Ceramic Sanitaryware Market Overview

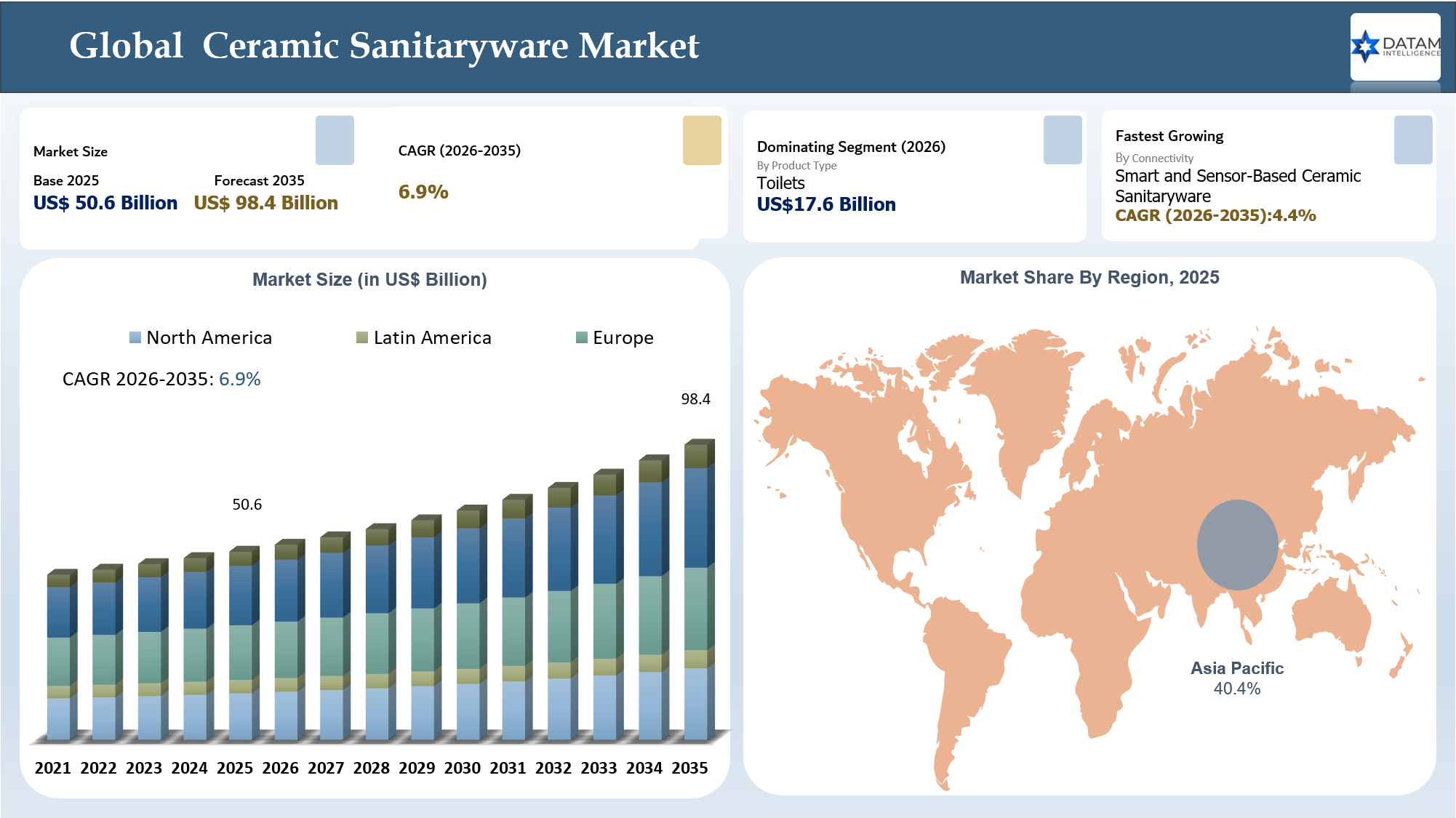

The Global Ceramic Sanitaryware Market stood at US$ 50.6 billion in 2025 and is expected to reach US$ 98.4 billion by 2035, growing with a CAGR of 6.9% during the forecast period 2026-2035.

