Deception Technology Market Overview

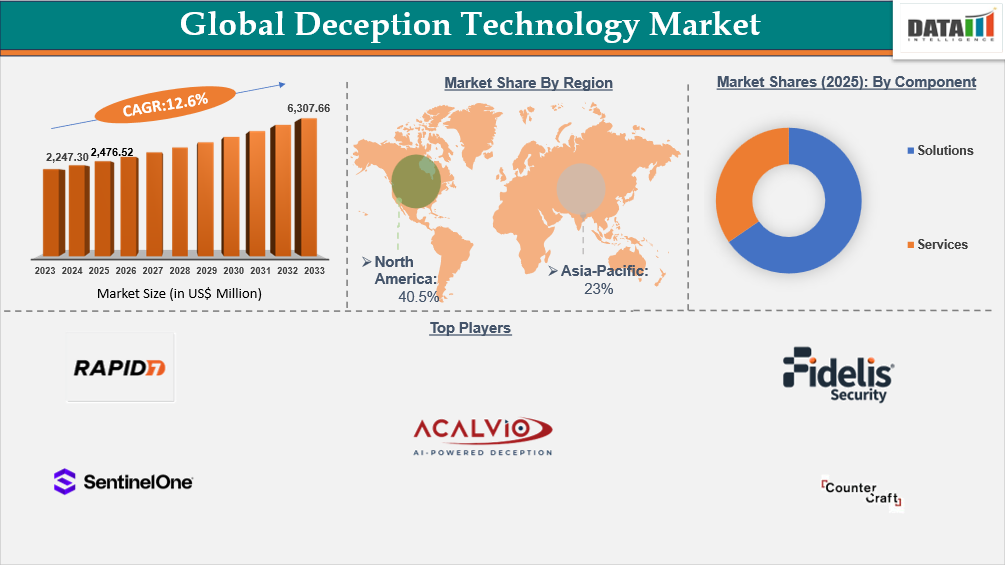

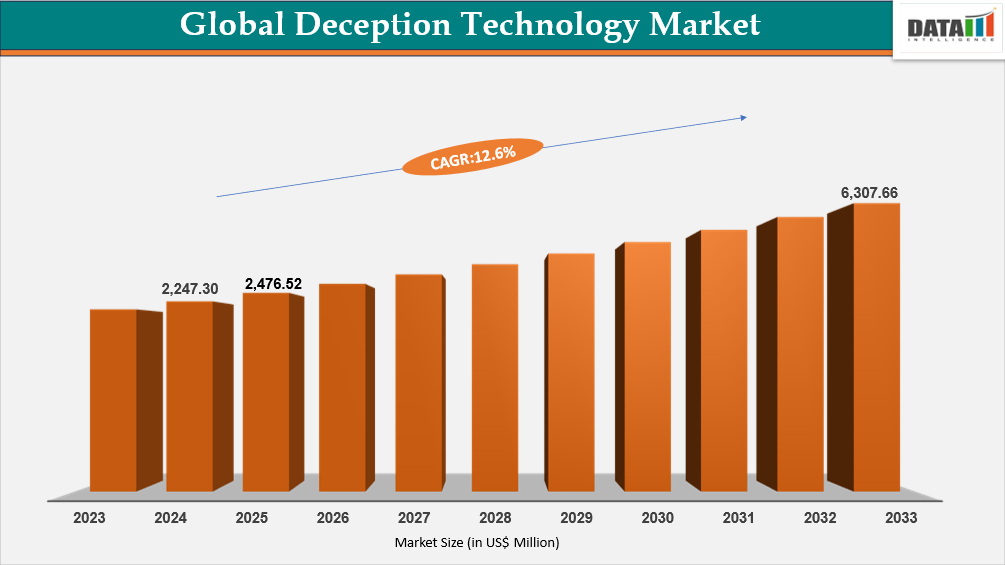

Global Deception Technology Market reached US$ 2,476.52 million in 2025 and is expected to reach US$ 6,307.66 million by 2033, growing with a CAGR of 12.6% during the forecast period 2026-2033.

