Overview

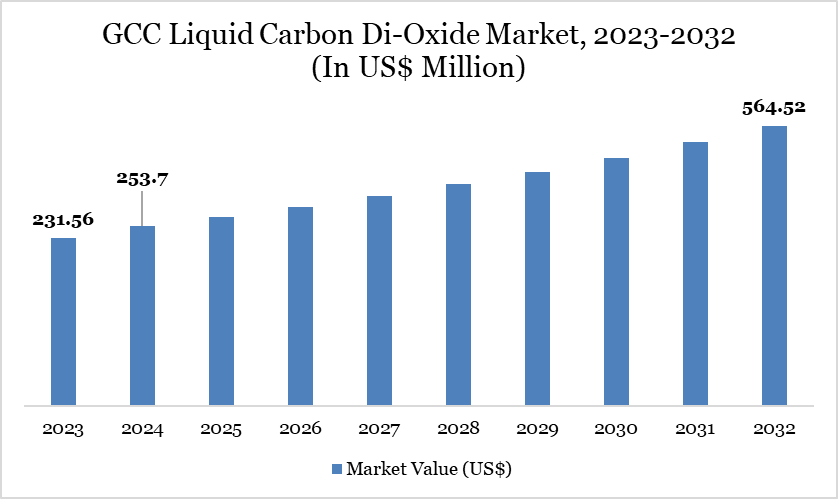

GCC liquid carbon di-oxide market reached US$ 280.7 Million in 2025 and is expected to reach US$ 639.0 Million by 2033, growing at a CAGR of 10.6% during the forecast period 2026-2033.

GCC liquid CO₂ market is growing steadily, driven by industrialization, low-carbon strategies, and economic diversification. Rising demand in food, healthcare, chemicals, and logistics, along with carbon capture and sustainability efforts, is boosting the need for high-purity liquid CO₂ across the region.

For instance, under Vision 2030, Saudi Arabia is investing in petrochemical clusters and industrial zones such as the Jubail Industrial City, where refineries, fertilizer plants, and steel industries generate and consume CO₂. These developments have led to increased installation of CO₂ liquefaction units and pipeline systems within these zones, supporting both on-site utilization and regional distribution.

Additionally, in 2024, Gulf Cryo launched the first carbon capture plant for the merchant market in Saudi Arabia’s Western Region. Located at Petro Rabigh’s MEG plant in Rabigh, the facility was built under a 20-year agreement with the Saudi Aramco–Sumitomo joint venture. Equipped with two compressors, it produces 300 metric tons of liquid CO₂ per day, helping cut 100,000 metric tons of CO₂ emissions annually.

Liquid Carbon Di-Oxide Market Trend

The liquid carbon dioxide market is experiencing steady growth driven by its expanding applications across various industries such as food and beverage, healthcare, and chemicals. Increasing demand for carbonated drinks and advancements in enhanced oil recovery techniques are key growth factors. Environmental concerns are pushing industries to adopt CO₂ for eco-friendly refrigeration and cleaning processes. Technological innovations are improving production efficiency and storage solutions, further fueling market expansion. Additionally, rising investments in industrial gas infrastructure are expected to support sustained market development in the coming years.