The ceramic sanitaryware market is witnessing a major shift as water conservation and hygiene-oriented washroom design is turning into essential criteria rather than add-ons while making purchasing decisions. The customers now prefer buying sanitary products like toilets, basins, urinals and cisterns that provide maximum water savings and are easy-to-clean, hygienic, durable and cost-effective in terms of maintenance in the long run. This is being brought about by growing urban water scarcity, green building demands, increased sanitation needs and growing demand for low maintenance washrooms at homes, hotels, commercial premises, hospitals, educational institutions, airport and other public spaces.

The major factor influencing the market is water-saving and hygiene-centric ceramic sanitaryware. The features like dual flush toilets, rimless toilets, antibacterial glaze, easy-clean finish and stain resistant ceramics are becoming more significant for the consumers because the products with water conserving capabilities and better hygiene are gaining greater importance. This provides immense benefits for developers and institutional buyers in terms of reducing costs and enhancing washroom hygiene standards. At the same time, it presents a great opportunity for the manufacturers of sanitaryware as they can shift their strategy towards higher quality, modern design and value-based offering of the products bundled as per projects.

Key Takeaways

- The Ceramic Sanitaryware Market is projected to grow from US$ 50.6 billion in 2025 to US$ 98.4 billion by 2035, registering a CAGR of 6.9%.

- The market is expected to add nearly US$ 47.8 billion in incremental revenue between 2025 and 2035.

- Asia-Pacific remains the strongest demand region, supported by urbanization and infrastructure investment. Asia already has more than 2.2 billion people living in cities, and its urban population is expected to grow by 50% by 2050.

- Developing Asia needs around US$ 1.7 trillion per year in infrastructure investment through 2030, including transport, water supply and sanitation, directly supporting project-led ceramic sanitaryware demand.

- Toilets remain a key demand category because they account for nearly 30% of average household indoor water consumption, making water-saving and high-efficiency ceramic toilets an important replacement and upgrade segment.

- Sanitation gaps continue to support long-term demand, as 3.4 billion people globally still lacked safely managed sanitation services in 2025, creating opportunities for durable and affordable sanitaryware products.

Ceramic Sanitaryware Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 50.6 Billion | |

| 2035 Projected Market Size | US$ 98.4 Billion | |

| CAGR (2026-2035) | 6.9% | |

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Product Type | Toilets, Basins and Washbasins, Urinals, Bidets, Cisterns and Flush Tanks, Ceramic Bathroom Accessories and Others | |

| By Material | Vitreous China, Fine Fireclay, Fireclay, Porcelain, Earthenware, Stoneware and Others | |

| By Connectivity | Non Connected Ceramic Sanitaryware, Connected Ceramic Sanitaryware, Smart and Sensor-Based Ceramic Sanitaryware and Others | |

| By Product Feature | Water Saving, Antibacterial Glazed, Easy Clean Coated, Anti Slip, Stain Resistant, Scratch Resistant and Others | |

| By Price Range | Economy, Mid Range, Premium and Luxury | |

| By Distribution Channel | Offline and Online | |

| By Project Type | New Construction, Renovation and Replacement and Others | |

| By Manufacturing Model | Mass Produced, Batch Produced, Artisanal and Studio, Private Label, Direct to Contractor and Others | |

| By End User | Residential, Commercial, Healthcare and Education, Industrial and Institutional, Infrastructure and Transportation Facilities and Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Disruption Analysis

Ceramic Sanitaryware Is Moving From Basic Bathroom Fixtures to Design-Led and Hygiene-Centric Bathroom Solutions

Market disruption in the ceramic sanitaryware industry is brought about by change in customer tastes, from traditional sanitary fixtures to designer bathrooms that offer convenience as well as better hygiene levels in washroom installations. Customers are not only demanding for toilet bowls, basins, and cisterns which they would use in new constructions or replacement but also rimless toilets, wall hung fixtures, concealed cisterns, countertop basins, antibacterial glaze, and easy-to-clean ceramic surfaces. Manufacturers are now compelled to stop relying on quantity sales alone, but instead sell on the basis of superior product performance, aesthetics, maintenance capability, and overall bathroom experience.

Sustainability, digital discovery, and smart features are also transforming the industry. Products that promote sustainability include water-efficient toilets, dual-flush systems, and durable ceramic fixtures, which are becoming increasingly important due to green building codes and water conservation requirements. Furthermore, the development of smart ceramic sanitaryware featuring sensors is giving rise to high-end products for use in premium private residences, hotels, office buildings, and transit facilities. Digital platforms are enhancing product comparisons and pricing transparency, although actual sales may still be made offline through distributors or general contractors. Thus, success in this market will depend on product innovation, distribution networks, project sales, digital presence, and efficient production.

