CAUTI Prevention Urology Products Market Size

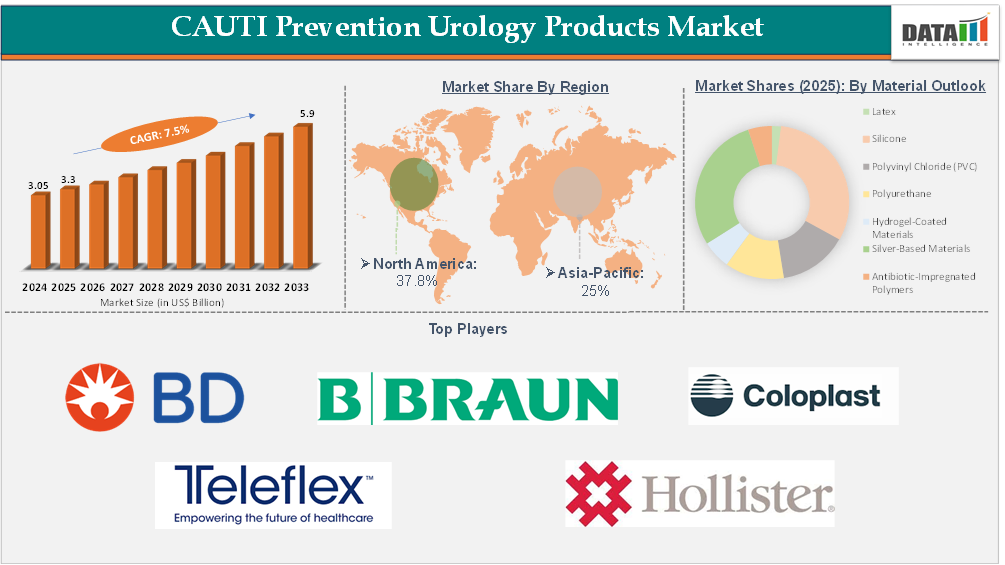

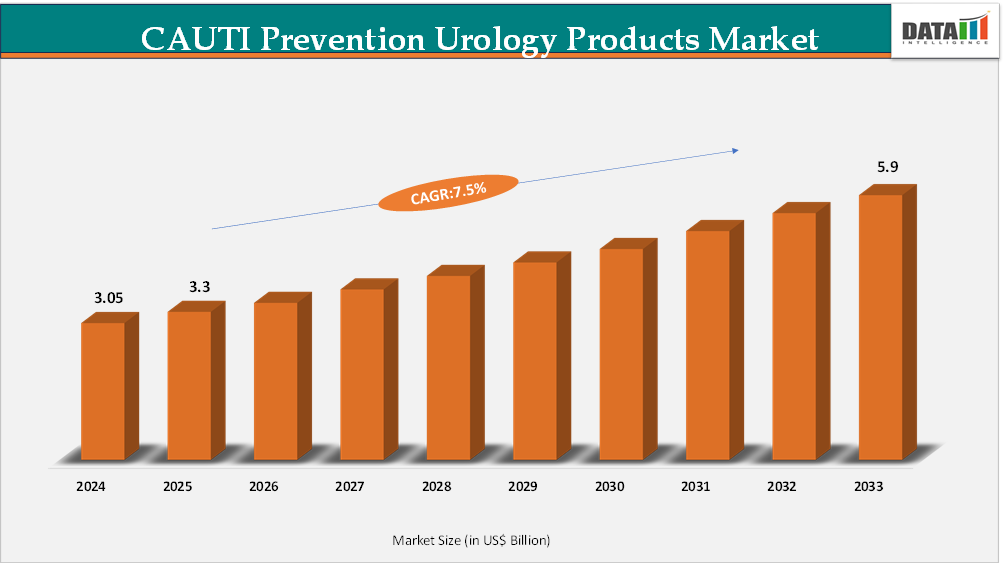

The Global CAUTI Prevention Urology Products Market reached US$ 3.30 billion in 2025 and is expected to reach US$ 5.90 billion in 2033, growing at a CAGR of 7.5% during the forecast period (2026–2033).

During the past decade CAUTIs have become a significant and largely preventable healthcare burden, with an estimated 65%–70% of infections being avoidable through implementation of proven prevention strategies. In the United States, between 95,000 and almost 388,000 CAUTIs could be averted each year and approximately 2,200 to 9,000 lives saved annually. A single episode of a CAUTI costs at least $600 from the economic perspective, while UTIs that result in bloodstream infections have exceeded costs of $2,800 per case, with overall annual preventable costs ranging from $115 million to 1.8 billion.

