Blood Clot Retrieval Device Market Overview

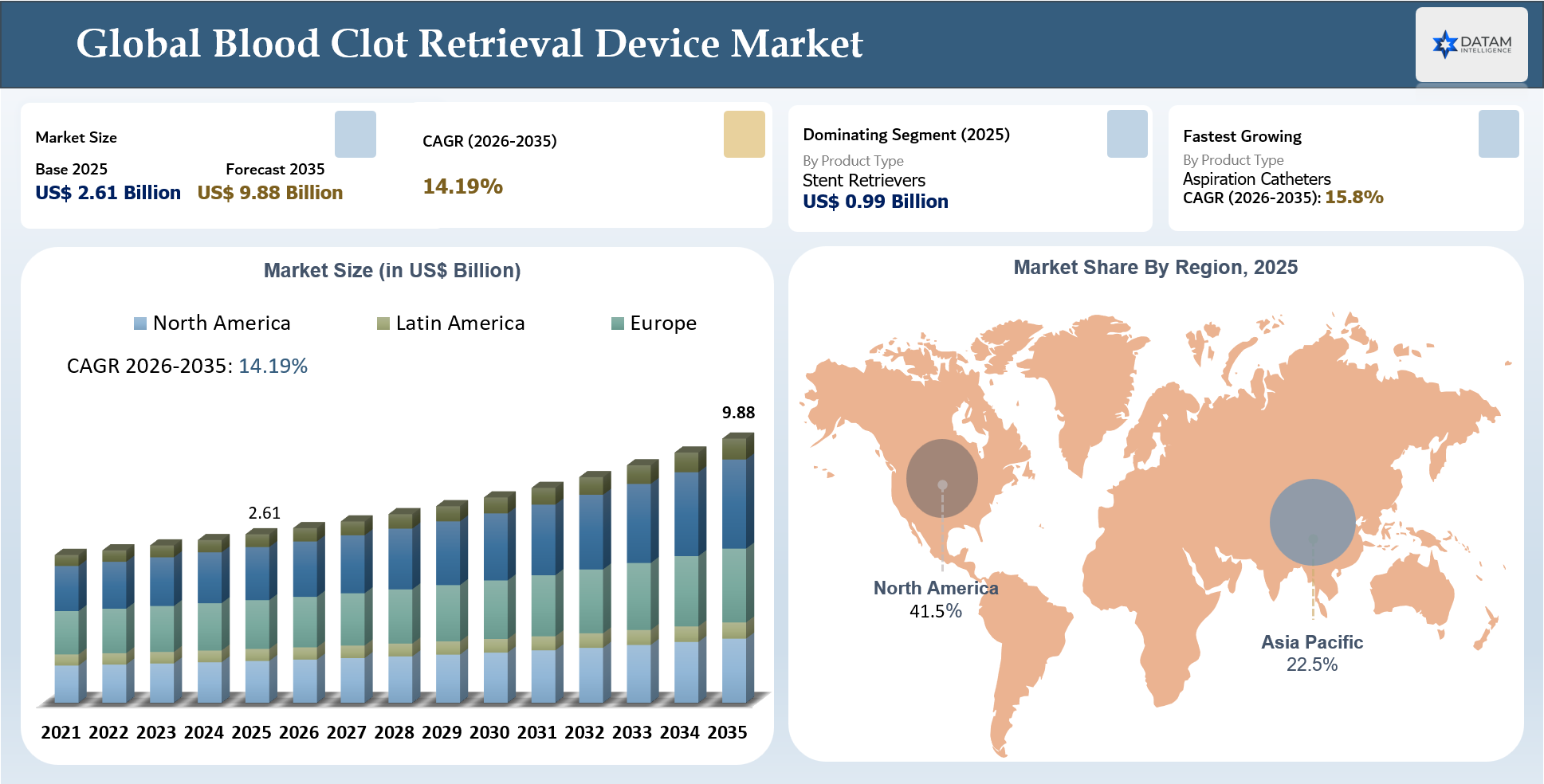

The Global Blood Clot Retrieval Device Market stood at US$ 2.61 billion in 2025 and is expected to reach US$ 9.88 billion by 2035, growing with a CAGR of 14.19% during the forecast period 2026-2035.

The Global Blood Clot Retrieval Device Market is evolving from individual thrombectomy devices into holistic, outcome-oriented clot retrieval platforms. The major trend in this market involves the growing use of aspiration-first, large-bore catheter, and combined mechanical thrombectomy treatment strategies that slowly but surely are replacing the traditional approach using stent retriever devices. Hospitals and intervention facilities have started to consider thrombectomy devices based on their success rate at first attempt, faster reperfusion, navigability within vessels, clot capture efficacy, reduced complications, and overall compatibility with complete endovascular procedures.