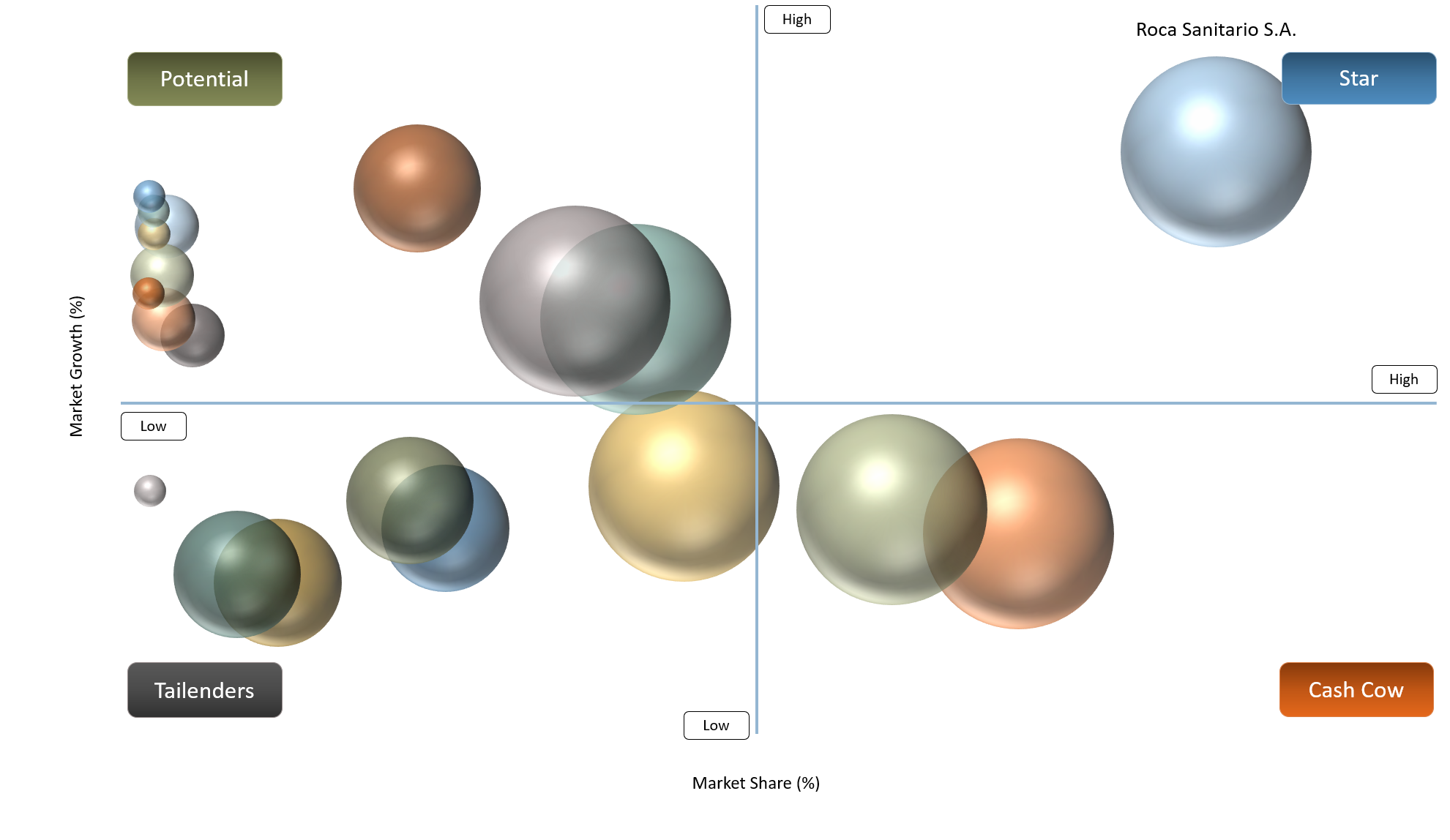

BCG Matrix: Company Evaluation

The key players in the ceramic sanitaryware industry include Stars like Roca Sanitario S.A., Kohler Co., TOTO Ltd., LIXIL Corporation, Geberit AG and RAK Ceramics PJSC, owing to their high brand value, international presence, wide range of ceramic sanitaryware products, and constant innovations in their offerings. This segment is dominated by premium toilets, basins, urinals, cisterns, technologically advanced and water-efficient products, and strong penetration in residential, commercial, hotel, and infrastructure projects. They benefit from growth in bathroom remodeling, urban construction, hygiene-driven improvements, and project-based buying. The Cash Cow segment comprises companies like Villeroy & Boch AG, Duravit AG, Ideal Standard International, and Porcelanosa Grupo, who have strong market share in mature premium markets due to the emphasis on aesthetics, quality, brands, and specifications-led purchases.

