Arc Welding Torch Market Overview

The arc welding torch market includes the offerings, systems, services, and value chain elements that affect demand dynamics, technology choice, and procurement practices. The market can be classified based on its process type, cooling method, degree of automation, consumables, current capacity, and end-user industry, with sales volume being determined by the intensity of specifications, regulatory requirements, supply stability, and supplier ability to meet performance standards for industrial usage.

It is evolving from being price- and availability-based to becoming a lifecycle performance-, efficiency-, integration-, and scalability-based approach. End-users are now seeking industry-specific solutions and dependability, thereby driving suppliers to align their product portfolios and build closer relationships with demand centers.

Arc Welding Torch Industry Trends and Strategic Insights

- Asia-Pacific remains the most influential region for demand creation and competitive benchmarking in the current market structure.

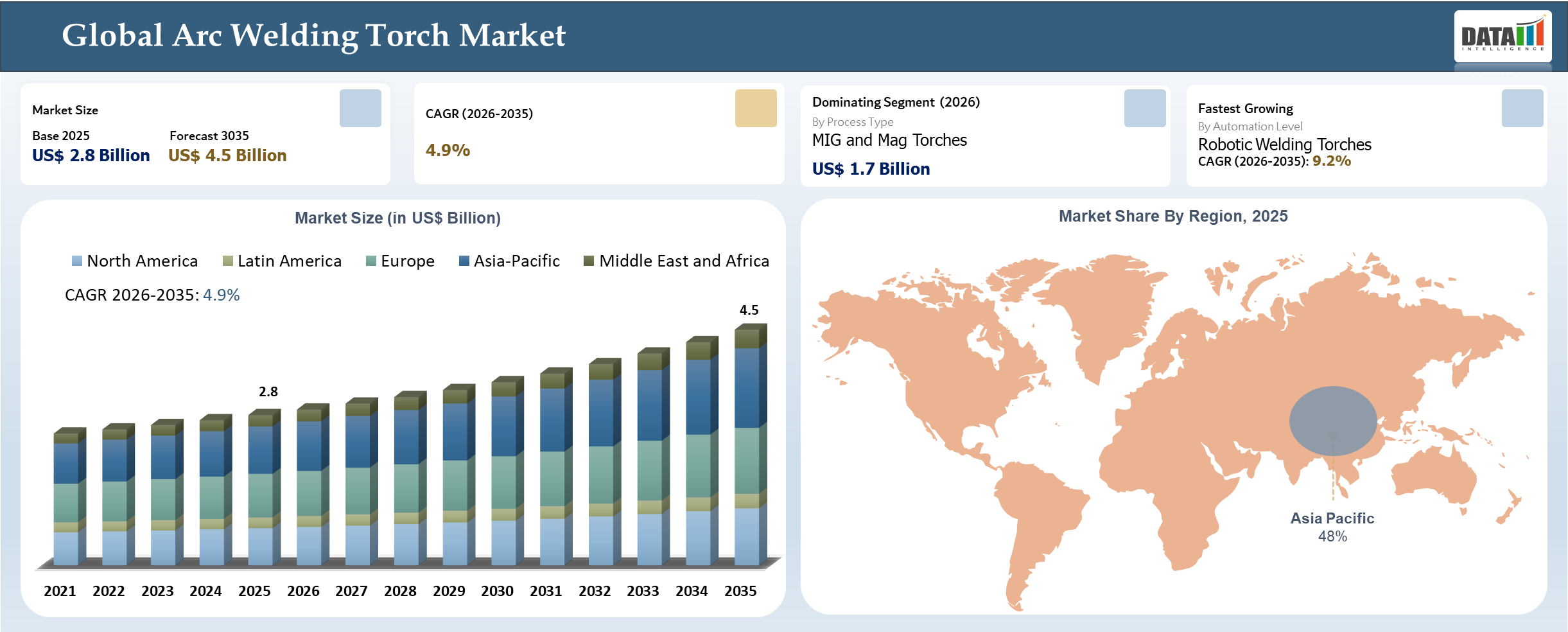

- MIG and MAG Torches is the most commercially important segment because it aligns with current buying behavior, installed base requirements, and near term scaling feasibility.

