Crisp Enhancers Market Overview

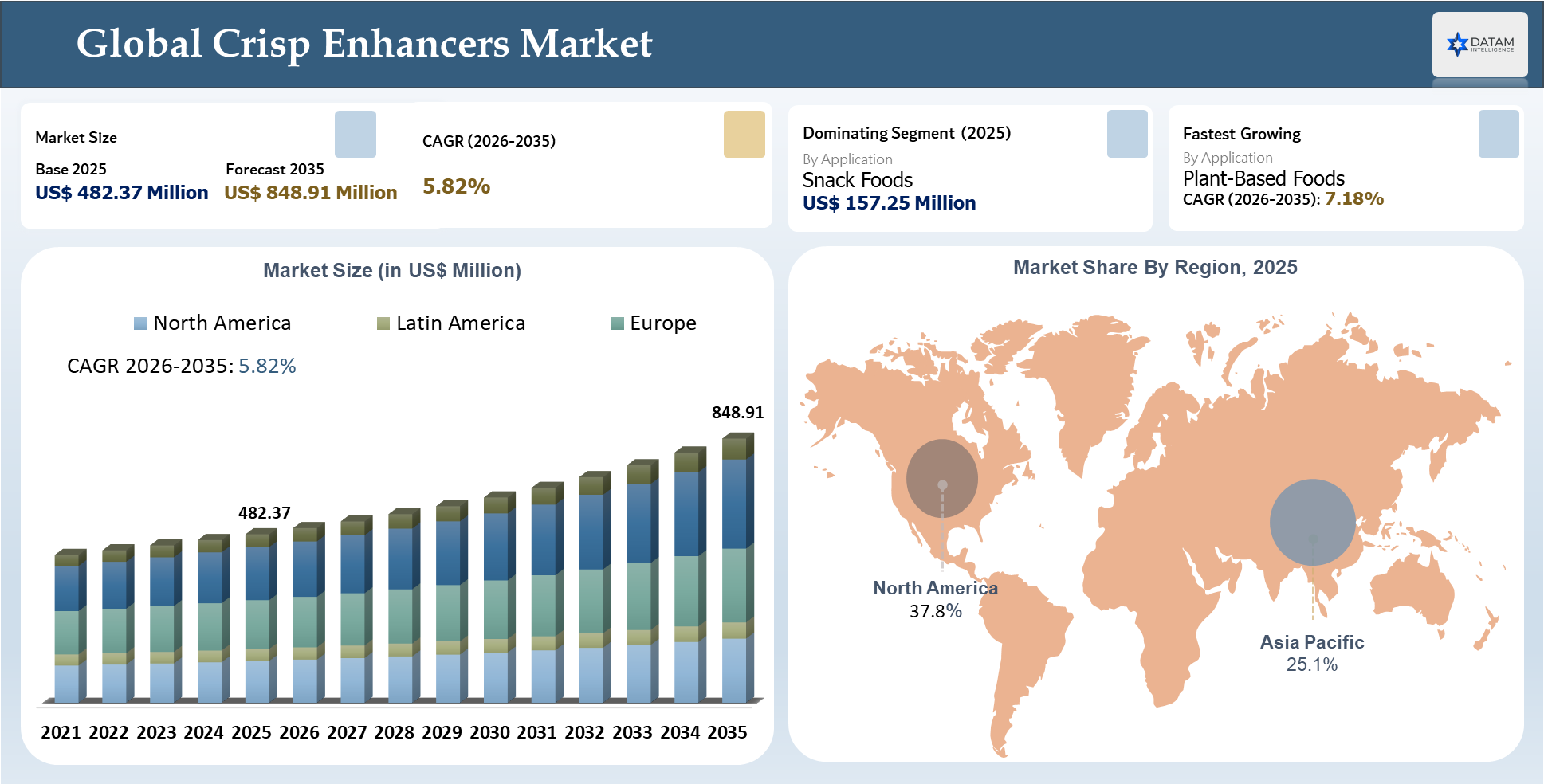

The Global Crisp Enhancers Market stood at US$ 482.37 million in 2025 and is expected to reach US$ 848.91 million by 2035, growing with a CAGR of 5.82% during the forecast period 2026-2035. There is an expanding demand for crisp retention, texture consistency, coating adherence, and moisture regulation in snacks, bakery goods, batter and breaded items, breakfast cereals, confectionary, ready meals, and vegan products. The growth in the market will be driven by premiumization of packaged snacks, rising consumption of frozen and ready-to-cook products, as well as increased utilization of starches, hydrocolloids, fibers, proteins, and emulsifiers as texturizing agents.