Question Marks are comprised of Jaquar Group, VitrA, CERA Sanitaryware Limited, Hindware Limited and Lecico Egypt. This is due to the fact that these companies have an existing regional footprint and expanding product offerings, but yet require increased global presence, enhanced brand premium and greater influence on project specifications in order to rival global competitors. The growth prospects for these firms are significant in developing countries, affordable housing developments, renovation opportunities and institutional facilities. On the other hand, there are no Dog products in any of these leading firms, although smaller or regionally-focused companies may fall under such a classification due to product differentiation issues, price competition and ceramic sanitaryware trends.

Ceramic Sanitaryware Market Dynamics

Ceramic sanitaryware demand is shifting from basic replacement purchases to design-led bathroom upgrades, supported by rising focus on hygiene, aesthetics, durability and property value enhancement

The increasing demand for ceramic sanitaryware products is not limited to basic replacement purchases but has been driven more by aesthetic preferences. The growing importance of hygiene and aesthetic considerations in product choice, along with durability and the ability to add value to properties through renovation work, has made it less acceptable to simply purchase toilet bowls, basins, and cisterns based solely on practicality requirements. Instead, there has emerged a need for products that do not just serve a basic function within the bathroom but can contribute towards overall property value appreciation. As a result, an increase in demand has been witnessed for rimless toilets, countertop basins, wall-hung sanitaryware, concealed cisterns, non-stick surfaces, as well as integrated bathroom suites. Additionally, the smaller bathrooms found in the urban residential segments are driving the demand for compact yet aesthetically pleasing sanitaryware products. Finally, hygiene has become an increasingly important factor in the purchasing decision for such items, especially in hospitals, hotels, corporate spaces, schools, and other public places. Developers, hospitality companies, and commercial property owners have begun leveraging ceramic sanitaryware products in order to enhance the perceived value of their assets.

Energy-intensive kiln firing is increasing production cost pressure for ceramic sanitaryware manufacturers, especially in markets exposed to natural gas and electricity price volatility.

Increasing cost pressure due to energy intensive firing of the product in kilns is experienced by ceramic sanitaryware producers in markets where gas and electricity prices are volatile. High-temperature firing of ceramic sanitaryware products is done in order to make them durable, strong and resistant to water. Therefore, energy cost constitutes one of the most significant cost elements in production. When there are changes in gas and electricity costs, manufacturers experience increased pressure on their production cost structure because it is not possible to increase prices significantly on mass produced sanitaryware products like toilets, urinals and basins. The problem is even more acute for small and medium scale producers who use old kilns or lack modern and efficient means of production. However, at the same time, customers who buy sanitary ware in economy or mid range category are also very price sensitive and it becomes difficult to pass increased costs on to dealers, contractors and end users. Energy cost fluctuations may also adversely impact export opportunities since producers located in low-cost areas will be better placed in terms of prices.

Segmentation Analysis

The global ceramic sanitaryware market is segmented based on product type, material, connectivity, product feature, price range, distribution channel, project type, manufacturing model, end user and region.

Toilets Remain the Demand Anchor of Ceramic Sanitaryware as Essential Installations, Water Efficiency and Sanitation Gaps Drive Long-Term Growth

Toilets are the largest sub-segment within the Ceramic Sanitaryware Market as they form the key source of demand within all built-up environments such as residential, commercial, institutional, public and healthcare buildings. In contrast to the other sanitary products such as washbasins, bidets, and accessories, toilets are mandatory installations, and thus they are crucial in new construction and replacement led demand dynamics. This is also facilitated by major affordable housing projects, public infrastructure investments, and urban sanitation initiatives, which focus on installing toilets as a priority component in order to improve hygiene and sanitation.

