Hematologic Malignancy Therapeutics Market Size and Trends

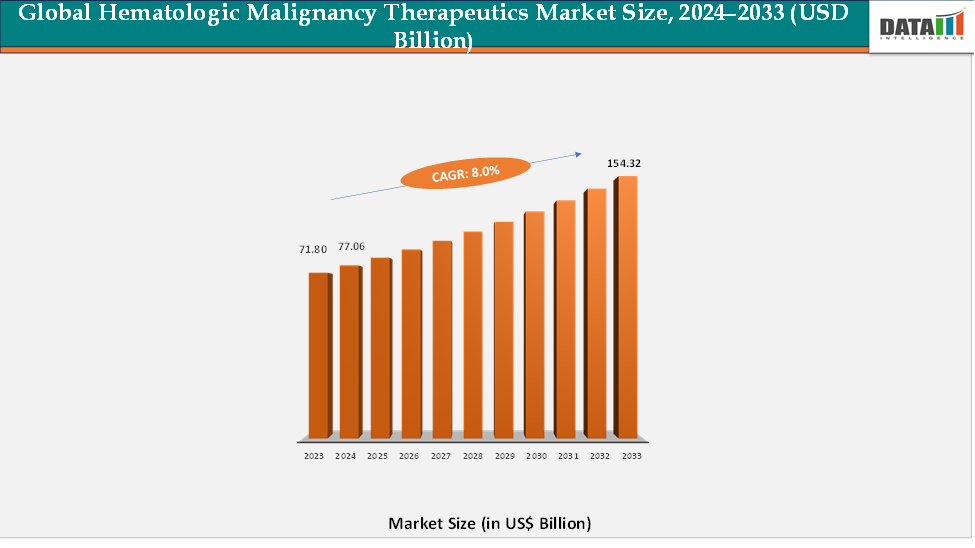

The global hematologic malignancy therapeutics market reached US$ 71.80 billion in 2023, with a rise to US$ 77.06 billion in 2024, and is expected to reach US$ 154.32 billion by 2033, growing at a CAGR of 8.0% during the forecast period 2025–2033. The global hematologic malignancy therapeutics market is witnessing steady growth, driven by the rising prevalence of blood cancers such as leukemia, lymphoma, and multiple myeloma, coupled with increasing advancements in targeted and immunotherapy-based treatments. Growing awareness of early diagnosis, expanding access to advanced cancer care, and a surge in clinical research activities are fueling the demand for effective hematologic cancer therapies. Pharmaceutical and biotechnology companies are heavily investing in the development of novel drugs, including CAR-T cell therapies, monoclonal antibodies, and small molecule inhibitors, aimed at improving survival rates and reducing relapse risks. With continuous innovation and collaborations between research institutions and drug developers, the hematologic malignancy therapeutics market is poised for sustained growth, addressing unmet clinical needs and improving outcomes for patients worldwide.

Key Market highlights

- North America accounted for approximately 42.5% of the global hematologic malignancy therapeutics market in 2024 and is expected to maintain dominance, supported by advanced healthcare infrastructure, strong regulatory support, and high adoption of targeted and immuno-oncology therapies.

- Asia–Pacific held around 18.7% of the global market in 2024 and is projected to be the fastest-growing region, driven by rising blood cancer prevalence, expanding healthcare access, and increasing adoption of innovative treatments. Government initiatives, growing awareness, and expanding clinical research networks continue to accelerate market growth across the region.