Market Scope

Metrics | Details |

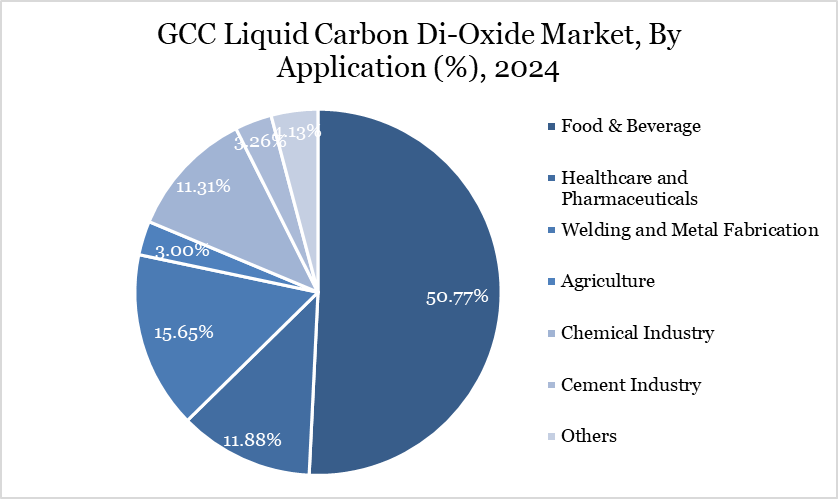

By Application | Food & Beverage, Healthcare and Pharmaceuticals, Welding and Metal Fabrication, Agriculture, Chemical Industry, Cement Industry, Others |

By Country | Saudi Arabia, United Arab Emirates (UAE), Kuwait, Qatar, Oman, Bahrain |

Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth |

Market Dynamics

Surging Demand from Food & Beverage Industry

The GCC liquid CO₂ market is witnessing a wave of strategic launches and infrastructure expansions driven by the rising demand from the food and beverage industry, as countries intensify efforts to boost domestic production, ensure food security, and support cold chain logistics. Several notable developments across the region are shaping this trend.

For instance, in the UAE, where just 0.7% of land is arable and over 85% of food is imported, tackling food challenges demands strategic partnerships and not just advanced tools. The National Food Security Strategy 2051 focuses on sustainable local production driven by technology and innovation to build resilient food systems.

Additionally, in 2023, UAE government has launched Food Tech Valley to become a global hub for agriculture and food technology, according to project head Ahmed Al Shaibani. The initiative brings together the entire food ecosystem with top-tier infrastructure, business support, and innovation programs to empower farmers, researchers, entrepreneurs, and businesses. Its aim is to tackle global food security and drive sustainable food production that redefines how the world produces and consumes food.

Fluctuating Feedstock Supply and Quality

The GCC liquid CO₂ market faces significant restraints due to fluctuating feedstock supply and inconsistent quality, primarily because the region’s liquid CO₂ production is heavily reliant on by-products from hydrocarbon-intensive industries such as petrochemicals, ammonia, ethanol, and hydrogen production. Any disruption or variability in these upstream sectors directly impacts the volume, purity, and consistency of liquid CO₂ supply, thereby creating a bottleneck for end-use industries.

For instance, in Saudi Arabia, fluctuations in natural gas processing and oil refining operations — due to scheduled maintenance or unexpected plant outages often lead to reduced CO₂ recovery rates. Since CO₂ is not the primary product but a by-product, its availability becomes secondary to the main operations. This was evident in 2022 when temporary shutdowns at several industrial gas plants impacted liquid CO₂ supplies to food and beverage processors in the Eastern Province, forcing them to delay production.

Therefore, the GCC liquid CO₂ market is hindered by its dependence on volatile and uneven feedstock sources, resulting in irregular availability and quality inconsistencies. These issues challenge supply chain reliability, limit industrial applications, and increase the operational risks and costs for both suppliers and end-users.

Segmentation Analysis

GCC liquid carbon di-oxide market is segmented based on application and country.

Significant Market Share of Food and Beverages in the Market Driven by Its Extensive Use in Carbonation, Preservation, and Packaging

The food and beverage sector holds a significant share in the GCC liquid carbon dioxide market, driven by a rapidly evolving consumption landscape. In recent years, carbonated drinks have seen a sharp rise in demand, particularly in countries like Qatar, where a 2024 NIH survey revealed that 26.8% of people consume soft drinks three or more times a day—the highest rate recorded globally. This strong preference for fizzy beverages has fueled an increasing demand for carbon dioxide in beverage carbonation processes. At a regional scale, the Arab beverage industry caters to approximately 300 million consumers and produces nearly 10 billion liters annually, as noted in the Eighth Arab Beverages Conference. This massive production volume directly supports the rising utilization of carbon dioxide in food and beverage manufacturing, preservation, and cold-chain distribution.