In addition to being a volume-driven category, the segment is also becoming a value-growth category. Rising demand for rimless, wall-hung, dual flush, water-saving, and smart toilets enables players to earn premium margins by offering value-added and innovative features. According to the U.S. EPA, nearly 30% of indoor household water use is attributable to toilets. Hence, it becomes important for households to install high efficiency toilets. WHO/UNICEF indicated that more than 3.4 billion people lacked safely managed sanitation in 2024.

Geographical Penetration

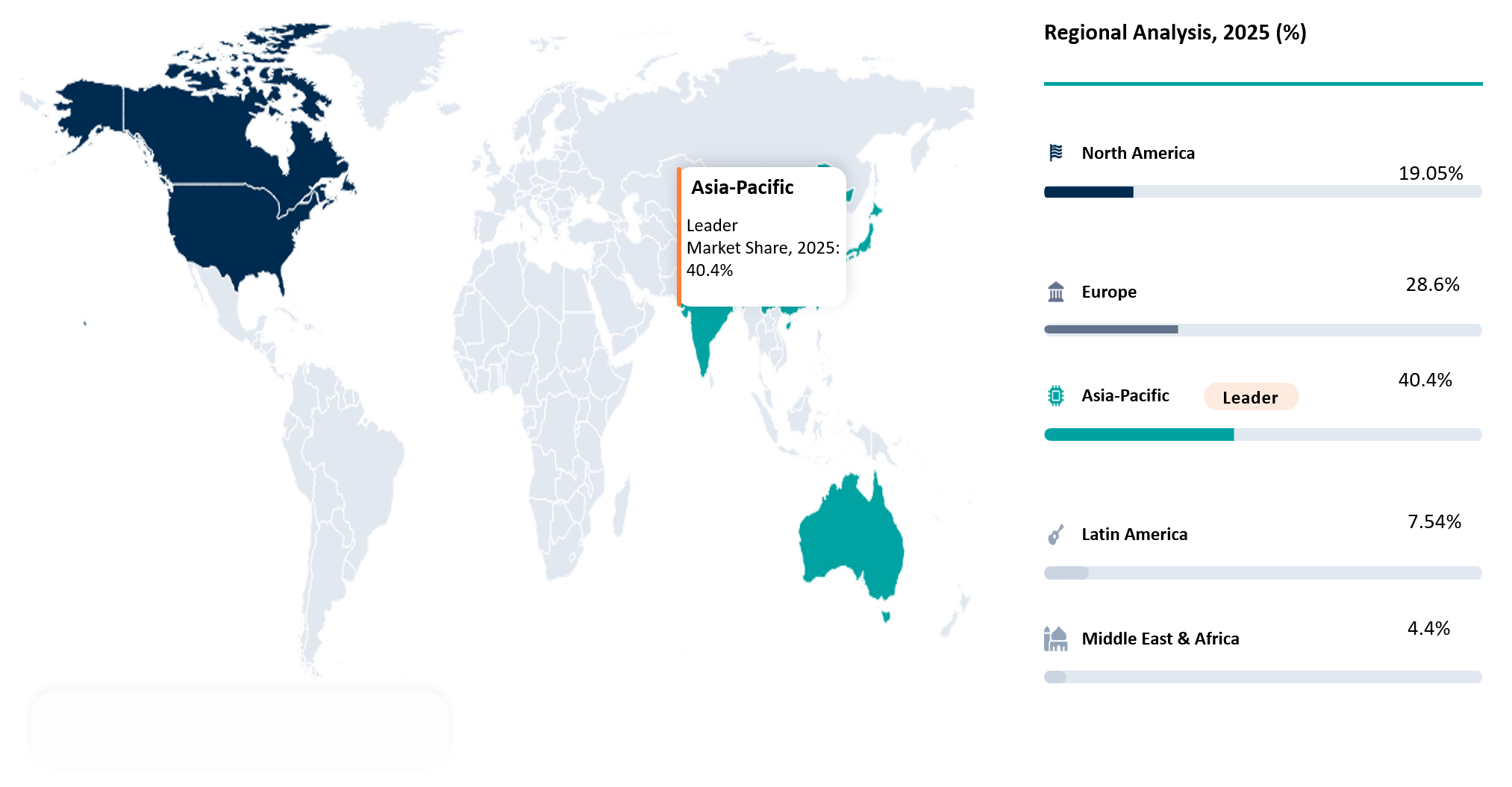

Asia-Pacific Leads Ceramic Sanitaryware Growth as Urban Expansion, Sanitation Gaps and Infrastructure Spending Drive Structural Demand

