Cryogenic Insulation Market Size

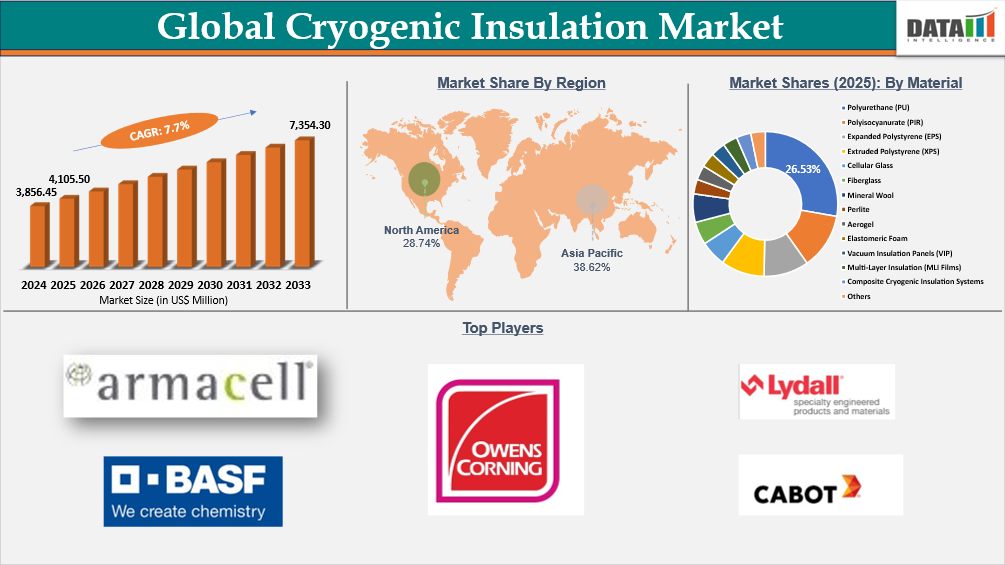

According to DMI analysis, the global cryogenic insulation market reached US$ 3,856.45 Million in 2024, rising to US$ 4,105.50 Million in 2025 and is expected to reach US$ 7,354.30 Million by 2033, growing at a strong CAGR of 7.7% during the forecast period from 2026 to 2033.

The main driving forces of the cryogenic insulation market are the increasing demand from the LNG industry. According to Shell’s LNG Outlook 2025 report, the demand for LNG worldwide is set to rise by around 60% in the next two decades up to the year 2040. The energy crunch in Asia and the demand for the decarbonization of industry and the adoption of cleaner fuels in shipping are prompting the development of the LNG transportation and storage infrastructure. The main application of cryogenic insulation is in the storage and transportation of LNG at extremely low temperatures. The need for sustainability is another driving force of the market.

The market growth is further fueled by an estimated increase of over 170 million tons in new LNG supplies, even though a growth rate of 407 million tons in international trades by 2024 has experienced subdued growth due to limitations in supplies. There is also an expansion in new hydrogen infrastructure, which is creating new avenues for advanced cryogenic equipment. There has also been an improvement in technology with respect to clean materials like aerogels and low-GWP foams. The Asia-Pacific market retains its fast growth rate due to expansion, clean energy strategies, and security.