The market dynamics will be impacted by clean-label reformulations, gluten-free product formulations, reduced-oil snacks, and the requirement for consistent crispness after packaging, storage, heating, and transportation. Snacks will continue to drive commercial success, while vegan foods are anticipated to grow faster due to improvements in bite, coating, and mouthfeel properties. On the other hand, complex formulations, high costs of raw materials, and variable performance during processing operations could limit adoption. The competitive edge in the market will be gained through application-specific formulations, clean-label suitability, reliable supply chains, shelf-life verification, and technical know-how on reproducible crispness performance.

AI Impact Analysis

AI has become a game-changer for the Global Crisp Enhancers Market by accelerating the formulation process, predicting the performance of ingredients, and creating products according to their specific applications. Through AI-enabled formulation modeling, ingredient companies can determine how starches, hydrocolloids, fibers, proteins, and emulsifiers will behave under various conditions such as frying, baking, extrusion, freezing, and reheating. This will minimize experimentation during texture development and assist ingredient manufacturers to come up with customized crispness solutions suitable for snacks, baked goods, coated foods, cereals, and plant-based food items.

In addition, food processors can leverage AI for sensory analytics, shelf-life prediction, moisture migration assessment, and oil absorption. This will assist food manufacturers to gain better control over crunchy textures, coating adhesion, and textural stability. Furthermore, AI-driven demand prediction will enable ingredient suppliers to synchronize production with rapidly growing segments like clean label snacks, gluten-free baked products, frozen appetizers, and plant-based foodstuffs. Procurement processes will be aided by AI tools that will enable ingredient manufacturers to track the fluctuations in the prices of commodities in corn, potato, rice, tapioca, and hydrocolloid value chains.

Crisp Enhancers Industry Trends and Strategic Insights

- Application segment continues to be the key parameter for commercialization, since demand is significantly driven by the use of the product in snacks, bakery items, battered and breaded products, breakfast cereals, confectionery products, ready-to-eat meals, and alternative foods.

- Increasing demand is being witnessed in application-oriented crispers that can provide crunch maintenance, moisture management, adhesive quality, oil absorption prevention, reheating performance, and clean-label compliance.

