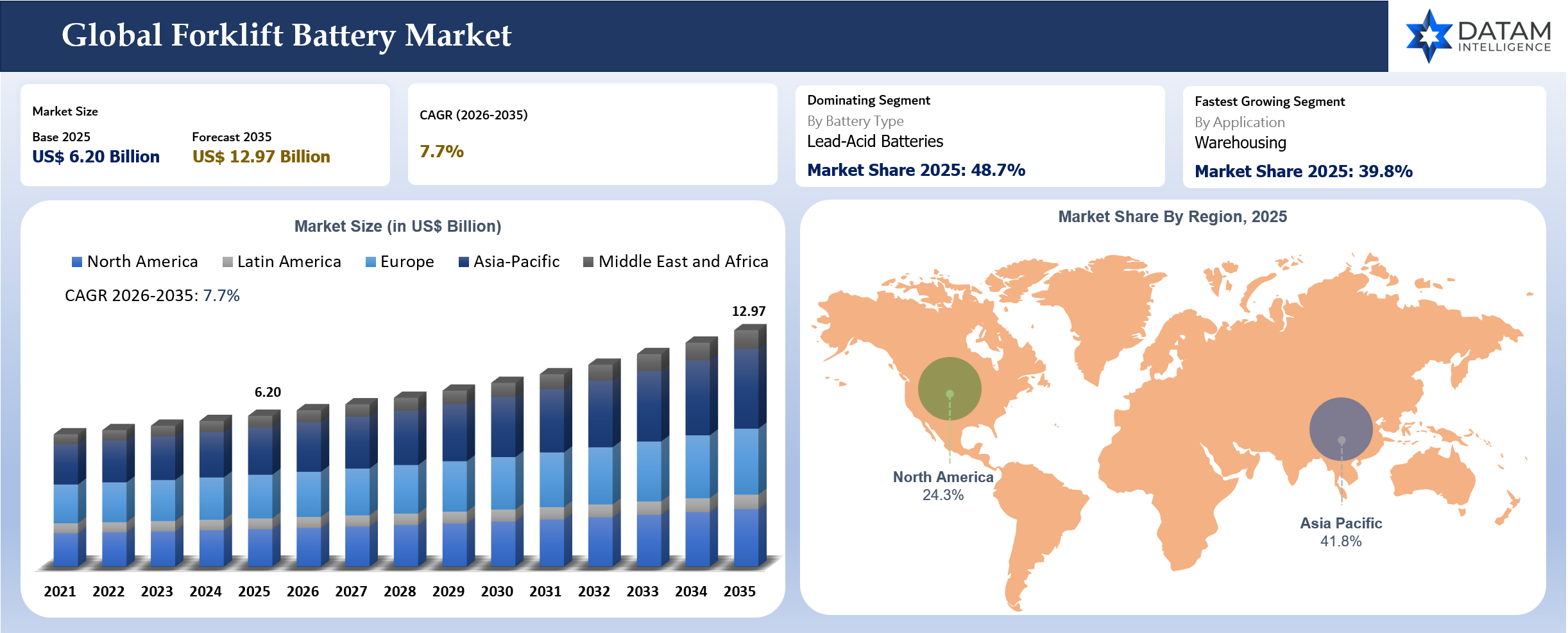

Forklift Battery Market Size

The global forklift battery market stood at US$ 6.20 billion in 2025 and is expected to reach US$ 12.97 billion by 2035, growing with a CAGR of 7.7% during the forecast period 2026-2035.

The global forklift battery market is undergoing rapid transformation as warehouses, logistics fleets, manufacturing facilities, and distribution centers accelerate electrification initiatives to improve operational efficiency, reduce carbon emissions, and lower long-term operating costs. The expansion of e-commerce, automated material handling systems, and smart warehouse infrastructure is significantly increasing demand for electric forklifts powered by advanced lithium-ion and lead-acid battery technologies. Industrial operators are increasingly replacing internal combustion forklifts with battery-powered alternatives due to tightening emission regulations, rising fuel prices, and corporate sustainability targets. Battery manufacturers are simultaneously investing in fast-charging systems, battery swapping infrastructure, and high-cycle-life chemistries to support 24/7 warehouse operations and autonomous logistics fleets.

Lithium-ion technology is emerging as the dominant trend across the forklift battery ecosystem because of its longer operating life, opportunity charging capability, lower maintenance requirements, and higher energy efficiency compared to conventional lead-acid systems. According to the International Energy Agency (IEA), global battery manufacturing capacity exceeded 3 TWh in 2024 and continues expanding rapidly due to electrification across transport and industrial sectors. The IEA also reported that global battery deployment surpassed the 1 TWh milestone in 2024, highlighting the massive scale-up of battery supply chains supporting electric mobility and industrial electrification. Falling lithium-ion battery costs are further accelerating forklift fleet conversion, with the IEA noting battery pack prices in China declined nearly 30% in 2024, improving affordability for industrial equipment manufacturers and warehouse operators.

China remains the center of global battery production, accounting for more than 80% of global battery manufacturing capacity in 2025 according to the IEA, enabling large-scale supply of industrial batteries for electric forklifts, automated guided vehicles (AGVs), and warehouse robotics systems. Rapid industrial battery investments are reshaping the competitive landscape, with governments and manufacturers expanding localized battery production facilities to secure supply chains and reduce dependence on imports. The IEA highlighted that manufacturing capacity in the United States grew by nearly 50% in 2024 while India and Southeast Asia are rapidly scaling battery production infrastructure through new gigafactory investments.