Cryogenic Insulation Industry Trends and Strategic Insights

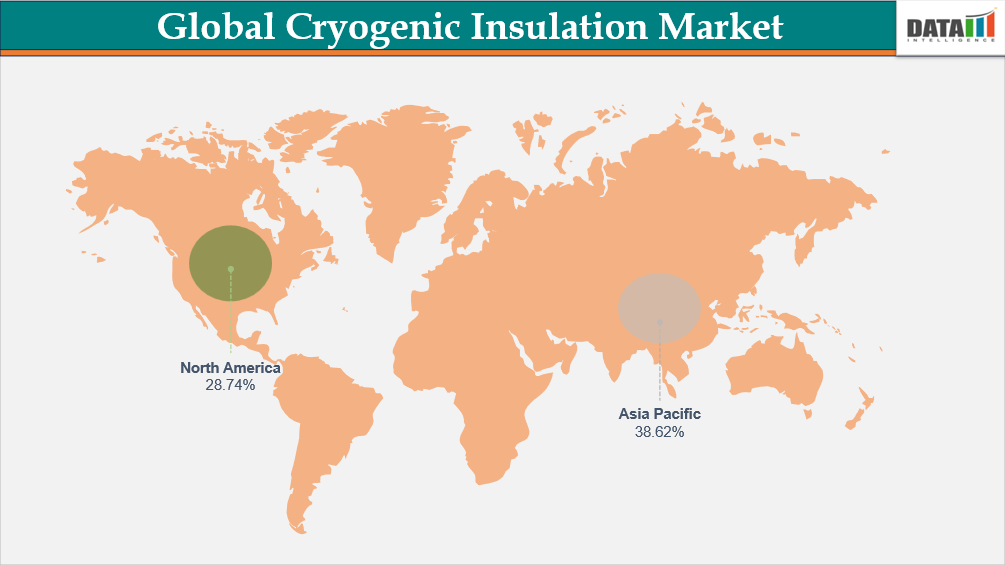

- Asia-Pacific leads the global cryogenic insulation market, capturing the largest revenue share of 38.62% in 2025, due to rapid industrialization, growing energy and gas infrastructure, and increased adoption of advanced insulation technologies in the region.

- By material, the Polyurethane (PU) segment led the global cryogenic insulation market, capturing the largest revenue share of 26.53% in 2025, due to its excellent thermal insulation properties, lightweight nature, and wide applicability across storage, transportation, and pipeline systems.

Global Cryogenic Insulation Market Size and Future Outlook

- 2025 Market Size: US$ 4,105.50 Million

- 2033 Projected Market Size: US$ 7,354.30 Million

- CAGR (2026–2033): 7.7%

- Dominating Market: Asia-Pacific

- Fastest Growing Market: North America

Market Scope

| Metrics | Details | |

| By Material | Polyurethane (PU), Polyisocyanurate (PIR), Expanded Polystyrene (EPS), Extruded Polystyrene (XPS), Cellular Glass, Fiberglass, Mineral Wool, Perlite, Aerogel, Elastomeric Foam, Vacuum Insulation Panels (VIP), Multi-Layer Insulation (MLI Films), Composite Cryogenic Insulation Systems, Others | |

| By Temperature Range | -50°C to -100°C, -100°C to -165°C, -165°C to -196°C, Below -196°C | |

| By Application | Storage Equipment, Transportation, Pipelines & Distribution, Process Systems | |

| By Form | Rigid Foam Panels / Boards, Spray Applied Foam, Pre-Fabricated Insulation Systems, Bulk-Fill / Perlite Systems, Vacuum Jacketed Systems, Flexible Blankets & Wraps, Multi-Layer Insulation Systems | |

| By End-User | Energy & Gas, Chemicals & Petrochemicals, Metallurgy & Industrial, Marine & Transport, Healthcare & Biotechnology, Aerospace & Defense, Food Processing | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Norway, Netherlands, Sweden, Denmark, Belgium, Switzerland, Austria, Poland, Finland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Egypt, Turkey, Qatar, Kuwait, Oman, Bahrain | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Market Share, Market Growth | |

Market Dynamics

Liquid Hydrogen Storage for Mobility and Industrial Decarbonization

Liquid hydrogen storage is becoming central to mobility applications such as fuel cell trucks, buses, shipping, and aerospace, where maintaining ultra-low temperatures (-253°C) is critical for performance and safety. The requirement is significantly increasing demand for high-efficiency cryogenic insulation materials such as vacuum insulated panels, multilayer insulation, and advanced foam systems. As hydrogen-powered transport scales globally, minimizing boil-off losses and improving storage efficiency are driving innovation in insulation technologies.

In the context of hydrogen-powered mobility services receiving significant momentum in the international market, the signing of an MoU in October 2025 by Tiger Logistics with Russia-based company H2 Invest for the deployment of advanced cryogenic storage solutions in India using the CryoSafe technology also refers to the hydrogen mobility sector fueling the growth of the cryogenic insulation sector.

Segment Analysis

The global cryogenic insulation market is segmented based on material, temperature range, application, form, end-user and region.

Polyurethane Holds the Highest Share in Global Cryogenic Insulation Market Due to Superior Thermal Efficiency, Cost-Effectiveness, and Strong LNG Infrastructure Demand

Polyurethane maintains the maximum market share of the total cryogenic insulation material due to its excellent thermal efficiency, low thermal conductivity, and high mechanical strengths at extremely low temperatures. The material shows high resistance to moisture, maximum durability, and hence has been used for LNG storage tanks, cryogenic pipelines, and industrial gas transportation systems. The lightweight constructions of these materials, along with their low costs, make them more favorable for large-scale industrial projects. Strong demand from oil & gas industry, along with LNG, maintains their large market share.

The leadership of the segment is further ensured by continuous innovation and expansion of production capacities by relevant players. For example, in November 2025, SIBUR unveiled a highly advanced grade of polyurethane foam (PUF), with a special focus on improving its thermic insulating properties for pipeline projects. The newly created insulating shells exhibit even more superior energy and thermal performance, allowing them to withstand extreme temperatures.

