Alumina Market Overview

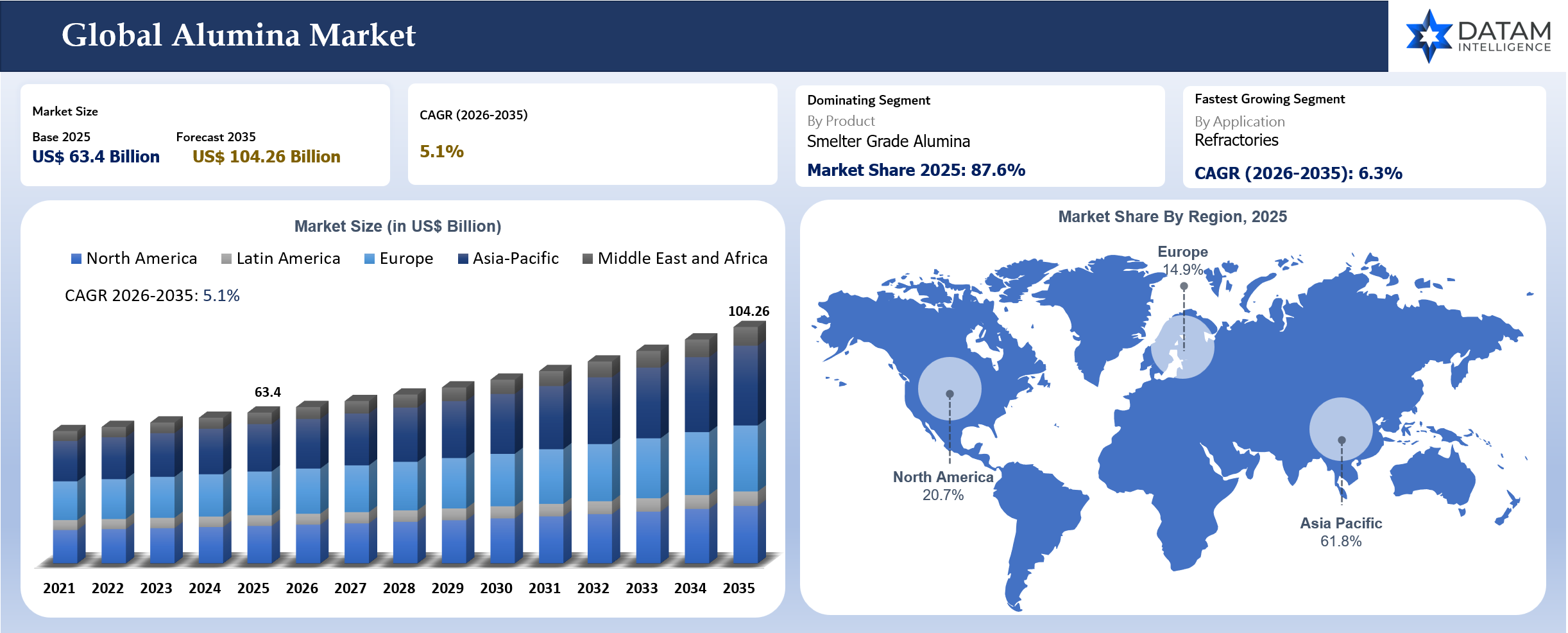

The global alumina market reached US$ 63.4 billion in 2025 and is expected to reach US$ 104.26 billion by 2035, growing at a CAGR of 5.1% during 2026-2035. Alumina remains one of the most important intermediate materials in the aluminum value chain because most output is consumed by primary aluminum smelters. Demand is closely linked to aluminum consumption in transportation, building and construction, packaging, electrical infrastructure, renewable energy equipment and industrial machinery.

Smelter-grade alumina continues to dominate market demand because aluminum producers require steady, high-purity alumina feedstock for electrolytic reduction. Refinery economics are shaped by bauxite quality, caustic soda use, energy cost, residue management, freight and regional supply access. China remains the largest consuming market, while Australia, Brazil, India, Guinea-linked supply chains and the Middle East play important roles in raw material and refining flows.

