Global Cyclic Olefin Copolymer Market Size

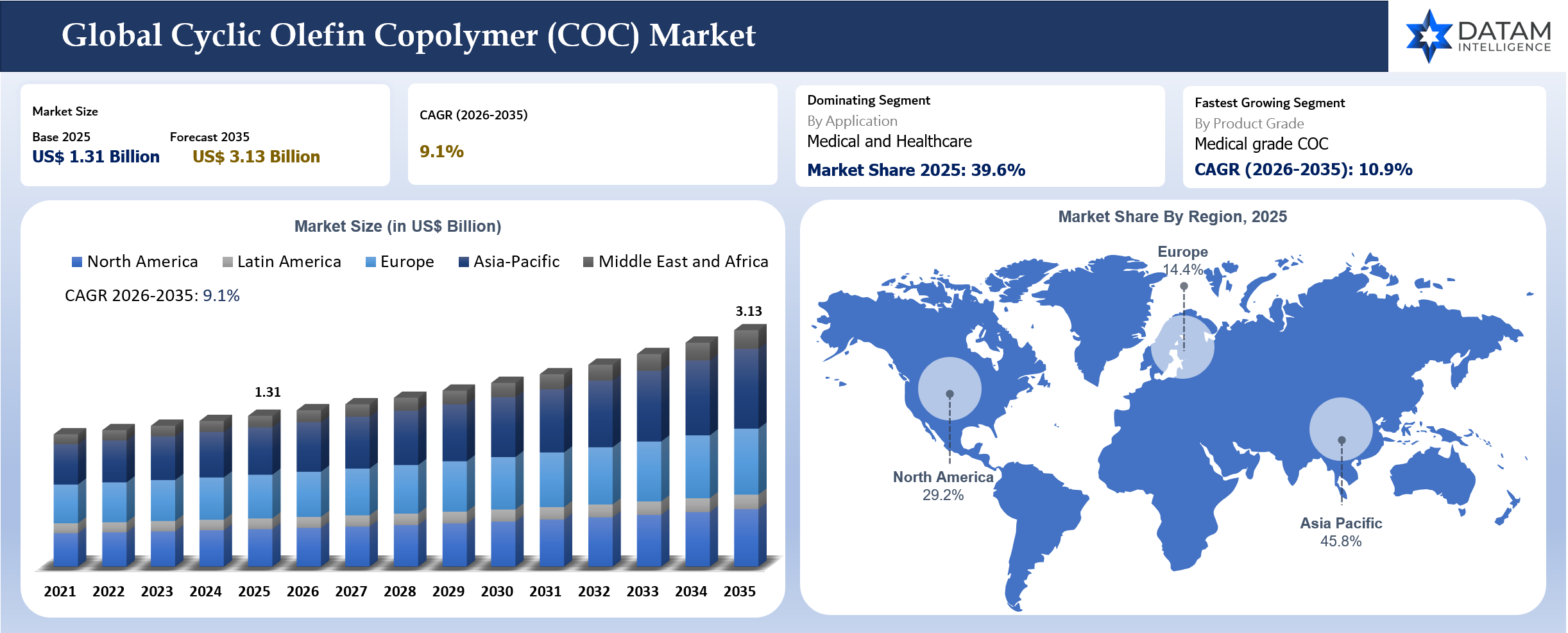

The global cyclic olefin copolymer market size is reached US$ 1.31 billion in 2025 and is expected to reach US$ 3.13 billion by 2035, growing at a CAGR of 9.1% during 2026 to 2035. COC is gaining stronger commercial relevance as pharmaceutical packaging, diagnostics, optical components, specialty films and microfluidic devices require cleaner and more dimensionally stable polymers. The material is valued where conventional plastics cannot provide the same balance of optical clarity, low extractables, moisture barrier, low birefringence and precision molding performance. Demand is strongest across prefilled syringes, diagnostic cartridges, microfluidic devices, blister packaging, optical lenses, camera modules, display films and labware where polymer purity directly influences performance.

Medical and diagnostic customers are creating the most attractive value opportunity. Drug delivery companies are evaluating COC for prefilled syringes, cartridges and vials because sensitive biologics need materials with lower ion leaching, lower breakage risk and better dimensional reliability than glass in selected applications. Diagnostics companies also value COC for microfluidic chips and optical detection because the material can reproduce fine molded features and maintain clarity during test workflows. The market is therefore moving from niche polymer use toward regulated healthcare and analytical platforms where supplier qualification can create long-term customer retention.

Packaging and optics will continue to support volume growth. COC films help improve stiffness, shrink behavior, deadfold, tear behavior and barrier performance in specialty packaging. Optical applications use COC where transparency, low moisture absorption and low birefringence are important. Growth will depend on the ability of suppliers to offer consistent grades, regulatory documentation, medical compliance support and reliable global supply for high-value converters and device manufacturers.

