Dermal Fillers Market Size & Growth

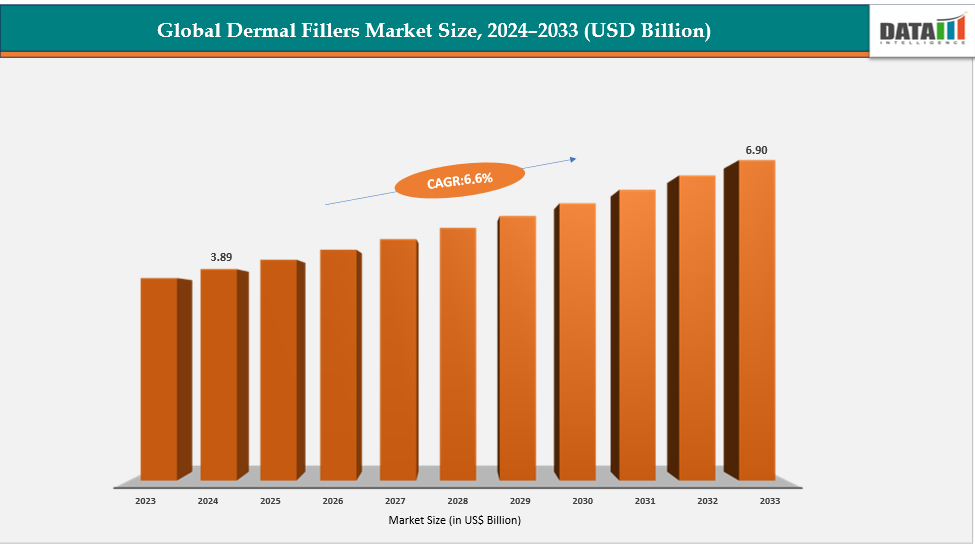

The global dermal fillers market size reached US$ 4.36 billion in 2025 is expected to reach US$ 6.90 billion by 2033, growing at a CAGR of 6.6% during the forecast period 2026-2033.

Another significant driver shaping the growth of the dermal fillers market is the rapidly increasing aging population and the global emphasis on age-related aesthetic enhancement. As individuals age, the skin naturally undergoes structural changes, including the breakdown of collagen, reduction in fat layers, and loss of skin elasticity. These changes result in wrinkles, fine lines, and facial volume loss, particularly in areas such as the cheeks, nasolabial folds, and around the lips. Dermal fillers offer a convenient, minimally invasive solution to counter these visible signs of aging by providing immediate volume restoration and contour improvements without the need for surgical procedures.

Additionally, growth in aesthetic clinics, dermatology centers, and medical spas has made these treatments more accessible. Continuous improvements in filler formulations especially hyaluronic acid-based fillers that offer higher biocompatibility, reversible results, and longer-lasting effects have also strengthened patient confidence. Collectively, these factors make the aging population and their aesthetic expectations a major driver propelling sustained growth in the dermal fillers market.

Dermal Fillers Market Dynamics

Drivers: Growing demand for minimally invasive cosmetic procedures driving the dermal fillers market growth

The growing demand for minimally invasive cosmetic procedures plays a major role in driving the dermal fillers market. Consumers today increasingly prefer aesthetic treatments that offer noticeable improvements without the risks, pain, or recovery time associated with surgical interventions. Dermal fillers fit this need perfectly, as they provide quick, outpatient procedures with immediate results and minimal downtime, allowing individuals to resume daily activities almost instantly. Rising social acceptance of cosmetic enhancements, coupled with the influence of social media and beauty standards, has made these procedures more mainstream across various age groups.

Additionally, continuous advancements in filler formulations and injection techniques have improved safety, comfort, and the natural appearance of outcomes, further boosting patient confidence. This widespread shift toward less invasive and more convenient cosmetic solutions continues to accelerate the adoption of dermal fillers globally.