As a result, there has been a growing demand for cutting-edge aspiration catheters, stent retrievers, guide catheters, microcatheters, access systems, and thrombectomy devices as part of an overall clot retrieval system. The shift involves the increased interest in reliable thrombectomy solutions that fit in well within a hospital facility's workflow process, have a user-friendly design and functionality, and bring real value to stroke and vascular intervention centers. As stroke centers and cath labs continue to open up across the globe, the companies with clinically proven solutions, strong hospital presence, good reimbursement capabilities, and a comprehensive range of thrombectomy solutions will find themselves in a favorable position.

Key Takeaways

- The global blood clot retrieval device market was valued at US$2.61 billion in 2025 and is projected to reach US$9.88 billion by 2035.

- The market is expected to grow at a CAGR of 14.19% during the forecast period 2026-2035.

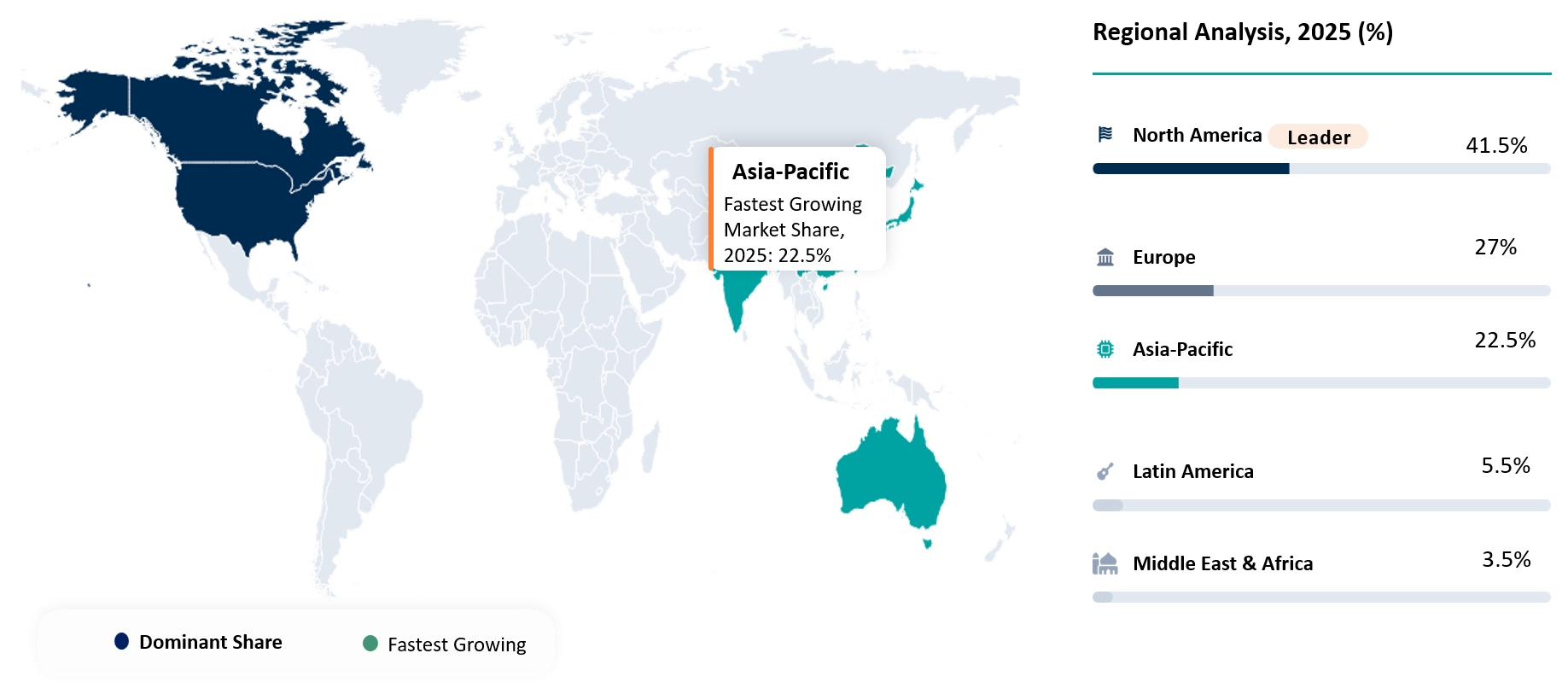

- North America held the highest market share at 41.5% in 2025, supported by advanced stroke care infrastructure, strong thrombectomy adoption, and favorable reimbursement.