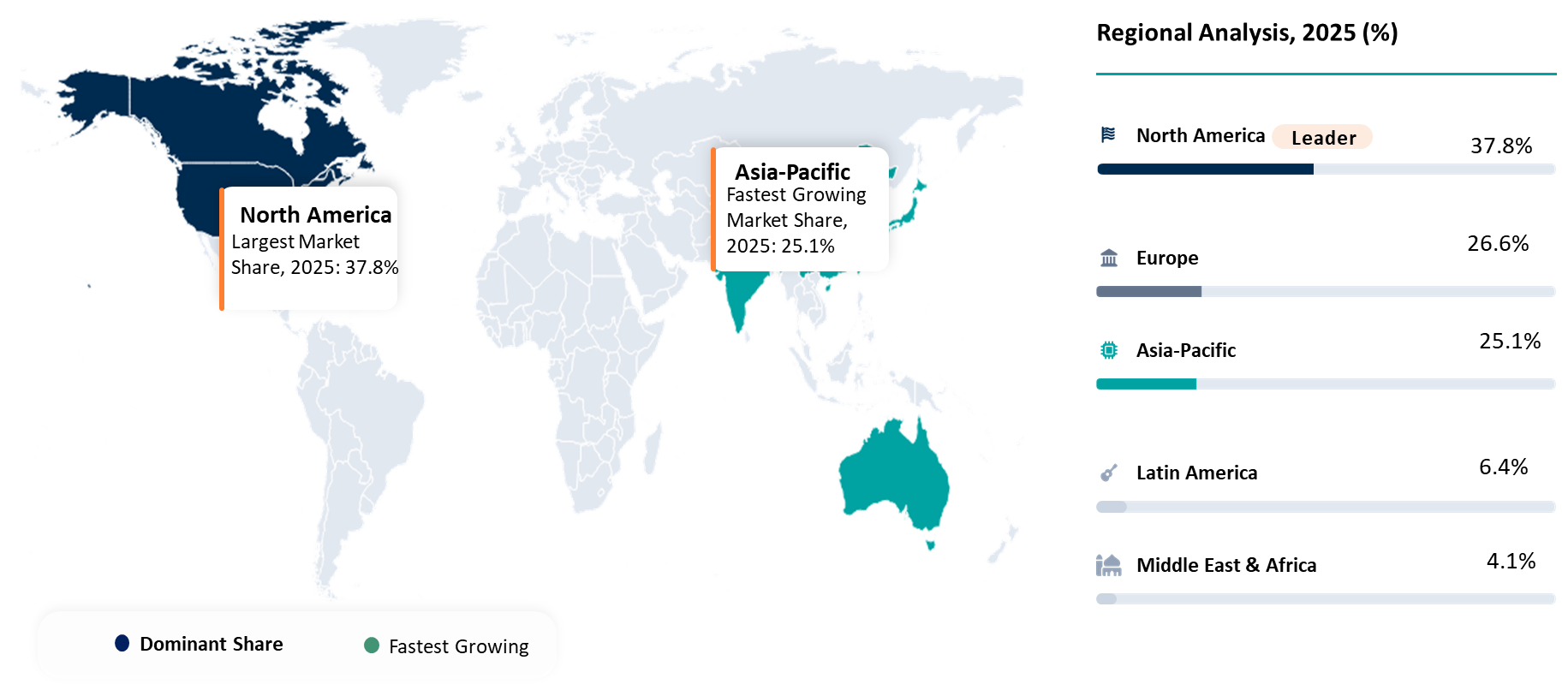

- North America appears to be a major regional player, backed by the sophistication of its packaged foods industry, high consumption of snacks, well-developed frozen foods industry, and robust foodservice logistics network.

- The winning players would be those who provide not only ingredients but also formulation assistance, such as texture analysis, shelf-life studies, clean-label formulations, consistent raw material supply, and regional technical support for food producers.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 482.37 Million | |

| 2035 Projected Market Size | US$ 848.91 Million | |

| CAGR (2026-2035) | 5.82% | |

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Product Type | Starch-Based Crisp Enhancers, Hydrocolloid-Based Crisp Enhancers, Protein-Based Crisp Enhancers, Cellulose-Based Crisp Enhancers, Fiber-Based Crisp Enhancers, Enzyme-Based Crisp Enhancers, Emulsifier-Based Crisp Enhancers, and Others | |

| By Ingredient Source | Plant-Based, Animal-Based, Synthetic, and Microbial-Based | |

| By Form | Powder, Liquid, Granules, and Premixes | |

| By Functionality | Crispness Enhancement, Moisture Barrier Formation, Oil Uptake Reduction, Coating Adhesion Improvement, Texture Stabilization, Shelf-Life Extension, Mouthfeel Improvement, and Others | |

| By Food Processing Method | Frying, Baking, Extrusion, Coating, Drying, and Roasting | |

| By Application | Snack Foods, Bakery Products, Fried Foods, Frozen Foods, Ready-to-Eat Meals, Breakfast Cereals, Confectionery, Plant-Based Foods, and Others | |

| By End User | Food Ingredient Manufacturers, Bakery and Confectionery Manufacturers, Frozen Food Manufacturers, Ready-to-Eat Food Manufacturers, Foodservice Operators, and Others | |

| By Distribution Channel | Direct Sales, Ingredient Distributors, Online B2B Platforms, and Specialty Food Ingredient Suppliers | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