Key Takeaways

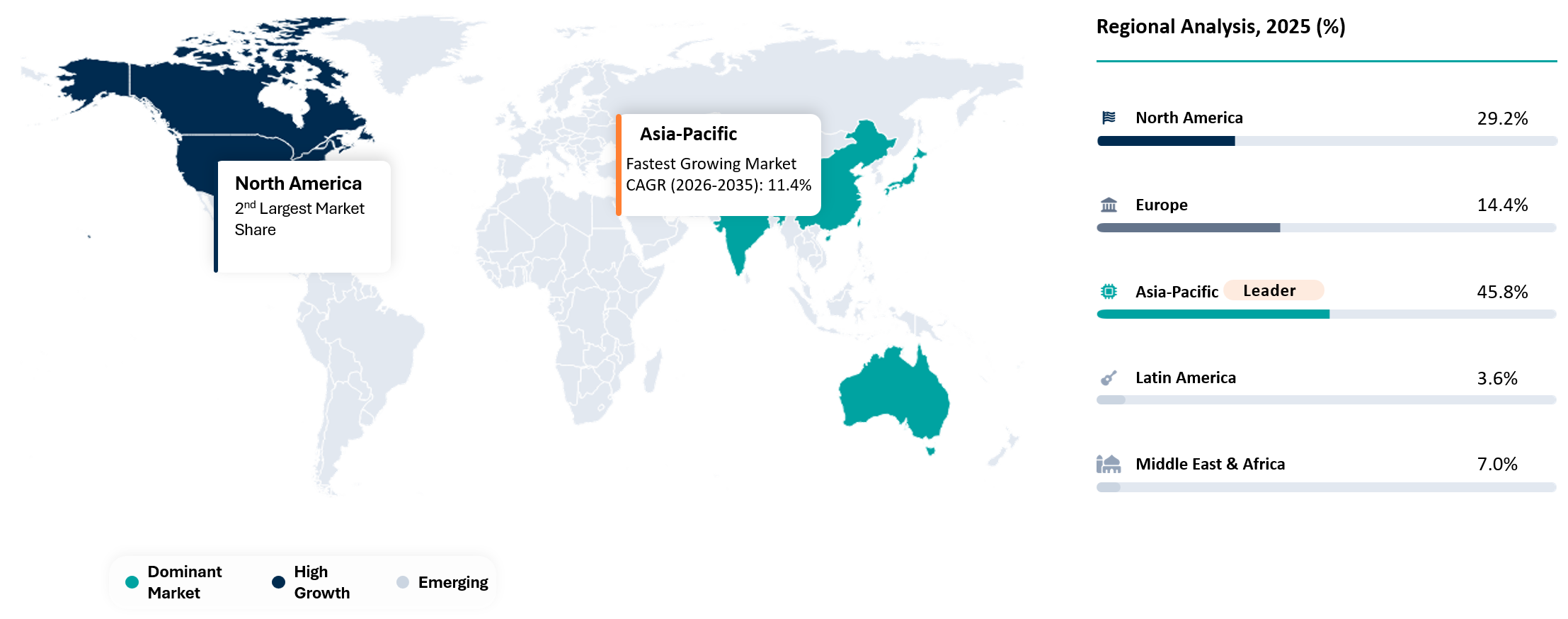

- Asia-Pacific dominated the global cyclic olefin copolymer market with 45.8% share in 2025, supported by medical device manufacturing, electronics, diagnostics, optics and specialty packaging production across Japan, China, South Korea and Southeast Asia.

- North America remained a high-value market in 2025 because pharmaceutical packaging, life science diagnostics, biologics delivery systems and laboratory consumables require validated polymer supply with strong documentation.

- Medical and healthcare applications dominated demand with 39.6% share in 2025, driven by prefilled syringes, cartridges, vials, diagnostic consumables, microfluidic chips and labware that require low extractables and high optical clarity.

- Medical grade COC is expected to be the fastest-growing product grade, growing with a CAGR of 10.9% between 2026 to 2035, supported by biologics, point-of-care testing, molecular diagnostics and microfluidic device growth.

- Injection molding dominated the processing route in 2025 because diagnostic cartridges, optical parts, microplates, vials and drug delivery components require dimensional precision and repeatability.

- Optical and electronics applications are gaining value as AR, VR, camera modules, display films and high-frequency electronics require materials with stable optical and dielectric behavior.