- The strongest growth trigger is higher welding intensity in automotive, fabrication, and infrastructure manufacturing, while the main execution risk is price pressure from low cost torch imports and longer life consumables.

- Vendors that combine product depth, application support, and faster commercialization pathways are best positioned to defend share.

Key Takeaways

- The increasing adoption of welding automation, robotic welding cells, and Industry 4.0-enabled manufacturing systems is emerging as a key industry trend, with end users seeking arc welding torches that offer higher precision, improved durability, seamless robotic integration, and reduced operational downtime.

- Asia-Pacific maintains a leading position due to its extensive manufacturing ecosystem, large-scale fabrication activities, expanding automotive production, growing shipbuilding industry, and continued investments in industrial automation and infrastructure development.

- North America is projected to record significant growth as manufacturers increasingly adopt advanced welding technologies, robotic welding systems, and high-performance welding equipment to improve productivity, quality control, and labor efficiency across industrial operations.

- Rising industrial fabrication requirements across automotive, construction, heavy machinery, energy, rail, and shipbuilding sectors are becoming major factors driving demand for high-performance arc welding torches capable of supporting continuous and precision-intensive welding applications.

- The growing integration of robotic and collaborative robotic (cobot) welding systems is increasing demand for automation-compatible welding torches that support consistent weld quality, enhanced productivity, and flexible manufacturing environments.

- Industry participants are increasingly evaluating investments based on lifecycle performance, reliability, ease of maintenance, automation compatibility, application-specific engineering support, and operational efficiency rather than focusing solely on upfront equipment costs.

- Increasing investments in manufacturing modernization, infrastructure construction, transportation equipment production, renewable energy projects, and smart factory initiatives are creating significant opportunities for arc welding torch manufacturers, welding equipment suppliers, and industrial automation solution providers worldwide.

Arc Welding Torch Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 2.8 Billion | |