- Asia-Pacific is expected to be the fastest-growing region, driven by rising stroke burden, expanding neurointerventional capacity, improving healthcare access, and growing investment in endovascular care.

- Stent retrievers were the largest product type segment in 2025, valued at approximately US$1.00 billion, supported by strong use in acute ischemic stroke thrombectomy.

- Aspiration catheters are projected to be the fastest-growing product type, expanding at an estimated 15.8% CAGR during 2026–2035.

- North America shows the highest investment activity, led by stroke-center expansion, thrombectomy-ready hospitals, AI-enabled stroke triage, and advanced aspiration-based intervention platforms.

- North America also has the largest end-user base across hospitals, stroke centers, specialty cardiovascular centers, and vascular surgery centers.

- The market has a strong competitive concentration, with major players including Medtronic, Stryker, Penumbra, Inc., Johnson & Johnson MedTech, and Terumo Neuro.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 2.61 Billion | |

| 2035 Projected Market Size | US$ 9.88 Billion | |

| CAGR (2026-2035) | 14.19% | |

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Product Type | Stent Retrievers, Aspiration Catheters, Combined Retrieval Systems, and Access and Support Devices | |

| By Retrieval Technique | Stent Retriever-Based Thrombectomy, Direct Aspiration Thrombectomy, Combined Mechanical Thrombectomy, Rescue Thrombectomy, and Others | |

| By Application / Use Case | Acute Ischemic Stroke, Pulmonary Embolism, Peripheral Arterial Thrombosis, Deep Vein Thrombosis, Dialysis Access Thrombosis, and Others | |

| By Vessel Location | Cerebral Arteries, Pulmonary Arteries, Peripheral Arteries, Peripheral Veins, and Dialysis Access Vessels | |

| By Vessel Compatibility | Small Vessel Devices, Medium Vessel Devices, and Large Vessel Devices | |

| By Usage Type | Single-Use Devices and Reusable Support Systems | |

| By End User | Hospitals, Stroke Centers, Specialty Cardiovascular Centers, Vascular Surgery Centers, Ambulatory Surgical Centers, and Others | |

| By Procurement Channel | Direct Hospital Procurement, Distributor-Based Sales, Group Purchasing Organizations, and Government and Public Hospital Tenders | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

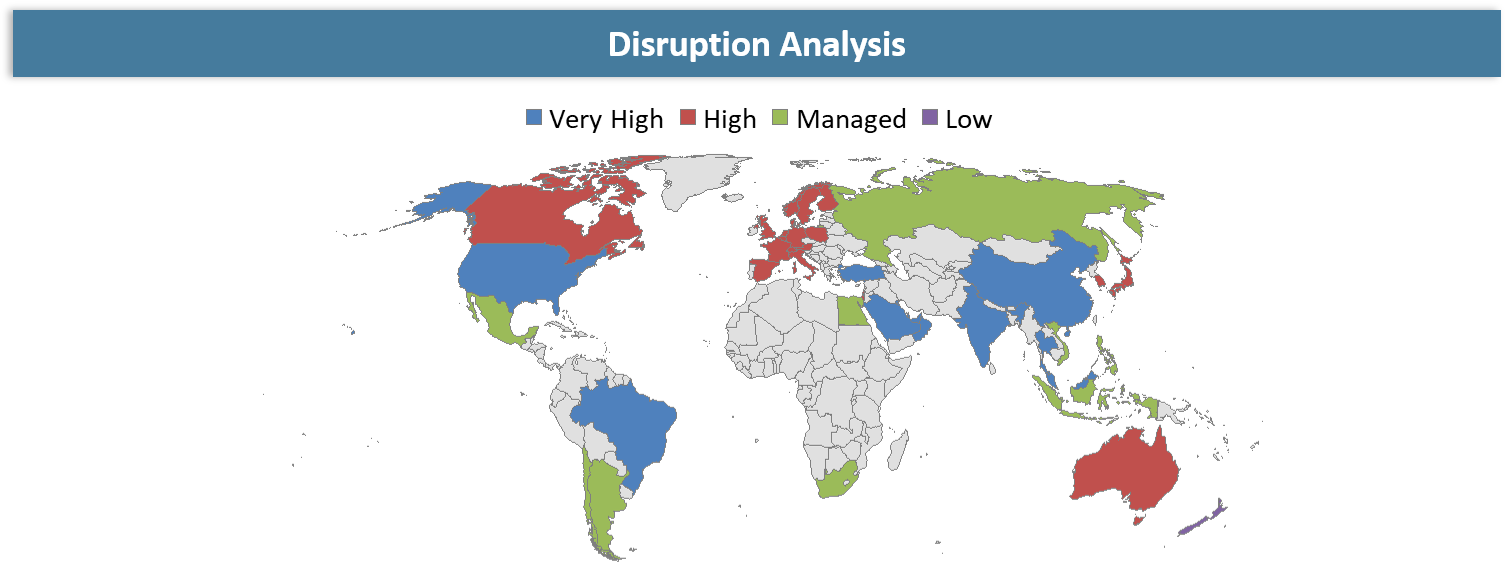

Disruption Analysis

Aspiration-Led Thrombectomy and AI-Enabled Workflows Are Disrupting Clot Retrieval Competition