The Asia-Pacific region is set to continue dominating the Ceramic Sanitaryware market and experience robust growth due to unmatched urban development and investments made in the region. The urban population in Asia comprises 54% of the total urban population worldwide and stands at over 2.2 billion individuals, with an expectation of 50% growth in urban population until 2050. These factors translate into substantial structural demand for sanitary fixtures including toilets, washbasins, urinals, cisterns, and bathroom sets used in residential apartments, commercial properties, educational institutions, hospitals, hotels, and other public infrastructure. According to ADB, Asia requires $1.7 trillion worth of infrastructure investments annually through 2030, including transportation and water & sanitation.

According to the consultancy approach, the leadership in the Asia-Pacific region is both demand-driven and supply-driven. There is abundant manufacturing depth from China, India, Vietnam, and Indonesia. In addition, the growing population and the remodeling of bathrooms have increased the use of wall-mounted toilets, vanity basins, concealed cisterns, water-saving sanitary fixtures, and smooth ceramic finishes. In terms of demand, there is still a need for sanitation due to the fact that WHO/UNICEF stated that 1.2 billion people worldwide were provided with safe sanitation services from 2015 to 2024. Furthermore, it is anticipated that by 2030, there will be 22 megacities in the Asia-Pacific region.

Japan Ceramic Sanitaryware Market Trends

Japan emerges as an example of a developed yet high-opportunity market in terms of the Ceramic Sanitaryware Market, thanks to its requirements for renovations, dense urban population, aged infrastructure, hospitality industry developments, and high affinity towards bathroom solutions that prioritize hygiene. The Japanese urban population was estimated to be around 114.3 million in 2024, thus constituting a dense consumer base for toilets, washbasins, urinals, cisterns, and small-sized bathrooms in apartments, hotels, offices, hospitals, and public infrastructures. Moreover, Japan has a robust sanitation base; hence the utilization rate of safely managed sanitation facilities was 99% in 2024, leading to growth opportunities for replacement products, luxury sanitary fixtures, water-saving products, and smart bathrooms.

According to a consultancy approach, the need for ceramic sanitaryware in Japan will depend on such factors as quality, aesthetics, efficient usage of space and lifecycle performance, but not solely on expansion of volume. In addition, housing starts and construction activity will play a role in demand for sanitaryware; moreover, the Ministry of Land, Infrastructure, Transport and Tourism in Japan records housing starts by type of residence, construction technique, structure and finance sources, thus, making it possible to measure demand at the level of project. Finally, the hospitality industry will provide demand for replacement sanitaryware; indeed, JETRO sees hotels as attractive tourism and hospitality destinations in Japan, and there is ongoing expansion of overseas luxury hotels in the country.

U.S. Ceramic Sanitaryware Market Outlook

The U.S. Ceramic Sanitaryware Market is supported by renovations-driven replacement, luxury bathroom installations, and new constructions. Home maintenance and improvements contribute around US$600 billion each year to the United States, ensuring a solid base for bathroom refurbishment and replacement of ceramic toilets, basins, and cisterns. U.S. housing starts stood at 1.465 million units at an annual rate in April 2026.

Efficient water usage remains one of the main demand drivers in the U.S., with consumers choosing high-efficiency toilets, dual flushes, and low water-use sanitary ware to lower utility expenses and stay sustainable. U.S. construction spending is substantial in both residential (US$929.7 billion in March 2026) and non-residential sectors (US$729.4 billion in March 2026). From the consultancy point of view, the most promising areas include remodeling, water-efficient products, self-cleaning ceramic materials, accessible bathrooms, and luxurious designs.

Competitive Landscape

The ceramic sanitaryware industry is moderately concentrated at the premium and global brand level but highly fragmented in regional and economic sectors. Competitors like Roca Sanitario S.A., Kohler Co., TOTO Ltd., LIXIL Corporation, Geberit AG, Villeroy & Boch AG and Duravit AG compete by way of brand equity, leadership in design, product innovation, water saving technology, smart features and specification in residences, hotels and business premises. The competitive advantage of these companies lies in their comprehensive product ranges, superior finishing, rim-free bowls, hidden cisterns, easy-to-clean surfaces and efficient sales via dealers and projects.