Key Takeaways

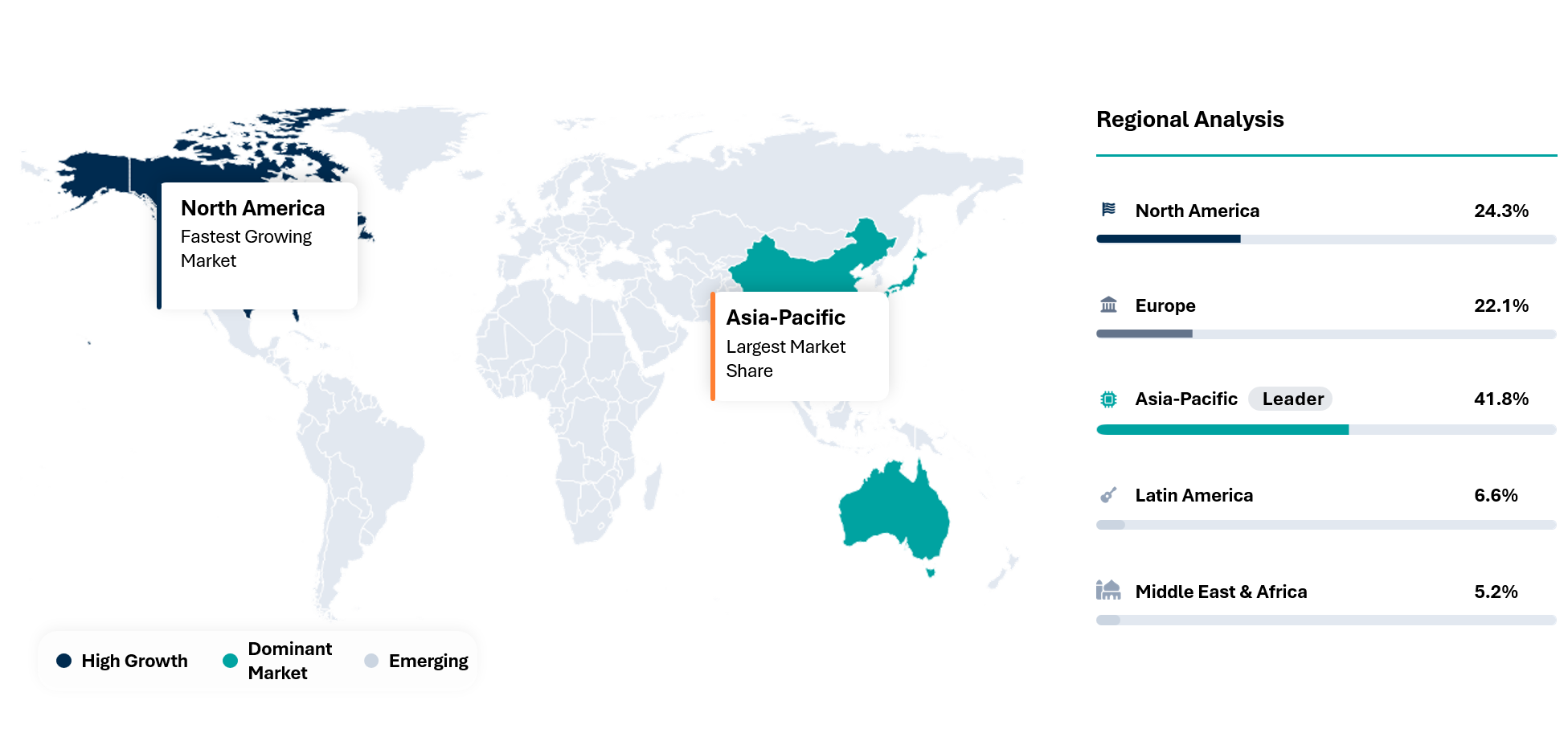

- Asia-Pacific is dominating the global forklift battery market, accounting for a share of 41.8% in 2025, while North America is forecast to register a CAGR of 6.9% between 2026 and 2035.

- In 2025, lead-acid batteries led the market with a share of approximately 48.7% due to their longer operational life, faster charging capability, and lower maintenance requirements across warehouse and logistics applications.

- The growing expansion of e-commerce warehousing, automated distribution centers, and electric material handling fleets is a major driver accelerating demand for advanced forklift battery technologies globally.

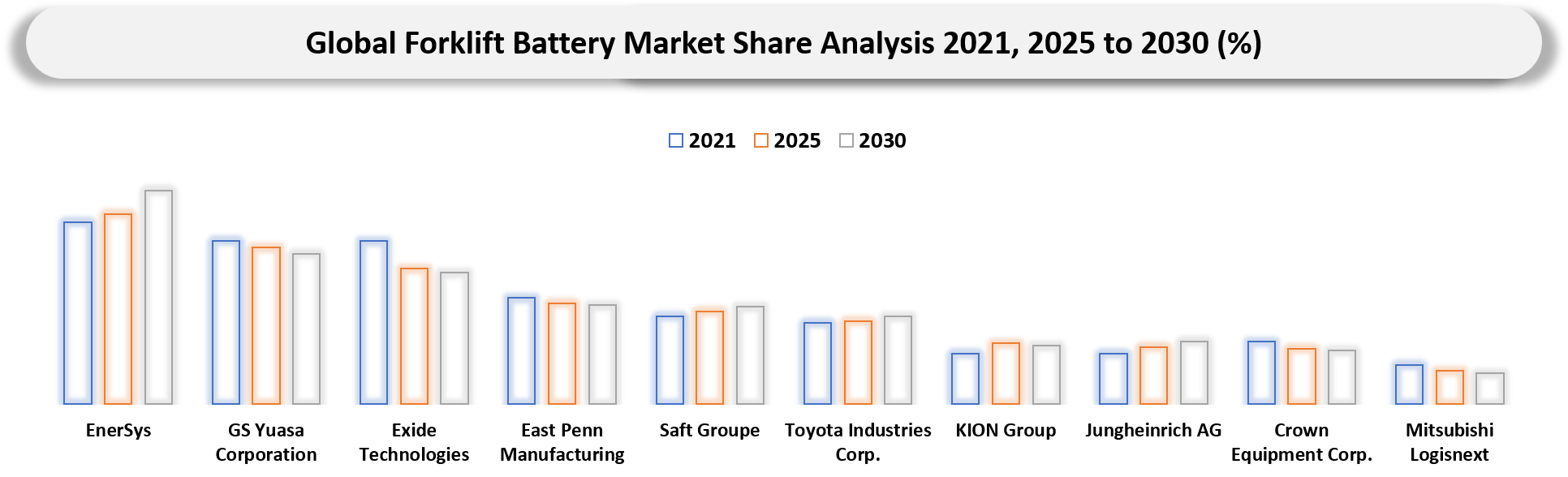

- Toyota Industries Corporation, Crown Equipment Corporation, and EnerSys have established themselves as leading players in the market through continuous advancements in lithium-ion battery systems, fast-charging technologies, strategic partnerships, and expansion of sustainable warehouse electrification solutions.

Forklift Battery Industry Trends and Strategic Insights

- With global warehouse automation accelerating and e-commerce companies expanding fulfillment capacity, electric forklifts are replacing propane and diesel-based fleets at a rapid pace. Lithium-ion battery systems are increasingly preferred because they support opportunity charging, eliminate battery swapping requirements, and improve fleet uptime.

- Asia-Pacific dominated the forklift battery market in 2025 due to strong battery manufacturing capabilities, industrial electrification policies, and the rapid expansion of logistics infrastructure across China, India, Vietnam, and Indonesia.