The global deception technology market is witnessing significant growth as organizations increasingly seek proactive measures to combat sophisticated cyber threats. Cyberattacks are becoming more frequent and complex, with industries such as finance, healthcare, manufacturing, and critical infrastructure reporting hundreds of daily intrusion attempts. In 2024 alone, cybercrime caused an estimated US$ 6 trillion in damages globally, reflecting both direct financial losses and indirect costs such as downtime, reputational damage, and regulatory fines. These trends underscore the urgent need for advanced cybersecurity solutions like deception technology.

Deception technology works by deploying decoys, traps, and honeypots that mimic real IT assets, networks, and applications. This allows security teams to detect, analyze, and respond to attacks in a controlled environment before they cause significant harm. Organizations implementing these solutions can identify zero-day attacks, insider threats, and advanced persistent threats (APTs) more effectively than relying solely on traditional firewalls and antivirus systems. For example, companies that adopted deception-based monitoring reported detection of unauthorized lateral movement within their networks within hours, compared to several days with conventional security tools.

The market is also being fueled by regulatory pressures and increasing awareness of cybersecurity risks. Governments and organizations worldwide are implementing stricter data protection and cybersecurity regulations, making early threat detection and mitigation essential. With global ransomware attacks increasing by nearly 40% year-over-year and phishing incidents affecting millions of users, deception technology provides a critical layer of defense that complements existing cybersecurity infrastructure.

Regulatory compliance requirements increasingly mandate proactive threat detection capabilities. The European Union's Digital Operational Resilience Act (DORA), enforced from January 2025, requires financial entities to implement advanced ICT risk management frameworks including threat-led penetration testing and threat intelligence capabilities. Similarly, the U.S. Securities and Exchange Commission's cybersecurity disclosure rules, effective December 2023, mandate material incident reporting within four business days, incentivizing technologies that accelerate threat detection timelines.

Looking forward, the convergence of deception technology with artificial intelligence and machine learning creates unprecedented detection capabilities, positioning this market segment for sustained expansion as organizations prioritize resilient, intelligence-driven security architectures.

Deception Technology Industry Trends and Strategic Insights

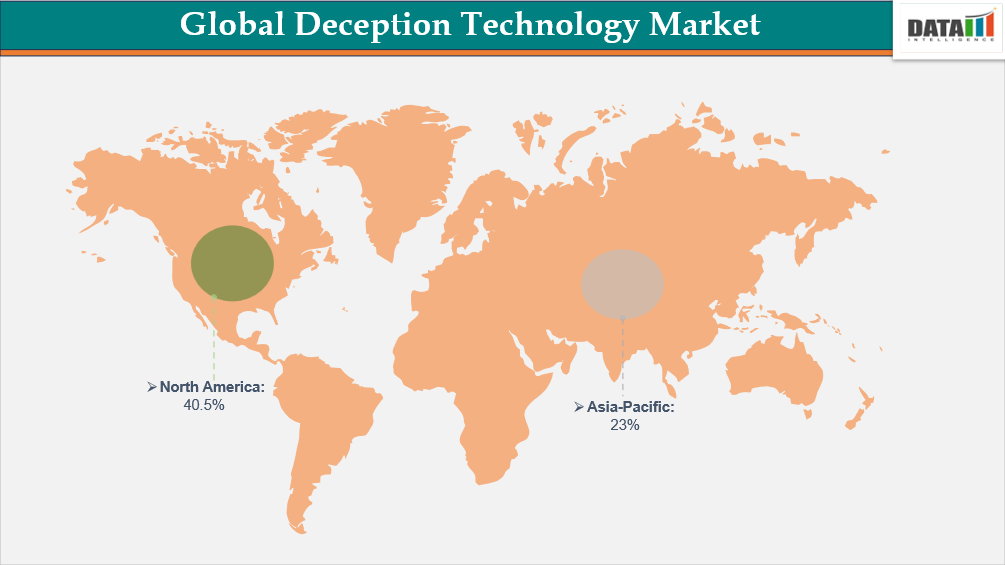

- Asia-Pacific is the fastest-growing region in the deception technology market, capturing the share of 23% in 2025.