The current global blood clot retrieval device market will be disrupted by the transition from the traditional stent retriever thrombectomy approach to aspiration first and large bore catheter thrombectomy or a combination of mechanical thrombectomy. The focus in hospitals for procedures will include faster reperfusion, higher first-pass success rates, decreased complication rates, and improved ability to navigate complex anatomy during vascular intervention. This development will compel blood clot retrieval device makers to design innovative aspiration catheters, distal access devices, mini stent retrievers, and integrated retrieval systems for the management of ischemic stroke, pulmonary embolism, peripheral arterial thrombosis, deep vein thrombosis (DVT), and dialysis access thrombosis.

Other upcoming disruptions in the market are expected in the area of AI-powered stroke triage, improved imaging workflows, and increased number of thrombectomy capable centers. The AI technology in imaging applications is helping healthcare providers identify suitable patients promptly and reduce delays in patient referrals between primary and comprehensive stroke centers. In an outcome driven procurement environment, medical device firms are not focusing just on product availability but also clinical proof of value, workflow optimization, physician ease of use, reimbursement, and total procedure benefit.

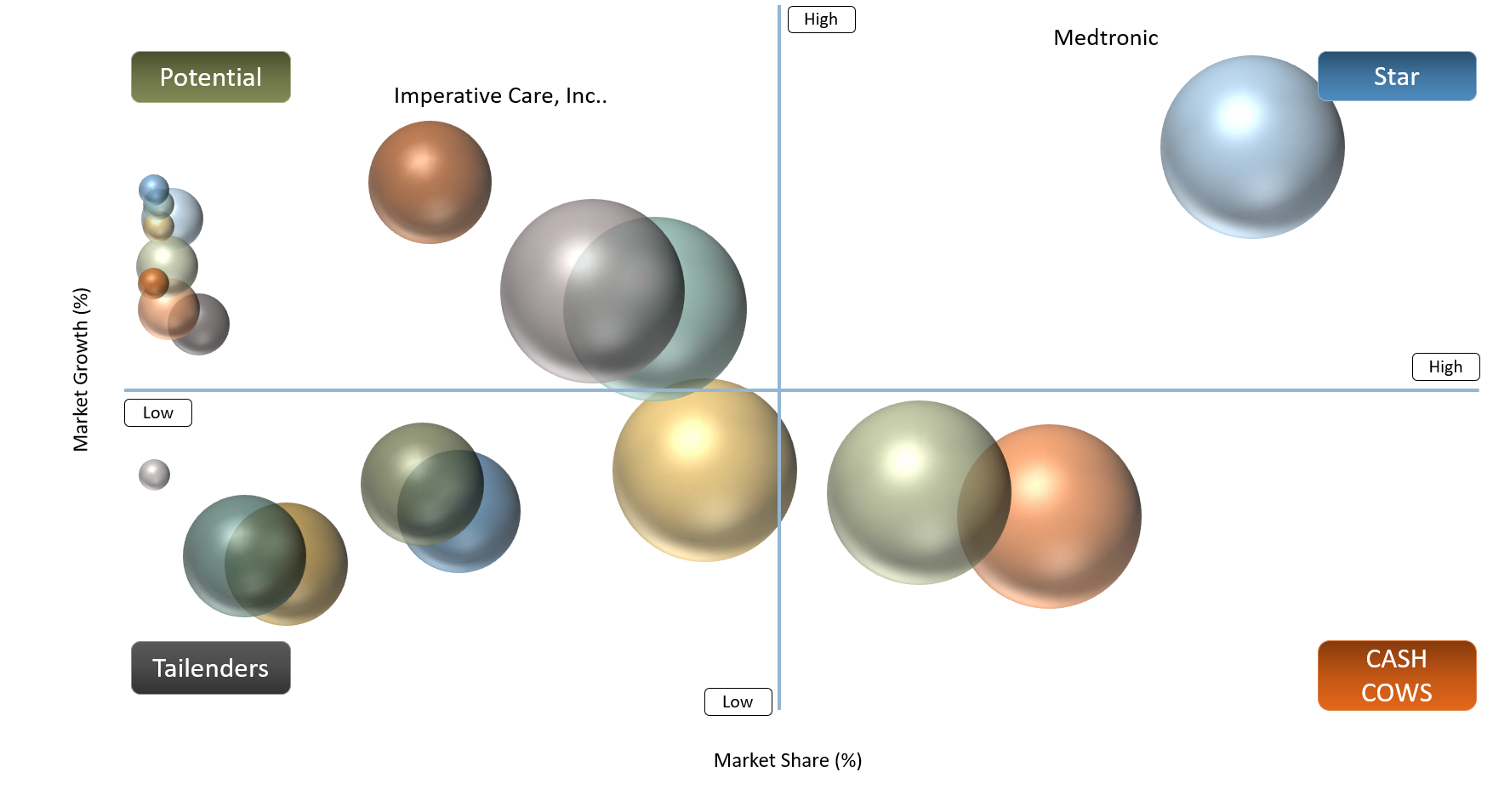

BCG Matrix: Company Evaluation

As for the BCG matrix, Stars of the Global Blood Clot Retrieval Device Market are companies with significant global influence, a comprehensive thrombectomy portfolio, physician endorsement, and a defined position in neurovascular, peripheral vascular, pulmonary embolism, and venous clot retrieval procedures. Medtronic, Stryker, Penumbra, Inc., Johnson & Johnson MedTech, Terumo Neuro, Boston Scientific Corporation, and Becton, Dickinson and Company are considered Stars due to their brand value, advanced thrombectomy technologies, hospital relationships, and ability to facilitate high-volume thrombectomy workflows.

Cash Cows are companies with established vascular intervention portfolios, hospital repeat purchasing, and product significance within the domain of clot management and endovascular procedures. AngioDynamics, Inc., Koninklijke Philips N.V., Balt Group, phenox, and ACANDIS GmbH can be referred to as Cash Cows due to the stable market position secured via dedicated thrombectomy systems, neurovascular interventions, and vascular access solutions that cater to procedure-related demands.

Question Marks are those companies with significant thrombectomy innovations but limited global scope or product relevance in specific regions. Imperative Care, Inc., Rapid Medical, and Vesalio Inc. are designated as Question Marks due to their unique products such as aspiration system, active clot retrieval systems, and neurovascular thrombectomy. Further development would largely depend upon the future clinical success, geographic scope, and commercialization within hospitals.