Geographical Penetration

DOMINATING MARKET:

Asia-Pacific Leads the Global Cryogenic Insulation Market Driven by LNG Expansion and Industrial Growth

Asia Pacific market accounts for the highest market size of global market, owing to high rates of industrialization and growing energy infrastructure. The growing LNG projects in countries such as China, India, Japan, and Korea have propelled market growth. The increased investments in LNG infrastructure, storage facilities, and cryogenic transportation pipes have fueled the market growth of the Asia Pacific market. In addition to these factors, the growing energy demands and infrastructure development have fueled market growth. The increasing chemical, electronic, and healthcare market growth has fueled market growth.

India Cryogenic Insulation Market Outlook

India's market for cryogenic insulation products is expected to show constant growth due to an increase in India's LNG imports, expansion of India's gas infrastructure, and rising demand for energy-efficient storage solutions. India's dependence on LNG imports has positively impacted its use of storage tanks, regasification facilities, and pipelines. Within India, gas production carried out locally decreased by 3.9% in September 2025. Furthermore, India's gas supplies rose by 1.2% due to an increase in LNG imported into India. In addition, a decrease of 1.1% in India's gas supplies was reported, with 5,207 MMSCMs available for sale. Moreover, a total of 5,642 MMSCMs of gas availability resulted from India's domestic supplies and those imported from elsewhere.

China Cryogenic Insulation Market Trends

The cryogenic insulation market in China is expected to register steady growth, with a rise in LNG infrastructure, an increase in ethane transportation, and an upsurge in demand for clean energy. Owing to strong shipbuilding and petrochemical industry activities, there is an increasing demand for high-end cryogenic insulation solutions, mainly for ships. In April 2022, there was a partnership between BASF and Shanghai Harvest Insulation Engineering, using the latter’s product, i.e., BASF’s Elastopor Cryo, on the delivery of the first-ever VL Ethane Carrier built by Jiangnan Shipyard. All these scenarios point towards advancements in technology, making China a strong player in terms of high-end cryogenic insulation.

Regulatory Analysis

The cryogenic insulation market is largely dependent upon the regulations and government legislations pertaining to aspects like energy efficiency, safety, and environmental protection. Some of the specific government regulations include the ISO (International Organization for Standardization), ASTM International, and building codes imposed on different regions, which largely define a set of regulations based on thermal performance, durability, and flame retardances. In a field like the use of liquefied natural gases, gases, and petrochemicals, safety codes like OSHA regulations for U.S. and ATEX regulations for Europe impose critical aspects of safety regulations to avoid any potential hazards due to extreme temperature conditions and the possibility of fires.

Environmental regulations are also affecting the market, especially those concerning carbon emission reduction, energy preservation, and sustainable material use. On one hand, the rising demand for LNG as a bridging fuel and the Hydrogen Economy initiatives in the U.S., EU, and Asia-Pacific regions will create more demand for environmentally friendly cryogenic storage and transport solutions.

Competitive Landscape

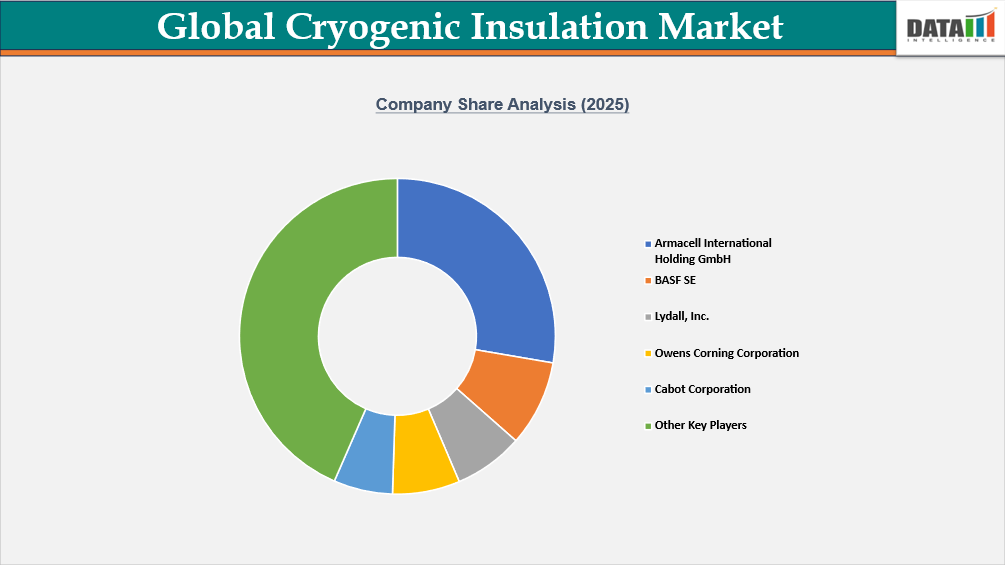

- The cryogenic insulation business is a competitive industry driven by demand from the LNG industry, industrial gases, petrochemicals, and the healthcare industry.