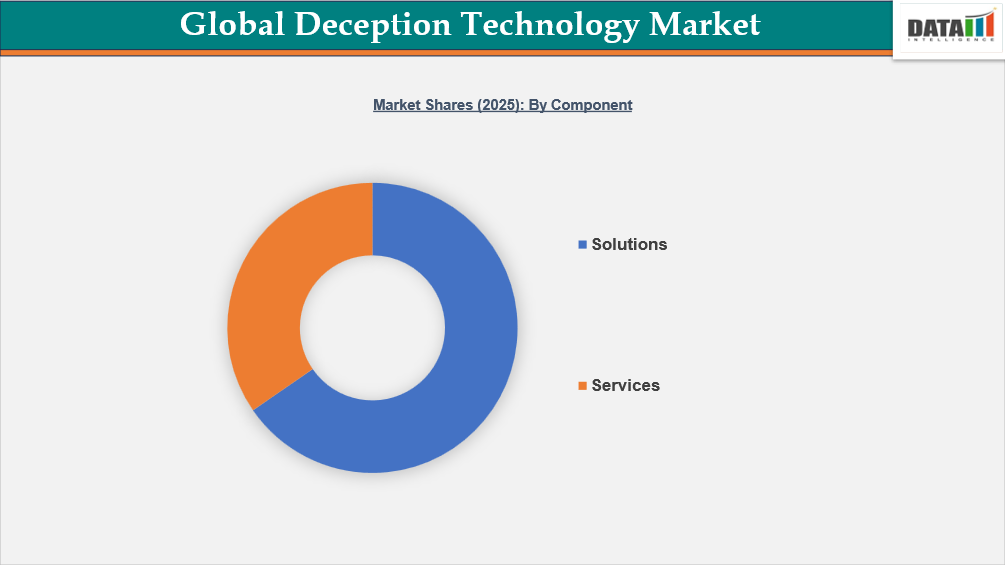

- By component, the solutions segment is projected to be the largest market, holding a significant share of about 67.1% in 2025.

Global Deception Technology Market Size and Future Outlook

- 2025 Market Size: US$ 2,476.52 million

- 2033 Projected Market Size: US$ 6,307.66 million

- CAGR (2026-2033): 12.6%

- Largest Market: North America

- Fastest Market: Asia-Pacific

Market Scope

| Metrics | Details |

| By Component | Solutions, Services |

| By Deployment Mode | On-Premises, Cloud-Based |

| By Organization Size | Large Enterprises, Small and Medium Enterprises (SMEs) |

| By Deception Stack | Network Security, Endpoint Security, Application Security, Data Security, Others |

| By End-User | Banking, Financial Services, and Insurance (BFSI), Government, Healthcare, IT and Telecommunications, Others |

| By Region | North America, South America, Europe, Asia-Pacific, Middle East, and Africa |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth |

Market Dynamics

Increasing Cyberattacks Push Companies to Adopt Deception Technology for Early Threat Detection

The rising frequency and sophistication of cyberattacks are driving organizations worldwide to adopt deception technology as a proactive cybersecurity measure. In 2024, global cyberattacks increased by over 30%, with critical infrastructure, financial institutions, and healthcare organizations experiencing hundreds of attacks weekly. For example, the National Stock Exchange of India reportedly faced more than 400 million attempted cyberattacks in a single day during a major coordinated attack, highlighting the scale of emerging threats.