Market Dynamics

Rising Stroke and Thromboembolic Burden Is Expanding the Addressable Pool for Emergency Clot Retrieval

The increasing prevalence of strokes and other thrombotic disorders is resulting in an expansion of the patient population eligible for the use of emergency clot removal tools. According to the World Stroke Organization's Global Stroke Fact Sheet 2025, there are currently 11.95 million new strokes occurring each year, and one out of every four adults above 25 years of age will suffer from strokes over their lifetimes. Therefore, there is a considerable number of patients requiring stent retrievers, aspiration devices, combination systems, and access products.

In general, the prevalence of the disorders associated with blood vessel obstruction continues to push healthcare organizations toward increasing their capacities for treating patients. More hospitals invest in infrastructure that enables effective thrombectomy treatment through quicker imaging and clot removal procedures performed by highly qualified specialists. With clot retrieval becoming more common in treating pulmonary embolism, peripheral arterial thrombosis, DVT, and dialysis access thrombosis, device manufacturers have been exploring new market areas within the cardiovascular and vascular intervention markets.

High Procedure Cost and Uneven Reimbursement Access Are Slowing Adoption in Cost-Sensitive Markets

High procedure cost remains a major restraint in the Global Blood Clot Retrieval Device Market, particularly across emerging and underfunded healthcare systems. Mechanical thrombectomy requires specialized devices, advanced imaging, catheterization or neurointerventional suites, trained specialists, and post-procedure critical care, making the total treatment pathway expensive. A 2025 India-based thrombectomy cost study reported an average total treatment cost of ₹555,399 per patient, highlighting the affordability challenge in private hospital settings and other self-pay markets.

Uneven reimbursement further limits adoption, even in developed markets where clinical value is well established. A 2024 analysis of U.S. Medicare thrombectomy economics reported that average submitted charges for stroke thrombectomy ranged from US$3,083 to US$3,784, while Medicare reimbursements averaged only US$621 to US$687, creating a reimbursement-to-charge gap of roughly 18–22%. As hospitals evaluate thrombectomy programs through both clinical and financial lenses, inconsistent payment coverage can delay procurement of advanced stent retrievers, aspiration catheters, and large-bore access systems, especially in cost-sensitive regions.

