacy robotics with hospital information platforms and inventory tools. Growth will be strongest in large hospitals and health systems that process high medication volumes. Vendors with strong pharmacy integration and service reliability will gain advantage as hospitals standardize medication workflows across departments.

Laboratory Sample and Specimen Transport

Laboratory sample and specimen transport is becoming a high growth use case because diagnostic speed directly affects clinical decisions. Robots reduce dependency on manual transport between wards, emergency units, laboratories and diagnostic departments. Hospitals with high test volumes need consistent movement and clear traceability for every sample. The market is moving toward priority based routing and real time sample tracking. Adoption will accelerate in large hospitals and diagnostic intensive facilities where delays affect turnaround time. The strongest solutions will combine safe navigation with laboratory workflow integration. This use case will expand as hospitals link logistics performance more closely with clinical efficiency.

Geographical Penetration

Largest Market:

Demand for Hospital Robotics (Logistics and Pharmacy) Market in North America

The North American demand for Hospital Robotics (Logistics and Pharmacy) is supported by quantifiable workforce shortages and increasing health care systems. Over 1 million completed deliveries of autonomous hospital robots have been performed through 2021; this demonstrates actual usage of these robots in the U.S. by the largest health systems within the industry for transporting medications and other supplies internally. Autonomous mobile robots are being deployed at hospitals and healthcare distributors across Canada as well, increasing the acceptance of robotic technology in this region for improving internal logistics and distributing pharmaceuticals.

U.S. Hospital Robotics (Logistics and Pharmacy) Market Outlook

Hospitals across the United States have increasingly turned to hospital robotics, such as those developed by Diligent Robotics, to address their ongoing staffing issues and operational pressures through the use of robot-assisted logistics and pharmacy operations; these robots, such as Moxi, so far have achieved over 1.25 million automated deliveries of supplies, medications and lab samples within 25+ hospitals in the U.S., freeing up clinicians and pharmacies from performing routine transport duties and improving workflow efficiency. This represents a clear indication of how hospital staff are benefitting from advancements in robotic technology and can spend more time on patient care as a result. Similarly, the larger U.S. senior living market-estimated to be worth $907.59 billion in use by 2024 - are also pursuing assorted robotic technologies that could support caregivers in their pursuit of quality care for elderly residents while experiencing short staffing issues; therefore, this is yet another example of how robotic technology will continue to play an increasing role in future health care environments.

Canada Hospital Robotics (Logistics and Pharmacy) Market Trends

The acceptance of Hospital Robotics is rising in Canada. Staffing shortages and a need for improved workflow and digitization of healthcare services have led to the gradual increase in adoption of robotics in hospitals. Autonomous mobile robots are used to transport medications, supplies, and lab samples within and between hospitals and their respective distribution centers, thus enhancing efficiencies and reducing the number of manual labor hours to complete those tasks. Automation tools for pharmacies, such as automated dispensing systems and medication management systems, are increasing the accuracy and efficiency of inventory control and contribute to a safer distribution of drugs. More and more healthcare organizations are investing in smart hospital infrastructure and automation technologies, thus further increasing the demand for robotics within those two segments.

Fastest Growing Market:

Asia-Pacific Records the Fastest Growth in the Hospital Robotics (Logistics and Pharmacy) Market

The Asia Pacific area has the highest levels of growth within the logistic and pharmacy hospital robotic market as a result of many early deployments and quick adoption in the operations of hospitals inside the region. Hospitals are utilizing autonomous delivery robots such as Panasonic’s HOSPI to run 24 hours, 7 days a week for the delivery of medication, lab samples, and supplies in many hospitals, such as Changi General Hospital in Singapore, to help patients with limited resources and improve their transportation efficiency. Hospitals are exhibiting the same trend by employing these robots as a method of supporting logistic and pharmacy functions and providing these robots with the traditional level of care. Moreover, recent research has proven that the vast majority of newly deployed robotic devices around the world are located in Asia (approximately 73% of new robotic devices placed last year), suggesting the anticipated momentum of robotic automation continues to be enhanced in Asia in terms of logistic/transportation support for the healthcare industry and providing service to these areas of activity. This momentum is further enhanced by government-backed innovation programs in countries such as Singapore, China, and Japan to support deployment of robotics and automation in hospitals as well as long-term care facilities, and this has allowed for a quicker rate of adoption here than other regions of the world.