In Europe, it is estimated that there are 4.1 million healthcare-associated infections reported in the European Centre for Disease Prevention and Control (ECDC) annually, with urinary tract infections accounting for approximately 30%. In clinical practice, prolonged catheterization has long been known as the predominant risk factor and bacteriuria increases at 3% to 8% with each day of catheterization. These conditions are driving the uptick of CAUTI prevention urology products such as antimicrobial and coated catheters, closed drainage systems and catheter care, contributing to long-term market growth influenced by patient safety concerns and cost containment pressures.

CAUTI Prevention Urology Products Industry Trends and Strategic Insights

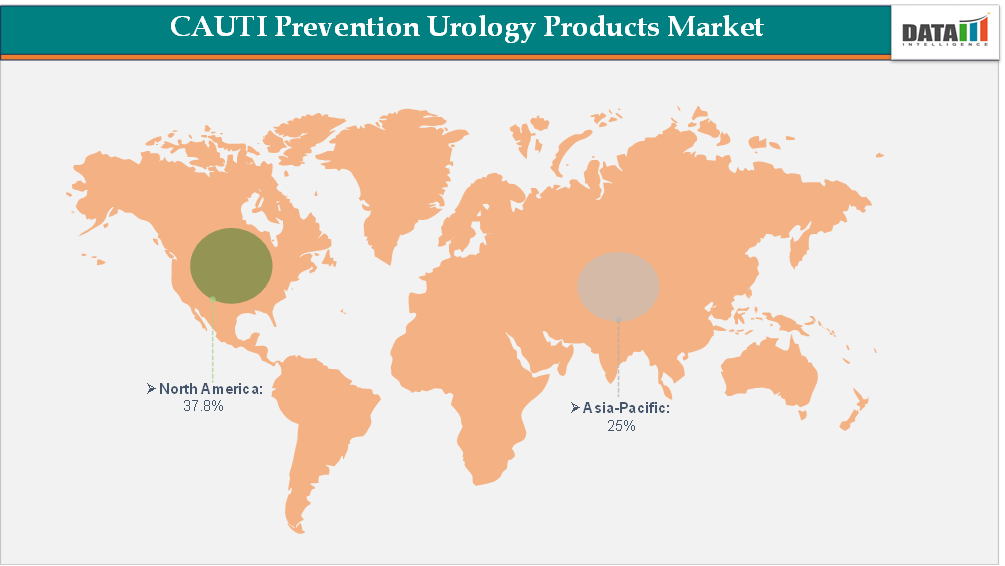

- North America is expected to take the lead in the Global CAUTI Prevention Urology Products Market commanding an estimated 35%-40% of the overall revenue share attributed to high catheter usage, stringent infection control regulations, and the rapid adoption of advanced technologies for preventing CAUTI.

- Strategically, the lower infection rates and compensation penalties of hospitals are including coated catheters, closed drainage systems, and standardized treatment kits into value-based CAUTI prevention bundles.

CAUTI Prevention Urology Products Market Size and Future Outlook

- 2025 Market Size: US$3.3 Billion

- 2033 Projected Market Size: US$5.9 Billion

- CAGR (2026–2033): 7.5%

- Dominating Market: North America

Fastest Growing Market: Asia-Pacific

Source : DataM Intelligence

For More Detailed information Request for Sample

Market Dynamics

Rising Healthcare Expenditure and Focus on Patient Safety

The healthcare systems in developed and emerging economies are experiencing growth in expenditures on infection prevention in line with maintaining effective control over the enormous clinical and economic burden of catheter, associated urinary tract infections (CAUTIs). CAUTIs are among the most common categories of hospital, acquired infections (HAIs) that can be avoided through adequate prevention measures, and they often lead to lengthier hospital stays, increased antibiotic consumption, greater rates of patient readmission, and serious complications such as bloodstream infections or sepsis, all of which together cause a marked drop in the overall cost of treatment.

Consequently, hospitals and healthcare organizations are redirecting their budgets from treatment towards prevention. It has become the main reason for the surge in an advanced range of CAUTI prevention urology products such as antimicrobial coated and hydrophilic catheters, closed urinary drainage systems, securement devices, and catheter care kits. Even though the acquisition cost of these medical products is high, they are able to contribute to cost reduction and improved patient outcomes and help in avoiding medico, legal cases by lowering infection incidences.