Non-metallurgical alumina creates a higher-value but smaller market layer. Specialty alumina is used in refractories, ceramics, abrasives, flame retardants, catalyst supports, polishing compounds, batteries and advanced materials. Growth in lithium-ion battery separators, technical ceramics and high-purity electronics applications is improving the strategic value of non-smelter grades.

Key Takeaways

- Smelter-grade alumina dominated the global alumina market with 87.6% share in 2025, supported by primary aluminum production across China, the Middle East, India, Russia, Canada and Europe.

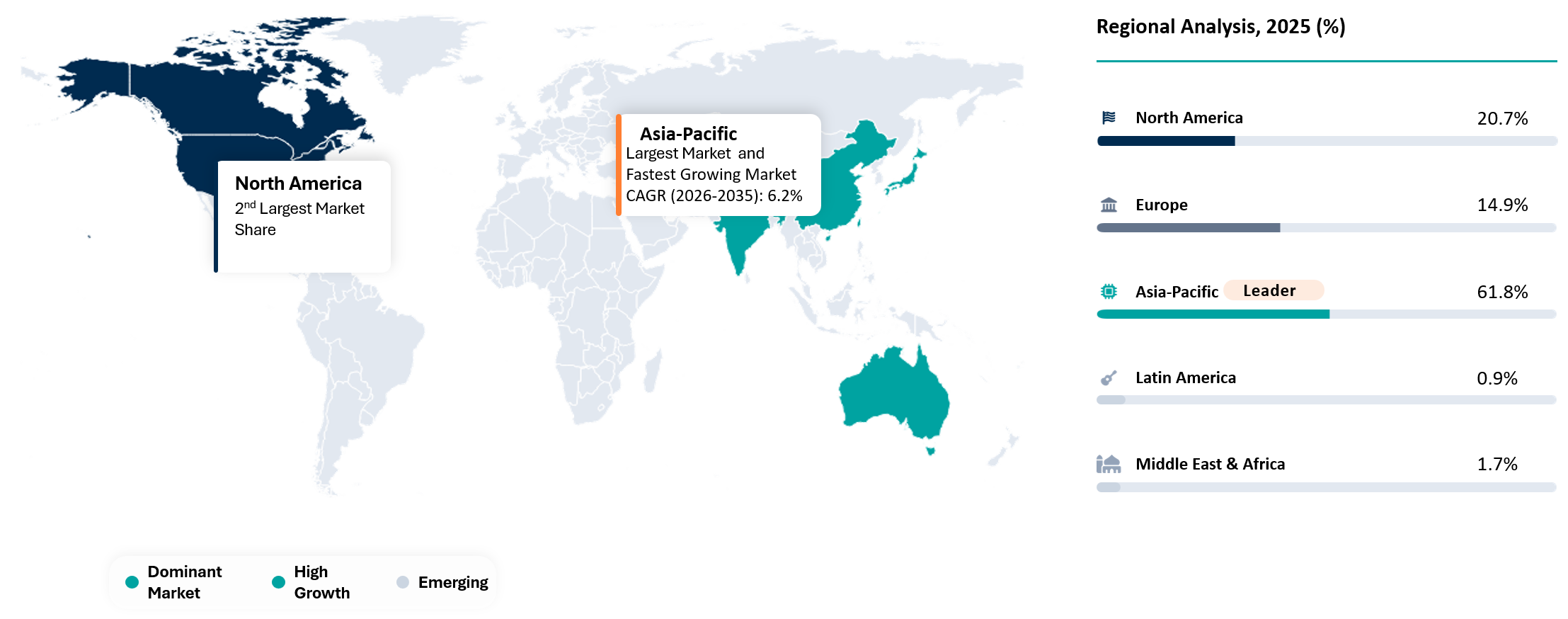

- Asia-Pacific dominated demand with 61.8% share in 2025, driven by China’s aluminum smelting base, India’s growing aluminum sector and downstream manufacturing demand.

- Non-metallurgical alumina is expected to grow faster during 2026-2035, supported by refractories, catalysts, technical ceramics, flame retardants, polishing and battery separator applications.

- Metallurgical application remains the largest demand area because aluminum smelting requires continuous alumina feedstock with tight quality specifications.

- Energy cost, caustic soda price, bauxite quality and residue storage remain the biggest refinery-margin pressure points.

- Supplier differentiation is moving toward bauxite security, low-cost refining, residue management, low-carbon alumina and specialty-grade capability.