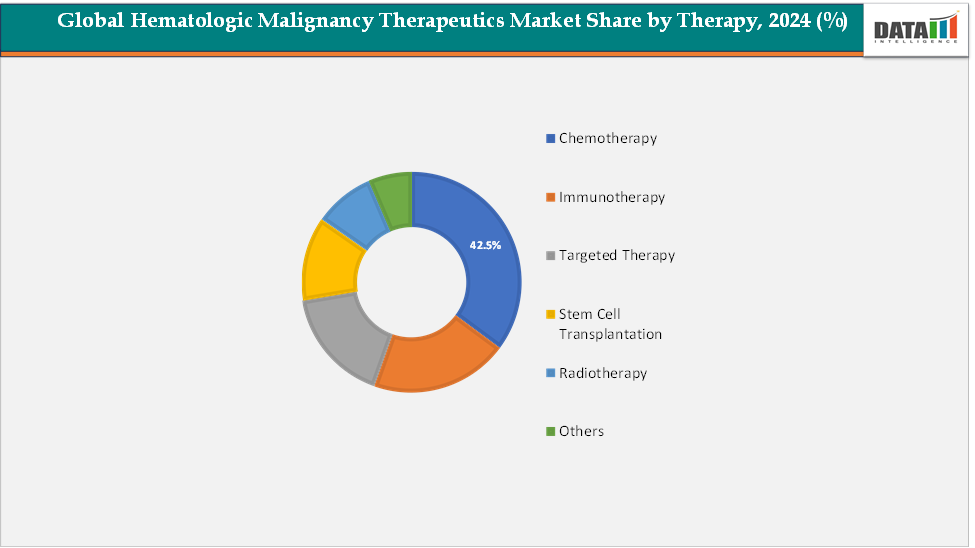

- Chemotherapy dominated the global hematologic malignancy therapeutics market in 2024, accounting for approximately 42.5% of total revenue. Its dominance is attributed to its long-standing role as the standard of care for treating various hematologic cancers, including leukemia, lymphoma, and multiple myeloma

Market Size & Forecast

- 2024 Market Size: US$77.06 billion

- 2033 Projected Market Size: US$154.32 billion

- CAGR (2025–2033): 8.0%

- North America: Largest market in 2024

- Asia Pacific: Fastest-growing market

Global Hematologic Malignancy Therapeutics Market Dynamics: Drivers & Restraints

Driver: Growing Approvals of Targeted Small Molecules

The increasing number of regulatory approvals for targeted small-molecule therapies is expected to significantly drive growth in the hematologic malignancy therapeutics market in the coming years. These agents are designed to specifically inhibit molecular pathways involved in cancer cell proliferation and survival, offering improved efficacy with reduced systemic toxicity compared to conventional chemotherapy. Regulatory bodies such as the U.S. FDA and European Medicines Agency (EMA) have accelerated the approval of novel small molecules targeting genetic mutations and signaling pathways associated with leukemia, lymphoma, and myeloma.

Compounds such as kinase inhibitors, BCL-2 inhibitors, and epigenetic modulators are increasingly being integrated into treatment regimens, either as monotherapies or in combination with immunotherapies. The growing clinical success of these therapies, along with expanding research into precision oncology, rising R&D investments, and increasing patient access to personalized treatment options, continues to strengthen market expansion for hematologic malignancy therapeutics worldwide.

Restraint: Limited Long-term Efficacy Data for Novel Immunotherapies

The lack of comprehensive long-term efficacy and safety data for newly approved immunotherapies is expected to restrain the growth of the Hematologic Malignancy Therapeutics Market. While these therapies show strong initial responses, uncertainty about their durability, potential late-onset side effects, and high costs limits physician confidence and widespread adoption, particularly in developing markets.

For more details on this report, Request for Sample

Global Hematologic Malignancy Therapeutics Market Segment Analysis

The global hematologic malignancy therapeutics market is segmented by disease condition, therapy and region.

Therapy: The chemotherapy segment is estimated to have 42.5% of the hematologic malignancy therapeutics market share.

Chemotherapy is expected to continue dominating the hematologic malignancy therapeutics market throughout the forecast period, maintaining its position as a cornerstone treatment for various blood cancers, including leukemia, lymphoma, and multiple myeloma. Despite the rapid emergence of targeted therapies and immuno-oncology drugs, chemotherapy remains widely utilized due to its proven efficacy, cost-effectiveness, and compatibility with combination regimens that enhance overall treatment outcomes. It is often the first line of therapy, especially in low- and middle-income regions where access to advanced biologics is limited.

The growing prevalence of hematologic cancers continues to fuel demand for chemotherapeutic agents. According to the International Myeloma Foundation, multiple myeloma affects over 180,000 people worldwide and accounts for nearly 10% of all hematologic malignancies. The increasing incidence of myeloma, coupled with ongoing improvements in chemotherapeutic formulations, supportive care, and combination protocols, reinforces chemotherapy’s enduring dominance in the treatment landscape for hematologic malignancies.

Global Hematologic Malignancy Therapeutics Market - Geographical Analysis

The North America hematologic malignancy therapeutics market was valued at 42.5% market share in 2024

North America holds a leading position in the global hematologic malignancy therapeutics market, supported by strong regulatory frameworks, advanced healthcare infrastructure, and a high prevalence of hematologic cancers such as leukemia, lymphoma, and multiple myeloma. The region’s dominance is further reinforced by the rapid adoption of targeted therapies, immuno-oncology treatments, and precision medicine approaches.

Reflecting this progress, in October 2025, Syndax Pharmaceuticals received the U.S. Food and Drug Administration (FDA) approval of Revuforj (revumenib) for the treatment of relapsed or refractory (R/R) acute myeloid leukemia (AML) with an NPM1 mutation in adult and pediatric patients aged one year and older who have no satisfactory alternative treatment options. This advancement underscores the region’s strong regulatory momentum and capacity to translate groundbreaking research into clinical application.