Besides, metrics related to patient safety and quality of care have become the focus of hospital accreditation, public reporting, and reimbursement systems. Poor CAUTI performance can lead to a drop in hospital ratings and financial losses, which in turn, will lead to more investments in evidence, based urology products that help infection control guidelines compliance. Consequently, increasing healthcare spending and at the same time, the emphasis on patient safety are still major factors that stimulate the growth of the CAUTI prevention urology products market.

Inconsistent Implementation of CAUTI Prevention Protocols

Although clinically endorsed CAUTI prevention protocols are readily available, there is wide variation in their take, up at healthcare institutions resulting from differences in the institutional policies, levels of staff training, and the availability of resources. Quite a few hospitals do not have set procedures for catheter insertion, maintenance, and removal, and compliance inspections are generally quite irregular. Consequently, the efficiency of CAUTI prevention urology products such as antimicrobial catheters, closed drainage systems, and catheter care kits is compromised when these products are not incorporated into a well, organized, protocol, driven system. Such inconsistency diminishes product value perception, decelerates the process of widespread adoption, and limits market penetration, especially in smaller hospitals and less resourceful environments.

Segmentation Analysis

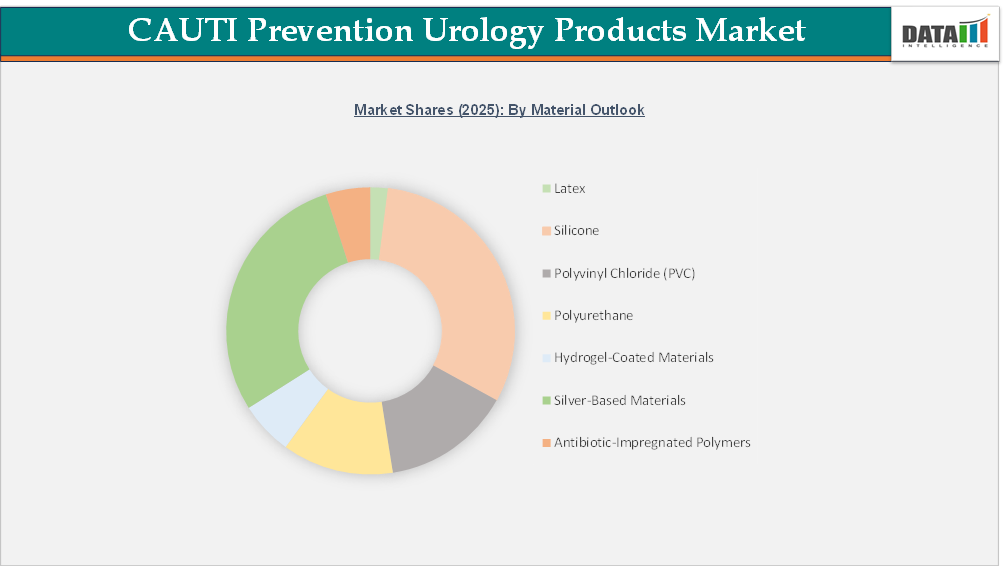

The global CAUTI prevention urology products market is segmented based on product outlook, application, end-user, material outlook, technology outlook, patient type and region.

Silver-Based Materials – CAUTI Prevention Urology Products Market

Clinical evidence indicates that silver-based materials of catheters have possible benefits in the reduction of the risk of infection, especially in terms of the decreased rate of bacteriuria and unspecified infection of the urinary tract. Clinical trials comparing silver-coated catheters have found no risk of urethral irritation or antimicrobial resistance and this reassures of its safety profile during clinical use. The mentioned advantages can be primarily linked to silver alloy formulations, which prove to be more efficient as antimicrobial agents than other silver formulations are.

Meta-analyses of randomized controlled trials suggest that the catheter materials made of silver alloy are useful in the prevention of the presence of asymptomatic bacteriuria, particularly when the catheter is used in short-term catheterizations (less than one week). It is also demonstrated that the findings hold with respect to various study designs and sources of data, which means that the results are robust. Experimental studies that have been carried out in special hospital environments also confirm the importance of silver-based materials in reducing the number of infections although the outcomes have been inconsistent in large hospitals.

On the whole, silver-based products, especially silver alloy technologies, are a clinically tested form of antimicrobial material in the CAUTI prevention market of urology products, which bears good results of reducing bacteria colonization when applied in the right times and length of stay.