- Lithium iron phosphate (LFP) batteries are emerging as the dominant chemistry in forklift applications because of their thermal stability, long operational lifespan, and safety advantages in high-cycle industrial environments. Industrial operators are also integrating smart battery management systems (BMS), cloud-based fleet monitoring, and AI-driven energy optimization technologies to improve battery performance and reduce downtime in warehouse operations.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 6.20 Billion | |

| 2035 Projected Market Size | US$ 12.97 Billion | |

| CAGR (2026-2035) | 7.7% | |

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Battery Type | Lead-Acid Batteries, Lithium-Ion Batteries, Nickel-Based Batteries, Emerging Battery Technologies | |

| By Forklift Class | Class I – Electric Motor Rider Trucks, Class II – Electric Narrow Aisle Trucks, Class III – Electric Hand Trucks, Class IV – Internal Combustion Cushion Tire Forklifts, Class V – Internal Combustion Pneumatic Tire Forklifts | |

| By Voltage Capacity | Low Voltage Batteries (Below 24V), Medium Voltage Batteries (24V - 48V), High Voltage Batteries (Above 48V) | |

| By Battery Capacity | Low Capacity (Below 200 Ah), Medium Capacity (200 - 600 Ah), High Capacity (Above 600 Ah) | |

| By Charging Technology | Conventional Charging, Fast Charging, Opportunity Charging, Wireless Charging, Smart Charging Systems | |

| By Application | Warehousing, Manufacturing, Logistics & Freight, Retail & E-Commerce, Construction, Mining, Food & Beverage, Pharmaceuticals, Others | |

| By End-User | Industrial Sector, Commercial Sector, Government & Public Sector, SMEs, Large Enterprises, Others | |

| By Sales Channel | OEM Sales, Aftermarket Sales, Distributor Sales, Online Sales | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Why this report matters in 2026?

The global forklift battery market is entering a high-growth transformation phase in 2026 as warehouse automation, electrified material handling operations, and industrial decarbonization strategies accelerate across logistics, manufacturing, retail, ports, and e-commerce sectors. Rising regulatory pressure to reduce diesel-powered industrial equipment emissions, combined with increasing investments in smart warehouses and battery-powered fleet modernization, is intensifying global demand for advanced forklift battery technologies. Governments and industrial operators across the U.S., China, Germany, Japan, South Korea, and other major manufacturing economies are prioritizing electric forklift adoption to improve operational efficiency, reduce carbon footprints, and support sustainable supply chain infrastructure. This transition is rapidly shifting the market from conventional lead-acid dependency toward technologically advanced lithium-ion and fast-charging energy storage ecosystems with stronger long-term commercial scalability.

At the same time, forklift battery manufacturers and energy solution providers are facing growing pressure to deliver higher energy density, faster charging capability, longer operational life cycles, and lower total cost of ownership amid increasing fleet electrification requirements. Rapid advancements in lithium-ion chemistries, battery management systems (BMS), opportunity charging technologies, hydrogen fuel cell integration, and intelligent fleet energy monitoring platforms are reshaping competitive dynamics across the industry. Buyers, logistics operators, warehouse integrators, and industrial fleet owners now require deeper visibility into charging infrastructure compatibility, battery replacement economics, energy efficiency performance, safety compliance standards, thermal management capabilities, lifecycle durability, and strategic supply chain partnerships to evaluate long-term operational reliability, optimize fleet productivity, and reduce energy transition risks in increasingly automated material handling environments.

Strategic Indicators For Forklift Battery

High Regulation Impact

The global forklift battery market is facing intensified regulatory scrutiny as lithium-ion localization mandates, battery recycling obligations, and carbon reporting standards reshape procurement economics across the U.S., China, Germany, Japan, and India. The U.S. Inflation Reduction Act and Department of Energy localization incentives are accelerating domestic lithium battery manufacturing for material-handling equipment, while the EU Battery Regulation is increasing compliance costs through mandatory digital battery passports and recycled-content thresholds. China continues tightening environmental inspections on lead-acid battery recycling clusters, directly impacting export-oriented suppliers. India’s Battery Waste Management Rules are forcing organized recycling partnerships among industrial battery OEMs supplying warehouse and logistics operators.

High Investment Activity

Investment activity in the forklift battery market accelerated sharply during 2025 as industrial electrification and warehouse automation spending expanded globally. The United States emerged as a strategic investment hub after EnerSys finalized a US$199 million U.S. DOE-backed lithium-ion gigafactory agreement in South Carolina to strengthen domestic industrial battery supply chains for logistics and defense applications. India is attracting large-scale manufacturing investments as multinational battery firms establish localized production to support rapid forklift electrification in warehousing and e-commerce logistics. China continues expanding lithium iron phosphate (LFP) industrial battery capacity, while Germany and Sweden remain central to advanced battery engineering and recycling ecosystem investments.

New Product Launches

- January 17, 2025: EnerSys secured final approval for a US$199 million U.S. DOE award supporting its lithium-ion gigafactory in South Carolina, targeting industrial motive-power batteries for forklifts, warehousing fleets, and defense logistics applications.

- February 13, 2025: Eternity Technologies acquired EnerSys India Batteries’ Vijayawada manufacturing facility to expand localized industrial battery production supporting India’s growing electric forklift and warehouse electrification demand.

Supply Chain Disruption

The forklift battery supply chain remains exposed to lithium carbonate volatility, graphite processing concentration in China, Red Sea shipping disruptions, and tightening environmental audits across Asian lead recycling hubs. China dominates refining and industrial battery component processing, creating procurement vulnerabilities for European and North American forklift OEMs. India and Southeast Asia are increasingly used as alternative assembly and sourcing bases to reduce geopolitical exposure. U.S. logistics operators are prioritizing localized lithium battery procurement following tariff uncertainty and industrial policy shifts. Simultaneously, stricter transportation compliance for hazardous battery materials is increasing warehousing and freight costs across Germany, the U.S., and Japan, extending industrial battery lead times.

Pricing Volatility

Forklift battery pricing remains highly volatile due to fluctuating lithium carbonate, nickel sulfate, lead, and industrial-grade graphite costs. Chinese oversupply in EV batteries temporarily softened lithium-ion pack pricing during early 2025, but industrial forklift battery pricing remained elevated because of localized manufacturing investments, freight inflation, and compliance-related certification costs. Lead-acid battery suppliers in India and Southeast Asia continue facing margin pressure from inconsistent recycled lead availability and tightening environmental controls. In Europe, energy-intensive battery manufacturing operations are experiencing persistent cost pressure from elevated electricity tariffs. U.S. warehouse operators increasingly prefer long-life lithium batteries despite higher upfront pricing because lifecycle operating costs remain comparatively lower.

Procurement Pressure

Large logistics operators across the U.S., Germany, China, and India are exerting intense procurement pressure on forklift battery suppliers to guarantee lifecycle performance, localized servicing capability, and ESG compliance simultaneously. Warehouse automation growth is increasing demand for opportunity-charging lithium batteries with minimal downtime, forcing suppliers to secure long-term raw material agreements and regional assembly capacity. Procurement teams are prioritizing vendors with domestic manufacturing footprints to mitigate tariff exposure and geopolitical risks. Additionally, e-commerce and third-party logistics companies are demanding integrated battery analytics, predictive maintenance software, and recycling traceability within procurement contracts, significantly increasing supplier qualification complexity across global industrial battery tenders.