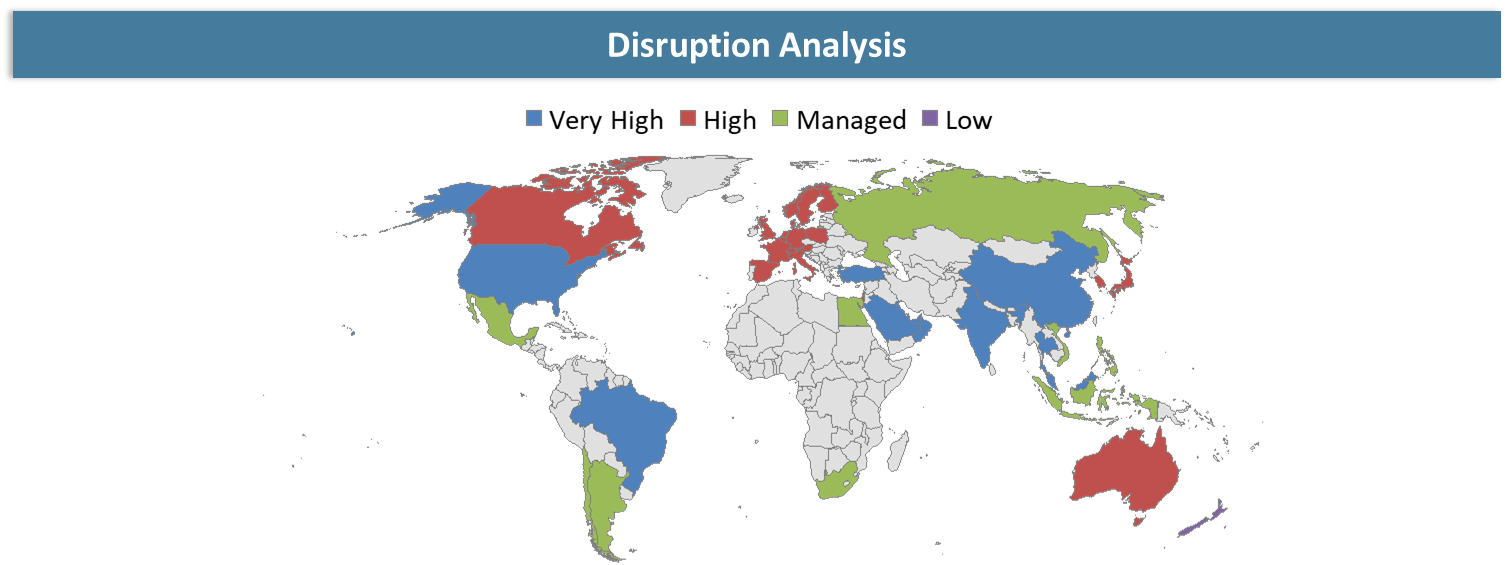

Disruption Analysis

Clean-Label Reformulation and Application-Specific Texture Systems Reshaping Crisp Enhancer Innovation

This disruption is being witnessed due to the transition from generic crispness texture agents to performance-driven and clean label crisping systems. The snack, bakery, frozen foods, and plant-based product manufacturers are not only evaluating their options on ingredient cost anymore; instead, they have started looking into options like crunch maintenance, moisture content control, oil absorption minimization, reheating tolerance, and clean label friendliness.

The disruption is further fueled by the demand for cleaner labeling, as there is a growing interest in crispness without the use of artificial ingredients and highly processed ingredients. On another hand, there is growing demand for crisping agents with performance after freezing, thawing, microwave heating, or air frying. The disruption is yet further fueled by the shift towards plant-based foods, especially since there is a need for enhancing the texture of meat and seafood substitutes. The ones who are providing support in application and customization services and ingredient availability in specific regions are expected to benefit, while commodity ingredient suppliers can be at risk.