Cybercriminals are increasingly using advanced techniques such as AI-driven malware, ransomware, and zero-day exploits, which often bypass traditional security tools. Deception technology helps counter these threats by deploying decoys, honeypots, and traps that mimic real IT assets, luring attackers into controlled environments. This allows organizations to monitor attacker behavior, detect breaches early, and respond before significant damage occurs.

The financial and operational impact of cyber incidents is also fueling demand for proactive defense solutions. In 2024, the global average cost of a data breach reached nearly US$ 5 million, while companies reported downtime from cyberattacks averaging 22 days per incident. Such figures underline the urgent need for early detection and mitigation technologies like deception systems.

Organizations are increasingly integrating deception technology with broader cybersecurity strategies, including AI-driven threat analysis, endpoint detection, and network monitoring. Industries such as finance, healthcare, and manufacturing are leading adopters, using deception tools to protect sensitive data and maintain regulatory compliance. As cyber threats grow in complexity, the adoption of deception technology is expected to continue rising, driven by its ability to provide early detection, improve threat intelligence, and reduce the operational and financial impact of attacks.

The global deception technology market is no longer about "building a better mousetrap." It is about creating a proactive, intelligence-led ecosystem that transforms the network into a minefield for attackers. By reducing the "dwell time" of threats and providing deep forensic insights into attacker methodology, deception technology has become the cornerstone of modern cyber resilience.

Surging frequency and sophistication of cyber-attacks globally

The rising frequency and sophistication of cyberattacks are accelerating global adoption of deception technology as a proactive cybersecurity strategy. In 2024, cyberattacks surged by over 30%, with critical sectors such as finance and healthcare facing hundreds of incidents weekly, including over 400 million attempted attacks in a single day on the National Stock Exchange of India. Advanced threats leveraging AI-driven malware, ransomware, and zero-day exploits increasingly bypass traditional defenses. Deception technology counters these risks by deploying decoys, honeypots, and trap credentials that mimic real IT assets, enabling early breach detection and attacker behavior analysis.

The growing financial impact of cybercrime further strengthens demand, with the average global data breach cost reaching nearly US$ 5 million in 2024 and downtime averaging 22 days per incident. Organizations are integrating deception platforms with AI-based threat analytics, endpoint detection, and network monitoring to reduce attacker dwell time. Industries including finance, healthcare, and manufacturing are leading adopters to safeguard sensitive data and ensure regulatory compliance. As threats evolve, deception technology is emerging as a core pillar of intelligence-led cyber resilience and modern security architecture.

High initial investment and perceived complexity of deployment

Despite strong detection benefits, the deception technology market faces adoption barriers due to high initial investment and deployment complexity. Implementing deception platforms often requires substantial upfront spending on software licenses, infrastructure integration, and professional services, with first-year costs accounting for 15–25% of total cybersecurity budgets for many mid-sized enterprises. This financial burden creates hesitation, particularly among cost-sensitive organizations.

Operational complexity further restrains growth, as effective deployment requires detailed network mapping, strategic decoy placement, and continuous tuning to replicate real production environments. Organizations with legacy systems may need extended implementation timelines, delaying time-to-value. Security teams also express concerns about integrating deception tools alongside existing SIEM, EDR, and SOC workflows, while the shortage of skilled cybersecurity professionals increases configuration and alert management challenges. Consequently, cost sensitivity and perceived technical complexity continue to limit broader adoption, especially among small and mid-sized enterprises.

Segmentation Analysis

The global deception technology market is segmented based on component, deployment mode, organization size, deception stack, end-user, and region.

Escalating Enterprise Need for Proactive, Low–False-Positive Threat Detection Accelerates Deception Solutions Adoption

The solutions segment is dominating with 67.1% share and driving core market demand as enterprises prioritize automated, high-confidence internal threat detection capable of identifying attackers during reconnaissance and lateral movement stages. By deploying realistic decoy servers, credentials, endpoints, and cloud assets, deception platforms function as an active internal defense layer rather than a reactive monitoring tool, significantly strengthening cyber resilience. A major adoption catalyst is the ability of deception solutions to reduce attacker dwell time by 50–80%, enabling earlier incident response before business-critical systems are compromised.