New Technology Adoption

Technology adoption in the forklift battery market is accelerating toward lithium iron phosphate (LFP), AI-enabled battery management systems, cloud-based fleet diagnostics, and ultra-fast charging architectures. The United States and Germany are leading deployment of predictive battery analytics integrated with warehouse automation systems, while China dominates cost-efficient LFP manufacturing scale. Japanese manufacturers continue investing in high-cycle industrial battery chemistry improvements for heavy-duty logistics operations. Indian warehouse operators are increasingly adopting maintenance-free lithium batteries to reduce labor-intensive battery room operations. Smart charging infrastructure integrated with autonomous forklifts and energy management software is becoming a competitive differentiator among global material-handling fleet operators.

Regional Expansion Opportunity

- North America remains the strongest regional expansion opportunity due to aggressive warehouse automation investments, Inflation Reduction Act incentives, and rapid adoption of lithium-powered forklift fleets across e-commerce, retail logistics, and defense warehousing operations. Domestic battery localization strategies are reshaping supplier partnerships and procurement priorities.

- Asia-Pacific offers the fastest industrial expansion opportunity driven by China’s battery manufacturing dominance, India’s logistics infrastructure modernization, and Southeast Asia’s emergence as an alternative industrial production hub supporting electric forklift adoption across export-oriented manufacturing ecosystems.

Government Policy Support

Government support for forklift battery manufacturing strengthened considerably during 2025 as industrial electrification became strategically linked to supply-chain resilience and energy transition policies. The U.S. Department of Energy expanded support for domestic lithium-ion manufacturing under industrial decarbonization initiatives, directly benefiting motive-power battery suppliers. Europe’s Battery Regulation is accelerating sustainable battery recycling and traceability investments across Germany and France. China continues supporting industrial electrification through manufacturing subsidies and localized battery supply-chain incentives. India’s Production Linked Incentive ecosystem, battery waste management framework, and warehousing modernization initiatives are encouraging multinational industrial battery companies to establish domestic assembly and recycling partnerships supporting electric material-handling fleets.

Import, Export, and Pricing Intelligence

Global forklift battery trade flows are increasingly shifting toward regionalized supply chains as geopolitical tensions and industrial policies reshape sourcing strategies. China remains dominant in lithium-ion battery component exports, while the U.S. and Europe are actively reducing dependence through localized manufacturing investments. India is emerging as a secondary industrial battery export hub serving Middle East and Southeast Asian logistics markets.

Industrial battery pricing negotiations are increasingly structured around lifecycle economics rather than upfront procurement costs. Lithium-ion forklift batteries continue commanding premium pricing because warehouse operators prioritize energy efficiency, lower maintenance, and reduced downtime. Lead-acid pricing remains vulnerable to recycled lead availability and environmental compliance costs, particularly across India, China, and Eastern European manufacturing ecosystems.

| HS Code | Reporter | Trade Flow | 2025 Trade Value | Interpretation |

| HS 850760 | China | Export | USD 68.4 Billion | China maintains dominant lithium-ion battery export leadership supporting global forklift and industrial vehicle battery supply chains |

| HS 850720 | United States | Import | USD 5.1 Billion | U.S. industrial battery imports remain elevated due to warehouse electrification and domestic supply shortages |

| HS 850720 | Germany | Import | USD 3.4 Billion | Germany’s logistics automation and industrial electrification continue driving advanced motive-power battery imports |

| HS 850720 | Japan | Export | USD 1.9 Billion | Japan continues exporting high-performance industrial batteries for premium warehouse and automated logistics operations |

Company Coverage Preview

EnerSys remains one of the most strategically positioned companies in the global forklift battery market due to its vertically integrated industrial battery ecosystem, strong motive-power portfolio, and aggressive lithium-ion expansion strategy. The company is strengthening North American supply-chain localization through its South Carolina lithium gigafactory initiative supported by the U.S. Department of Energy. EnerSys benefits from deep relationships with warehouse automation operators, logistics companies, and industrial fleet managers across more than 100 countries. Its increasing focus on fast-charging lithium systems, predictive battery analytics, and maintenance-free motive-power platforms positions the company competitively against Asian lithium battery manufacturers targeting global warehouse electrification opportunities.

AI Impact Analysis

Artificial intelligence is transforming the forklift battery market through predictive maintenance, intelligent charging optimization, fleet energy analytics, and warehouse automation integration. Battery manufacturers are embedding AI-driven battery management systems capable of monitoring temperature, charge cycles, degradation rates, and operational efficiency in real time. Large warehouse operators in the U.S., Germany, and China are deploying AI-enabled fleet orchestration platforms that optimize forklift battery utilization and charging schedules to reduce downtime and electricity costs. AI is also improving demand forecasting and raw-material procurement planning for battery manufacturers facing supply-chain volatility. Advanced analytics increasingly support battery lifecycle extension, recycling traceability, and energy-efficiency benchmarking across industrial logistics ecosystems.

Disruption Analysis

Traditional lead-acid battery systems are increasingly being replaced by lithium-ion technologies due to advantages including faster charging cycles, reduced maintenance requirements, higher energy efficiency, and longer operational lifespan. This shift is fundamentally altering supplier dynamics, manufacturing investments, and procurement strategies within logistics and material handling industries. Major disruptions are particularly visible in China, the United States, Germany, and Japan, where automated warehouses and e-commerce fulfillment centers are accelerating demand for intelligent battery management systems and opportunity charging infrastructure.

Another disruptive factor is the integration of IoT-enabled battery monitoring platforms and AI-driven fleet energy optimization systems. Companies are increasingly adopting connected forklift ecosystems capable of real-time battery diagnostics, predictive maintenance, and energy utilization analytics. Simultaneously, stricter emission reduction policies and corporate ESG targets are forcing distribution centers and manufacturing facilities to transition toward fully electric forklift fleets. Battery swapping technologies, ultra-fast charging systems, and second-life battery applications are also reshaping operational economics across large warehouse operators.