| 2035 Projected Market Size | US$ 4.5 Billion | |

| CAGR (2026-2035) | 4.9% | |

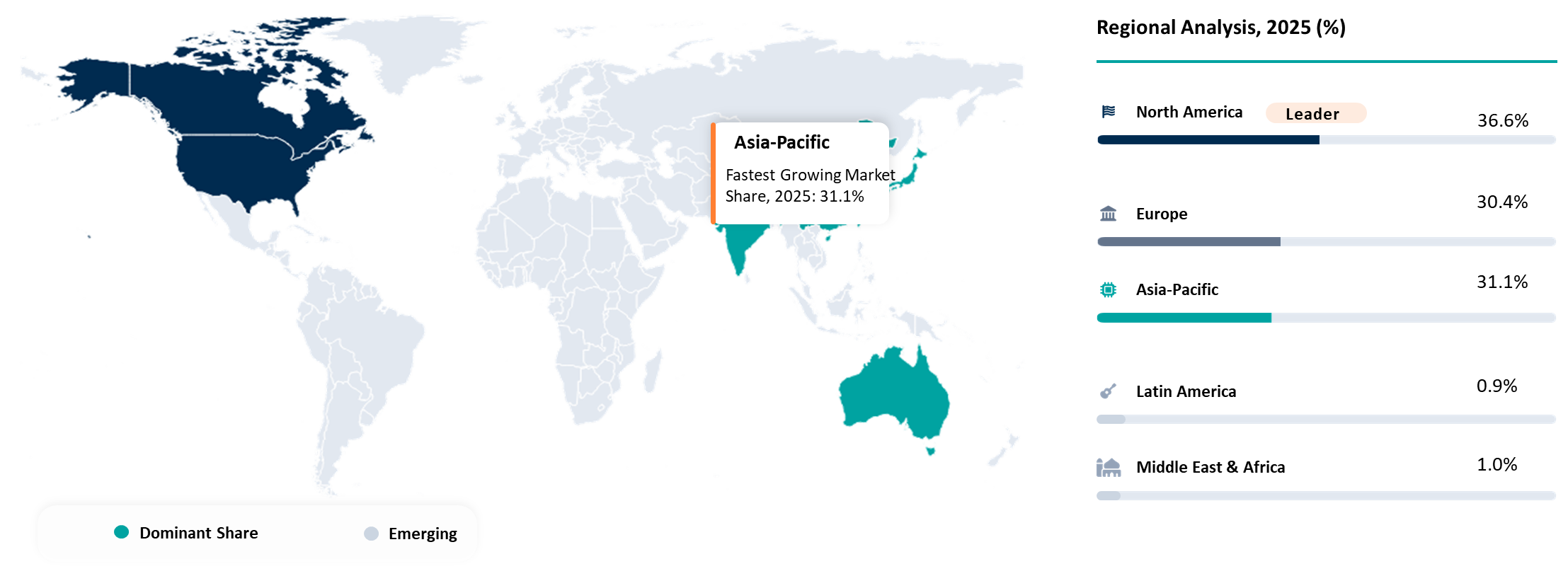

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Process Type | MIG and MAG Torches, TIG Torches, Plasma Torches, Submerged Arc Torches | |

| By Cooling Type | Air Cooled, Water Cooled | |

| By Automaton Level | Manual, Semi Automatic, Robotic and Automated | |

| By Wear Part | Gas Nozzles, Contact Tips, Diffusers, Collets and Collet Bodies, Electrodes | |

| By Current Rating | Below 300A, 300A to 50A, Above 500A | |

| By End-Use Industry | Automotive, Construction, Shipbuilding, Heavy Machinery, Energy and Power, Aerospace and Rail | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Arc Welding Torch Disruption Analysis

Shift from Equipment-Centric Welding to Outcome-Driven Performance Solutions Redefining Value Metrics

The first disruption within the arc welding torch segment is associated with the transition from competition based on products to value assessment focused on results. The purchasing decision today is made based on metrics related to uptime, welding results, efficiency, compliance with regulations, and total cost of ownership. This requires suppliers to adjust their approaches from being product-oriented to being oriented at performance and operational efficiency.

Another disruption is linked to ecosystem convergence that involves the growing level of connectivity between torches, power sources, consumables, automation systems, and services. Such a change creates advantages for players who have integrated offers and collaboration with other parties; however, switching costs increase due to increased integration. At the same time, generalist companies can lose relevance unless they innovate specifically, whereas newcomers may attract attention thanks to innovative offers tailored to niches.