- Supplier differentiation is moving toward medical-grade documentation, extractables support, sterilization compatibility, optical consistency, long-term grade availability and customer qualification support.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 1.31 Billion | |

| 2035 Projected Market Size | US$ 3.13 Billion | |

| CAGR (2026-2035) | 9.1% | |

| Largest Market | Asia-Pacific, 45.8% Share in 2025 | |

| Fastest Growing Market | Asia-Pacific | |

| Dominating Sales Channel | Medical and Healthcare, 39.6% Share in 2025 | |

| By Product Grade | Medical Grade COC, Optical Grade COC, Packaging Grade COC, Electronics Grade COC, General Purpose COC | |

| By Processing Method | Injection Molding, Extrusion, Blow Molding, Thermoforming, Film Casting, Others | |

| By Application | Medical and Healthcare, Packaging, Optics, Electronics, Others | |

| By End-User | Pharmaceutical, Medical Device, Diagnostics, Packaging, Optical Component, Electronics, Research Laboratories, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Why This Report Matters in 2026

COC buyers enter 2026 with higher expectations around material validation, long-term supply and application-specific performance. Pharmaceutical and diagnostics companies cannot treat COC as a commodity resin because even small variation in extractables, molding behavior or optical properties can affect regulatory files, device performance and customer qualification. Procurement teams are evaluating suppliers on consistency, documentation and technical support rather than only resin price. The market is becoming more demanding because COC is increasingly used in applications where material failure or contamination risk can create a costly device redesign.

The strongest change is the growing use of COC in healthcare and life science platforms. Biologics, personalized medicine, molecular diagnostics and point-of-care testing need materials that support accurate fluid handling, clean optical detection and stable drug contact. COC is increasingly positioned against glass, PC, PMMA and COP depending on breakage risk, optical need, processing method and chemical exposure. Suppliers that help device makers compare these materials with practical application data will hold a stronger position in qualification programs.

A strong market view needs to connect product grade, processing route, application and regional demand because a film-grade packaging opportunity behaves very differently from a medical-grade microfluidic or drug delivery opportunity. Buyers are also evaluating regional supply security as medical and diagnostic customers reduce dependence on single-source inputs. The report supports clients in identifying where COC demand is moving and which suppliers are best positioned to serve regulated, high-value applications.

Strategic Indicators For Cyclic Olefin Copolymer

High Regulation Impact

COC demand is closely linked to medical device, pharmaceutical packaging and diagnostics regulation because the polymer is often used in products that contact drugs, biological samples or clinical workflows. Buyers require extractables and leachables data, biocompatibility support, sterilization compatibility and long-term grade availability. Regulatory pressure does not only influence the final device. It influences resin choice at the design stage because a material change after validation can delay product launches and increase testing cost. Suppliers that provide technical files, stability data and consistent grade availability can move from material vendor to qualification partner.

High Investment Activity

Investment is concentrated in medical packaging, diagnostic consumables, microfluidics, optical components and specialty film conversion. Pharmaceutical packaging companies are evaluating COC and COP platforms for syringes, vials, cartridges and containers used with biologics and sensitive injectables. Diagnostics companies are investing in molded cartridges and microfluidic platforms that require optical clarity and fine feature replication. Film converters are investing in specialty structures where COC improves stiffness, shrink, barrier or forming behavior. Investment will remain selective because COC is a premium material, but growth is strong where performance justifies the higher resin cost.

Supply Chain Disruption

Supply-chain pressure is concentrated around limited producer capacity, specialized monomers, medical-grade documentation and long customer qualification cycles. A COC grade cannot easily be replaced once it is locked into a diagnostic cartridge, optical part or drug delivery component. Customers therefore need visibility into supply continuity, second-site manufacturing and grade-change policies. Packaging and healthcare converters are increasingly asking suppliers to provide long-term supply assurances. Disruption risk is higher in medical applications because replacement material qualification can require testing, documentation updates and customer approvals that may take months.

Pricing Volatility

COC pricing is influenced by specialty monomer availability, production scale, medical-grade documentation, quality control, resin purity and application support. Commodity polymer comparisons are not useful because COC is often selected for performance that PE, PP, PET or PC cannot provide in the same application. Medical and diagnostic grades carry stronger pricing because they require documentation, consistency and low extractables. Packaging blends may be more price-sensitive because COC is often used as a modifier in multilayer films. Buyers should compare performance cost at the final device or package level rather than only resin price per kilogram.

Procurement Pressure

Procurement teams face pressure to reduce resin cost while engineering and regulatory teams need material stability. A cheaper substitute can become expensive if it changes microfluidic behavior, optical transmission, sterilization performance or drug contact compatibility. Healthcare buyers increasingly involve quality, regulatory, engineering and procurement teams in material selection. Suppliers that provide processing support, mold flow guidance, extractables data and documentation can reduce buyer risk. Procurement decisions are therefore moving toward total qualification cost and supply reliability rather than only purchase price.

New Technology Adoption

Technology adoption is strongest in precision injection molding, microfluidic device manufacturing, cleanroom molding, optical part replication and multilayer film conversion. COC supports molded features that are important in lab-on-chip and diagnostic devices, which creates value in point-of-care and molecular testing. Optical applications also require stable processing and low birefringence. Digital manufacturing controls, cavity pressure monitoring and automated inspection are becoming important where COC parts are used in regulated systems. Technology adoption supports higher yields and reduces variation in high-value molded parts.