India Hospital Robotics (Logistics and Pharmacy) Market Insights

The healthcare infrastructure in India is supported by the existence of more than 70,000 hospitals creating very large operational demand for logistics and pharmacy services internally. There has been a rise in inpatient volume and increasing complexity in procedures to put more pressure on manual medication distribution and supply transport processes. Additionally, with India's number of nurses for every 1,000 citizens remaining close to 2 (well below the global average), challenges related to workforce constraints have increased interest in automation. While the current use of robots in hospitals is still very early, a few of India's large tertiary hospitals are testing autonomous delivery systems to improve efficiency and reduce nonclinical burden on staff. Also, the continued growth of digital health initiatives and the modernization of hospital IT systems will eventually enable more widespread use of robotics for logistics and pharmacy operations.

China Hospital Robotics (Logistics and Pharmacy) Market Industry Growth

The Chinese healthcare sector is moving closer towards using automation as a result of the expanding capabilities of hospitals, as well as increasing demand for greater internal efficiencies. During the first eight months of 2025, there are datasets from public procurements showing 77 logistics robot projects that have been completed or are being completed in the country; logistics robots are used in 53 hospitals across 20 provinces, and over half of these projects are in tertiary hospitals. This means that there is evidence of greater real-world examples of robot-assisted logistics being deployed in the corridors of hospitals and completing pharmacy delivery functions.

Many hospitals in China now have autonomous logistics robots in place that help transport medications, medical supplies, laboratory specimens and other goods (between pharmacy, ward, etc.) for the primary purpose of reducing staff workload and improving the efficiency of material delivery. Many of these deployments will be part of a national smart hospital initiative, and gradually the digital infrastructure that supports robotics is being integrated with the hospital information systems. With the continued advancement of operational demand within China's extensive healthcare system, it is clear that robotics in the area of logistics and robotics in the area of pharmacy will continue to be an essential part of modernizing workflows and optimizing the internal supply chain.

