Broaching Tools Market Overview

The global broaching tools market reached US$ 0.49 billion in 2025 and is expected to reach US$ 0.79 billion by 2035, growing with a CAGR of 5.0% during the forecast period 2026-2035. Broaching remains a specialized precision-machining process because each tool must be engineered around part geometry, pull capacity, workpiece hardness, coolant conditions and cycle-time targets. A broach is therefore a productivity asset rather than a simple cutting consumable, especially when it controls splines, keyways, turbine slots, bearing profiles, ring gears and other repeatable internal or external features.

Asia-Pacific accounted for 45.5% of 2025 revenue and remains the largest as well as fastest-growing regional market. China, India, Japan, South Korea and ASEAN manufacturing clusters are expanding demand for precision tools used in automotive components, industrial machinery, bearings, rail equipment and electric vehicle assemblies. Broaching machines generated 42.8% of machine-type demand in 2025 because dedicated horizontal and vertical systems remain the preferred route for high-volume spline, keyway and slot production where repeatability matters more than flexible job-shop routing. Automotive and electric vehicles represented 31.7% of end-user demand in 2025 and are forecast to grow at 5.9% CAGR through 2035 as e-axle interfaces, steering systems, brake components, shafts and precision fit features offset the gradual decline of selected legacy transmission applications.

Lead time creates the strongest commercial pressure in custom broaching. Drawings often mature late in a production program while toolmakers still need time to select HSS or carbide grades, define coating requirements, validate chip evacuation and match the broach to the machine. Buyers are prioritizing suppliers that can support early drawing review, rapid quote iteration, documented reconditioning and local service. Material volatility around tungsten, cobalt and specialty steels also increases the importance of realistic quotation validity, repair economics and regional sourcing resilience.

Buyer attention is shifting toward cost per accepted feature, reconditioning turnaround, local sharpening capacity, machine compatibility, audit-ready documentation and proof that a premium broach can reduce scrap or downtime. Investment activity is concentrated in precision grinding, coating access, inspection capability, repair programs and application engineering rather than broad factory expansion. The most attractive suppliers will behave like process partners that protect launch schedules and production continuity.

Key Takeaways

- Asia-Pacific led the global broaching tools market with 45.5% share in 2025 and is also the fastest-growing region due to manufacturing scale across automotive, EV, bearing, industrial machinery and precision component clusters.

- Broaching machines remained the largest machine type with 42.8% share in 2025 as dedicated machines continue to outperform flexible alternatives in validated high-volume spline, keyway and slot use cases.

- Automotive and electric vehicles held 31.7% of market demand in 2025 and are forecast to grow at 5.9% CAGR during 2026-2035 as e-drive, steering, braking and shaft assemblies require stable mechanical engagement features.

- Supplier differentiation is moving from unit price toward lifecycle economics, including regrind planning, repair speed, drawing support, process validation and cost per accepted profile.

- Major competitive signals include investment in precision grinding capacity, coating access, documented tool history, local service networks and engineering support for aerospace, EV, defense and heavy equipment programs.

Broaching Tools Industry Trends and Strategic Insights

- Broaching suppliers are competing on process confidence, service depth and lifecycle economics. Buyers increasingly want evidence that a tool will protect part quality, reduce downtime and maintain form accuracy over long production runs.

- Commercial opportunity is strongest where the broach controls a feature that affects assembly, noise, fit, safety or inspection time. Premium suppliers should frame value around cost per accepted feature and documented process stability.

- U.S. customers emphasize resilience, traceability and local technical support. Japanese customers emphasize accuracy, supplier trust and long-term reconditioning discipline. Asia-Pacific volume buyers emphasize productivity, availability and local application support.

- EV demand is redirecting broaching rather than eliminating it. Demand is moving from selected legacy transmission components toward e-axle, ring gear, spline, shaft, braking and steering-related use cases that still require repeatable internal or external profiles.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 0.49 Billion | |

| 2035 Projected Market Size | US$ 0.79 Billion | |

| CAGR (2026-2035) | 5.0% | |

| Largest Market | Asia-Pacific, 45.5% share in 2025 | |

| Fastest Growing Market | Asia-Pacific | |

| Largest Machine Type | Broaching Machines, 42.8% share in 2025 | |

| Fastest Growing End-User | Automotive and Electric Vehicles, 31.7% share in 2025 and 5.9% CAGR during 2026-2035 | |

| By Tool Grade | High Speed Steel (HSS), Solid Carbide | |

| By Machine Type | Broaching Machines, CNC Turning Machines, Machining Center, Other | |

| By Workpiece Detail | P Steel, M Stainless Steel, K Cast Iron, N Non Ferrous Metals, H Hardened Materials | |

| By End-User | Automotive and Electric Vehicles, Aerospace and Defense, General Machining, Job Shops, Industrial Machinery, Construction and Agriculture Equipment, Energy and Power Generation, Oil and Gas, Rail, Marine and Shipbuilding, Bearing Manufacturing, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Why this report matters in 2026?