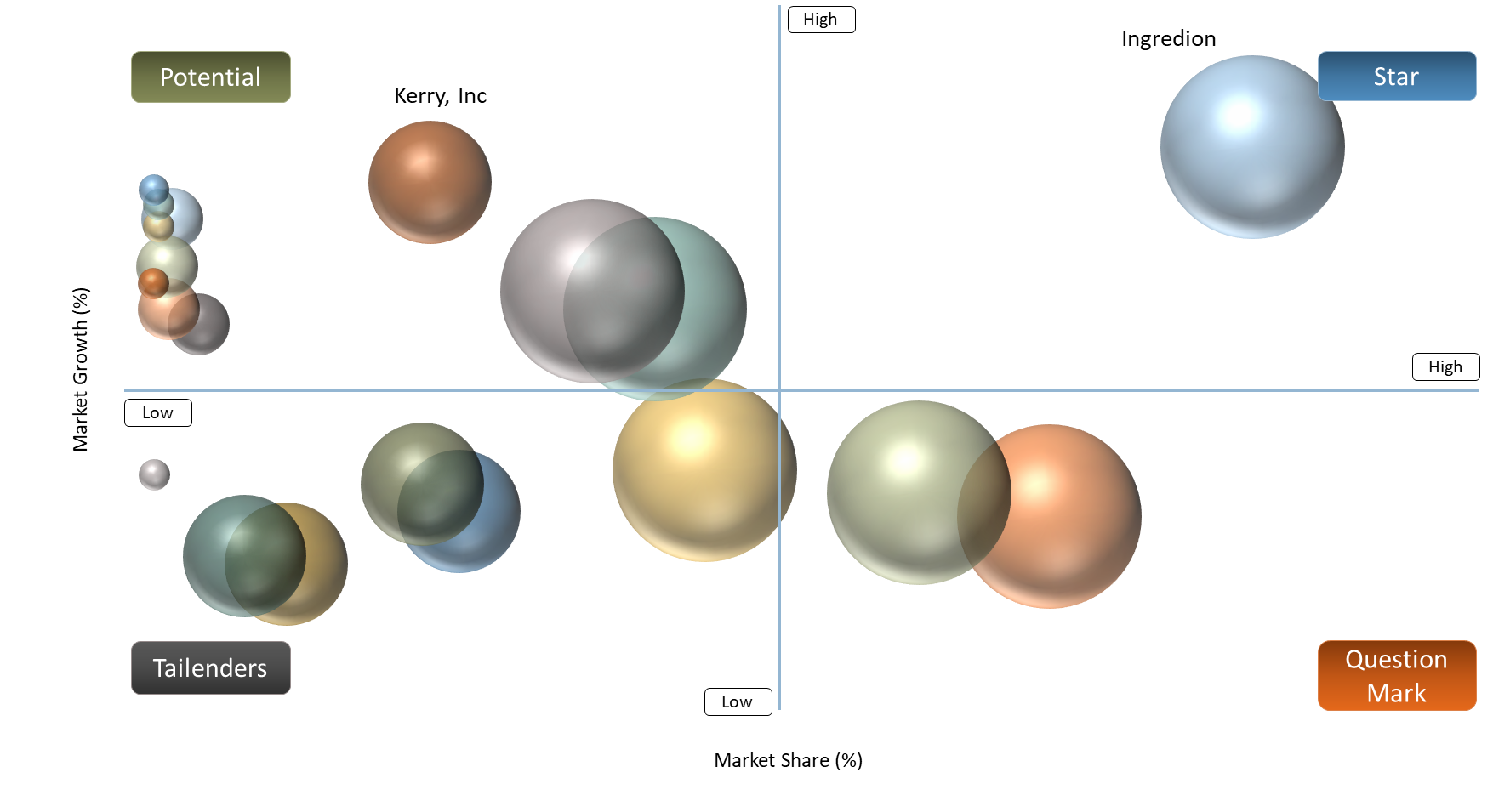

BCG Matrix: Company Evaluation

As for the BCG matrix, the Stars within the Global Crisp Enhancers Market are represented by those companies that have a significant presence globally, high formulation capability, access to the customer base, solid technical support infrastructure and good connections with snack, bakery, frozen food, coating and convenience food manufacturers. The companies like Ingredion, Cargill, Incorporated, Tate & Lyle PLC and Roquette Frères should be positioned as the Stars because they are capable of benefiting from their scale and global capabilities, diverse experience in food ingredients as well as the ability to support large manufacturers of foods using these ingredients.

The Cash Cows are defined as those players, which benefit from stable demand within mature food processing segments, including bakery, cereals, snacks, coatings, frozen foods and foodservice. The names of Avebe, KMC, Emsland Group, BENEO and Kerry, Inc. belong here because they feature strong regional or category positions, recurring orders from mature food manufacturers, good connections with them. These companies would continue generating profits due to the need for ongoing formulation services.

The question mark business involves firms that have good niche relevance but narrow positioning compared to other competitors within the market of crisp enhancers. MGP falls within this segment owing to the company’s high relevance in specific food texture applications but with little market exposure compared to big international ingredients firms. The firm’s potential for expansion is linked to its ability to extend the number of application areas, increase visibility in different regions, and enhance brand awareness within specific industries.

Market Dynamics

Snack Premiumization Accelerating Demand for Crunch Retention Ingredients

Premiumization of snacking is emerging as one of the key drivers for the Global Crisp Enhancers Market due to the growing preference of consumers for superior texture, constant crunchiness, and premium snacking experience among all packaged snacks, bakery snacks, coated nuts, crackers, chips, and extruded snacks. With food companies going beyond the concept of flavor innovation and leveraging texture as a major differentiator for their products, especially premium, natural, gluten-free, protein, and vegan snacks.