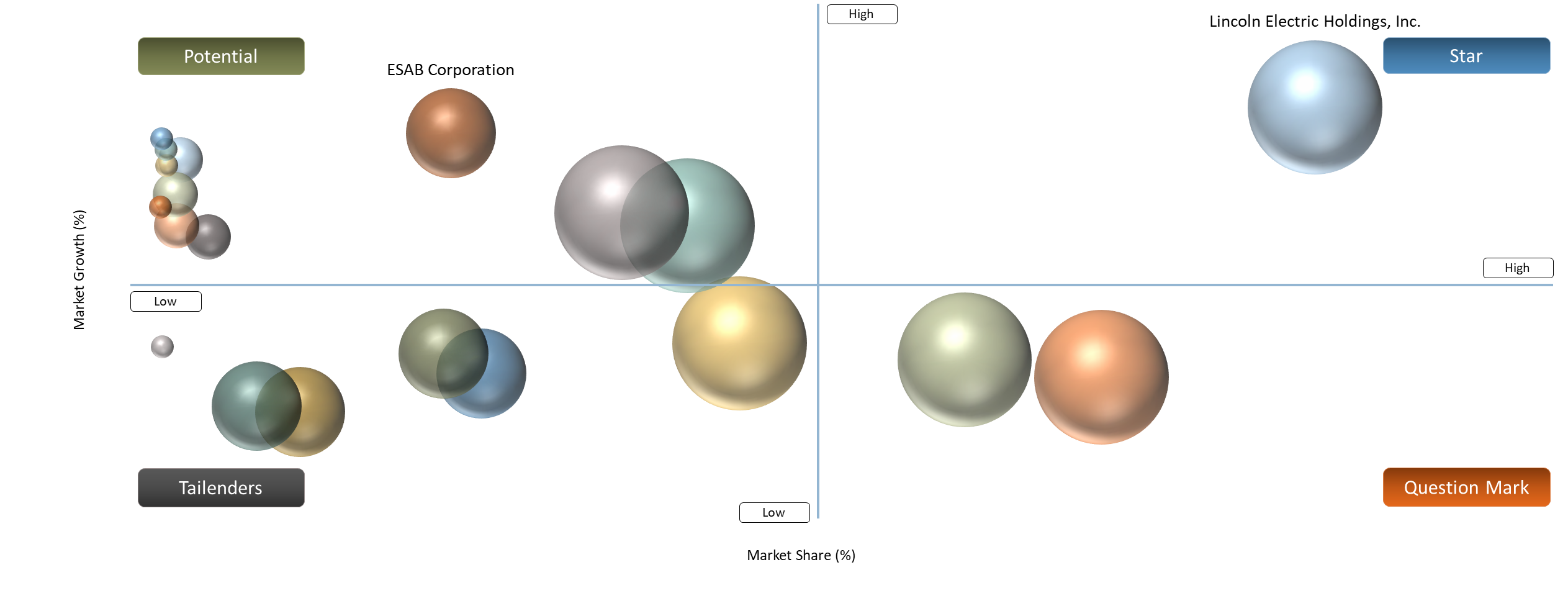

BCG Matrix: Company Evaluation

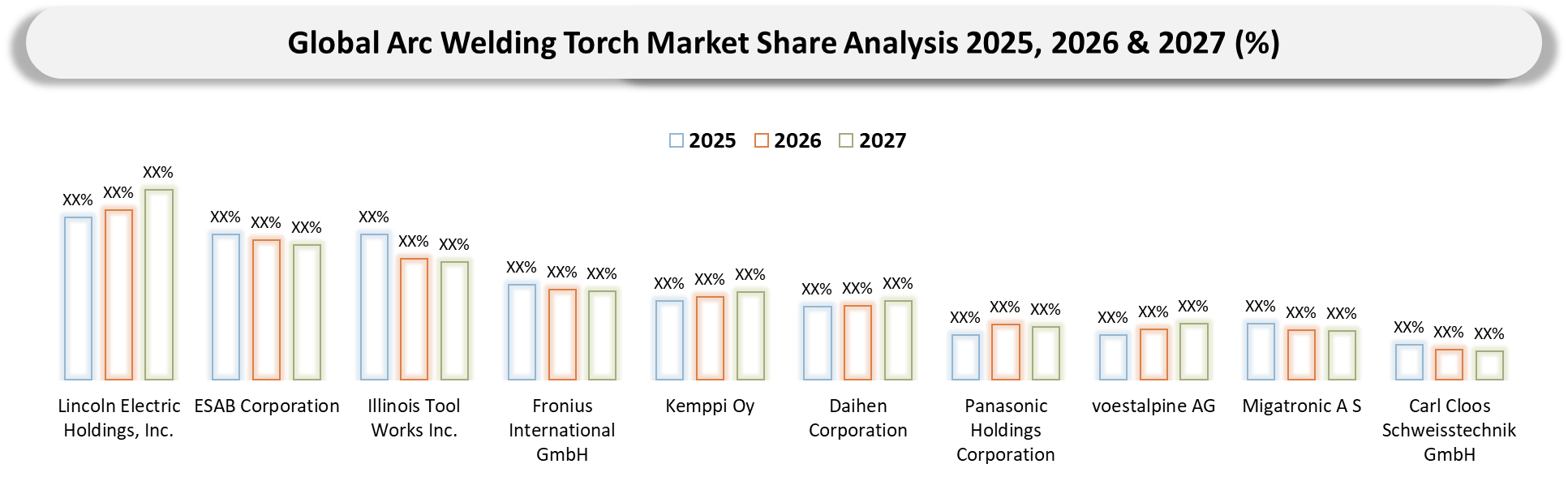

The market leaders quadrant is formed by the companies Lincoln Electric Holdings, Inc., ESAB Corporation, and Illinois Tool Works Inc. due to their high market share and development of robotic and automated arc welding torches. Fronius International GmbH and Kemppi Oy complement the market leaders quadrant with their innovative digital welding technology and precision torches. Companies such as Panasonic Holdings Corporation and Daihen Corporation form the established performance quadrant due to their stability in their earnings and industrial demand along with their automation capabilities. Companies such as voestalpine AG and Carl Cloos Schweisstechnik GmbH enjoy consistent earnings by virtue of their robust OEM relationships and automation capabilities.