Broaching tools buyers enter 2026 with a practical challenge: production programs are becoming more precise while launch windows and sourcing tolerance are shrinking. EV platforms, aerospace engine programs, defense supply-chain localization and heavy equipment modernization are forcing manufacturers to validate tooling partners earlier in the design cycle. A delayed or poorly specified broach can stop a production cell, damage expensive parts or create dimensional drift that appears only after assembly or inspection.

The decisive change is not a single demand driver. Supply-chain resilience and input-cost volatility are turning tool sourcing into a production-risk decision. Tungsten, cobalt, HSS and specialty steel exposure, coating queues, skilled grinding labor and international shipping uncertainty make lead-time confidence as important as initial tool price. Buyers need visibility into which suppliers can support local regrinding, repair, fast engineering response, documented tool history, machine compatibility and substitute options before a critical profile goes out of tolerance.

Decision-makers also need a clearer view of where demand is moving. EV adoption reduces selected traditional transmission components but creates new requirements for e-drive interfaces, splines, shafts, braking systems and steering assemblies. Aerospace and defense programs require traceability, material control and high-confidence turbine or structural component machining. A report that connects these shifts with supplier capability, regional service depth and procurement economics can support better sourcing, partnership and investment decisions.

Strategic Indicators For Broaching Tools

High Regulation Impact

Broaching suppliers are increasingly affected by safety, quality and chemical-compliance expectations because tools are used for turbine slots, steering components, transmission parts, locking features and other high-consequence geometries. Aerospace, defense and premium automotive buyers increasingly request tool history, inspection records, reconditioning logs and controlled repair practices. European attention on process chemicals, worker exposure and hard-metal dust control is raising expectations for coolant management, grinding-dust handling, coating documentation and material declarations. Compliance is becoming part of supplier approval rather than a background requirement.

High Investment Activity

Investment is concentrated in precision grinding, reconditioning, inspection and specialized machine capability. FORST commissioned its newly developed USM universal grinding machine for tool manufacturing in 2024, a relevant signal because broach quality depends on long tool geometry, tooth progression, surface integrity and repeatable sharpening accuracy. EV and hybrid powertrain programs are redirecting investment toward e-axle components, ring gears, splines, precision profiles and hard-broached features. Aerospace and energy programs are also supporting engineering and metrology investments for turbine-disc broaching tools.

New Product Launches

Recent product activity is concentrated around servo-driven broaching machines, MQL-compatible broaches, advanced gear-cutting tools, precision grinding systems and hard-broaching capabilities. Suppliers are positioning around longer tool life, lower lubricant consumption, faster setup and tighter control of internal or external profiles.

NACHI has promoted servo-motor broaching machines and environmentally focused MQL broaches. LMT Tools continues to strengthen gear-cutting and precision tooling offerings for automotive, aerospace and energy machining. FORST’s USM grinding investment indicates continued focus on higher precision and faster tool-manufacturing capacity.

Supply Chain Disruption

Supply-chain disruption is visible in carbide blanks, specialty steels, PCD supply, coating queues, long custom grinding cycles and international logistics. A small delay in one input can delay the full tool because broach production depends on sequential operations. Tooling cost is small compared with a stopped cell. Buyers are therefore willing to pay for resilient supply where the feature is critical. Suppliers with regional warehouses, local regrind partners and transparent lead-time systems can convert disruption into a competitive advantage.

Pricing Volatility

Broaching prices are more exposed to engineering hours and lead time than many catalogue milling or drilling tools. Profile complexity, tooth rise, workpiece hardness, material selection, coating requirements, inspection effort and machine setup support can change the final cost materially.

Raw material volatility still matters because tungsten carbide, cobalt-based hard-metal systems and specialty steels are used in demanding broach designs and repair programs. Procurement teams should compare new tool design, grinding hours, inspection, coating, tryout, regrind and emergency remake premiums separately instead of benchmarking only purchase price.