Crisp enhancers assist in providing better crunch retention, prevent sogginess, control moisture migration, and offer sustained bite in terms of texture even after the process of packaging, storage, and distribution. Increased competition among snacks has encouraged manufacturers to adopt starch-based, hydrocolloids-based, fiber-based, and coatings-based crisping systems to ensure stable texture and encourage repeat purchases. The demand for crisp enhancers is also gaining traction in baked snacks and healthy snacking options, which require crispness without the requirement of oil and frying.

Application-Specific Performance Variability Limiting One-Ingredient Scalability

The application-specific variation in performance is one of the most important constraints to the Global Crisp Enhancers Market due to the differences in the requirements for crispness in snacks, bakery goods, batter and breaded products, breakfast cereals, candies and ready meals. An ingredient that is highly efficient at achieving the right crispness effect in the fried coatings can be much less effective in baked crackers, extruded snacks, frozen appetizers and microwaveable meals. The level of moisture, the amount of oil, processing temperatures, coating thickness, ingredient interaction and packaging have a direct impact on the performance.

It makes it challenging for food producers to develop a universal ingredient blend for all types of products. Customized mixes will require repeated trial runs, testing for shelf stability, sensory evaluation and other activities prior to implementation. It will take more time and money to implement and rely heavily on the assistance from ingredient manufacturers. Small food processors are likely to refrain from using costly ingredient systems that would not guarantee performance and require modification of the processing lines.

Segmentation Analysis

The Global Crisp Enhancers Market is segmented based on product type, ingredient source, form, functionality, food processing method, application, end user, distribution channel and region.

Snack Foods Dominate the Market as Brands Prioritize Crunch Retention and Premium Texture Differentiation

The leading application segment in the Global Crisp Enhancers Market is snack foods because texture has emerged as one of the key purchase drivers in chips, extruded snacks, crackers, coated nuts, pellets, and baked snacks. Premium snacks now offer a consistent crunch, clean bite, mouthfeel enhancement, and increased crispness longevity, which is why food companies prefer using sophisticated crisp enhancer technology over simple innovations in flavor alone. In today's intense retail shelf competition, marketers use textural differentiation to enhance their product positioning, repeat purchase opportunities, and price premiums.

Crisp enhancers perform many vital functions in snack foods applications, such as improved crunch retention, moisture management, expansion, sogginess reduction, and texture preservation during packaging and storage. Starch-based, rice-based, potato-based, hydrocolloid-based, and fiber-based systems will gain more traction as food companies reformulate their products for clean label, gluten-free, low-oil, and plant-based offerings. The market dominance of snack foods is likely to continue in the coming years because food companies favor textural innovations that can scale up in large production batches and various snack categories.

Geographical Penetration

North America’s Advanced Packaged Food Ecosystem Driving Demand for Application-Specific Crisp Enhancers

North America represents one of the prominent geographies of the Global Crisp Enhancers Market, owing to the presence of an advanced packaged food sector, high consumption of snacks in the region, well-established frozen food industry and efficient food service supply chain. There has been increasing adoption of crisp enhancers for ensuring improved crunchiness, better coatings and moisture management capabilities among chips, crackers, bakery snacks, frozen fries, nuggets, coatings, and ready to cook foods. Product innovation in line with clean label, gluten-free, low oil content and premium eating experience is being encouraged as part of the reformulation process.

The United States accounts for one of the major consumer bases for these ingredients owing to a significant presence of snack producers, bakery companies, frozen food companies, and quick service restaurant ingredient suppliers. Suppliers of such ingredients in North America are working towards offering customized solutions that can ensure consistency of crispness from manufacturing through packaging, transport, reheating, and storage. With rising competition in the world of snacks and convenience foods, there has been a growing focus on texture as a differentiating characteristic.

U.S Crisp Enhancers Market Trends

The U.S. market for crisp enhancers is showing signs of strength due to the growing competition based on texture, sensory performance, and product consistency among food companies. Manufacturers in the sectors of snacks, baked goods, frozen foods, and foodservices use crisp enhancers to achieve better retention of crunchiness, avoidance of sogginess, better adhesion of coatings, and maintenance of quality in foods like chips, crackers, nuggets, frozen french fries, appetizers, and cook-in packaging products. Reformulations in clean label, gluten free, low oil, and premium snacking drive additional demand.