Alumina Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 63.4 Billion | |

| 2035 Projected Market Size | US$ 104.26 Billion | |

| CAGR During 2026-2035 | 5.1% | |

| Largest Market | Asia-Pacific, 61.8% Market Share in 2025 | |

| Fastest Growing Market | Asia-Pacific, 6.2% CAGR between 2026 and 2035 | |

| Dominating Product | Smelter Grade Alumina, 87.6% Market Share in 2025 | |

| Fastest Growing Application | Refractories, 6.3% CAGR between 2026 and 2035 | |

| By Product | Smelter Grade Alumina, Chemical Grade Alumina, High Purity Alumina, Calcined Alumina and Specialty Alumina | |

| By Manufacturing Process | Bayer Process, Sintering Process, Combined Bayer Sintering Process, Alkoxide Hydrolysis Route, Hydrochloric Acid Leaching Route, Others | |

| By Application | Aluminum Smelting, Refractories, Ceramics, Abrasives, Catalyst Supports, Flame Retardants, Polishing, Battery Materials and Others | |

| By End-User | Aluminum Producers, Refractory Manufacturers, Ceramic Manufacturers, Chemical Companies, Battery Material Producers, Electronics Manufacturers and Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Why Does This Report Matter in 2026?

Alumina buyers enter 2026 with stronger exposure to energy cost, refinery reliability and bauxite security. Aluminum smelters need stable alumina supply because feedstock disruption can directly affect metal output. At the same time, refinery operators are managing caustic soda costs, residue storage challenges, decarbonization pressure and regional trade shifts.

The most important change is the separation between bulk smelter-grade supply and high-value specialty alumina demand. Smelter-grade alumina is driven by aluminum metal production, while specialty grades are linked to technical ceramics, refractories, batteries and electronics. Buyers need a market view that does not treat all alumina as one commodity.

Strategic Indicators for Alumina

High Regulation Impact

Environmental regulation directly affects alumina refining because bauxite residue storage, water use, caustic handling, emissions and land rehabilitation are closely scrutinized. Refineries need strong residue management and community engagement to maintain operating permits. Low-carbon aluminum commitments are also pushing buyers to review alumina supply chains more carefully.

High Investment Activity

Investment is focused on refinery efficiency, low-carbon alumina, residue reuse, high-purity alumina and specialty alumina production. Aluminum producers are improving energy performance and securing bauxite access. Specialty alumina suppliers are investing in ceramics, batteries and electronics-grade materials where margins are higher than smelter-grade products.

Supply Chain Disruption

Alumina supply chains can be disrupted by bauxite quality changes, refinery outages, port constraints, caustic soda shortages, energy disruptions and geopolitical restrictions. Smelters are exposed because alumina is consumed continuously and inventory buffers are limited. Refineries with captive bauxite and port access are better protected.

Pricing Volatility

Alumina pricing is affected by aluminum prices, refinery operating rates, caustic soda cost, energy prices, freight and regional supply disruptions. Smelter-grade alumina has tighter linkage with aluminum metal economics, while specialty alumina pricing depends more on purity, particle size, phase composition and customer qualification.

Procurement Pressure

Smelters need reliable alumina supply with consistent chemistry, particle size and moisture levels. Specialty buyers need tighter quality control and technical support. Procurement teams are increasingly evaluating supply security, low-carbon credentials, residue management and delivery reliability alongside price.

New Technology Adoption

Technology adoption is focused on process optimization, residue valorization, energy reduction, digital refinery control and high-purity refining. Advanced analytics can improve digestion efficiency, precipitation control and product quality. Specialty alumina producers are adopting tighter classification and calcination controls.

Regional Expansion Opportunity

India, China and the Middle East offer strong demand opportunities due to aluminum smelting and downstream consumption. Australia and Brazil remain key refining and bauxite-linked supply regions. Europe and North America offer higher-value opportunities in specialty alumina, ceramics and batteries.

Import-Export and Pricing Intelligence

Smelter-grade alumina pricing is closely linked to aluminum smelter demand, refinery operating rates, bauxite quality, caustic soda cost, freight and regional disruptions. Pricing can tighten quickly when refinery outages reduce available supply because smelters require continuous feedstock and cannot easily substitute material without operational risk. Atlantic and Pacific alumina prices may also diverge when freight, refinery availability or China import demand changes.