Geographical Penetration

Largest Market:

Demand for CAUTI Prevention Urology Products Market in North America

The high incidence of CAUTIs in healthcare facilities and the high incidence of urinary catheter utilization are strong factors that drive the demand of CAUTI prevention urology products in North America. The U.S. Centers for Disease Control and Prevention (CDC) states that the probability of receiving an indwelling urinary catheter by the hospitalized patient is roughly between 15-25 %, which exposes a big number of patients to chances of infection. The CDC also indicates that approximately three quarters of urinary tract infection acquired in hospitals are related to urinary catheters, which makes CAUTIs one of the most frequent and preventable healthcare-associated infections in the area. CAUTIs are associated with long hospitalization, antibiotic overuse, higher readmissions, and severe complications including bloodstream infection and sepsis, which pose a significant clinical and financial strain on hospitals. As such, the infection prevention strategies, such as the use of advanced CAUTI prevention urology products, including the use of antimicrobial-coated catheters, closed urinary drainage systems, and the use of standardized catheter care solutions, are increasingly becoming priorities of the healthcare providers in North America in order to minimize the number of infections and enhance patient safety outcomes.

Market Outlook

In the U.S., the CAUTI prevention urology products market prognosis is facilitated by a significant clinical catheter-associated urinary tract infection rate and the use of continued infection control efforts. The Centers for Disease Control and Prevention (CDC) reports that between 12-16% of hospital inpatients will be having an indwelling catheter at some stage of their hospitalization, and every day that the catheter stays in the organism, the risk of developing CAUTI is raised by 3-7%. There are a high patient morbidity, extended hospitalization, and higher healthcare expenses and an estimated 13,000 annual deaths of patients associated with urinary tract infections linked to CAUTIs, indicating the significance of effective prevention strategies and products in the clinical setting. These statistics demonstrate the ongoing demands of sophisticated catheter material, antimicrobial coatings, and catheter management products, which minimize the risk of infection, which makes the prevention of CAUTI urology products a significant target market in the larger healthcare-associated infection prevention market in the U.S.

Canada CAUTI Prevention Urology Products Market Trends

In Canada, healthcare-associated infections (HAIs) and catheter-associated urinary tract infections (CAUTIs) are a considerable patient safety issue, which imposes major clinical and financial costs in acute-care hospitals. Data available on national surveillance of Hais provided by the Public Health Agency of Canada (PHAC) show that an average of 220,000 Canadian patients acquire an HAI in hospital annually, which explains why preventing device-associated infections like CAUTIs are very important. Although the separate CAUTI incidence rates on a national scale are not regularly released, the device related infections surveillance is conducted using the Canadian Nosocomial Infection Surveillance Program, which indicates the necessity of intensifying the surveillance and infection control measures in the Canadian healthcare facilities. Furthermore, 18.1% of the patients in the surveyed acute-care Canadian hospitals were found to be having an indwelling urinary catheter on the survey day, which highlights the high rate of catheter use that predisposes patients to the occurrence of CAUTIs and contributes to the demand of preventive urology products. These tendencies underline the continuing attention towards the decreased rate of CAUTI incidence due to the enhanced infection prevention measures and the use of products in the Canadian healthcare sector.

Fastest Growing Market:

Asia-Pacific Records the Fastest Growth in the CAUTI Prevention Urology Products Market

Due to more healthcare resources, greater inpatient volume and more hospitals focusing on preventing hospital-associated infections, the Asia-Pacific region has become a rapidly growing market for CAUTI prevention urology products. Hospitals and long-term care facilities throughout this region are becoming increasingly likely to utilize CAUTI techniques such as antimicrobial catheters, closed drainage systems and mechanical prevention methods to combat these types of infections. The prevalence of elderly persons, as well as chronic urological conditions, is leading to increased catheter usage by patients, and increasing pressure to create effective prevention techniques. A large-scale international surveillance study conducted in eight Asian countries found that the average CAUTI incidence was 3.08 per 1,000 urinary catheter days for hospitalized patients, especially in the intensive care unit in patients with urological conditions. The documented levels of CAUTI infection in addition to the high levels of device utilization and prolonged patient catheterization time support the emphasis on implementing preventive measures with urgency and as such propel the increased use of CAUTI prevention urology products within all health care systems in the Asia-Pacific Region.