Procurement Pressure

Procurement teams face pressure to reduce tooling spend while production teams need fewer stoppages and better part stability. A shared cost-per-accepted-feature model helps reduce the gap between purchase price and production economics. Vendor rationalization is also increasing. Large plants want fewer suppliers but deeper technical coverage, including drawing review, local repair, coating access, machine compatibility knowledge, service records and fast escalation during launch.

New Technology Adoption

Technology adoption in broaching is practical rather than platform-led. Digital tool configuration, AI-assisted quotation, process simulation, tool vending, connected inventory, automated inspection feedback and predictive regrind planning are gaining relevance where they reduce errors, stockouts or downtime.

Suppliers should present technology through plant-level outcomes. Customers respond when technology shortens launch time, improves quotation accuracy, reduces scrap or makes service planning easier.

Regional Expansion Opportunity

- Regional expansion should focus on customer clusters rather than broad country entry. Demand appears near automotive, aerospace, medical, electronics, machinery, rail and heavy equipment supply chains.

- India, Mexico, Vietnam, Thailand and Eastern Europe are attractive for localized service because manufacturing is expanding and buyers need technical support close to plants. Japan, Germany and the U.S. remain premium markets where trust and documentation can support pricing.

Government Policy Support

Policy support reaches broaching through defense, aerospace, rail, energy and localized automotive manufacturing. U.S. defense industrial base programs, European resilience initiatives, India’s manufacturing incentives and Japan’s precision machinery support all create second-order demand for reliable tooling.

Critical mineral policy also matters because carbide and wear-resistant materials depend on tungsten and related inputs. Suppliers using recycled carbide programs and raw-material traceability can strengthen positioning in aerospace, defense and premium industrial accounts.

Import, Export, and Pricing Intelligence

Trade flows under HS 820760 remain useful for validating broaching and boring tool movements, although the code should be used with product-level checks because it can include adjacent precision tooling categories. Pricing intelligence should separate commodity tooling from custom broaches, hard-broaching tools, turbine-disc tools and repair-heavy programs.

| HS Code | Reporter | Trade Flow | 2025 Trade Value | Interpretation |

| 820760 | Germany | Exports | USD 135.45 Million | Germany remained the largest global exporter of precision broaching and boring tools, reflecting strong automotive and aerospace tooling demand. |

| 820760 | European Union | Exports | USD 112.44 Million | The EU maintained technological dominance in high-precision cutting and broaching tool manufacturing ecosystems. |

| 820760 | United States | Exports | USD 86.84 Million | Strong exports indicate advanced domestic machining capability and demand from defense and industrial sectors. |

| 820760 | Japan | Exports | USD 48.15 Million | Japan continued supplying ultra-precision broaching tools for electronics and automotive production lines. |

| 820760 | China | Exports | USD 36.01 Million | China exported high-volume industrial broaching tools at competitive pricing across emerging manufacturing economies. |

Company Coverage Preview

NACHI-FUJIKOSHI is a key manufacturer because it connects cutting tools, gear tools, bearings, robots, hydraulic equipment, machine tools and specialty steel. The company’s integrated manufacturing identity gives it credibility with automotive, bearing and machinery customers. NACHI acts as a broader production-technology partner rather than a narrow tool supplier, which supports its positioning in splines, keyways and drivetrain-related features where process confidence is critical.

AI Impact Analysis

AI impact in precision tooling is most useful when it supports engineering judgement rather than replacing it. Tool drawings, workpiece material, machine type, coolant condition and past failure records can be converted into better recommendations. A supplier with structured application history can respond faster than a supplier relying only on informal engineer memory.

Tool wear, regrind frequency, coating life and customer rejection records can be analyzed to detect patterns before a production stoppage. Analytics are valuable because many tooling failures show early signals through burr formation, surface change, noise variation or dimensional drift. Commercial teams can also use AI to improve proposal quality through similar-part search, quote templates, regional lead-time risk and cost-per-part models.

Disruption Analysis

Disruption is not arriving as one single technology that replaces conventional broaching tools. Change is coming through process integration, digital ordering, tighter quality gates, sustainability expectations and localized supply-chain strategies. Buyers want fewer surprises at launch and more proof before committing to a supplier.