Segmentation Analysis

The global blood clot retrieval device market is segmented based on product type, retrieval technique, application / use case, vessel location, vessel compatibility, usage type, end-user, procurement channel, and region.

Aspiration Catheters Are Becoming a Core Platform for Faster and More Efficient Clot Removal

The aspiration catheters are experiencing strong popularity in the Global Blood Clot Retrieval Device Market. It has been predicted that the segment will hold around 28.3% market share in 2026 due to the growing adoption of aspiration-based thrombectomy and the high commercial value associated with penumbra-like retrieval systems. This segment is highly favored because of its capability of allowing direct clot aspiration, quicker reperfusion, reduced number of passes, and procedural efficiency in acute ischemic stroke, pulmonary embolism, peripheral arterial thrombosis, and venous blood clot removal procedures.

Another reason contributing to the commercial success of the aspiration catheter segment includes continuous advancements in terms of larger catheter bore, flexibility, trackability, suction efficacy, and compatibility with modern guide catheters. While the large-bore aspiration catheters are in growing demand for high-clot-burden cases, distal access catheters have become very popular for difficult cases of vessel occlusions. In light of the fact that hospitals are favoring faster treatment time, reduced risk of complications, and devices focused on delivering better outcomes, this segment has emerged as a highly commercially viable one in the industry.

Geographical Penetration

North America’s Advanced Stroke Infrastructure Is Driving Adoption of Integrated Blood Clot Retrieval Device Platforms

North America is anticipated to be the leader in the blood clot retrieval device market, capturing 41.5% market share owing to its state-of-the-art infrastructure of stroke treatment, high adoption rate of mechanical thrombectomy, neurointerventional capabilities, and good reimbursement prospects. The United States stands out as the key region, fueled by the existence of well-established stroke networks, hospitals equipped with thrombectomy capabilities, advanced imaging technologies, and the presence of market leaders like Medtronic, Stryker, Penumbra, Johnson & Johnson MedTech, and Boston Scientific.

The region is also propelled forward by growing usage of aspiration catheters, stent retrievers, clot retrieval systems, and AI-powered workflow solutions for stroke patients. As hospitals aim to improve reperfusion times, reduce disabilities, and deliver better emergency vascular care outcomes, North America leads in purchasing cutting-edge clot retrieval devices for applications in acute ischemic stroke, pulmonary embolism, peripheral arterial thrombosis, DVT, and dialysis access thrombosis cases.

U.S Blood Clot Retrieval Device Market Trends

The U.S. market for blood clot retrieval devices will be influenced by increasing demand for endovascular thrombectomy, improved stroke center capabilities, and adoption of both aspiration and combined clot retrieval techniques. According to the October 2024 updates on stroke facts by the CDC, there are over 795,000 cases of stroke annually in the U.S., out of which 610,000 cases are new strokes. Hence, there is a big opportunity in terms of emergency care applications for stent retriever, aspiration catheter, thrombectomy system, and access devices for the acute ischemic stroke procedure.

A significant trend impacting the market is the move away from stand-alone clot retrieval technologies to integrated thrombectomy solutions incorporating large-bore aspiration catheters, stent retrievers, guide catheters, artificial intelligence-assisted imaging, and stroke workflows. The focus for hospitals in the U.S. is on achieving door-to-puncture time, increasing first pass success, reducing complication rates, and improving procedure efficiency. With the expansion of stroke programs and vascular intervention physicians performing clot procedures beyond stroke, there is an increasing emphasis on outcomes-driven device selection.

Japan Blood Clot Retrieval Device Market Outlook

Japan can be considered a high-potential country for selling blood clot retrieval systems due to the growing number of elderly in the country, the availability of hospitals, and acute stroke care initiatives in the country. As stated in the Aging Society Report 2024 from the government of Japan, the country currently has a population of 36.23 million elderly aged 65 years and above, which amounts to 29.1% of the total population in the nation. Such demographic data directly translates to increased risks for ischemic stroke, thromboembolisms, and vascular interventions; therefore, constant demand will be present for such devices as stent retrievers, aspiration catheters, combination retrieval tools, and access equipment.

Another driver behind market expansion is the growing number of thrombectomy experts and facilities in Japan. According to a study by Yoshimura et al. (2026), as of September 2024, Japan has 2,427 neuroendovascular therapy specialists as well as 812 mechanical thrombectomy specialists. However, limited accessibility in remote areas still exists. On the whole, prospects for the Japanese market of clot retrieval products are positive, as market growth will occur due to aging-related conditions, stroke center development, process standardization, and adoption of aspiration and combined thrombectomy technologies.