Specialty alumina pricing follows a different logic. Calcined alumina, tabular alumina, reactive alumina, high purity alumina and catalyst-grade alumina are priced around purity, soda content, particle size, surface area, phase composition, application qualification and supplier consistency. A high purity alumina used in battery separator coatings or semiconductor ceramics cannot be compared with bulk smelter-grade alumina only by tonnage or headline alumina price.

Import reliance is especially important for countries with aluminum smelting but limited refining capacity. Export competitiveness is strongest where bauxite security, low-cost refining, port access and refinery scale are present.

| HS Code | Reporter | Trade Flow | 2025 Trade Value | Interpretation |

| 281820 | Canada | Import | US$ 2.43 Million | Canada imports reflect balancing demand from aluminum smelters and specialty users when domestic refinery supply tightens. |

| 281820 | Australia | Export | US$ 6.33 Million | Australia acts as a major alumina export base due to integrated bauxite mining, refinery scale and port access. |

| 281820 | India | Import | US$ 1.31 Million | India imports support aluminum smelting growth and specialty alumina demand in refractories, ceramics and battery materials. |

| 281820 | UAE | Import | US$ 1.27 Million | UAE imports are linked to large aluminum smelting operations that require consistent smelter-grade alumina feedstock. |

| 281820 | Brazil | Export | US$ 3.45 Million | Brazil exports are supported by bauxite availability, established refining infrastructure and Atlantic Basin supply access. |

AI Impact Analysis

AI can improve alumina refinery performance by optimizing digestion, precipitation, calcination and residue handling. Refinery operators can use process data to reduce caustic loss, improve yield and stabilize product quality. This is especially valuable where bauxite quality varies and process control is difficult.

Predictive maintenance can reduce unplanned outages in grinding mills, digesters, pumps, filters and calciners. Refinery downtime can affect alumina supply and customer shipments, making reliability analytics commercially valuable.

Specialty alumina producers can use advanced analytics to control particle size, phase composition and purity. Better process control can improve consistency for ceramics, batteries and electronics applications.

Disruption Analysis

Alumina disruption is coming from low-carbon aluminum demand, refinery cost pressure and specialty material growth. Aluminum customers increasingly want lower-carbon supply chains, which pushes attention upstream to bauxite mining and alumina refining.

Residue management is becoming a larger operating issue. Bauxite residue storage requires land, monitoring and long-term environmental responsibility. Refineries that find credible residue reuse or reduction pathways can improve permitting and community acceptance.

Specialty alumina is disrupting the value mix. Smaller volumes can create stronger margins in ceramics, batteries and electronics. Producers with high-purity and engineered alumina capability can reduce exposure to bulk commodity cycles.