Tool suppliers are moving closer to machine builders, CAM providers, inspection companies and distributors with inventory visibility. A tool sale is becoming part of a broader process package. Suppliers unable to support trials, regrind planning or technical documentation risk being pushed into low-margin catalogue orders.

Another disruption is the shift from price-based procurement to production-risk procurement. Customers increasingly ask who can keep the cell running, who can provide urgent support and who can explain the economics of a premium tool. Such questions favor technically capable suppliers even when the initial quote is higher.

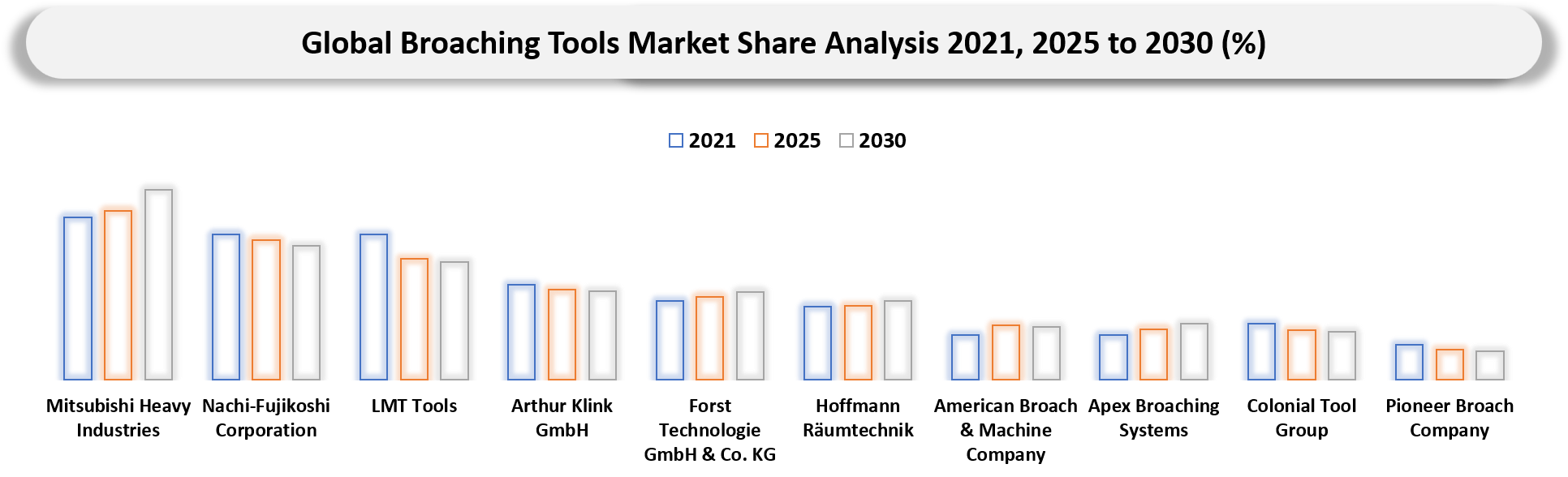

BCG Matrix: Company Evaluation

STAR

Star players include NACHI-FUJIKOSHI, Mitsubishi Heavy Industries Machine Tool, The Ohio Broach and Machine Company, Forst Technologie, Miller Broach and Hassay Savage because they combine broach design, precision grinding, material knowledge and repair capability. Customer trust is built through years of form accuracy and reliable sharpening rather than broad catalogue visibility.

POTENTIAL

Potential players include Pioneer Broach, Colonial Tool, V W Broaching Service, regional tool rooms and specialist carbide broach developers serving aerospace, defense, rail and EV component clusters. Smaller suppliers can win where local engineering access, emergency repair and quick sharpening matter more than global brand scale.

Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

Automotive and EV component programs increase precision-profile demand | 5.4% | Asia-Pacific, North America, Europe | Spline, shaft, ring gear, steering, braking and e-axle use cases | Supports stable demand as EV platforms redirect tooling needs rather than eliminate broaching. |

Aerospace and defense machining requires high-confidence broaching | 4.8% | U.S., Germany, Japan, UK and France | Turbine slots, actuation parts, structural locking features and hard-metal profiles | Raises demand for documented process control, repair discipline and traceable tool histories. |

Automation increases the value of repeatable dedicated processes | 4.5% | High-volume manufacturing plants globally | Automated cells, transfer lines and high-throughput profile machining | Improves economics for dedicated broaching where cycle time and inspection stability are critical. |

Localized manufacturing and reshoring strengthen service-led supplier selection | 4.1% | U.S., Mexico, India, Eastern Europe and Southeast Asia | Local regrinding, emergency remake, machine support and launch assistance | Rewards suppliers with nearby engineering and repair capability. |

Spline and Keyway Repeatability Keeps Broaching in Production Lines

Mechanical assemblies still rely on splines, keyways and internal forms that need repeatable geometry. Broaching can create those profiles quickly when volume and design are right. A dedicated broach can remove multiple milling passes and reduce inspection variation. Automated lines increase the value of predictable features because parts must fit without hand correction.