Competitive Landscape

The Global Blood Clot Retrieval Device Market is moderately concentrated and is dominated by large medtech firms with robust offerings in the neurovascular, peripheral vascular and thrombectomy space. Medtronic, Stryker, Penumbra, Inc., Johnson & Johnson MedTech, Terumo Neuro, Boston Scientific Corporation and Becton, Dickinson and Company are leading companies with strong competitive positioning due to established relationships with hospitals, comprehensive device offerings, solid clinical data and the capability of handling high volumes of thrombectomy procedures. Competitive dynamics in this market are driven by first pass success rate, catheter deliverability, clot capture effectiveness, suction power, vessel safety and physician confidence.

Key specialty companies in this market include AngioDynamics, Inc., Imperative Care, Inc., Rapid Medical, phenox, ACANDIS GmbH, Balt Group, Vesalio Inc. and Koninklijke Philips N.V. These firms are enhancing competitive intensity in this market through focused product offerings in the areas of aspiration thrombectomy, neurovascular clot retrieval, large vessel thrombus removal and advanced access solutions. Competition will shift from stand-alone products to integrated thrombectomy platforms, procedural workflow, favorable payment structure and extension to pulmonary embolism, peripheral thrombosis, DVT and dialysis access thrombosis.

Recent Developments

- April 2026: Rapid Medical received FDA clearance for TIGERTRIEVER 25, strengthening its position in large vessel occlusion stroke treatment with an adjustable thrombectomy device designed for high clot-burden proximal vessels.

- February 2026: Vesalio expanded its international neurovascular portfolio with CE Mark certification for NeVa VS and NeVa 3.0 mm and additional FDA clearance for aspiration catheters, reinforcing its position in distal and complex stroke thrombectomy.

- February 2026: Avantec Vascular, a NIPRO company, received FDA 510(k) clearance for a thrombectomy system targeting thrombus removal in the peripheral venous system, supporting broader commercialization in DVT-focused clot retrieval.

- July 2025: Stryker’s Inari Medical launched the next-generation InThrill Thrombectomy System, addressing arteriovenous access and small vessel thrombus cases with a purpose-built small vessel thrombectomy platform.

- March 2025: Stryker’s Inari Medical launched the Artix Thrombectomy System, a combined aspiration and mechanical thrombectomy platform designed for a broad spectrum of peripheral arterial thrombus cases.

- February 2025: Stryker completed the acquisition of Inari Medical, Inc., expanding its position in the peripheral vascular thrombectomy segment and adding a strong venous thromboembolism clot removal portfolio to its device platform.

- January 2025: Imperative Care received FDA 510(k) clearance for its Zoom System, including the large-bore 0.088-inch catheter for aspiration when used with Zoom catheters, strengthening complete stroke thrombectomy workflows.

AI Impact Analysis

AI is expected to bolster the growth of the Global Blood Clot Retrieval Device Market through enhanced patient identification, patient prioritization for stroke treatment, treatment prioritization, and workflow optimization in thrombectomies. The largest effect of AI is expected to come from imaging software equipped with AI technology that can identify large vessel occlusions, determine clot location, evaluate viable brain tissue, and aid in efficient patient routing to facilities able to perform thrombectomy.

AI is not expected to render blood clot retrieval devices redundant. However, it can help optimize the decision-making process in the use of such devices by accelerating procedures, assisting in appropriate case selection, and coordinating communication between emergency units, stroke centers, radiologists, and neurointerventionists. Companies that integrate thrombectomy devices with AI-powered imaging software, workflow tools, procedural planning solutions, and outcome assessment software will benefit from this transition to a faster, data-oriented approach to clot removal treatment.

White Space Opportunities

There are significant white space opportunities within the Global Blood Clot Retrieval Device market for companies whose solutions cannot yet adequately meet the current standards with regard to first-pass success, distal vessel navigability, clot capture efficiency, and procedure complexity. The market is moving towards devices that can facilitate faster reperfusion, safe navigation in tortuous blood vessels, and efficient clot removal in strokes, pulmonary embolisms, peripheral thrombi, deep vein thrombi, and dialysis access thrombosis.

White space opportunities include advanced generation aspiration catheters, large bore access devices, mini-stent retrievers for distal vessel occlusions, multi-modality thrombus retrieval systems, and pulmonary embolism thrombectomy devices. Organizations that provide integrated solutions with improved device compatibility, shorter procedure times, decreased risk of complications, and greater clinical effectiveness would stand a good chance of tapping into this need. There are also opportunities to explore new markets, especially emerging countries, where there is a growing presence of stroke centers and cath labs.