To meet this growing need sustainably, Saudi Arabia has taken a bold step by launching its first carbon capture and utilization facility in Rabigh. In December 2023, a collaboration between Petro Rabigh and Gulf Cryo, the plant captures emissions and processes them into high-purity, food-grade liquid carbon dioxide, which is then redistributed to industries such as food and beverage.

Similarly, Qatar is accelerating its green initiatives through a partnership between QatarEnergy and General Electric in September 2022 to develop a national carbon capture roadmap. As part of a US$50 billion investment, Qatar aims to establish a large-scale carbon hub at Ras Laffan Industrial City, home to more than 80 gas turbines. With this strategy, Qatar not only strengthens its climate leadership but also ensures a steady, eco-friendly supply of carbon dioxide for key sectors.

Country Penetration

Saudi Arabia Holds a Significant Share in the Liquid Carbon Dioxide Market Due to Its Expanding Industrial and Energy Sectors

Saudi Arabia plays a prominent role in the liquid carbon dioxide (CO₂) market across the Gulf Cooperation Council (GCC), owing to its expansive industrial base, petrochemical capacity, and large-scale carbon capture operations. Saudi Arabia, which dominates the industrial gas sector in the region, contributes the largest share of this demand, driven by widespread usage in enhanced oil recovery (EOR), food processing, beverage carbonation, and industrial gas applications.

Saudi Arabia is also actively scaling up its carbon capture, utilization, and storage (CCUS) infrastructure, which will significantly increase demand for liquefied CO₂. The Ministry of Energy has publicly announced a multi-phase project to establish a major CCUS hub in Jubail Industrial City with a target capacity of 9 million tonnes per annum (Mtpa) by 2027. This is part of a larger national strategy that aims to capture, utilize, or store 11 Mtpa of CO₂ by 2035, with the ultimate goal of reaching 44 Mtpa by the same year. These initiatives align with the objectives of the Saudi Green Initiative and Vision 2030, which emphasize reducing carbon intensity and developing low-carbon industrial value chains.

Saudi Arabia’s climate policy framework also plays a pivotal role in encouraging the utilization and processing of CO₂. As part of its commitment under the Saudi Green Initiative, the country has pledged to reduce or avoid 278 million tons of carbon dioxide equivalent (MtCO₂eq) annually by 2030. In addition, it is aiming to reach net-zero carbon emissions by 2060. These targets are being pursued through active investments in low-carbon technologies, including CCUS. The government’s regulatory environment supports liquid CO₂ projects through incentives, permitting, and infrastructure support, thereby strengthening its role in the regional CO₂ economy.

Sustainability Analysis

The GCC liquid carbon dioxide (CO₂) market is increasingly aligning with global sustainability goals, driven by national commitments to reduce greenhouse gas emissions, promote circular carbon economies, and build environmentally responsible industries. One of the most significant sustainability aspects of the market lies in its integration with carbon capture, utilization, and storage (CCUS) initiatives.

For instance, the Al Reyadah facility in Abu Dhabi, operated by ADNOC, captures over 800,000 tons of CO₂ annually from steel production and repurposes it for enhanced oil recovery (EOR) and industrial use, thereby transforming emissions into valuable inputs.

Similarly, Gulf Cryo’s carbon capture plant in Rabigh, Saudi Arabia, captures CO₂ from a monoethylene glycol plant and liquefies it for commercial supply, reducing 100,000 metric tons of CO₂ emissions annually. These facilities not only mitigate industrial emissions but also support a circular economy by enabling the reuse of CO₂ across sectors such as food, beverages, and chemicals.

Moreover, the production and utilization of food-grade liquid CO₂ supports sustainable practices in the food industry. By enabling Modified Atmosphere Packaging (MAP) and dry ice-based refrigeration, liquid CO₂ helps extend shelf life, reduce food spoilage, and support energy-efficient cold chains key to minimizing food waste. Countries like the UAE and Saudi Arabia, through initiatives like Food Tech Valley and the Jeddah Food Cluster, are incorporating CO₂ technologies into their broader food security strategies to promote sustainable, locally sourced food systems.