The emerging growth quadrant is formed by companies Migatronic A/S, Alexander Binzel Schweisstechnik GmbH and Co. KG, and EWM GmbH, who are growing in terms of innovation and automation but have yet to grow on the global level. Companies like Ador Welding Limited and Riland Industrial Corporation Limited are forming their presence by offering competitive prices and expanding into other markets. The niche and specialized quadrant is formed by companies such as TBi Industries GmbH, Dinse GmbH, Cebora S.p.A., Trafimet Group S.p.A., and OTC Tools Company.

Arc Welding Torch Market Dynamics

Shift Toward High-Performance and Specialized Welding Applications

The market dynamics for arc welding torches have become more inclined towards the rising need for high-quality and application-specific welding. During the last decade, the portion of complex welding applications including high-tensile steel, aluminum welding, and specialized alloy welding has grown from around 30% to 35% to almost 50% to 55% of the total welding operations carried out in the industry across leading manufacturing zones.

Such developments are expected to increase the demand for customized torches designed to achieve superior arc stability, enhanced heat resistance, and optimal material compatibility. Market analysts indicate that the segment of high-end and application-specific welding equipment is recording a compound annual growth rate of 6%-8%, faster than regular equipment types. Consequently, manufacturers with specialized and premium torch products have started gaining increased pricing leverage and extended replacement periods, thus supporting market value expansion.

High Wear Rate Leading to Frequent Replacement and Higher Lifecycle Costs

Arc welding torches are subjected to constant conditions of high temperatures, spatter, and physical stress that contribute to fast degradation of important elements like nozzles, contact tips, and liners. Under industrial conditions, their replacement frequency may be as little as a couple of weeks depending on the level of use, thus necessitating increased maintenance needs from end users.

The process of frequent replacements not only contributes to an increase in overall costs, but also makes purchasing decisions more reliant on running costs in addition to the upfront cost of the equipment itself. In cost-driven industries, it may lead to postponing the adoption of more efficient torches due to higher costs.

Arc Welding Torch Segmentation Analysis

The global Arc Welding Torch market is segmented based on process type, cooling type, automation level, wear part, current rating, end use industry and region.

MIG/MAG and TIG Welding Torches Driving Core Value Concentration in Arc Welding Market

Process type segmentation becomes highly significant for the arc welding torches industry, with the MIG/MAG and TIG welding torches being the most valuable segments. Such segmentation is important since the efficiency and functionality of torches are dependent on a wide range of variables, including deposition rate, duty cycle, operator proficiency, automation capability, and application requirements, among others, making it a more useful criterion than broad-based product segmentations.

There is an increasing trend toward optimizing processes and minimizing costs in relation to consumables and their lifetime rather than purchasing the equipment alone. There is thus growing interest in purchasing torches that minimize downtimes and can be integrated into robot or collaborative robot setups, as well as those that facilitate quick replacement of wear parts.

Arc Welding Torch Geographical Penetration

Asia-Pacific Dominance Driven by Industrial Scale, Hybrid Automation Adoption, and Evolving Distribution Models

Asia-Pacific emerges as the market segment with the highest structural density in terms of arc welding torches owing to the heavy fabrication environment, along with diversified industrial structure. The demand for arc welding torches here is spread out across low-cost manual welding units, exports-based manufacturing units, and precision-oriented automated units. Such an environment results in continuous demand for arc welding torches in both economic and superior versions.

The region operates within a mixed phase where both robotic welding units and manual/semi-automatic welding units operate side-by-side, ensuring that continuous demand exists at different levels of technology.

China Arc Welding Torch Market Trends

China represents the largest market for arc welding torches because of the heavy demand for shipbuilding, automotive industry, construction machinery, and fabrication sectors. The consumption extends to all levels of arc welding torches from inexpensive manual type to sophisticated robot-compliant types, thus representing a diversified market both in terms of quantity and specifications.

Automation-based improvements in the manufacturing sector, which is export-oriented in nature, influence the arc welding torch market because torches are selected based on criteria of robot compatibility, thermal capabilities, and longevity of consumables apart from cost considerations. Along with that, the buyer behavior trends towards systemized buying with more focus on reliability and rapid replacement, giving an advantage to established global players and efficient local players.