Company Coverage Preview

TOPAS Advanced Polymers is a key company because TOPAS COC is strongly associated with healthcare, diagnostics, optics and packaging applications. The company’s positioning around clarity, purity, barrier performance and precision molding makes it highly relevant for applications such as prefilled syringes, vials, microfluidic devices, pharmaceutical blister packaging and specialty films. Its strength lies in application support and grade breadth rather than commodity resin volume.

Mitsui Chemicals is relevant through APEL cyclic olefin copolymer materials used in optical, packaging and electronic applications. The company’s broader chemical platform gives it credibility with converters and electronics customers that need transparency, heat resistance and low birefringence. Mitsui’s position is especially important in Japan and Asia-Pacific where optics, electronics and precision molding demand remains strong.

Zeon Corporation is an important adjacent competitor through ZEONEX and ZEONOR cyclic olefin polymer materials. COP and COC compete in many overlapping applications, especially in medical packaging, diagnostics and optics. Zeon’s optical and healthcare positioning gives customers another high-performance cyclic olefin option when they evaluate clarity, chemical resistance, sterilization and low extractables.

AI Impact Analysis

AI can support the COC market through faster material selection, molding optimization and defect analysis. Medical and diagnostic customers often need to compare resin grade, wall thickness, optical path, sterilization method and fluid behavior during early design. AI-enabled simulation and data-driven processing models can help reduce trial cycles by predicting shrinkage, birefringence, flow behavior and dimensional tolerance outcomes. Value is strongest where molded parts have microchannels, small optical windows or tight assembly interfaces.

AI can also improve manufacturing yield. COC parts used in diagnostics and drug delivery require high consistency and low defect rates. Advanced analytics can connect cavity pressure, temperature, cycle time, visual inspection and final part performance to identify drift before it causes batch rejection. For medical-grade applications, better production data can also strengthen traceability and quality documentation.

Material discovery and formulation work may also benefit from AI, but near-term impact will come from application engineering and processing support. Customers still need physical validation, extractables testing and regulatory review. AI will reduce development cycles and improve quality control, but it will not replace material qualification in regulated healthcare, optical and diagnostic uses.

Disruption Analysis

The market is being disrupted by the shift from glass and commodity polymers toward high-performance plastic systems in healthcare and diagnostics. Glass remains strong in many pharmaceutical applications, but COC can offer breakage resistance, lower weight and different interaction profiles in selected drug delivery platforms. Diagnostic devices also benefit from molded polymer designs that support small fluid volumes and automated testing. This shift is creating opportunities for resin suppliers, molders and device companies that can work together early in product development.

Packaging disruption is more selective but still relevant. COC can be used in films where converters need stiffness, shrink behavior, deadfold, tear control or moisture barrier improvement. Use is often performance-driven rather than cost-driven, which means adoption depends on whether COC solves a specific packaging limitation. Flexible packaging converters will continue using COC as a specialty modifier where it creates measurable value.

Optical and electronics disruption is linked to demand for lighter, clearer and more dimensionally stable components. AR, VR, camera modules and high-frequency electronics create niche but high-value opportunities. COC suppliers that maintain optical consistency and processing support will benefit from this shift. The market will remain specialized, but the value per application can be attractive.