- Key global players include Aspen Aerogels, Cabot Corporation, BASF SE, Lydall, Armacell, Owens Corning, Johns Manville, and Rochling Group.

- Companies compete on the basis of product performance, thermal, durability, with products conforming to extremely stringent safety criteria. Innovation, especially in the materials technology area of aerogels and advanced foams.

Key Developments

- April 2026 – Aspen Aerogels and Cabot expanding advanced aerogel insulation technologies

Aspen Aerogels and Cabot Corporation enhanced high-performance cryogenic insulation materials for LNG storage, hydrogen transportation, and industrial gas applications. - March 2026 – BASF and Armacell strengthening low-temperature insulation solutions

BASF SE and Armacell advanced insulation systems designed to improve thermal efficiency, reduce energy loss, and enhance safety in cryogenic environments. - February 2026 – Owens Corning and Johns Manville increasing industrial insulation capacity

Owens Corning and Johns Manville expanded production of cryogenic insulation products to support growing LNG infrastructure and clean energy projects worldwide. - January 2026 – Rising demand from LNG, hydrogen, and energy storage sectors

Companies such as Lydall and Röchling Group increased focus on lightweight, durable insulation materials for next-generation energy transportation and storage systems. - In April 2025, Armacell announced the launch of its next-generation cryogenic and dual-temperature aerogel blanket, named as ArmaGel XGC. The blanket has shown its ability to provide high performance while being compliance-tested to ASTM C1728 Type I & IV, as well as being able to withstand extreme temperatures as low as -196°C.

What Sets This Global Cryogenic Insulation Market Intelligence Report Apart

- Latest Data & Forecasts – Comprehensive, up-to-date insights and projections through 2033. Coverage includes global value by Material, temperature range, application, form, end-user and region. Scenario forecasts with region-level splits (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa) and sensitivity to factors such as regulatory reclassification and raw-material costs.

- Regulatory Intelligence – Actionable analysis of regulatory frameworks that materially affect Cryogenic Insulation commercialization, revenue by country, allowable label claims, permitted doses, import/export controls and advertising restrictions.

- Competitive Benchmarking – Standardized profiling and benchmarking of leading pharma and nutraceutical players, contract manufacturers and e-commerce specialists active in the market.

- Geographic & Emerging Market Coverage – Region-by-region market sizing, growth drivers, reimbursement dynamics, cultural/consumer behavior and market access considerations. Focus on high-growth or regulatory-uncertain markets.

- Actionable Strategies – Identify opportunities for launching innovative products, while leveraging strategic partnerships and supply chain integration for maximum ROI.

- Pricing & Cost Analysis – In-depth assessment of price trends, raw material costs and sustainability-driven cost efficiencies across regional markets.

- Expert Analysis – Insights from industry experts such as product specialists, regulatory affairs professionals and key manufacturing companies.

Target Audience 2026

- LNG & Natural Gas Companies– LNG plant operators, regasification terminals, floating storage units (FSRUs), and midstream gas companies requiring high-performance insulation for storage tanks, pipelines, and transport systems.

- Hydrogen & Clean Energy Developers – Companies involved in liquid hydrogen production, storage, and transportation infrastructure, including green hydrogen project developers and energy transition investors.

- Industrial Gas Manufacturers - Producers and distributors of oxygen, nitrogen, argon, carbon dioxide, and specialty gases requiring cryogenic storage tanks, vacuum-insulated piping, and transport solutions.

- Energy Storage Project Developers (LAES & Cryogenic Energy Storage) – Firms deploying liquid air energy storage (LAES) and other cryogenic-based grid stabilization technologies.

- EPC Contractors & Engineering Firms – Engineering, procurement, and construction companies designing LNG terminals, hydrogen facilities, petrochemical plants, and cryogenic processing units.

- Cryogenic Equipment Manufacturers – OEMs producing cryogenic tanks, valves, piping systems, heat exchangers, and insulation systems integrating aerogels, PU/PIR, cellular glass, and multilayer insulation.

- Petrochemical & Chemical Processing Companies – Operators handling ultra-low-temperature processes requiring reliable thermal insulation for safety and efficiency.

- Healthcare & Biotechnology Companies – Hospitals, biobanks, pharmaceutical manufacturers, and research labs using liquid nitrogen storage systems.