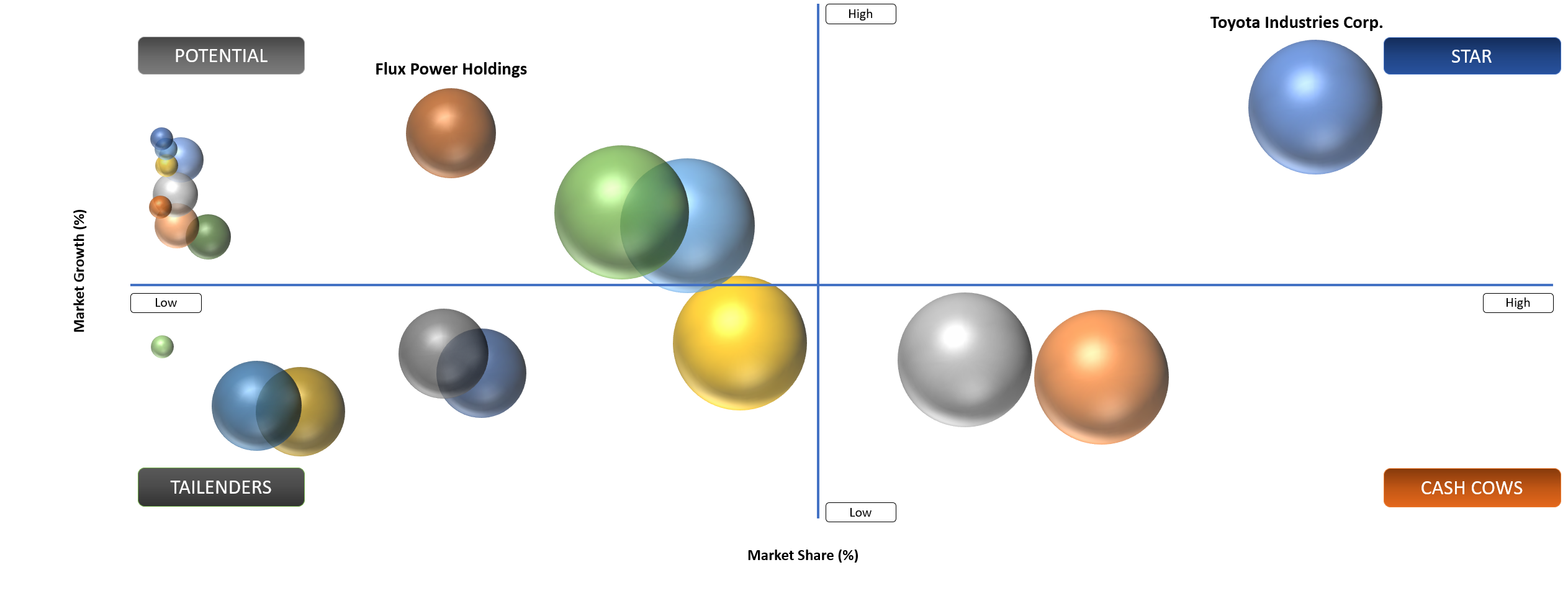

BCG Matrix: Company Evaluation

STAR

The star players in the global forklift battery market are dominated by technologically advanced and vertically integrated manufacturers such as Toyota Industries Corporation, EnerSys, Exide Industries, BYD Company, and GS Yuasa Corporation. The companies maintain strong market positions due to extensive lithium-ion battery investments, large-scale manufacturing capabilities, and strategic partnerships with warehouse automation providers and OEM forklift manufacturers. Their dominance is reinforced by rising demand from e-commerce logistics, automated warehousing, and electric material handling equipment. Toyota and BYD are particularly benefiting from integrated electric forklift ecosystems, while EnerSys continues expanding fast-charging and maintenance-free battery technologies.

POTENTIAL

Potential players in the global forklift battery market include emerging energy storage and lithium battery specialists such as Flux Power Holdings, Microvast Holdings, Leoch International Technology, Tianneng Battery Group, and Crown Battery Manufacturing. The companies are gradually increasing market penetration through specialized lithium-ion solutions, modular battery platforms, and rapid charging technologies tailored for warehouse fleets and industrial logistics operations. Their growth potential is strongly linked to the accelerating transition away from lead-acid batteries and the expansion of smart warehouses across Asia-Pacific and North America. Many of these firms are securing opportunities through niche applications, fleet electrification projects, and partnerships with regional forklift manufacturers.

Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

Increasing Adoption of Electric Forklifts Across Warehousing and Logistics Operations | 5.20% | North America, Europe, China, Japan, and major e-commerce fulfillment hubs | Electric material handling, warehouse automation, indoor logistics operations | Accelerates transition from internal combustion forklifts to battery-powered fleets, driving large-scale battery replacement and procurement demand |

Expanding E-commerce, Retail Distribution, and Cold Storage Infrastructure | 4.90% | Asia-Pacific, North America, and Western Europe logistics corridors | High-throughput warehouse operations, pallet transportation, cold chain material handling | Strengthens demand for high-performance forklift batteries capable of supporting continuous multi-shift operations and energy-efficient fleet management |

Rising Investments in Lithium-Ion Battery Technology and Fast-Charging Infrastructure | 4.70% | Advanced manufacturing economies and industrial automation ecosystems | Fast-charging forklifts, automated guided vehicles (AGVs), smart warehouse fleets | Enhances operational efficiency, reduces charging downtime, and supports broader adoption of lithium-ion forklift battery systems |

Growing Sustainability Regulations and Industrial Decarbonization Initiatives | 4.40% | European Union, U.S., China, and industrial manufacturing clusters | Zero-emission warehouse operations, green logistics, sustainable manufacturing facilities | Encourages enterprises to replace lead-acid batteries with energy-efficient and low-maintenance battery technologies, supporting long-term electrification strategies |

Rising Electrification of Warehousing and Logistics Operations

The forklift battery market is expanding rapidly because global warehouse operators are aggressively electrifying their material handling fleets. The continued growth of e-commerce, third-party logistics providers, and automated distribution centers is driving large-scale deployment of electric forklifts equipped with lithium-ion batteries. Modern warehouses increasingly operate 24/7 multi-shift systems, making fast-charging and maintenance-free batteries essential for operational continuity.

In North America and Europe, major retailers and logistics companies are modernizing warehouse fleets to comply with emission reduction targets and indoor air quality standards. According to industry estimates, electric mobility applications accounted for more than 55% of forklift battery deployments in 2024, reflecting the shift away from internal combustion equipment. In addition, Chinese battery manufacturers and forklift OEMs are rapidly scaling production capacity for industrial lithium-ion systems to meet growing demand from logistics parks and export-oriented manufacturing hubs.

The growing adoption of automated guided vehicles (AGVs), autonomous forklifts, and robotics-assisted warehouse systems is further increasing demand for intelligent high-density battery platforms. Battery suppliers are increasingly focusing on ultra-fast charging, modular battery architecture, and predictive maintenance technologies that minimize operational interruptions in large-scale fulfillment centers.