Restraints: High cost of treatment and limited insurance coverage are hampering the growth of the dermal fillers market

A key restraint in the dermal fillers market is the high cost of treatment combined with limited insurance coverage. Dermal filler procedures can be expensive, particularly when multiple syringes are required to achieve desired results or when patients need periodic maintenance every 6–18 months. Since these treatments are primarily classified as elective aesthetic procedures, they are generally not covered by health insurance plans, meaning patients must bear the full cost out-of-pocket.

This financial burden can limit accessibility, especially in price-sensitive markets or among younger consumers with lower disposable incomes. As a result, while demand for aesthetic enhancements is growing, cost-related concerns continue to restrict wider adoption and may prevent repeat or long-term use among certain patient groups.

For more details on this report – Request for Sample

Dermal Fillers Market Competitive Landscape

Top companies in the dermal fillers market include Abbvie Inc, Galderma, Merz Pharma, Sinclair Pharma plc, Teoxane Laboratories, Dr. Korman Laboratories Ltd, Advanced Aesthetic Technologies, Revance Aesthetics, Tiger Aesthetics Medical, LLC. and among others.

Abbvie Inc:- AbbVie Inc. plays a prominent role in the dermal fillers market as a leading innovator in aesthetic medicine. The company leverages its strong R&D capabilities to develop advanced hyaluronic acid-based fillers and neuromodulators that cater to a growing demand for minimally invasive cosmetic procedures. AbbVie’s established global distribution network, extensive clinical expertise, and focus on product safety and efficacy help strengthen its market presence. By continuously expanding its aesthetic portfolio and introducing new formulations, AbbVie contributes significantly to market growth, particularly in regions with high adoption of cosmetic treatments.

Recent Industry Developments

- March 2026 – Hyaluronic acid (HA) fillers remain the dominant product category globally

Hyaluronic acid-based fillers continue to lead due to high safety, reversibility, and natural aesthetic outcomes, accounting for the largest share of injectable aesthetic procedures worldwide. - March 2026 – AI-assisted aesthetic planning and personalized injection mapping gains traction

Clinics are increasingly adopting AI-based facial mapping tools to simulate filler outcomes and personalize treatment planning, improving precision in volume restoration and contouring procedures. - February 2026 – AbbVie expands premium filler portfolio for facial contouring

AbbVie (via Allergan Aesthetics) continues strengthening its Juvederm portfolio for jawline, cheek, and lip augmentation, focusing on longer-lasting and more natural-looking results in premium aesthetic markets. - February 2026 – Galderma strengthens Restylane and biostimulatory filler innovations

Galderma continues to expand its Restylane range and biostimulatory fillers such as Sculptra, supporting demand for collagen stimulation and long-term facial rejuvenation treatments. - January 2026 – Revance Therapeutics advances RHA filler line for dynamic facial areas

Revance is expanding its RHA (Resilient Hyaluronic Acid) filler platform designed for dynamic facial areas, supporting natural facial movement while reducing fine lines and wrinkles.

Market Scope

| Metrics | Details | |

| CAGR | 6.6% | |

| Market Size Available for Years | 2022-2033 | |

| Estimation Forecast Period | 2026-2033 | |

| Revenue Units | Value (US$ Bn) | |

| Segments Covered | Product Type | Hyaluronic Acid (HA), Calcium Hydroxylapatite (CaHA), Poly-L-Lactic Acid (PLLA), Polymethylmethacrylate (PMMA), Others |

| Material | Biodegradable, Non-Biodegradable | |

| Application | Facial Line Correction, Lip Enhancement, Wrinkle Reduction Facial Contouring, Scar Treatment, Others | |

| Gender | Female, Male | |

| End User | Dermatology Clinics, Hospitals, Others | |

| Regions Covered | North America, Europe, Asia-Pacific, South America and the Middle East & Africa | |

The global Dermal Fillers market report delivers a detailed analysis with 62 key tables, more than 57 visually impactful figures, and 159 pages of expert insights, providing a complete view of the market landscape.