A clear sign of the potential of the market is its size which depends on the size of the overall food industry in the U.S. USDA ERS states that total food expenditures in 2024 amounted to USD 2.58 trillion where the share of food at home was USD 1.06 trillion while the rest USD 1.52 trillion represented expenditures on food away from home. It means that there is constant demand for texture modifying ingredients needed in the formulations of snack, bakery, frozen foods, and food service products.

Japan Crisp Enhancers Market Outlook

The market for crisp enhancers in Japan is projected to witness steady growth backed by its well-developed processed foods industry and vibrant snack culture along with premium bakery consumption and preference for quality convenience foods. Japanese consumers value texture, freshness perceptions, and sensory consistency, wherein crispness, light bite, and clean break significantly impact the acceptance of products. This trend is driving snack, bakery, confectionery, frozen food, and ready meal manufacturers to adopt crisp enhancers for preserving crunch, moisture management, coating adherence, and texture stability.

One of the significant factors reflecting an opportunity in the market is the presence of a large base of food processing in Japan. As per USDA FAS, Japan’s food processing industry witnessed a 3.9% growth in the value of food production in 2024 to reach USD 174 billion. It produces traditional Japanese, Western, and healthy foods, and food processors have continued to innovate products to appeal to consumers. This presents a favorable base for the adoption of crisp enhancers in crackers, coated snacks, bakery products, fried foods, cereals, and ready-to-eat meals. In the coming years, demand will be driven by premiumization, clean-label reformulation, portion-controlled snacking, and texture-preserving products.

Competitive Landscape

The global market for Crisp Enhancers is moderately consolidated, with competition being driven primarily by existing companies in the food ingredients industry which boast high formulation skills, application technology support and customer base consisting of large snack, bakery, frozen foods and convenience foods manufacturers. The prominent competitors within this market, namely, Ingredion, Cargill, Incorporated, Tate & Lyle PLC and Roquette Frères are competitively advantaged, owing to their size, global customer presence and extensive expertise in the areas of texture, starch and food formulation solutions.

Companies like Avebe, KMC, Emsland Group and BENEO contribute significantly to the strength of the market via their specific ingredient expertise and application-driven solutions for snacks, bakery products, cereals and coated foods respectively. Meanwhile, Kerry, Inc is another significant competitor that provides an edge through its formulation-oriented approach targeting customers, especially in coatings and convenience foods, among other foodservice applications. MGP has a relatively niche position as it caters specifically to texture and inclusion applications. Competitive pressure is gradually moving away from commodity raw ingredient supplies towards tailored crisp enhancer systems, technical services and clean labels.

Key Developments

- April 2026: Roquette Frères published the inauguration of its new starch and polyol pilot center at Lianyungang, China, supporting starch-based food formulation and texture development.

- March 2026: Ingredion highlighted plant science-led ingredient innovation for consistent, high-performing texture solutions, relevant to crispness and crunch performance in food applications.

- January 2026: Ingredion emphasized texture optimization and sensory performance in high-protein reformulation, supporting broader use of texture-enhancing ingredients in snacks and bakery-style applications.

- November 2025: Emsland Group highlighted its growing Asia-Pacific presence, supporting regional expansion of starch-based and food texture solutions.

- November 2025: Emsland Group discussed ultra-processed food from a differentiated perspective, relevant to formulation improvement and ingredient functionality in processed food categories.

- July 2025: Emsland Group published “Clean Label, Clear Benefits,” supporting clean-label starch and texture ingredient positioning.

- May 2025: Ingredion discussed plant-based egg substitutes with texture and shelf-life benefits for bakery and snack applications.

- November 2024: Tate & Lyle PLC completed the acquisition of CP Kelco, strengthening its specialty gums, pectin and nature-based ingredient capabilities for texture and stability applications.

- November 2024: Avebe won recognition at Food Ingredients Europe 2024 for potato-based plant-based food innovations, including adhesive coating solutions relevant to crispy coatings.

- May 2024: Roquette Frères expanded its CLEARAM TR botanical tapioca starch range, strengthening its plant-based texturizing solutions for food manufacturers.

White Space Opportunities

Areas of white space within the global crisp enhancers market include clean label, application-specific, and stability-focused texture innovations. As the food industry moves towards formulating more complex products with better performance and nutrition profiles, food producers are less interested in standard texture agents and seek crisp enhancers that could resolve issues like moisture migration, sogginess post-reheating, oil absorption, coating degradation, and reduced crunchiness over time. Such an environment opens up substantial opportunities for suppliers of rice, potato, tapioca, pea starches, fiber systems, and hydrocolloid mixtures.