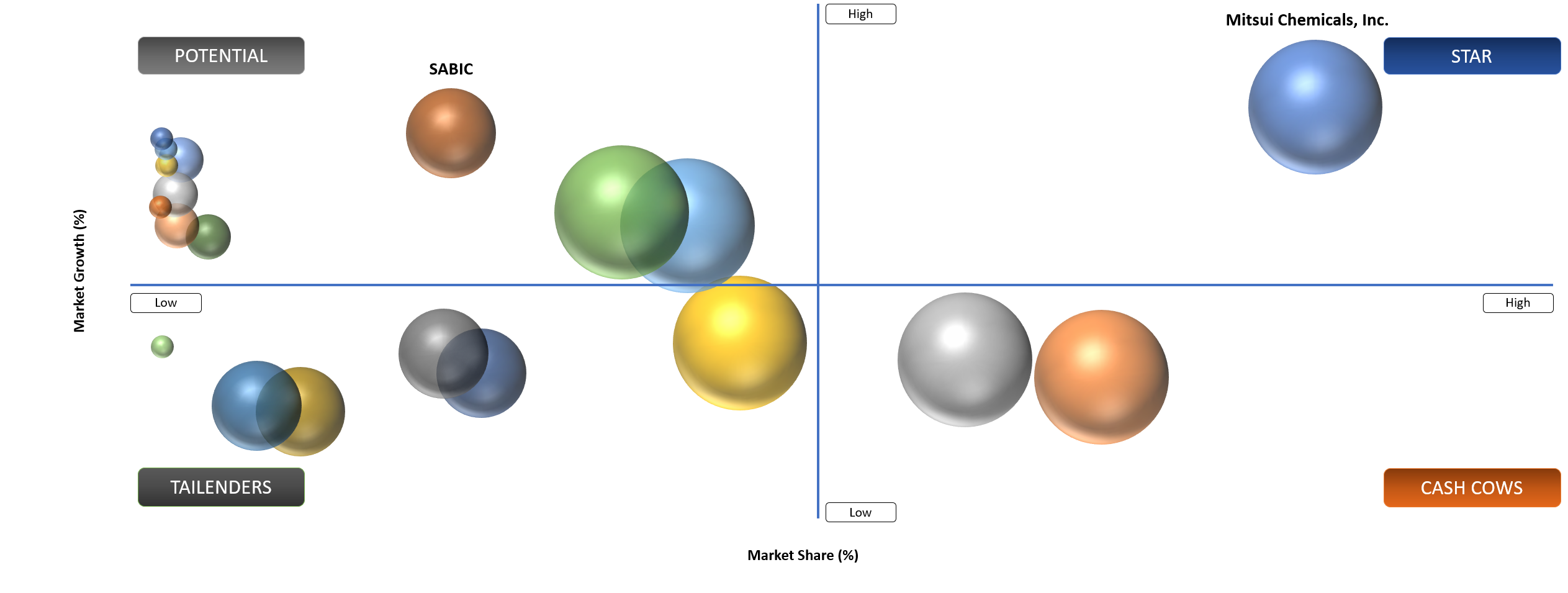

BCG Matrix: Company Evaluation

STAR

Star players include TOPAS Advanced Polymers, Mitsui Chemicals and Zeon Corporation because these companies are closely tied to core cyclic olefin material platforms and high-value applications. Their strength comes from recognized grades, application credibility, technical documentation and customer qualification in healthcare, diagnostics, packaging and optical components. These companies are positioned to capture growth where customers need purity, clarity, precision molding and stable supply.

POTENTIAL

Potential players include specialty compounders, medical molders, diagnostic consumable producers, optical component manufacturers and packaging converters that build proprietary expertise around COC processing. These companies may not control base resin supply, but they can create market value through part design, cleanroom molding, surface treatment, microfluidic device production and multilayer film structures. Growth potential is highest where converters become preferred partners for pharmaceutical, diagnostics and life science customers.

Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact | Demand Concentration | Impacted Use Case | Strategic Impact |

Biologics and injectable therapies increase demand for glass-alternative packaging | High | U.S., Europe and Japan | Prefilled syringes, cartridges and vials | Supports medical-grade resin qualification |

Point-of-care diagnostics expands microfluidic consumable demand | High | U.S., Japan, China and Europe | Diagnostic cartridges and lab-on-chip devices | Raises demand for optical clarity and molded precision |

Optical components require low birefringence materials | Medium To High | Japan, South Korea, China and Taiwan | Camera modules, lenses and display films | Creates premium demand for optical-grade materials |

Specialty packaging needs barrier and stiffness improvement | Medium | Global packaging converters | Blister packs, shrink films and barrier films | Supports COC as a high-performance modifier |

Medical Diagnostics Are Creating The Strongest Demand Pull

Medical diagnostics are one of the most important demand drivers because COC can support optical detection, microfluidic channels and clean sample contact surfaces. Diagnostic cartridges must handle fluids accurately while allowing reading through clear windows. COC’s ability to reproduce fine molded features makes it attractive for lab-on-chip designs and small-volume assays. This is especially valuable as testing shifts toward decentralized and automated formats.

Point-of-care systems also require materials that can be produced at scale. A diagnostic consumable must be consistent across millions of units because assay accuracy depends on uniform geometry and optical behavior. Resin suppliers and molders must therefore support tight processing control. COC demand grows when diagnostics companies move from research devices into commercial production.

Healthcare customers also value supply continuity. Once a material is qualified in a diagnostic platform, replacement is difficult and expensive. This creates a strong long-term relationship between resin suppliers, molders and device companies. Suppliers that help customers validate processing and documentation can secure durable demand.

Restraint Impact Analysis

| Restraint | Drag On Market Growth | Primary Impact Area | Impacted Use Case | Strategic Impact |

Premium resin cost limits adoption in commodity packaging | High | Price-sensitive packaging | Flexible films and consumer packs | Keeps COC focused on performance-critical structures |

Long qualification cycles slow material substitution | Medium To High | Medical and diagnostics | Drug delivery and clinical consumables | Protects incumbents but delays new adoption |

Limited producer base increases supply risk | Medium | Global resin supply | Medical grades and optical grades | Raises need for dual sourcing and supply agreements |

Processing sensitivity increases scrap risk | Medium | Precision molding | Microfluidics and optical parts | Rewards experienced converters |

Premium Cost And Qualification Slow Broader Adoption

COC carries a higher resin cost than many conventional polymers. Packaging converters will not use it unless it improves barrier, stiffness, shrink, forming or tear behavior enough to justify the cost. This limits broad adoption in commodity packaging and keeps the material focused on performance-sensitive formats. Customers therefore need application evidence before switching from cheaper polymers.