EVs are changing but not eliminating broached features. Steering systems, shafts, brake components and e-drive interfaces still need mechanical engagement. Suppliers should map component-level demand rather than assume all transmission-related broaching declines. Customers want evidence around cycle time, form accuracy, tool life and sharpening cost before committing to a dedicated tool.

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

Custom broach cost can push low-volume work toward flexible machining | 4.3% | Prototype and low-volume programs | Milling, shaping, slotting and wire EDM alternatives | Delays purchase approval until volume and design stability are clear. |

Raw material and coating cost volatility raises quotation risk | 3.9% | Carbide, HSS, cobalt and tungsten-exposed supply chains | Hard broaching, turbine-disc tools and high-wear repair programs | Shortens quote validity and increases focus on staged payments or escalation clauses. |

Skilled grinding and application-engineering shortages limit service speed | 3.6% | Custom toolmakers and regional repair providers | Regrind planning, tool repair and emergency remake | Creates lead-time pressure and favors suppliers with trained tool-room capacity. |

Alternative processes reduce broaching dependence in mixed-product plants | 3.4% | Job shops and plants with uncertain annual volumes | CNC machining-center broaching, EDM, shaping and skiving | Requires clearer cost-per-feature justification for dedicated tools. |

Custom Broach Cost and Program Uncertainty

Custom broaches require long tool bodies, exact tooth progression and careful material choice. Engineering cost can be difficult to justify for prototypes or low-volume parts. Milling, shaping, slotting or wire EDM can look safer when annual volume is limited. Program uncertainty increases the restraint because a dedicated broach may become obsolete before payback if the customer expects design revisions.

Capital intensity also matters. Dedicated broaching machines, fixtures and handling systems create a larger commitment than using an existing machining center. Suppliers can respond with modular thinking, phased tooling plans and clear cost-per-profile comparisons. Broaching wins when the economic case is visible and when the buyer understands the cost of slower alternative processes.

Segment Analysis

The global broaching tools market is segmented based on tool grade, machine type, workpiece detail, end-user and region.

Broaching Machines Remain the Leading Machine-Type

Broaching machines accounted for 42.8% of machine-type demand in 2025 because validated production programs still prefer dedicated equipment for repeated internal and external profile use cases. Horizontal machines are used widely for long internal profiles and high-force operations, while vertical machines support compact layouts and specific production-cell designs. Dedicated machines allow stable pull force, repeatable alignment and consistent chip evacuation when the tool and fixture are correctly specified.

Internal Broaches Remain Critical for Spline, Keyway and Fit-Feature Use Cases

Internal broaches create the features that let shafts, gears and couplings transmit torque or position parts accurately. Automotive, rail, industrial machinery and bearing plants rely on those use cases when assembly repeatability matters. HSS remains important because long tooth trains need toughness and reliable regrindability. Carbide can be attractive in abrasive or high-volume applications but requires careful process control.

Surface Broaches Protect Throughput in Repeat Profile Use Cases

Surface broaches are used where a flat, slot, contour or external profile needs consistent geometry at speed. High-volume production can justify a dedicated broach because each pass completes a feature that milling may produce through several operations. Tool design must match workpiece support and chip flow. Poor fixturing can create chatter or uneven wear, which makes coordination between the toolmaker, fixture designer and production engineer essential.

Automotive and Electric Vehicles Lead End-User Growth

Automotive and electric vehicles held 31.7% share in 2025 and are expected to grow at 5.9% CAGR during 2026-2035. Traditional transmission content is changing but EV platforms still require stable mechanical engagement use cases across e-axle components, shafts, brake systems, steering assemblies and precision housings. Suppliers with application review capability can defend relevance by proving cycle-time savings, inspection stability and tool-life economics.