However, the most attractive areas of white space include air-fried snacks, frozen coated foods, meatless meats, gluten-free bakery, and high protein snacks, wherein the texture issue continues to be the main obstacle to consumer acceptance. Brands that are entering into these sectors would want their products to maintain crispy textures while at the same time maintaining nutritional benefits, simplicity on labels, and easy processability. In the ingredient world, suppliers can stand out by providing customized crisping solutions, sensory assessment, shelf-life studies, and applications training instead of selling individual ingredients. Geographical opportunities exist in the Asia-Pacific and Latin American regions where innovations in snacks and ready-to-eat meals are driving demand.

DMI Opinion

According to DataM, the key impediment to market entry is not lack of demand, but rather the supplier’s ability to translate different textural needs into commercially viable performance for snacks, baked products, coated and battered foods, cereals, confectionery, and convenience foods. The market rewards vendors with a portfolio that goes beyond simply delivering an ingredient, including formulation support, application testing, clean-label capabilities, moisture control performance, shelf-life verification, and reliable quality.

Crispness maintenance, coating integrity, low oil uptake, bite consistency, resistance to overheating, allergen information, and cost-in-use considerations are gaining importance among food manufacturers as purchase criteria. Food manufacturers of snack foods, frozen foods, bakery, plant-based and foodservice items have increased their interest in suppliers that are able to minimize reformulation risks and exhibit performance under various processing conditions such as frying, baking, extrusion, freezing, and microwave reheating.

Although some suppliers still choose to compete primarily based on price or cost, the sustainability of such a strategy might be challenged by consumer demands for unique textures, clean label information and superior sensory characteristics. Vendors offering crisping system formulations, plant-based options, gluten-free solutions and expert formulation knowledge are well-suited to succeed in the international market.

Why Choose DataM?

- Innovation in Ingredients: Investigates the progress made in crisp enhancer ingredients formulation, looking into various types including modified starches, rice starch, potato starch, hydrocolloids, cellulose derivatives, emulsifiers, enzymatic systems, clean-label crisp enhancers and texture enhancers from plants.

- Evaluation of Performance & Positioning within Formulations: Examines the efficacy of various crisp enhancer ingredients when applied in snacks, baked goods, fried foods, frozen foods, breakfast cereals, coatings and plant-based foods. The comparison covers factors such as crispness retention, moisture management, reduction in oil uptake, adhesion of coatings, texture stability and shelf-life performance.

- Practical Applications of Crisp Enhancers: Identifies examples of crisp enhancers in action through applications such as potato chips, extruded snacks, crackers, wafers, coated nuts, frozen French fries, fried chicken coatings, tempura batters, bakery coatings and ready meals. It discusses the role of modifying texture to enhance consumer appeal and encourage repurchase.

- Market Developments & Industry Changes: Follows changes in the market such as clean label reformulation, low oil frying, gluten-free snack development, plant-based food texturization, premiumization in frozen foods, new ingredient launches and increasing need for snacks' texturization in North America, Europe, Asia-Pacific and developing regions.

- Competitive Strategies: Examines competitive moves that key ingredient suppliers are undertaking to fortify their market share with advances in starch technology, coating systems, clean-label ingredients, formulation expertise, geographic coverage and collaboration with snack, bakery and frozen food makers.

- Pricing & Market Access: Discusses pricing trends in crisp enhancer formulations, hydrocolloid blends, emulsifier combinations, specialized coating agents and clean-label texture enhancers. The report highlights supplier capabilities, distribution channels, formulation expertise and geographic presence in food production.

- Market Opportunities & Expansion: Highlights growth drivers resulting from increased snacking, high-end bakery products, frozen foods, quick service restaurant operations, plant-based foods and clean label reformulations. It also provides recommendations on market entry and expansion for ingredient providers through application-focused innovations, local formulation services and partnerships with food producers.

Target Audience 2026

- Snack food manufacturers

- Bakery and confectionery manufacturers

- Frozen food and ready-to-eat meal producers

- Fried food coating, batter and breading solution providers

- Food ingredient and texture solution manufacturers

- Starch, modified starch and hydrocolloid suppliers

- Breakfast cereal and extruded snack manufacturers

- Meat, seafood and plant-based food processors

- Quick-service restaurant and foodservice suppliers

- Procurement, R&D and product innovation teams