Medical and diagnostic applications face a different restraint. The value case can be strong, but qualification cycles are long. Extractables, sterilization, stability, molding and regulatory documentation must be reviewed before launch. Material changes after validation can create delays, so customers move carefully even when COC offers performance benefits.

Processing also requires expertise. Optical parts, microfluidics and thin-wall components can be sensitive to temperature, flow, mold design and cooling. Experienced converters can reduce scrap and improve yield. Suppliers that support processing trials can reduce this barrier.

Segment Analysis

Medical and healthcare applications will continue to lead value creation.

Medical and healthcare applications will remain the most attractive demand area because COC supports drug delivery, diagnostic testing and labware where material performance has direct product impact. The category accounted for 39.6% share in 2025 and is expected to remain the leading value pool through 2035. COC is especially relevant where optical clarity, low extractables, breakage resistance and precision molding matter more than resin price.

Prefilled syringes, vials and cartridges are important because biologics and sensitive injectables require packaging materials that reduce interaction risk. Glass remains established, but COC can be used where breakage, delamination or design flexibility create issues. Adoption depends on drug compatibility, sterilization method and regulatory pathway.

Diagnostic consumables are another major opportunity. Microfluidic cartridges, cuvettes, plates and lab-on-chip devices need consistent optical and dimensional performance. COC helps device makers build parts that support small fluid paths and optical reading. Growth will be strongest where diagnostic platforms scale into commercial production.

Diagnostic Consumables

Diagnostic consumables are gaining demand because laboratories, hospitals and decentralized testing sites need accurate and repeatable test cartridges. COC supports transparent molded structures, low background interference and dimensional precision. These properties help assay developers design compact systems with reliable optical detection. Growth is linked to molecular diagnostics, immunoassays and point-of-care testing.

A diagnostic consumable must work consistently across large production batches. Poor dimensional control can affect fluid flow and test accuracy. COC converters therefore need clean molding environments, controlled processing and inspection systems. Suppliers with application knowledge can influence material selection early in the device design phase.

Procurement decisions in diagnostic consumables are risk-led. A lower-cost material may not be acceptable if it changes assay performance. Customers value suppliers that can provide technical documentation, traceability and long-term grade support. These factors make diagnostics a sticky and attractive demand pocket.

Drug Delivery Components

Drug delivery components include prefilled syringes, cartridges, vials and device parts that contact or support sensitive therapies. COC offers breakage resistance and optical clarity while reducing some concerns linked to glass in selected applications. Demand is supported by biologics, self-injection devices and higher-value injectable therapies.

Material selection in drug delivery is conservative because patient safety and regulatory acceptance are central. Drug compatibility, sterilization resistance and extractables data must be reviewed carefully. COC suppliers need to support pharma packaging companies with robust documentation and stable quality.

Growth will be gradual but valuable. Once COC is qualified in a drug delivery platform, switching risk can be high. Suppliers that win early-stage design involvement can build durable revenue streams across product lifecycles.

Geographical Penetration

U.S. Cyclic Olefin Copolymer Market Trends

The U.S. market is shaped by pharmaceutical packaging, medical devices, diagnostics and life science consumables. Biologics, injectable therapies and point-of-care testing create demand for materials that combine optical clarity with low extractables and strong molding performance. Device companies often qualify materials through long development cycles, so supplier consistency becomes a competitive advantage. U.S. customers also value documentation and technical support because resin selection can influence regulatory files and commercial launch timelines.

Diagnostic cartridge production is an important opportunity because COC can support molded microchannels, optical detection windows and clean fluid handling. U.S. life science companies value materials that reduce assay interference and support repeatability across high-volume consumables. Contract molders with cleanroom capability can create additional demand because they help convert resin performance into qualified finished parts. Resin suppliers that work with molders and device owners can shorten application development cycles.

Pharmaceutical packaging demand is also moving toward alternatives to glass where breakage, delamination and weight are concerns. COC can compete in selected vial, syringe and cartridge uses where device design, sterilization method and drug compatibility are aligned. Growth will depend on validation with drug manufacturers and device platform owners. Long-term supply assurance will remain important because pharmaceutical customers do not want unexpected grade changes once commercial products are approved.

India Cyclic Olefin Copolymer Market Landscape

India is an emerging opportunity because domestic pharmaceutical manufacturing, diagnostics and medical device production are expanding. The country is not yet a large COC resin production base, but demand is likely to increase as Indian manufacturers move into higher-value diagnostic consumables, injectable packaging and medical components. Export-oriented device makers will be the early adopters because they must meet stricter performance and documentation expectations for regulated markets.