For instance, in 2024, Rapid7, a U.S.-based cybersecurity analytics and threat detection company, expanded its deception capabilities within the InsightIDR platform to enhance detection of lateral movement, credential misuse, and advanced persistent threats through AI-driven techniques. Additionally, the near-zero false-positive nature of deception alerts improves SOC efficiency and reduces operational costs by an estimated 30–40% compared to traditional SIEM or IDS systems. Strategic integrations further highlight solution-driven expansion. In 2024, Attivo Networks, a U.S.-based identity security and deception technology provider, partnered with Microsoft to integrate deception-based threat detection into Microsoft Azure environments, strengthening cloud and hybrid enterprise security visibility.

Rising Managed and AI-Driven Security Operations Propel Deception Technology Services Growth

The services segment is emerging as a major growth engine as enterprises increasingly rely on managed and professional services to operationalize deception platforms amid rising cyber complexity and talent shortages. Managed Deception Services now include 24/7 monitoring, decoy lifecycle management, alert triage, and SOC integration, helping organizations reduce response times by 30–50% while minimizing internal resource strain.

AI-driven adaptive deception is also strengthening service value propositions. Leading vendors such as CrowdStrike, Palo Alto Networks, and SentinelOne are embedding deception within broader MDR and XDR ecosystems, with CrowdStrike launching Falcon Deception in 2025 as part of its integrated detection platform. For instance, in 2025, Frenetik, a Spain-based cybersecurity startup, introduced patented “Deception In-Use” technology that continuously rotates active identities and resources across Microsoft Entra, AWS, Google Cloud, and on-premises environments, advancing continuous deception-as-a-service models.

Geographical Penetration

Rising Identity-Driven Cyber Threats Accelerating Deception Adoption in Asia-Pacific

Asia-Pacific is the fastest-growing region in the global deception technology market, accounting for approximately 23% of global cyber incidents in 2024 and demonstrating strong revenue expansion in 2025. Rapid digital infrastructure growth, sustained ransomware activity, and credential-based intrusions across government, healthcare, telecom, and utilities are driving structural demand for internal threat detection aligned with Zero Trust frameworks. Enterprises are embedding deception platforms to identify lateral movement and identity misuse after perimeter controls fail. For instance, in August 2025, Trend Micro introduced Scam Radar within its ScamCheck platform in Singapore, enabling real-time detection of phishing, impersonation, and AI-driven social engineering threats, reinforcing regional commercialization of deception-aligned technologies.

India Deception Technology Market Outlook

India represents a high-growth nucleus within Asia-Pacific due to the scale of its digital economy and escalating financial fraud exposure. With over 900 million internet users and 400+ million active UPI accounts, India recorded approximately 25 lakh cyber incidents in 2025, generating financial losses exceeding ₹9,812 crore, largely linked to identity-driven fraud.

Institutional response is accelerating the adoption of behavior-based detection frameworks, while innovation hubs are strengthening domestic cybersecurity capability. For instance, in October 2024, CloudSEK, an India-based cybersecurity and digital risk management firm, launched a free AI-powered deepfake detection platform to identify manipulated video and audio across BFSI, healthcare, government, and media sectors, strengthening deception-detection deployment across the region.

Australia Deception Technology Market Trends

Australia’s deception technology market reflects high incident density and increasing policy maturity, with over 94,000 cybercrime cases recorded in a single year. Sustained ransomware exposure and supply-chain vulnerabilities are prompting enterprises to integrate honeypots, honeytokens, and deceptive infrastructure into SOC workflows to reduce attacker dwell time. Government and industry discussions increasingly position active cyber defense as core security architecture. For instance, in 2026, Cyber Security Agency of Singapore launched the National Simulated Scams Exercise under Exercise SG Ready 2026 to simulate impersonation-style cyber threats and strengthen scam detection awareness, reflecting broader regional momentum toward proactive, deception-informed defense models.