DMI Opinion

As per the findings of DataM, the main constraint faced in the Global Blood Clot Retrieval Device Market does not revolve around generating clinical needs, but rather, providing devices that allow for faster reperfusion, excellent clot engagement, safe navigations through vessels, and reliability in results achieved. It is shifting away from traditional methods of thrombectomy treatment and towards aspiration technology, large bore catheters, stent retrievers, retrieval technique combinations, and distal vessel access.

Clinical performance, first-pass success rate, compatibility of the device, surgeon's trust, reimbursement coverage, and integration into stroke and vascular interventional procedures will define the success of any commercial enterprise. According to DataM, future growth in the Global Blood Clot Retrieval Device Market will rely heavily on the companies' ability to provide an end-to-end solution for acute ischemic stroke, pulmonary embolism, peripheral thrombosis, DVT, and dialysis access thrombosis.

Why This Report Matters in 2026?

The Global Blood Clot Retrieval Device Market will become very strategic by 2026 as healthcare institutions focus more on achieving quicker reperfusion, minimally invasive removal of clots, and better results for life-threatening vascular disorders. Increasing numbers of acute ischemic stroke, pulmonary embolism, DVT, peripheral arterial thrombosis, and dialysis access thrombosis patients are motivating healthcare facilities to improve their thrombectomy techniques.

As part of that shift, there is an increasing preference for the use of endovascular tools as opposed to standalone thrombectomy devices, such as stent retrievers, aspiration catheters, large bore access systems, and guide catheters, among others. The buyers' focus is now on the degree of first pass efficacy, navigability within blood vessels, clot removal efficiency, risks involved, and payment support for procedures, among others.

This report is relevant since it gives stakeholders insights into where the growing need exists for blood clot removal devices, the emerging technological advancements in the field, regions with high adoption potential, as well as companies best placed to dominate this niche market.

Why Choose DataM?

- End-to-End Blood Clot Retrieval Device Ecosystem Assessment: Analyzes the comprehensive ecosystem for thrombectomy devices, including stent retrievers, aspiration catheters, retrieval system hybrid devices, guide catheters, micro-catheters, and related access devices for use in emergency vascular procedures.

- Product and Technology Assessment: Analyzes leading platform technologies, including those based on stent retriever platforms, aspiration thrombectomy platforms, large bore catheters, distal access catheters, and mechanical thrombectomy hybrid devices to uncover commercially viable technology.

- Application/Use Case and End-User Assessment: Tracks adoption of thrombectomy devices in acute ischemic stroke, pulmonary embolism, peripheral artery thrombosis, deep vein thrombosis, and dialysis access thrombosis, as well as hospital, stroke center, cardiovascular center, and vascular surgery utilization.

- Clinical, Regulatory, and Reimbursement Review: Considers the effect of thrombectomy candidate qualifications, stroke center development, referral network creation, regulatory approval, reimbursement, and clinical adoption on regional market growth.

- Competitive Strategy Benchmarking: Monitors competition of Medtronic, Stryker, Penumbra, J&J MedTech / CERENOVUS, Terumo Neuro, Boston Scientific, BD, AngioDynamics, and Imperative Care based on product innovation, portfolio development, and hospital partnerships.

- Pricing, Procurement & Market Access Insights: Evaluates hospital buying focus, medical device pricing, clinical procedure economics, tendering trends, impact of reimbursement on hospital decision-making, and criteria for evaluation.

- Growth Opportunities and Product Expansion Strategy: Explores white space opportunities and new product strategies in aspiration thrombectomy, distal vessel clot retrievals, pulmonary embolism thrombectomy, stroke workflow solutions, next-generation thrombectomy platforms, and emerging markets.

Key Procurement Priorities and Buyer Evaluation Criteria

- Buyers in the Global Blood Clot Retrieval Device Market are increasingly prioritizing devices that deliver faster reperfusion, higher first-pass success, strong clot engagement, improved vessel navigation, and lower procedural complication risk.

- Procurement decisions are shifting toward integrated thrombectomy solutions that combine stent retrievers, large-bore aspiration catheters, access systems, guide catheters, microcatheters, and support devices for complete endovascular clot removal workflows.

- Hospitals, stroke centers, neurointerventional units, cardiovascular centers, and vascular surgery teams are evaluating vendors based on clinical efficacy, device deliverability, clot capture performance, compatibility with existing cath lab infrastructure, physician familiarity, reimbursement support, and procedural cost efficiency.

- Vendors with strong capabilities in aspiration thrombectomy, distal vessel access, combined retrieval systems, pulmonary embolism thrombectomy, and neurovascular intervention support are better positioned to win long-term hospital contracts as buyers move toward outcome-driven and procedure-efficient device selection.