Competitive Landscape

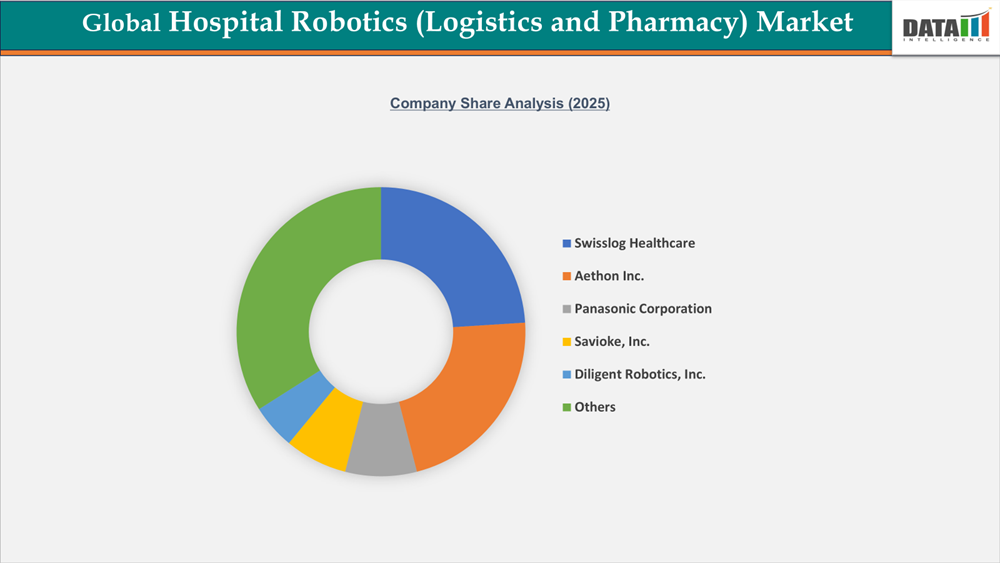

The Global Hospital Robotics (Logistics and Pharmacy) Market is highly competitive, dominated by major players such as Aethon Inc., Omnicell, Inc., Diligent Robotics, Inc., and Panasonic Corporation, alongside key generics manufacturers including Savioke, Inc., Mobile Industrial Robots A/S, Stryker Corporation, Siemens Healthineers AG, Swisslog Healthcare, and UBTech Robotics Corp.

The Hospital Robotics (Logistics and Pharmacy) Sector is progressively competitive due to innovations in autonomous mobility, artificial intelligence, and advanced pharmacy automation. The majority of companies leverage hospital relationships, global distribution channels and system interoperability to solidify their market position. Continuous product difference, strategic partnerships, as well as entering into the health smart hospital ecosystem will provide various growth opportunities.

Recent Developments

- March 2026 – Aethon and similar AMR platforms expand hospital deployment scale

Aethon Inc. continues to see large-scale deployment of its autonomous delivery robots in hospitals, supporting medication transport and logistics automation across multi-floor facilities. - February 2026 – Diligent Robotics advances human-assistive logistics robots in clinical settings

Diligent Robotics expands adoption of its hospital assistant robots (e.g., Moxi-type systems), helping nurses with medication delivery, supply transport, and non-patient-facing tasks to reduce staff burden. - In October 2025, Diligent Robotics is expanding from acute-care hospitals into the US Senior Living sector with its Moxi robots, which will perform medication deliveries, transport supplies and assist with other routine logistical tasks. This strategic expansion demonstrates the growing demand for workforce-support automation due to labors shortages in healthcare and presents more options for expansion outside of traditional hospital environments.

- In September 2025, Diligent Robotics and Swisslog Healthcare will collaborate to add autonomous delivery robots to their transport and pharmacy automation systems, creating complete delivery solutions for hospitals. The goal of this collaboration is to provide hospitals with complete delivery solutions, complementing Swisslog’s current systems, and improving efficiency throughout the entire logistics and pharmacy workflows.

What You Get Compared with Competitors

| Dimension | Traditional Market Research | DataM Intelligence |

| Product | Static PDF reports covering broad hospital automation trends with limited visibility into robotics logistics, pharmacy automation and deployment models | Custom dashboards for hospital robotics logistics and pharmacy automation with interactive views across applications, countries, companies and end users |

| Data Age | 6 to 12 months old with historical snapshots of hospital automation adoption and limited updates on robotics deployments | Living data with continuous updates on autonomous mobile robots, pharmacy automation, hospital procurement activity and emerging technology shifts |

| Engagement | One time transaction with limited follow up after delivery of market size, segmentation and competitive data | Continuous partnership with embedded analyst support to track hospital adoption, vendor moves, investment activity and procurement triggers |

| Output | Raw market information with limited guidance on how hospitals, vendors or investors should act on robotics logistics and pharmacy trends | Actionable insights with clear recommendations for market entry, product positioning, hospital targeting and investment evaluation |

| Customization | One size fits all syndicated templates with limited tailoring for hospital size, country readiness, pharmacy workflow or logistics use case | Tailored solutions through DMI Insights and DMI Connect built around each client’s context, with 81% of our clients choosing a customized solution |

| Market Depth | General coverage of healthcare robotics with limited detail on medication transport, robotic compounding, sample movement and sterile supply delivery | Focused intelligence on hospital robotics logistics and pharmacy automation across use cases, adoption maturity, ROI drivers and white space opportunities |

| Decision Support | Limited ability to compare countries, applications, vendors and procurement readiness in one view | Dashboard based comparison of country opportunity, adoption maturity, vendor positioning and investment attractiveness |

| Retention | Low chance of re engagement once the report is delivered | Over 35% of our clients are repeat customers due to ongoing updates, customization and long term decision support |