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

High Initial Investment and Battery Replacement Costs | 4.50% | Fleet electrification economics and capital budgeting | Electric forklift fleet deployment in warehouses, ports, and manufacturing facilities | Slows battery transition among cost-sensitive SMEs and delays replacement cycles in developing markets |

Limited Charging Infrastructure and Long Charging Downtime | 4.00% | Operational productivity and fleet utilization efficiency | Multi-shift warehouse operations, high-throughput logistics centers | Reduces operational continuity and restricts adoption in intensive material handling environments |

Volatility in Lithium, Lead, and Nickel Raw Material Prices | 3.90% | Battery manufacturing costs and supply chain stability | Lithium-ion and lead-acid forklift battery production | Creates pricing uncertainty for OEMs and fleet operators, impacting procurement planning and long-term contracts |

Limited Availability of Battery Recycling and Skilled Maintenance Ecosystem | 3.50% | Aftermarket serviceability and sustainability compliance | Industrial battery maintenance, recycling, and lifecycle management | Slows circular economy adoption and increases operational risks associated with battery disposal and servicing |

High Initial Costs and Charging Infrastructure Challenges

A major challenge facing the global forklift battery market is the high upfront investment associated with lithium-ion battery systems and industrial charging infrastructure. Although lithium-ion batteries offer lower lifetime operating costs compared to lead-acid batteries, the initial capital expenditure remains significant for small and medium-sized warehouse operators. Large-scale electrification projects often require charging stations, upgraded electrical infrastructure, energy management systems, and workforce training programs, increasing implementation complexity.

Heavy-duty warehouse operations running continuous shifts also require robust charging infrastructure capable of supporting high-power charging cycles without overloading facility grids. Industrial operators in emerging economies continue to rely heavily on lead-acid batteries because of lower acquisition costs and established servicing ecosystems. Additionally, supply chain volatility involving lithium, nickel, cobalt, and graphite continues to impact battery manufacturing economics and long-term procurement planning.

Safety concerns around thermal runaway, battery disposal, and fire risks in high-capacity lithium-ion systems also remain important operational considerations for warehouse operators. Several industrial users continue evaluating hydrogen fuel-cell forklifts as an alternative for high-utilization environments requiring rapid refueling and continuous operation. Research into hydrogen-powered forklifts and industrial fuel-cell systems is increasing, particularly in North America, Japan, and South Korea.

Segmentation Analysis

The global forklift battery market is segmented based on the battery type, forklift class, voltage capacity, battery capacity, charging technology, application, end-user, sales channel and region.

Lithium-Ion Battery Segment Leads Market Expansion

Lithium-ion batteries are becoming the fastest-growing segment within the global forklift battery market because they significantly improve productivity, charging efficiency, and fleet utilization. Unlike traditional lead-acid systems, lithium-ion batteries support partial charging during work breaks without affecting battery lifespan, allowing forklifts to operate continuously across multiple shifts.

Lithium iron phosphate (LFP) batteries are particularly gaining traction in warehouse and manufacturing applications because of their superior thermal stability and long cycle life. Industry analysis indicates that LFP chemistry accounted for more than half of lithium-ion forklift battery deployments in 2024. Battery manufacturers are increasingly investing in advanced BMS technologies, cloud analytics platforms, and intelligent charging systems to optimize fleet performance and reduce maintenance costs.

Several battery manufacturers are also expanding industrial battery production capacity worldwide. In India, Ola Cell Technologies announced investments exceeding ₹2,200 crore toward lithium-ion cell manufacturing expansion, reflecting broader industrial momentum toward localized battery production ecosystems. Similar investments are being observed across China, Europe, and the United States as governments prioritize battery supply chain localization and industrial electrification.

Hydrogen Fuel-Cell Forklifts Gain Attention in Heavy-Duty Applications

Hydrogen-powered forklifts are increasingly being explored for large-scale industrial operations that require rapid refueling and uninterrupted operations. Hydrogen fuel-cell forklifts eliminate long charging times and can operate continuously in heavy-duty logistics environments such as ports, cold storage facilities, and large distribution centers.

Research programs supported by the U.S. Department of Energy (DOE) and industrial partners continue advancing hydrogen forklift technologies. Hydrogen forklifts are particularly attractive for facilities operating large fleets where battery charging infrastructure may become operationally restrictive. Companies are also evaluating hydrogen systems for container handling equipment and high-capacity forklifts used in shipping yards and industrial manufacturing plants.

South Korean and Japanese industrial equipment manufacturers are actively developing hydrogen-powered forklift platforms as part of broader hydrogen economy strategies. However, hydrogen infrastructure costs, storage complexity, and fuel availability remain major barriers to widespread commercial deployment

Geographical Penetration

U.S. Forklift Battery Market Landscape

The United States forklift battery market is experiencing strong transformation due to rapid warehouse electrification, rising e-commerce fulfillment activity, and aggressive investments in domestic battery manufacturing infrastructure. Large distribution operators including Walmart, Amazon, and third-party logistics providers are accelerating deployment of electric forklifts to improve operational efficiency and reduce emissions from internal combustion material handling fleets. The growing preference for lithium-ion forklift batteries is particularly visible across high-throughput warehouses because opportunity charging reduces downtime and eliminates battery swap rooms. According to the U.S. Department of Energy (DOE), the federal government finalized a US$2.5 billion loan program for Ultium Cells battery manufacturing facilities in Ohio, Tennessee, and Michigan to strengthen domestic lithium-ion battery supply chains and create more than 11,000 jobs. In parallel, battery recycling and localized cathode production investments are increasing across Nevada, North Carolina, and South Carolina to reduce dependence on imported battery materials. The United States is also witnessing rising adoption of automated guided vehicles (AGVs) and autonomous forklifts across manufacturing and retail logistics operations, further boosting demand for intelligent battery management systems and fast-charging industrial batteries.

Another important trend shaping the U.S. forklift battery market is the transition toward energy-efficient and maintenance-free lithium iron phosphate (LFP) battery systems for indoor warehouse operations. Industrial operators are prioritizing batteries capable of multi-shift operations, faster charging cycles, and lower total lifecycle costs. Federal clean-energy incentives and battery manufacturing support programs are encouraging domestic production of industrial battery cells, modules, and recycling infrastructure. Recent DOE-backed initiatives and battery investments exceeding several billion dollars are strengthening North America’s industrial battery ecosystem and improving supply security for electric material handling equipment. In addition, the expansion of cold-chain logistics, food retail automation, and smart warehousing facilities is increasing demand for advanced forklift batteries capable of operating in temperature-sensitive environments. Fleet operators are increasingly integrating telematics-enabled lithium battery systems that provide real-time monitoring of charging cycles, operating temperatures, and asset utilization, supporting predictive maintenance and higher warehouse productivity.