Competitive Landscape

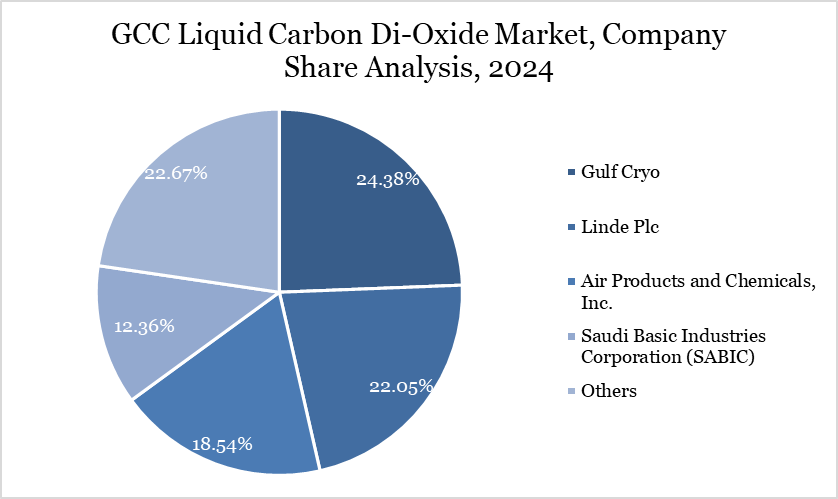

The major players in the market include Air Products and Chemicals, Inc., Gulf Cryo, Arabia Gas Company, National Industrial Gas Plants (NIGP), Sharjah Oxygen Company (SOC), Axcel Gases, Saudi Basic Industries Corporation (SABIC), Linde Plc, and Buzwair Industrial Gases.

Key Developments

- In 2026, the GCC liquid carbon dioxide market continued growing steadily, supported by expanding demand across food & beverage, healthcare, industrial, and chemicals applications as regional industries increased usage of high‑purity CO₂ for carbonation, preservation, refrigeration, and specialty processes.

- In 2026, sustainability trends and regional decarbonization initiatives such as carbon capture, utilization, and storage (CCUS) investments boosted the availability of purified CO₂ infrastructure and enhanced the long‑term viability of liquid CO₂ supply chains in industrial hubs like Jubail and Ras Laffan.

- In early 2026, governments and industrial stakeholders emphasized establishing integrated CO₂ capture and utilization hubs near refineries, petrochemical clusters, and industrial zones to secure reliable feedstock and support emerging low‑carbon applications such as enhanced oil recovery (EOR) and industrial fermentation.

- In late 2025, the GCC liquid CO₂ market was valued at approximately US$253.7 million in 2024 and was projected to grow at a 10.6% CAGR through 2032, with an expected market size of around US$564.5 million by that year.

- In 2025, key regional developments included Saudi Arabia’s carbon capture plant launch in Rabigh, where Gulf Cryo partnered with Petro Rabigh to produce high‑purity liquid CO₂ about 300 metric tons per day helping reduce emissions and supply merchant CO₂ across industries.

- In 2025, strategic investments were highlighted with initiatives such as Qatar’s large‑scale carbon hub project at Ras Laffan Industrial City (part of a broader US$50 billion national carbon roadmap), aimed at ensuring a stable, eco‑efficient liquid CO₂ supply for industrial applications.

- In 2025, the food & beverage sector remained the dominant application in the region driven by carbonation, modified atmosphere packaging, preservation, and dry‑ice logistics while oil & gas, medical, and industrial uses continued contributing to overall market demand.

Why Choose DataM?

Data-Driven Insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. This approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. This personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. These insights complement and go beyond what is typically available in generic databases.

Target Audience 2026

Manufacturers/ Buyers

Industry Investors/Investment Bankers

Research Professionals

Emerging Companies