India Arc Welding Torch Market Outlook

India’s arc welding torch market is expanding at a steady pace, fueled by robust consumption from the automotive, construction, heavy engineering, and fabrications sectors. Welding is an integral part of these industries, with torches being extensively employed within workshops and industrial manufacturing operations. The growth in the market will be influenced by infrastructure development and manufacturing capabilities, which will drive equipment and consumables sales.

The trend towards automation and inverter welding, especially in automotive clusters and manufacturing locations exporting goods overseas. Despite manual welding techniques being predominantly practiced, there is an upswing in using efficient torches suitable for robotic applications. Additionally, consumers have started to emphasize consistency in welds and uptime along with cost-effective solutions, thus driving market demand.

Arc Welding Torch Competitive Landscape

The competitive landscape is led by a mix of global leaders and focused specialists, with Lincoln Electric Holdings, Inc., ESAB Corporation, Illinois Tool Works Inc., and Fronius International GmbH shaping category standards. Market positioning depends on portfolio breadth, application depth, route to market strength, and the ability to support customers after the initial sale.

The strongest companies are using product upgrades, partnerships, regional manufacturing, and selective vertical focus to defend share. As the market matures, leadership is likely to concentrate further around suppliers that can translate technical capability into faster commercialization and stronger customer retention.

Key Developments of Arc Welding Torch Market

- Jan 2026: Lincoln Electric partnered with ORNL to advance arc welding automation and large-scale metal fabrication systems using advanced torch-based welding technologies for industrial production.

- Jun 2025: ESAB Corporation acquired EWM GmbH to expand its portfolio of advanced welding torches and automation systems for heavy industrial applications.

- Feb 2025: Lincoln Electric launched the Ranger Air 330MPX welding system integrating multi-process arc welding torch capabilities for construction and field welding operations.

- March 2025: Miller Electric introduced new robotic welding torch systems with seam tracking and touch sensing for improved automation accuracy in industrial welding.

- September 2025: Miller Electric partnered with Gullco International to integrate high-deposition arc welding torch technology into mechanized track welding systems for heavy fabrication applications.

Why Choose DataM?

- Technological Innovations: Covers advancements in arc welding torch design including improved heat resistance materials, optimized cooling systems, inverter-compatible torch configurations, and automation-ready interfaces. These developments are enhancing weld stability, reducing consumable wear, and improving productivity in high-duty industrial applications.

- Product Performance & Market Positioning: Evaluates torch performance across manual, semi-automatic, and robotic welding environments, comparing arc stability, duty cycle, consumable life, and thermal efficiency. Leading manufacturers differentiate through durability, compatibility with automation systems, and consistency in weld quality across varied industrial conditions.

- Real-World Evidence: Highlights application use cases across automotive fabrication, shipbuilding, infrastructure construction, and heavy engineering. Measurable outcomes include improved welding speed, reduced rework rates, higher uptime in production lines, and better material compatibility in complex welding tasks.

- Market Updates & Industry Changes: Tracks developments such as increased automation in welding lines, expansion of robotic welding cells, rising adoption of inverter-based systems, and regional manufacturing expansion across Asia-Pacific, India, and China. Industry demand is also influenced by infrastructure investments and industrial modernization cycles.

- Competitive Strategies: Analyzes how key players are strengthening market position through expanded distributor networks, consumable-focused offerings, automation-compatible torch systems, and localized service support. Differentiation is increasingly driven by reliability, aftermarket service strength, and integration with robotic welding ecosystems.

- Pricing & Market Access: Explains pricing variations across standard manual torches, heavy-duty industrial models, and robotic-compatible systems, along with consumable-driven cost structures. Market access is influenced by regional distribution strength, aftermarket availability, and service responsiveness.

- Market Entry & Expansion: Identifies growth opportunities in emerging manufacturing hubs driven by infrastructure development, automotive expansion, and fabrication growth. OEMs are expanding through regional partnerships, localized production, and strengthened after-sales networks to improve penetration and service efficiency.

Target Audience

- OEMs and product developers active across the arc welding torch value chain

- Distributors, channel partners, and regional aggregators

- Strategy teams, product managers, and corporate development leaders

- Procurement heads and technical buyers at key end users

- Investors, consultants, and market intelligence teams tracking emerging growth pockets