Rising Financial Exposure and Zero Trust Mandates Driving Deception Technology Adoption in North America

North America is the dominant region with approximately 40.5% share in 2025 in the global deception technology market, driven by measurable financial losses from AI-enabled fraud, expanding Zero Trust mandates, and enterprise demand for internal threat detection.

For instance, in March 2024, TrapX Security, a U.S.-based deception technology specialist, enhanced its DeceptionGrid platform with machine-learning–driven detection and automated response capabilities to accelerate identification and mitigation of sophisticated cyberattacks. This development reflects the region’s shift toward active, automated deception systems that reduce attacker dwell time and strengthen cyber resilience across complex enterprise environments.

U.S. Deception Technology Market Insights

The U.S. remains a core growth hub for deception technology as enterprises embed deception into managed detection and response workflows to counter credential abuse and lateral movement. For instance, in 2025, CrowdStrike, a U.S.-based endpoint and cloud security provider, launched Falcon Deception as part of its broader detection ecosystem, integrating deception capabilities into MDR services to enable earlier attacker exposure within enterprise networks. This integration aligns with widespread Zero Trust adoption and reinforces deception technology as a high-confidence internal detection layer within US cybersecurity architectures.

Canada Deception Technology Industry Growth

Canada’s deception technology market is expanding amid rising operational technology (OT) exposure and increasing financial impact from cyber incidents. In September 2025, national cybersecurity reporting indicated that 73% of Canadian cyber incidents impacted OT systems, highlighting growing vulnerability across industrial and building infrastructure. Statistics Canada further reported that 16% of businesses experienced cyber incidents in 2023, rising to nearly 30% among large enterprises, with recovery spending reaching $1.2 billion. As identity theft, fraud, and ransomware incidents increase, Canadian enterprises are prioritizing high-confidence internal detection tools to address lateral movement risks within segmented networks, strengthening long-term demand for deception technology across regulated and infrastructure-intensive sectors.

Regulatory Analysis

The deception technology market is shaped by evolving cybersecurity, data protection, and operational resilience regulations worldwide. In the U.S., the SEC’s cybersecurity disclosure rules and sectoral mandates in BFSI and healthcare require rapid incident reporting and continuous monitoring, increasing demand for advanced early-detection solutions. Canada’s risk-based cybersecurity framework similarly emphasizes critical infrastructure protection and breach preparedness. Across Europe, GDPR, DORA, and the NIS2 Directive mandate strict breach notification timelines, ICT risk management, and continuous threat monitoring, significantly elevating the cost of delayed detection.

In the Asia-Pacific, countries such as Singapore, India, Japan, Australia, and China have strengthened cybersecurity and data protection laws, including India’s Digital Personal Data Protection Act and Japan’s APPI, reinforcing early breach identification requirements. In Latin America, Brazil’s LGPD and expanding financial-sector regulations promote proactive detection and internal visibility. The Middle East & Africa region, particularly the UAE and Saudi Arabia, has introduced mandatory reporting and critical infrastructure protection frameworks. These regulatory developments collectively increase compliance pressure, encouraging organizations to adopt high-confidence, low–false-positive technologies such as deception-based detection platforms.

Sustainability Analysis

The sustainability of the deception technology market is anchored in its integration into broader, long-term cybersecurity architectures rather than remaining a standalone niche solution. As cyber threats increasingly target identities, cloud workloads, and AI systems, deception capabilities are being embedded into core enterprise platforms, ensuring recurring relevance and sustained vendor investment. This platform-based integration enhances scalability, reduces false positives, and supports continuous monitoring—key factors for long-term market resilience.