Major Hospital Robotics Pain Points and How to Derisk them

Hospital robotics logistics and pharmacy automation is being pulled into the center of hospital operating strategy as labor pressure and medication complexity increase. Hospitals are facing persistent gaps in non-clinical task coverage, especially across medicine movement, sample transport, sterile supply delivery and pharmacy handling. Manual workflows are no longer sustainable in large facilities where internal movement volumes are rising faster than available support staff. The strongest business action is the automation of repeatable delivery routes and high-risk medication workflows. Pharmacy automation reduces dispensing variation and supports tighter control of medication movement. Autonomous mobile robots reduce dependency on manual runners and improve delivery consistency across departments. The most attractive adoption zones are large hospitals, multi building campuses and facilities with centralized pharmacy operations. Market demand is strongest where operational delays directly affect care quality, staff productivity and medication safety performance.

Country Opportunity Scoreboard

The country opportunity scoreboard ranks North America as the strongest near-term adoption region, led by the United States and Canada. These markets combine advanced hospital infrastructure, higher healthcare automation budgets, stronger vendor presence and greater acceptance of robotic workflow support. Asia Pacific ranks as the fastest growth region, with China and India standing out because of hospital expansion and healthcare modernization. China benefits from smart hospital investment and a large addressable hospital base. India shows high future potential as private hospital chains expand and pharmacy workflow standardization improves. Europe remains a steady opportunity base, supported by workforce constraints and strong focus on healthcare efficiency. The highest scoring countries share two characteristics, strong hospital digitization and pressure to reduce non clinical workload. Markets with weak building integration and lower capital availability will adopt more slowly.

Adoption Maturity Curve

Hospital adoption is moving through four clear maturity levels. The first level is manual logistics, where staff move medicines, supplies, samples and linens with limited tracking. The second level is point automation, where hospitals deploy pharmacy dispensing systems or selected robotic delivery routes. The third level is connected automation, where autonomous mobile robots link with elevators, access controls, pharmacy platforms and hospital information systems. The fourth level is enterprise orchestration, where robot fleets operate across departments with real time dashboards and workflow analytics. Most hospitals are currently between point automation and connected automation. Large urban hospitals and smart hospital campuses are advancing fastest because they have higher delivery volume and stronger digital infrastructure. The next competitive shift will come from hospitals scaling robotics beyond isolated pilots into standard operating workflows across pharmacy, logistics and laboratory movement.

ROI and Payback Analysis

The economic case for hospital robotics is strongest where labor shortages and high movement volumes overlap. Autonomous delivery robots reduce manual transport hours across medicines, lab samples, linens and supplies. Pharmacy automation improves accuracy and lowers time spent on repetitive dispensing or compounding tasks. Payback is most attractive in large hospitals with centralized pharmacy operations and heavy interdepartmental movement. Smaller hospitals face longer payback periods unless vendors offer service based pricing or shared automation models. The strongest value drivers are labor substitution, delivery reliability, medication traceability and reduced workflow delays. Service contracts and software subscriptions are becoming important to vendor economics because hospitals require maintenance, integration support and workflow optimization after deployment. Investment returns improve when robots are used across multiple departments rather than one isolated function. High utilization is the key determinant of financial performance.

Procurement Trigger Analysis

Hospital procurement is triggered by operational stress rather than technology interest alone. The strongest buying signals are staff shortages, medication safety pressure, internal delivery delays and smart hospital upgrades. Pharmacy directors become key decision influencers when medication volume rises and manual handling creates traceability concerns. Operations leaders push adoption when support staff cannot manage frequent movement across floors or buildings. Chief information officers become central when robotics must connect with hospital information systems and building infrastructure. Procurement teams focus on total cost of ownership, service reliability, implementation complexity and vendor deployment record. Hospitals favor solutions with proven performance in live clinical settings and strong post installation support. Purchase urgency rises when automation links directly to workforce relief and measurable workflow improvement. The market will increasingly reward vendors that reduce integration risk and shorten deployment timelines.