India CAUTI Prevention Urology Products Market Insights

The impact of catheter-associated urinary tract infections (CAUTIs) as a category of hospital-acquired infections is significant within Indian hospitals, particularly within the intensive care department and tertiary care medical settings. CAUTIs in India have an approximate national incidence of 3.4 cases per 1,000 catheter days, which reflects the degree of infection observed in the majority of Indian hospitals. On the contrary, multiple studies conducted at tertiary care institutions demonstrate a much greater CAUTI incidence of 7-10 cases per 1,000 catheter days and indicate a CAUTI prevalence of 14-15% among patients with urinary catheters. Factors that contribute to the high CAUTI rates in Indian hospitals include prolonged catheter duration, increased patient load, and inconsistent adherence to infection control measures. The clinical and financial burden of CAUTI is significant because it extends the length of hospital stays, increases the use of antibiotics, and increases the likelihood of complications, and has created a demand for CAUTI prevention urology products such as antimicrobial-coated catheters, closed drainage systems and standardized catheter care solutions. Hospitals in India are placing additional emphasis on the importance of infection prevention and patient safety.

China CAUTI Prevention Urology Products Market Industry Growth

In China, catheter-associated urinary tract infections (CAUTIs) represent a huge burden on the healthcare system, creating a need for effective urology prevention products as well as monitoring of CAUTI's in tertiary hospitals’ intensive care units. While almost 90% of ICUs are routinely monitoring CAUTIs as a part of the state/region’s health care provider, less than 57.6% of these ICUs document CAUTI’s annually (i.e., they capture data of the annual CAUTI’s in their patient population); the median rate of the CAUTIs in patients that report was 0.86 per 1,000 patients. The CAUTI rates indicate an ongoing risk for CAUTI’s due to urinary catheter utilization, and the need for increased prevention methods. In conjunction with past data sources indicating that the CAUTI’s in ICUs from the Shanghai demonstrate an incidence density of 1.67 CAUTI’s per 1000 catheter-day’s, the CAUTI infection burden will continue to be an indication of the continued presence of device-associated infections in critically ill. The increased incidence of catheter utilization and increased focus on infection control provide an increase demand for advanced technologies for CAUTI prevention and urology products in this healthcare market.

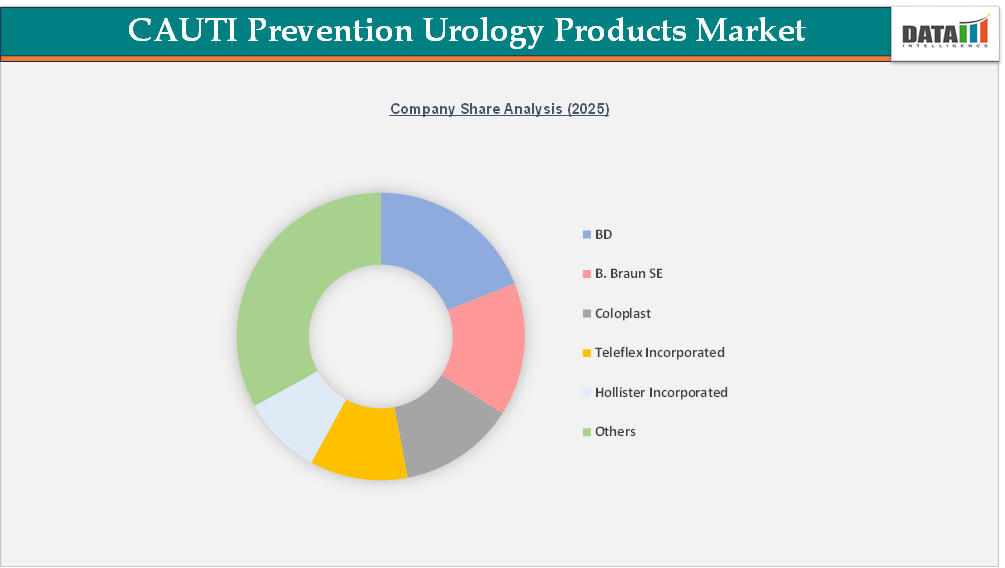

Competitive Landscape

The urology products market, which includes CAUTI prevention products, consists of many well-known global medical device manufacturers such as B. Braun SE, Teleflex Incorporated, Hollister Incorporated, Coloplast, and BD; in addition, many of these manufacturers have many other recognized manufacturers supporting them, such as ConvaTec Group PLC, Boston Scientific Corporation, Cardinal Health, Inc., Merit Medical Systems, Inc., and Medline Industries,LP. Overall, these companies offer a very broad range of urology products, including indwelling and intermittent urinary catheters; closed drainage systems; external urine management devices; and catheter care and maintenance solutions that are designed to help prevent infections and ensure that catheters are used safely.