Japan Forklift Battery Market Outlook

Japan remains one of the most technologically advanced forklift battery markets globally, supported by the country’s leadership in electric forklifts, factory automation, and lithium-ion battery innovation. Japanese manufacturers such as Toyota Industries Corporation continue to expand development of high-efficiency lithium-ion powered forklifts and circular battery reuse systems for industrial applications. Toyota Material Handling has highlighted that lithium-ion powered forklifts are witnessing sustained growth because of their fast charging capability, reduced maintenance requirements, and superior energy efficiency compared with conventional lead-acid batteries. Japan’s advanced manufacturing ecosystem, combined with widespread automation across automotive, electronics, semiconductor, and precision engineering industries, is increasing demand for reliable electric material handling equipment. The country’s emphasis on carbon neutrality and energy optimization is also encouraging replacement of diesel and LPG forklifts with battery-powered alternatives in factories and logistics centers. Japanese warehouse operators are increasingly adopting compact lithium-ion forklifts for space-constrained industrial environments, particularly in urban manufacturing clusters around Tokyo, Osaka, and Nagoya.

Japan is also emerging as a leader in sustainable forklift battery lifecycle management and second-life battery utilization. In 2023, Toyota Material Handling Japan introduced the MEGALORE stationary power storage system that reuses lithium-ion batteries from electric lift trucks for stationary energy storage applications. This reflects Japan’s broader strategy to strengthen battery circularity, reduce industrial waste, and improve long-term energy sustainability. Japanese forklift battery manufacturers are heavily investing in thermal management systems, smart battery monitoring technologies, and rapid charging infrastructure to support 24/7 warehouse operations. Additionally, Japan’s aging workforce is accelerating adoption of autonomous forklifts and automated material handling systems, increasing demand for high-performance batteries capable of supporting uninterrupted robotic operations. The integration of AI-driven warehouse systems, robotics, and industrial IoT platforms is further enhancing demand for intelligent forklift battery solutions with predictive diagnostics and remote fleet management capabilities. Strong collaboration between industrial equipment manufacturers, battery developers, and electronics firms continues to reinforce Japan’s position as a premium technology hub within the global forklift battery ecosystem.

China Forklift Battery Market Trends

China represents one of the largest and fastest-evolving forklift battery markets globally due to its dominant manufacturing sector, extensive warehouse infrastructure, and leadership in lithium-ion battery production. The country’s rapid industrial automation and export-oriented logistics ecosystem continue to accelerate adoption of electric forklifts powered by lithium-ion and lithium iron phosphate (LFP) batteries. According to statistics associated with the China Construction Machinery Industry Association, forklift sales in China exceeded 739,000 units during the first half of 2025, reflecting strong growth in both domestic and export demand. Electric forklifts are increasingly replacing internal combustion models across ports, factories, e-commerce warehouses, and manufacturing facilities due to lower operating costs and stricter environmental policies. China also dominates global lithium refining and battery manufacturing capacity, enabling local forklift battery manufacturers to achieve cost advantages and rapid product commercialization. Several Chinese suppliers are expanding production of high-capacity forklift lithium battery systems with rapid charging capability and operational lifespans exceeding 4,000 charge cycles.

China’s forklift battery market is additionally benefiting from aggressive investments in next-generation battery chemistries, including sodium-ion technology and advanced LFP systems. Major Chinese battery manufacturers such as CATL and BYD are investing heavily in sodium-ion and industrial battery innovation to reduce dependence on critical minerals and improve charging performance in industrial applications. China’s broader push toward smart manufacturing, AI-enabled warehouses, and autonomous logistics systems is also increasing demand for intelligent forklift batteries equipped with thermal management systems, CAN communication, and real-time monitoring software. Large-scale industrial automation programs and growth in automated guided vehicles (AGVs) are creating sustained demand for maintenance-free industrial battery systems capable of supporting continuous multi-shift warehouse operations. Furthermore, China’s dominance in global battery processing and industrial equipment manufacturing enables forklift OEMs to rapidly scale production of electric material handling solutions for both domestic use and export markets, reinforcing the country’s strategic importance within the global forklift battery value chain.

Competitive Landscape

- The global forklift battery market is highly competitive and characterized by the presence of industrial battery manufacturers, lithium-ion technology providers, and material handling equipment suppliers focused on electrification and intelligent energy management systems.

- Key players include EnerSys, BYD, Flux Power Holdings, Exide Technologies, Amara Raja Energy & Mobility, CATL, LG Energy Solution, Samsung SDI, Panasonic Holdings, and BSL Battery Industrial.

- Companies are competing through investments in lithium iron phosphate battery technology, fast-charging systems, AI-enabled battery management platforms, cloud-based fleet analytics, and localized manufacturing expansion. Strategic collaborations between forklift OEMs, battery manufacturers, logistics companies, and energy infrastructure providers are becoming increasingly important as industrial electrification accelerates globally.

MAJOR PAIN POINTS

- High upfront replacement cost of lithium-ion and advanced forklift battery systems continues to limit adoption among small and medium-sized warehouse operators.

- Long charging durations and operational downtime associated with conventional lead-acid batteries reduce fleet productivity in high-throughput logistics environments.

- Limited charging infrastructure availability across aging warehouses and distribution centers slows the transition toward electric forklift fleets.

- Rising volatility in raw material prices, particularly lithium, nickel, cobalt, and lead, creates pricing pressure for battery manufacturers and fleet owners.

- Battery performance degradation under extreme temperature conditions impacts operational efficiency in cold storage and outdoor industrial applications.

- Frequent battery maintenance requirements, including watering, equalization, and cleaning for lead-acid batteries, increase labor and operational costs.

- Concerns regarding battery lifespan, cycle stability, and replacement frequency create uncertainty around long-term return on investment.

- Inadequate battery recycling infrastructure and tightening environmental regulations increase compliance complexity for industrial fleet operators.

- Compatibility challenges between advanced battery systems and existing forklift models hinder seamless fleet electrification initiatives.

- Supply chain disruptions and dependency on Asia-based battery cell manufacturing create procurement delays and inventory management risks for OEMs and distributors.

RECENT DEVELOPMENTS

- May 2026: EnerSys highlighted expanding lithium-battery commercialization initiatives and industrial energy-storage investments during fiscal 2026 earnings discussions.

- April 2026: Crown Equipment Corporation promoted V-Force lithium-ion battery upgrades for warehouse forklifts, targeting improved productivity and charging efficiency.

- March 2026: EnerSys showcased advanced smart-battery monitoring technologies and industrial battery solutions during Transport 2026 industry exhibitions.

- February 2026: EnerSys confirmed ongoing lithium-battery product development efforts, strengthening motive-power and industrial energy-storage market positioning.

- January 2026: EnerSys announced fiscal 2026 financial updates emphasizing industrial battery demand growth across material-handling and warehouse electrification sectors.