North America continues to benefit from significant R&D investments by major biopharmaceutical companies, well-established academic cancer research institutions, and a robust innovation ecosystem that accelerates therapy development. Furthermore, widespread access to advanced diagnostic technologies, early adoption of novel therapeutics, and supportive reimbursement policies contribute to maintaining North America’s dominant position in the hematologic malignancy therapeutics market.

The European hematologic malignancy therapeutics market was valued at 20.2% market share in 2024

Europe maintains a significant share in the global Hematologic Malignancy Therapeutics Market, supported by its well-established healthcare infrastructure, strong emphasis on cancer research, and consistent regulatory approvals for novel therapies. The European Medicines Agency (EMA) and national health authorities play a key role in facilitating the development and authorization of advanced treatments for hematologic cancers. For instance, in October 2025, GSK plc announced that the U.S. Food and Drug Administration (FDA) approved Blenrep (belantamab mafodotin-blmf) in combination with bortezomib and dexamethasone (BVd) for adults with relapsed or refractory multiple myeloma who have received at least two prior lines of therapy. This development underscores GSK’s leadership in hematologic oncology, backed by robust research, manufacturing, and clinical expertise rooted in Europe.

The region’s strong academic research network, collaborative R&D frameworks, and widespread access to advanced diagnostic technologies further reinforce its position. In addition, favorable reimbursement policies, national cancer control strategies, and ongoing innovation in targeted and immunotherapeutic approaches continue to strengthen Europe’s role as a key contributor to the global hematologic malignancy therapeutics industry.

The Asia-Pacific hematologic malignancy therapeutics market was valued at 18.7% market share in 2024

The Asia–Pacific region is poised to register the fastest growth in the hematologic malignancy therapeutics market during the forecast period. Growth is primarily fueled by the rising incidence of blood cancers, improving diagnostic capabilities, and expanding access to novel treatment options in countries such as China, Japan, South Korea, and India. Governments across the region are strengthening cancer control programs and expanding healthcare spending, which supports early diagnosis and advanced treatment adoption. Moreover, pharmaceutical and biotechnology companies are increasingly investing in clinical trials, biosimilar development, and local production of oncology drugs, enhancing treatment affordability and accessibility.

Japan and China, in particular, are seeing accelerated approvals for targeted and immunotherapeutic agents, supported by regulatory harmonization with international standards. The growing number of collaborations between regional oncology research institutions and global pharma companies is further driving innovation in hematologic malignancy therapies. Rising awareness, improving insurance coverage, and increasing patient participation in clinical trials contribute to the region’s rapid market expansion.

Global Hematologic Malignancy Therapeutics Market – Competitive Landscape

The major players in the hematologic malignancy therapeutics market include Pfizer Inc., F. Hoffmann-La Roche Ltd, Sanofi, Syndax Pharmaceuticals, Novartis Pharmaceuticals Corporation, GSK plc, Johnson & Johnson, Amgen Inc., AbbVie, among others.

Key Developments:

- In February 2025, Pfizer Inc. announced that the U.S. FDA has approved a supplemental Biologics License Application (sBLA) for ADCETRIS (brentuximab vedotin) in combination with lenalidomide and rituximab for the treatment of adult patients with relapsed or refractory large B-cell lymphoma (LBCL), including DLBCL and high-grade B-cell lymphoma (HGBL), after two or more prior therapies who are ineligible for stem cell transplantation or CAR T-cell therapy.

- In September 2025, Kura Oncology, Inc. (Nasdaq: KURA) and Kyowa Kirin Co., Ltd. announced that the Journal of Clinical Oncology published full results from the pivotal KOMET-001 trial (NCT04067336), evaluating ziftomenib, an investigational oral menin inhibitor, in adults with relapsed or refractory NPM1-mutated acute myeloid leukemia (AML).

Market Scope

| Metrics | Details | |

| CAGR | 8.0% | |

| Market Size Available for Years | 2022-2033 | |

| Estimation Forecast Period | 2025-2033 | |

| Revenue Units | Value (US$ Bn) | |

| Segments Covered | Disease Condition | Leukemia, Lymphoma, Multiple Myeloma |

| Therapy | Chemotherapy, Immunotherapy, Targeted Therapy, Stem Cell Transplantation, Radiotherapy, Others | |

| Regions Covered | North America, Europe, Asia-Pacific, South America, and the Middle East & Africa | |

The global hematologic malignancy therapeutics market report delivers a detailed analysis with 70 key tables, more than 66 visually impactful figures, and 195 pages of expert insights, providing a complete view of the market landscape.

Suggestions for Related Report

For more pharmaceutical-related reports, please click here