Investor White Space Analysis

Investor white space is strongest in connected hospital automation platforms that combine robotics hardware with workflow software. Autonomous mobile robots remain a major opportunity, especially in hospitals with high logistics intensity. Pharmacy automation is also expanding as medication safety and centralized dispensing become bigger priorities. Robotic compounding and secure medication transport represent higher value opportunities because they address regulated and risk sensitive workflows. Software layers that connect robots with pharmacy systems, inventory platforms, elevators and dashboards are becoming more strategically valuable than standalone hardware. Service based models will expand the addressable market by reducing upfront capital barriers. The most attractive investment targets have hospital access, integration capability, recurring revenue and deployment proof. Consolidation is likely as larger healthcare technology players seek automation assets that improve hospital efficiency and strengthen digital health portfolios.

Competitive Moat and Vendor Positioning Scorecard

Vendor positioning in hospital robotics logistics and pharmacy automation is defined by integration depth and deployment reliability. Hardware performance remains important, but long-term advantage depends on how well robots work inside complex hospital environments. Strong vendors have proven navigation in crowded corridors and reliable elevator connectivity. They also have pharmacy workflow integration and responsive service networks. Companies with hospital installed bases gain an adoption advantage because procurement teams prefer vendors with live clinical proof. Software capability is becoming a major moat as hospitals demand route optimization, delivery tracking, fleet utilization and workflow analytics. Vendors with recurring service revenue and strong integration support will outperform hardware focused competitors. The competitive landscape is shifting toward platform providers that can support hospital wide automation. Narrow product vendors will face pressure unless they build partnerships or deepen software capability.

Funding, Partnership and M&A Tracking

Funding and partnership activity is moving toward hospital robotics companies that solve workforce pressure and medication workflow inefficiency. Strategic partnerships are increasing between robotics vendors and hospital technology providers as hospitals demand better integration with clinical and operational systems. Pharmacy automation companies are also becoming important partners because medication movement is one of the highest value hospital use cases. M and A activity is expected to focus on software orchestration, robotic fleet management, pharmacy automation assets and service networks. Investors are prioritizing companies with deployment proof and recurring revenue potential. Strategic acquirers will favor assets that improve hospital workflow visibility and extend automation across multiple departments. The strongest capital flows will move toward companies that combine hospital access and technical integration capability. This makes connected automation platforms the most attractive category for long term investment.

What Sets This Global Hospital Robotics (Logistics and Pharmacy) Market Intelligence Report Apart

- Latest Data & Forecasts – Comprehensive and up-to-date market intelligence with forecasts through 2033, covering global demand by type of robot, functionality, technology, end-user, application, deployment model, hospital size, with region-wise analysis across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

- Regulatory Intelligence – Comprehensive evaluation of hospital accreditation standards, cybersecurity requirements, FDA device classification, CE marking, NMPA approvals, and data privacy frameworks affecting integration with hospital information systems, all of which have an impact on robotics deployment.

- Competitive Benchmarking – Leading robotics providers are systematically benchmarked according to their technological prowess, installed base, AI navigation performance, pharmaceutical automation integration, service models, geographic reach, strategic alliances, and recurring revenue structures.

- Geographic & Emerging Market Coverage – Regional analysis of hospital infrastructure expansion, labor shortages, digital health maturity, reimbursement settings, and smart hospital efforts, with a focus on high-growth regions like Asia-Pacific and technology-intensive markets in North America and Europe.

- Actionable Strategies & Cost Dynamics – Strategic insights on ROI models, total cost of ownership, workflow optimization benefits, maintenance and service agreements, and integration expenses, with input from hospital administrators, pharmacy directors, healthcare IT specialists, and robotics solution vendors.