- June 2025: Contemporary Amperex Technology Co. Limited advanced Indonesia lithium-battery manufacturing investments, supporting global industrial and electric-vehicle battery supply expansion.

- July 2025: EnerSys initiated broader fiscal 2026 strategic restructuring plans supporting industrial battery operations and long-term profitability improvements.

KEY PROCUREMENT PRIORITIES AND BUYER EVALUATION CRITERIA

- Organizations investing in the Global Forklift Battery Market are increasingly selecting suppliers based on their ability to deliver high-performance, energy-efficient, and operationally reliable battery systems that support intensive warehouse automation and long-duration material handling operations. Buyers are prioritizing vendors offering faster charging capabilities, extended battery lifecycle, lower maintenance requirements, and compatibility with electric forklift fleets operating in logistics, manufacturing, retail, ports, and e-commerce distribution centers.

- Procurement strategies are being influenced by the accelerating transition from lead-acid batteries to lithium-ion technologies, rising adoption of automated guided vehicles (AGVs), and growing demand for smart battery management systems integrated with fleet monitoring and warehouse management platforms. Companies are also emphasizing energy optimization, opportunity charging capabilities, reduced downtime, and sustainability compliance while evaluating forklift battery providers.

- Logistics operators, industrial manufacturers, warehouse operators, and third-party logistics providers assess charging efficiency, cycle life performance, thermal stability, safety certifications, total cost of ownership, and after-sales service support before selecting forklift battery suppliers and long-term technology partners.

ANALYST VIEW / OPINION

- Rapid electrification of warehouse fleets and material handling equipment is accelerating demand for lithium-ion forklift batteries due to their longer lifecycle, fast charging capabilities, and lower maintenance requirements compared to lead-acid alternatives.

- E-commerce expansion and rising investments in automated warehouses are significantly increasing forklift deployment across logistics, retail distribution, and third-party fulfillment centers worldwide.

- Lithium-ion technology is expected to capture a progressively larger market share as companies prioritize operational efficiency, opportunity charging, and reduced downtime in high-throughput warehouse environments.

- Asia-Pacific remains the dominant production and consumption hub driven by large-scale manufacturing activity, expanding industrial infrastructure, and growing adoption of electric forklifts in China, Japan, South Korea, and India.

- Sustainability regulations and corporate carbon reduction initiatives are encouraging industries to replace internal combustion forklifts with electric alternatives, directly strengthening forklift battery demand globally.

- Increasing adoption of automated guided vehicles (AGVs) and autonomous forklifts in smart factories and Industry 4.0 facilities is creating strong opportunities for advanced high-performance battery systems.

- Battery manufacturers are focusing on energy density improvements, fast-charging technologies, thermal management systems, and battery management software to improve productivity and fleet reliability.

- Lead-acid batteries continue to maintain a substantial installed base in cost-sensitive industries due to lower upfront costs, despite growing competitive pressure from lithium-ion technologies.

- Rising investments in cold storage warehouses and food supply chain logistics are supporting demand for specialized forklift batteries capable of operating efficiently in low-temperature environments.

- Strategic partnerships between forklift OEMs, battery manufacturers, and warehouse automation providers are intensifying as companies aim to deliver integrated electric material handling solutions with optimized energy performance.

TARGET AUDIENCE

| INDUSTRY | WHO SHOULD BUY THIS REPORT? | REASON TO BUY THIS REPORT |

| Automotive & Electric Vehicle Manufacturers | EV Fleet Managers, Battery Procurement Teams, Warehouse Automation Engineers | Analyze forklift battery demand for electric material handling fleets, lithium-ion transition strategies, and warehouse electrification initiatives |

| Logistics & Warehousing Companies | Distribution Center Managers, Fleet Operations Teams, Energy Management Departments | Evaluate battery performance requirements for high-throughput warehouse operations, multi-shift applications, and charging infrastructure optimization |

| E-Commerce & Retail Distribution Companies | Fulfillment Center Heads, Automation Engineers, Procurement Managers | Assess forklift battery adoption trends supporting automated warehouses, fast-order fulfillment, and energy-efficient intralogistics operations |

| Manufacturing & Industrial Facilities | Plant Operations Managers, Material Handling Supervisors, Maintenance Teams | Understand battery requirements for continuous forklift operations in manufacturing plants, assembly lines, and industrial logistics environments |

| Forklift OEMs & Material Handling Equipment Manufacturers | Product Development Teams, Electrification Engineers, Strategic Sourcing Departments | Identify growth opportunities for battery-integrated forklifts, electric fleet expansion, and advanced battery management system integration |

| Battery Manufacturers & Energy Storage Providers | R&D Teams, Battery Technology Engineers, Market Intelligence Departments | Benchmark lithium-ion, lead-acid, and emerging forklift battery technologies, lifecycle performance, and industrial adoption trends |

| Cold Storage & Food Processing Companies | Refrigerated Warehouse Managers, Facility Engineers, Fleet Maintenance Teams | Evaluate forklift battery solutions optimized for low-temperature environments, operational reliability, and extended runtime performance |

| Ports, Airports & Freight Terminal Operators | Cargo Handling Teams, Equipment Operations Managers, Infrastructure Planning Departments | Analyze demand for heavy-duty forklift batteries supporting cargo movement, container handling, and large-scale logistics operations |

| Mining, Construction & Heavy Equipment Companies | Industrial Fleet Managers, Heavy Equipment Operations Teams, Procurement Departments | Assess durable forklift battery solutions for rugged industrial environments, high-load applications, and remote operational sites |

| Investors, Private Equity & Consulting Firms | Investment Analysts, Industrial Technology Consultants, Strategic Research Teams | Evaluate market growth opportunities, competitive positioning, battery technology advancements, and long-term electrification trends in the forklift battery industry |

WHY CHOOSE DATAM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

WHAT DATAM UNIQUELY PROVIDES

- Real-time industrial battery procurement intelligence mapped across logistics, warehousing, manufacturing, and material-handling fleet operators globally.

- Country-level lithium-ion localization assessment linked with industrial electrification incentives, battery recycling mandates, and warehouse modernization investments.

- Detailed benchmarking of forklift battery chemistries including LFP, TPPL, lead-acid, and fast-charging industrial lithium platforms.

- AI-driven supply-chain disruption tracking covering lithium, graphite, recycled lead, separator materials, and industrial battery freight bottlenecks.

- Integrated pricing intelligence combining raw-material volatility, lifecycle economics, maintenance savings, and regional manufacturing cost structures.

- Competitive analysis incorporating warehouse automation partnerships, charging infrastructure ecosystems, and predictive battery analytics capabilities.

- Exclusive trade intelligence mapping forklift battery import-export dependencies, regional manufacturing shifts, and geopolitical sourcing exposure.