Local converters are increasingly evaluating advanced polymers for healthcare products. COC can gain share where Indian medical device and diagnostic manufacturers serve customers that require high optical clarity, low contamination risk and strong part consistency. Price sensitivity remains important, so adoption will be strongest in applications where performance requirements justify premium material cost. Suppliers will need to support customers with processing advice and material qualification support.

India’s pharmaceutical industry also supports long-term interest in COC for drug delivery and packaging. Wider adoption will require local technical service, moldability guidance and reliable distribution. Suppliers that can support Indian converters with documentation and application development will be better positioned. Growth may begin with imported resin and qualified converters before local supply ecosystems become deeper.

Japan Cyclic Olefin Copolymer Market Outlook

Japan is a core market because key cyclic olefin material suppliers and precision customers are based in the country. Japanese customers value optical quality, precision molding and long-term material stability. Optics, diagnostics, electronics and medical packaging all support domestic demand. Material qualification is often conservative, but approved suppliers can retain customers for long periods when quality remains stable.

Japanese device makers often prioritize reliability over rapid material switching. Once a resin is qualified for an optical or diagnostic application, customer retention can be strong. Suppliers need to provide stable grade availability, high consistency and strong technical support. Japan’s high-end molding and optical component ecosystem gives the market an important role in premium cyclic olefin demand.

Optical applications remain important. Cameras, lenses, display components and sensors need materials with low birefringence and dimensional stability. Japan’s precision manufacturing base makes it a premium market even when volume growth is moderate. Healthcare applications also remain attractive as diagnostics and drug delivery platforms demand clean, transparent and stable materials.

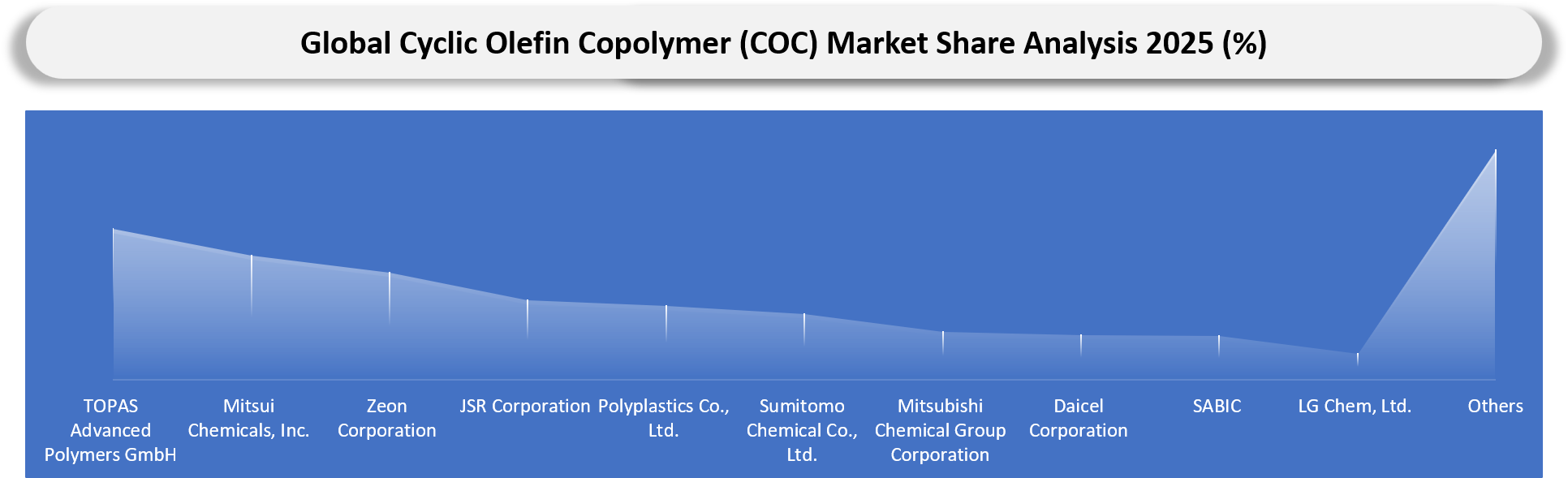

Competitive Landscape

- Competition is concentrated among a small group of specialty polymer suppliers rather than broad commodity resin producers because COC requires specific polymerization technology, application development and technical documentation.

- TOPAS Advanced Polymers competes strongly in COC through medical, packaging, diagnostic and optical applications, while Mitsui Chemicals participates through APEL and Zeon participates through adjacent COP materials such as ZEONEX and ZEONOR.

- Healthcare and diagnostics customers compare suppliers on extractables data, molding behavior, sterilization compatibility, transparency, regulatory support and long-term grade continuity rather than only resin cost.

- Packaging customers evaluate COC on blend performance, film stiffness, barrier enhancement, shrink behavior, seal behavior and compatibility with PE and other film structures.

- Competitive benchmarking should track medical-grade availability, regional technical support, optical-grade quality, application validation, customer qualification status and supply reliability.