For instance, SentinelOne integrated Attivo Networks’ identity-focused deception into its Singularity platform to strengthen Active Directory and credential misuse protection. Zscaler embedded deception into its Zero Trust Exchange, extending capabilities to protect GenAI and LLM environments. Fortinet offers FortiDeceptor for OT and ICS ecosystems, while Rapid7 integrates honeytokens within InsightIDR for early breach detection. These integrations demonstrate how deception is becoming a durable, embedded security capability, reinforcing sustained market growth and long-term adoption.

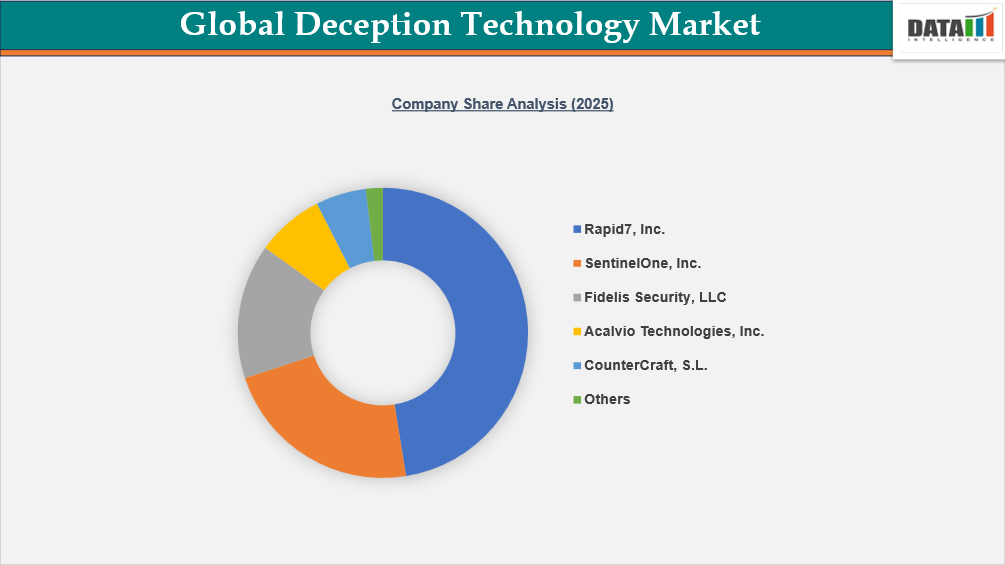

Competitive Landscape

- The global deception technology market is characterized by a competitive landscape that includes both established and regional players.

- Key players include Rapid7, Inc., SentinelOne, Inc., Fidelis Security, LLC, Acalvio Technologies, Inc., CounterCraft, S.L., CyberTrap Software GmbH, Proofpoint, Inc., Fortinet, Inc., Cynet Security Ltd., ECS Infotech Pvt. Ltd., RevBits, LLC

Key Developments

- In 2025, RevBits, a U.S.-based cybersecurity solutions provider, expanded into South America through a partnership with FMP Soluções. The move introduced its Cyber Intelligence Platform, integrating EDR, PAM, Zero Trust, and deception technology via a unified dashboard.

- In 2025, CounterCraft, a Spain-based deception technology company, formed a strategic partnership with Mission First Cyber to support U.S. federal and defense organizations. The alliance combines deception-powered intelligence with deployable cyber defense kits for real-time detection across tactical and air-gapped environments.

- In 2025, CounterCraft, a Spain-based deception technology company, partnered with CYBER RANGES to deliver deception-powered threat intelligence and advanced cyber defense capabilities to government agencies. The collaboration integrates real-time intelligence with attack emulation environments to enable proactive threat detection and mitigation.

Why Choose DataM?

- Data-Driven Insights: Dive into detailed analyses with granular insights such as pricing, market shares, and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. This approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. This personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. These insights complement and go beyond what is typically available in generic databases.

Target Audience 2026

- Manufacturers/ Buyers

- Industry Investors/Investment Bankers

- Research Professionals

- Emerging Companies