Geographical Penetration

U.S. Broaching Tools Market Landscape

The U.S. market is supported by defense, aerospace, medical devices, semiconductor equipment, heavy machinery and reshoring programs. Customers often value documentation, local support and production continuity because downtime on a critical feature can affect expensive assemblies and qualified production lines. Tariff and shipping risk have made local inventory, quick servicing, and domestic repair partners more important in supplier selection.

Regional distributors, regrind partners, and technical specialists increasingly influence final buying decisions. Global brands remain important but buyers also ask whether the supplier can visit the plant, inspect machine condition, support trials and provide emergency remake options.

Japan Broaching Tools Market Outlook

Japan should be treated separately because buyer behavior is different from pure volume markets. Precision machinery, automotive suppliers, bearings, robotics and machine tool builders reward consistency, long-term support and trusted engineering relationships. Japanese customers are demanding on service quality and expect repeatability across design review, trial, delivery and reconditioning. Low price alone rarely wins if it increases uncertainty inside a precision production environment.

Asia-Pacific Broaching Tools Market Trends

Asia-Pacific held 45.5% share in 2025 and remains the most important regional opportunity because demand is spread across automotive, electronics, industrial machinery, construction machinery, shipbuilding and precision components. China provides volume and low-cost options, India is building demand through mobility, defense and machine tools, Japan emphasizes accuracy and supplier discipline, South Korea links tooling demand to EVs, shipbuilding and electronics, and Southeast Asia creates opportunities through contract manufacturing.

A broad Asia-Pacific strategy is not enough. Tooling for a Japanese precision-reducer plant is sold differently from tooling for an Indian workshop or a Vietnamese contract manufacturing facility. Demand must be analyzed by machine category, material class, buyer vertical and local service expectations.

Competitive Landscape

- Competition is fragmented at product level but more concentrated for global accounts and technically demanding applications. Large suppliers win where they offer breadth, application engineers, coatings, digital infrastructure and cross-regional support.

- Specialist suppliers win where they solve difficult features faster or provide local service that large companies cannot match. Emergency repair, quick sharpening and strong drawing interpretation can outweigh brand scale in customer clusters.

- Distributor influence remains strong for standard tools. Direct manufacturer relationships become more important for custom tools, high-value production programs and sensitive materials. Strong go-to-market models combine digital availability with expert field support.

Competitive benchmarking should track custom quote speed, local regrind capability, coating access, drawing support, machine compatibility knowledge, inventory transparency and ability to provide trial evidence.

MAJOR PAIN POINTS

- Gap between tool selection and production performance when procurement compares price while production carries the cost of scrap and downtime.

- Long lead times for custom geometry, coating, inspection and precision grinding when customer drawings change late in the program.

- Weak visibility into replacement timing because many plants service high-value broaches only after part quality begins drifting.

- Shortage of skilled grinding labor and application engineers capable of diagnosing pull force, lubrication, alignment and machine-condition issues.

- Raw material and coating cost volatility that makes quotation validity difficult for large custom tools.

- Limited local repair and reconditioning options in fast-growing manufacturing clusters.

- Difficulty comparing dedicated broaching against CNC, EDM or shaping alternatives without a cost-per-feature model.

High consequence of broach breakage because damage can extend to parts, fixtures and machines.

RECENT DEVELOPMENTS

- April 2025: LMT Tools expanded gear-cutting expertise through additional manufacturing capabilities, advanced tooling innovations and integrated PWS technical knowledge globally.

- March 2025: NACHI-FUJIKOSHI Corporation highlighted servo-motor broaching machines enabling stable high-speed machining, automated setup changes, energy savings and compact manufacturing operations.

- February 2025: LMT Tools strengthened precision tooling offerings for automotive, aerospace and energy machining through expanded advanced-tool development capabilities worldwide.

- January 2025: NACHI-FUJIKOSHI Corporation promoted environmentally focused MQL broaches delivering longer tool life, reduced industrial waste generation and improved machining efficiency.

2024: FORST Technologie commissioned its newly developed USM universal grinding machine for tool manufacturing to expand production capacity and improve precision grinding capability.

KEY PROCUREMENT PRIORITIES AND BUYER EVALUATION CRITERIA

- Buyers are evaluating suppliers on drawing-review capability, machine compatibility knowledge, expected tool life, regrind economics, local service response and proof of process stability.

- Automotive and EV manufacturers prioritize cycle time, form accuracy, launch support, stable supply and tooling economics for spline, shaft, braking, steering and e-drive use cases.