Major Pain Points

- Premium resin cost limits use in commodity packaging where PE, PP, PET and PC meet basic performance needs.

- Medical and diagnostic qualification cycles are long because customers need documentation, sterilization data and application testing.

- Limited producer base creates sourcing risk for customers that need secure long-term supply.

- Processing sensitivity can increase scrap when converters lack experience with optical parts, microfluidic chips or thin-wall components.

- Resin substitution is difficult after device validation because changes can affect regulatory files and customer approvals.

- Packaging converters need clear value evidence before adding COC to multilayer film structures.

- High-purity applications require strict traceability and documentation that smaller suppliers may not be able to provide.

- Customers often struggle to compare COC with COP, PC, PMMA, glass and other alternatives without application-specific testing.

Recent Developments

- March 2026: TOPAS Advanced Polymers continued positioning TOPAS COC for medical, diagnostic, packaging and optical applications with emphasis on clarity, purity, moisture barrier and precision molding performance.

- February 2026: Zeon Corporation continued strengthening ZEONEX and ZEONOR cyclic olefin polymer offerings for optics, medical packaging and diagnostic applications, supporting demand for high-clarity polymer alternatives in precision applications.

- November 2025: Mitsui Chemicals continued promoting APEL cyclic olefin copolymer materials for optical, packaging and electronic applications where heat resistance, transparency and low birefringence are required.

- August 2025: Healthcare packaging converters increased COC evaluation in prefilled syringe and cartridge programs as biologics and high-value injectables required stronger breakage resistance and cleaner contact surfaces.

- May 2025: Diagnostic device manufacturers increased adoption of cyclic olefin materials in microfluidic cartridges and optical detection formats for point-of-care and laboratory testing applications.

Key Procurement Priorities And Buyer Evaluation Criteria

- Medical device buyers prioritize extractables data, sterilization compatibility, biocompatibility support, long-term grade continuity and regulatory documentation.

- Diagnostic manufacturers prioritize optical clarity, microfeature replication, dimensional stability, clean molding and reliable high-volume part consistency.

- Packaging converters prioritize film compatibility, barrier improvement, shrink behavior, forming performance, seal behavior and cost effectiveness.

- Optical component customers prioritize low birefringence, transparency, dimensional control, moisture resistance and tight processing windows.

- Preferred suppliers provide application testing, molding support, clean documentation, supply continuity and clear guidance on COC versus competing materials.

Analyst View And Opinion

- Medical and diagnostics applications will remain the most attractive value pool because material qualification creates longer customer relationships and higher switching barriers.

- COC will continue replacing glass and other polymers selectively rather than broadly, especially where breakage risk, optical clarity and extractables performance matter.

- Film and packaging demand will remain important but more price-sensitive than healthcare and optics because COC is often used as a performance modifier in multilayer structures.

- Japan will remain a technology anchor, while the U.S. and Europe will drive high-value medical and life science demand.

- India and China will create long-term growth opportunities as local medical device, diagnostics and pharma packaging ecosystems upgrade material requirements.

- Supplier consolidation is unlikely to move quickly because the market is technically specialized and the number of established global producers is limited.

Target Audience

| Industry | Who Should Buy This Report? | Reason To Buy This Report |

| Pharmaceutical Packaging | Packaging Engineers, Regulatory Teams, Procurement Leaders | Evaluate COC use in syringes, cartridges, vials and biologics packaging |

| Medical Devices | Product Development Teams, Material Engineers, Quality Teams | Compare COC with glass, PC, PMMA and COP for regulated devices |

| Diagnostics | Cartridge Designers, R and D Teams, Manufacturing Heads | Understand demand for optical and microfluidic consumables |

| Packaging Converters | Film Development Teams, Commercial Leaders | Assess opportunities in blister films, shrink films and specialty structures |

| Optical Components | Lens and Display Component Teams | Evaluate optical-grade COC demand and supplier positioning |

| Investors | Specialty Materials Investors, Corporate Strategy Teams | Assess high-value polymer opportunities and qualification barriers |

| Consulting Firms | Chemicals and Healthcare Materials Teams | Support market entry, supplier benchmarking and customer targeting |

What DataM Uniquely Provides:

- Client-ready market views that connect COC demand with product grade, processing route, application, end-user and regional supply.

- Bottom-up demand modelling using resin suppliers, converters, device makers, packaging formats, diagnostics platforms and pharmaceutical packaging trends.

- Supplier scorecards covering medical documentation, optical-grade consistency, processing support, supply continuity and regional technical service.

- Procurement intelligence covering resin price, qualification risk, grade substitution risk, lead time and supply security.

- Application-fit matrices comparing COC with COP, glass, PC, PMMA, PE, PP and PET across healthcare, optics and packaging.

- Risk-mitigation roadmaps covering single-source exposure, regulatory documentation gaps, processing scrap and material validation delays.