Regional and emerging competitors like RAK Ceramics PJSC, Jaquar Group, VitrA, Lecico Egypt, CERA Sanitaryware Limited and Hindware Limited are competing effectively based on pricing and project-based requirements by leveraging localized production, distributor networks, construction company collaborations, and middle-end product offerings. The focus of competition is increasingly moving beyond just price and availability into product longevity, hygiene characteristics, design options, ease of installation, and bulk availability. In the future, those firms that demonstrate high manufacturing efficiency, online presence, omnichannel distribution, ability to win projects, and a range of ceramic products are likely to benefit.

Recent Developments

- October 2025: RAK Ceramics participated at Saudi Build 2025 and showcased its latest tiles, sanitaryware and KLUDI faucet collections, strengthening its visibility in Saudi Arabia’s project-led construction and mega-project demand.

- July 2025: CERA Sanitaryware launched POLIPLUZ, a new brand focused on smart and affordable bathroom solutions, expanding its reach in value-driven sanitaryware and bath fitting demand.

- March 2025: TOTO India launched a new matte washbasin collection in finishes such as Matte Black, Matte White, Matte Grey and Matte Beige, reflecting rising demand for premium and design-led ceramic bathroom products.

- March 2025: Roca presented its latest bathroom collections, products and technologies at ISH Frankfurt 2025, reinforcing its positioning around design, innovation and sustainability in the sanitaryware industry.

- January 2025: TOTO India hosted its yearly ACP educational program with factory tour and training, supporting stronger channel capability, product knowledge and brand engagement in India’s sanitaryware ecosystem.

- August 2024: TOTO India completed 10 years of manufacturing excellence in Gujarat and announced strategic expansion to strengthen regional connect across its bathroom product portfolio.

AI Impact Analysis

AI is anticipated to impact the ceramic sanitary ware industry through its involvement in the design process, production, quality control, demand prediction, and consumer interaction. In product innovation, designers can use AI technology to evaluate consumer tastes, bathroom configurations, physical attributes of the product, color schemes and installation aspects that would lead to the design of market-responsive designs for the manufacture of toilets, basins, urinals, and ceramic ware. Such technology allows for the rapid creation of efficient, energy-saving, easily cleanable and designer toilet products, particularly those meant for urban residential areas, hotels and office spaces. AI will also aid the production of intelligent and sensory-based ceramic sanitary ware products.

On the production side, there could be significant improvements in kiln performance, defect detection, glaze control, and production yields. Some of the problems faced during production of ceramic sanitary wares include firing problems, cracking, warping, uneven glazing, and high energy consumption. The use of AI-based solutions in terms of visual inspections and process prediction is likely to detect problems early enough and minimize the rejection rate. Such improvements are crucial since kiln firing is still one of the major expenses incurred by manufacturing firms. In addition, AI-powered forecasting of demand can enable manufacturers to have improved inventory management skills. Stock imbalance between dealers and project-based delivery issues could be avoided through the adoption of such technology. Nonetheless, some of the smaller firms might be slow in adopting such solutions because of costs, availability of data and technical issues.

White Space Opportunities

White space opportunities in the ceramic sanitaryware industry are evident in various categories of water-saving, hygiene-focused, and design-oriented sanitaryware products. Significant potential is available for the manufacture and sale of dual-flush toilets, low-flow urinals, and water-saving toilet cisterns for cities facing water shortages, green buildings, hotels, and other public utility installations. Anti-bacterial glazing and stain-resistant sanitaryware are also white spaces due to their suitability in hospitals, airports, schools, shopping malls, and public toilets where perception of hygiene and ease of sanitation are essential. Compact sanitaryware for bathrooms in densely populated apartment blocks can also be an opportunity in sanitary ware products that include wall-mounted toilets, corner wash basins, and hidden toilet cisterns. Premium matte finish, color-casted sanitary ware, and bathroom suite sets could also provide opportunities in high-end residential buildings and boutique hotels. Another opportunity would be project-oriented sanitary ware kits including toilet sets for real estate developers, building contractors, and hotel chains at standardized prices.