- Aerospace and defense buyers prioritize traceability, documentation, process control, inspection records and repair discipline because tool failure can affect safety-critical or high-value components.

- Procurement teams increasingly require a cost-per-accepted-feature view that separates new tool cost, grinding hours, coating, inspection, tryout, repair, regrind and emergency remake premiums.

Preferred suppliers are those that can support both engineering and procurement conversations, converting price discussions into production-risk and lifecycle-value decisions.

ANALYST VIEW / OPINION

- DataM expects the strongest suppliers to behave like process partners rather than tool sellers. Customers are paying for confidence that a part feature will remain stable at production speed.

- Regional service depth will become a stronger differentiator as tariffs, shipping uncertainty and shorter product launches make local sharpening, repair and application support commercially important.

- Market winners will combine technical evidence, digital customer convenience and lifecycle economics. Suppliers that can prove cost per accepted feature and maintain service records will have a stronger argument with both engineering and procurement teams.

- Asia-Pacific should remain the volume center, while Japan, Germany and the U.S. will remain premium markets for high-confidence tools and documented reconditioning programs.

- EV demand should be evaluated By Tool Grade-level use cases rather than broad drivetrain assumptions because some legacy features decline while new precision engagement features scale.

TARGET AUDIENCE

| INDUSTRY | WHO SHOULD BUY THIS REPORT? | REASON TO BUY THIS REPORT |

| Automotive & EV Manufacturers | Transmission Manufacturing Teams, Powertrain Engineers, Production Heads | Analyze broaching tool demand for gears, splines, keyways and EV drivetrain components. |

| Aerospace & Defense Companies | Precision Machining Engineers, Tooling Specialists, Aerospace Manufacturing Teams | Evaluate high-precision broaching solutions for turbine discs, aerospace alloys and structural components. |

| Industrial Machinery Manufacturers | Plant Operations Managers, CNC Broaching Engineers, Manufacturing Departments | Optimize broaching productivity, tooling efficiency and high-volume component machining operations. |

| General Engineering & Metal Fabrication Companies | Workshop Supervisors, Fabrication Managers, Process Engineering Teams | Identify durable broaching tools for internal profiles, slots and precision metal cutting applications. |

| CNC Machine Tool Manufacturers | Product Development Teams, Automation Engineers, Strategic Alliance Teams | Understand demand trends for CNC broaching systems and automated machining integration. |

| Oil & Gas Equipment Manufacturers | Heavy Machining Teams, Reliability Engineers, Procurement Managers | Evaluate wear-resistant broaching tools for valves, pumps and drilling equipment manufacturing. |

| Energy & Power Generation Companies | Turbine Component Teams, Plant Engineering Departments, Sourcing Managers | Assess broaching tool requirements for turbine discs, generator shafts and precision power equipment. |

| Construction & Mining Equipment Manufacturers | Heavy Equipment Production Teams, Manufacturing Operations Managers | Analyze heavy-duty broaching solutions for large-scale and high-strength material machining. |

| Railway Equipment Manufacturers | Rail Component Manufacturing Teams, Operations Engineers, Procurement Departments | Understand tooling demand for couplings, brake systems and railway drivetrain component manufacturing. |

| Tooling Manufacturers & Broach Producers | Product Innovation Teams, Competitive Intelligence Departments, Strategy Managers | Benchmark broaching technologies, tool materials, coatings and competitive market positioning strategies. |

WHY CHOOSE DATAM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

WHAT DATAM UNIQUELY PROVIDES

- Client-ready views that connect tooling demand with part programs, machine type, workpiece material, region, trade flows and supplier capability.

- Bottom-up market modeling using customer interviews, distributor checks, HS trade codes, machine installation patterns, tool grade mapping and end-equipment analysis.

- Supplier scorecards covering quote speed, regrind capability, coating access, machine compatibility knowledge, service depth and lifecycle support.

- Procurement intelligence covering cost-per-feature economics, pricing trackers, sourcing risk, lead-time benchmarks and reconditioning models.

- Regional opportunity mapping for automotive, EV, aerospace, defense, rail, machinery, heavy equipment and job-shop demand clusters.

- Application-fit matrices that help clients compare dedicated broaching against CNC alternatives, EDM, shaping or skiving on economic and operational grounds.

- Risk-mitigation roadmaps covering raw material exposure, coating queues, local repair capacity and backup supplier options.