The majority of manufacturers have focused their competitive efforts on improving the safety of patients, assisting with adherence to protocols related to the management of catheters, and decreasing the risk of infection by means of product design the selection of materials that would be used in manufacturing urology devices, and the use of systems that can assist with preventing infections. Most of the companies in this market have placed a large emphasis on having comprehensive urology portfolios and standard solutions that align with hospital infection control practices and clinical guidelines. Furthermore, these companies have been able to maintain a solid competitive position in acute care, long-term care, and home care through their strong manufacturing ability, their compliance with regulatory standards, and their established relationships with health care providers.

Key Developments

- In November 2025, BD (Becton, Dickinson and Company) released the PureWick™ Portable Collection System, the first ever, battery-operated, personal urine management device for wheelchair users, and mobility impaired individuals. Users, according to BD, will be able to manage urine incontinence, and be mobile at home and on the go. Urinary incontinence is said to affect 25 million Americans, and is associated with lower confidence and social participation. Its Portable Collection System is intended to provide greater independence to users. This is the latest addition to the expanding PureWick™ Urology line.

- In June 2025, Teleflex Incorporated published the results of a multinational cohort study involving over 6,670 patients from 12 ICUs across 8 countries (India, Malaysia, Papua New Guinea, Colombia, Egypt, and Turkey). Teleflex describes the study as showing that, of the Arrow® Chlorhexidine-Impregnated Central Venous Catheters (CVC), there are less cases of central line-associated bloodstream infections (CLABSIs) than of the standard non-impregnated CVCs, regardless of whether the CVCs are inserted and maintained according to established protocols. All in all, this study reinforces that the implementation of CVCs with antimicrobial and antiseptic functionalities is essential in the containment and prevention of infections in the critical care environment.

- In January 2025, Vizient, Inc. awarded Teleflex Incorporated its first contract for the Central Venous Access and Arterial Catheters, effective January 1, 2025. Under this contract, Vizient’s provider-customers, covering most U.S. acute care providers and academic medical centers, will gain access to Teleflex’s vascular access products at pre-set competitive prices and savings. This will enhance Teleflex’s penetration in U.S. hospitals and promote the adoption of its catheter technology.

What Sets This Global CAUTI Prevention Urology Products Market Intelligence Report Apart

- Latest Data & Forecasts – This report utilizes the latest market data combined with advanced forecasting to provide accurate market sizing, trend analysis, and growth forecasts. It crystallizes the current market state, while also forecasting demand, technology adoption, and investment in the CAUTI prevention urology products segment.

- Regulatory Intelligence – The report offers specific details regarding the regulations of CAUTI prevention urology medical devices, including the approval process, the details of the compliance, infection control, and reimbursement frameworks in the key regions. The report incorporates the regulations and guidance from the following bodies: U.S. FDA, EMA, MHRA, CDSCO, PMDA, NMPA, and Health Canada, which helps the manufacturers incorporate the development of the medical devices and the market strategies to the regional regulations.

- Competitive Benchmarking – The report also gives an overview of fast-growing and emerging markets, not just mature markets; how ready health care systems are to deal with catheters at different care levels; how much focus is being placed on CAUTI prevention; what types of procurement methods are being utilized; whether institutional purchasing occurs, and any regional cost issues. In addition, the report identifies some of the areas where there may be growth potential; operational challenges; and practical considerations regarding entering these markets in different countries.

- Geographic & Emerging Market Coverage – A complete geographic analysis of markets in North America, Europe, Asia- Pacific, Latin America, Middle East & Africa are presented in this report, with details on market dynamics by region; healthcare infrastructure; catheter utilization; and CAUTI prevention trends by region. Opportunities and hotspots have been identified which can be leveraged to help make educated decisions about entering the marketplace and to facilitate long-term growth in the region.

- Actionable Strategies & Cost Dynamics – The purpose of this report is to provide information that links the CAUTI prevention urology products market dynamics (e.g. device cost structures, hospital adoption economics, and trends in value-based purchasing) through the evaluation of product pricing strategies, opportunities for optimizing cost, and positioning of products related to infection reduction, achieving clinical outcomes, and hospital/long-term care facility purchasing priorities.