DMI Opinion

DMI expects the ceramic sanitaryware industry to evolve from a product-based replacement market into one characterized by value-based bathroom solutions in which design, hygiene, water conservation and project suitability will drive growth. Although conventional toilet, basin, and cisterns will still account for volume sales, future growth in value terms will be driven by rimless toilets, wall-mounted models, countertop basin designs, concealed cisterns, anti-bacterial coating and easy-to-clean ceramic surface finishes. The leading segments in terms of demand will include urban homes, bathroom refurbishment, hotel upgrades, hospitals, public sanitation projects and transportation construction.

Competition wise, companies depending on the usual white ceramic wares and dealer sales channels may struggle because of local competitors and pricing sensitivities. Brands that will have better positions include those that will be able to provide bundled solutions for developers, unique premium ceramic finishes, innovative water conservation products, strong project management skills and online presence. Manufacturers who will have more efficient factories will enjoy cost savings because of high energy consumption involved in kiln firing processes and raw material instability.

Why This Report Matter in 2026?

The ceramic sanitaryware sector in 2026 will prove important as consumer need is not limited to the provision of new bathrooms or replacement needs. Consumers are now focusing on a trend towards hygiene-focused, water-efficient and innovative bathroom products. In effect, consumers will make comparisons between rimless toilet bowls, easy-to-clean basins, antibacterial glazed products, concealed cisterns and other premium ceramic finish products. In the current market landscape, it is imperative for businesses such as manufacturers, developers, distributors and investors to have knowledge of these changes so as to realize value in terms of business development.

This research will help organizations understand which parts of the market are presenting the best opportunities in areas such as product type, materials, connectivity, product features, end users, distribution methods and projects. It will further explain how factors such as increased costs of energy, raw material price volatility, fragmented distribution systems and local pricing will affect profitability in this sector. In 2026, businesses with the ability to offer ceramic quality, efficient water usage, innovative designs, project opportunities and digital presence will enjoy more success. This report is important in that it transforms an otherwise fragmented sanitary ware industry into one of opportunities.

Why Choose DataM?

Consulting-Led Market Intelligence

DataM goes beyond standard market sizing by connecting ceramic sanitaryware demand with product strategy, project procurement, renovation trends, pricing pressure and competitive positioning.

Actionable Segmentation Framework

The report provides commercially relevant segmentation across product type, material, connectivity, features, end users, channels and project type to support clear opportunity mapping.

Strong Competitive Benchmarking

DataM evaluates leading companies based on portfolio strength, regional presence, innovation focus, project capabilities and positioning across premium and value-driven markets.

Demand-Side and Project-Led Insights

The study captures demand from residential, commercial, hospitality, healthcare, infrastructure and public sanitation projects, helping clients identify high-growth customer groups.

Strategic Decision Support

DataM helps manufacturers, distributors, investors and developers understand where to compete, which products to prioritize and how to improve market entry, expansion and sales planning.

Key Procurement Priorities and Buyer Evaluation Criteria

- Buyers in the Ceramic Sanitaryware Market prioritize product durability, glaze quality, dimensional accuracy and long service life, as poor ceramic quality can lead to cracks, staining, leakage issues and higher replacement costs across residential, commercial and public facility projects.

- Hygiene and ease of maintenance are major evaluation factors, with buyers assessing rimless designs, antibacterial glazed surfaces, easy-clean coatings, stain resistance, flushing efficiency and suitability for high-footfall washroom environments such as hospitals, airports, schools, hotels and public toilets.

- Water efficiency is becoming a critical procurement priority, especially in urban housing, green buildings, hospitality and public infrastructure projects, where dual-flush cisterns, water-saving toilets and low-water urinals help reduce operating costs and support sustainability requirements.

- Buyers increasingly prefer suppliers that can offer complete ceramic sanitaryware bundles, including toilets, basins, urinals, bidets, cisterns and bathroom accessories, as developers, contractors and hospitality chains look for standardized design, consistent quality, faster delivery and simplified procurement.

- Commercial reliability is becoming a key selection criterion, with buyers evaluating brand reputation, dealer network strength, project supply capability, warranty support, installation compatibility, after-sales service and the ability to meet bulk orders across new construction, renovation and replacement projects.

Related Reports:

Explore additional market intelligence and industry insights related to sanitaryware, smart homes, water management, and sustainable infrastructure. These reports provide deeper analysis of emerging trends, growth opportunities, technological advancements, and competitive dynamics shaping the future of water-efficient and connected living environments.

Sanitary Ware Market

Smart Home Market

Water Treatment Equipment Market

Industrial Water Treatment Market

Smart Water Valves Market