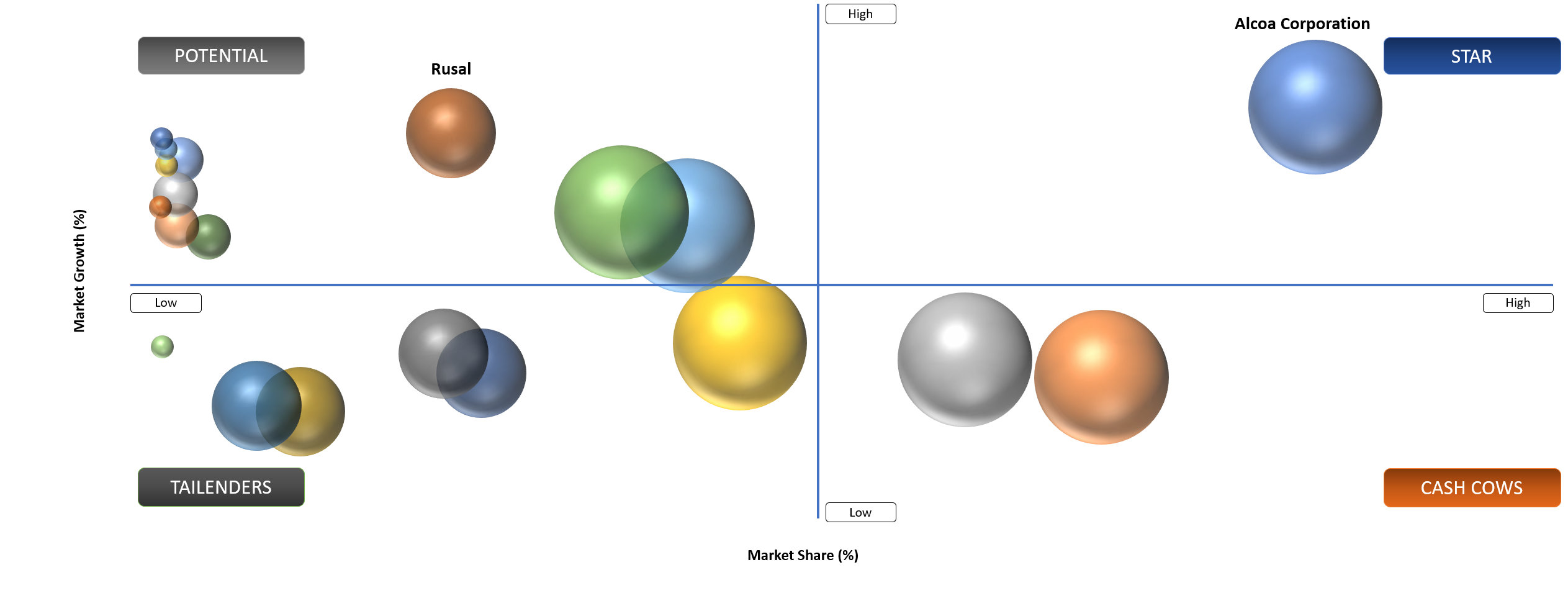

BCG Matrix: Company Evaluation

Star

Star players include Alcoa Corporation, Rio Tinto Group, South32 Limited, Aluminum Corporation of China Limited, Norsk Hydro ASA, Hindalco Industries Limited, Emirates Global Aluminum PJSC and Vedanta Limited. These companies benefit from integrated bauxite, alumina and aluminum positions.

Potential

Potential players include high-purity alumina producers, specialty alumina companies and battery-material suppliers serving separators, ceramics and electronics. Growth depends on purity control, customer qualification and ability to serve high-value applications.

Alumina Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact | Demand Concentration | Impacted Use Case | Strategic Impact |

Aluminum smelting demand sustains bulk alumina consumption | 3.8% | China, India, Middle East and Russia | Smelter-grade alumina | Maintains large-volume demand base |

Specialty alumina demand grows in ceramics and batteries | 2.9% | Japan, South Korea, China, U.S. and Europe | High-purity and calcined alumina | Improves margin opportunities |

Light weighting supports aluminum demand | 2.6% | Automotive, packaging and construction | Aluminum production | Pulls alumina through the metal value chain |

Refinery efficiency investments improve cost competitiveness | 1.9% | Australia, Brazil, China and India | Smelter-grade production | Supports operating margin resilience |

Specialty Alumina Demand Grows in Ceramics and Batteries

Specialty alumina is becoming a stronger growth driver because advanced ceramics, battery separator coatings, electronic substrates, wear-resistant components and polishing applications require tighter particle control than smelter-grade alumina. Buyers in these applications are not purchasing alumina only as an aluminum precursor. They are purchasing controlled chemistry, morphology, surface area, purity, particle size distribution and processing consistency that directly affect the performance of the finished product.

Ceramic manufacturers are increasing the use of calcined, reactive, tabular and high purity alumina where components must survive heat, wear, corrosion and electrical stress. Electronic ceramics, semiconductor process parts, kiln furniture, insulators, wear plates and precision components need alumina grades that support sintering behavior and final part reliability. Suppliers with strong calcination control, low soda grades and application-specific technical support can defend pricing better than bulk alumina refiners.

Battery applications are creating another growth pocket. High purity alumina is used in separator coating applications where thermal stability and safety performance matter. Lithium-ion battery producers and separator manufacturers need materials that can improve heat resistance and reduce failure risk under demanding operating conditions. Growth is strongest where battery customers move from lab-scale trials into qualified supply and where suppliers can prove purity, particle control and lot consistency.

Demand growth will not be evenly distributed across all alumina producers. Smelter-grade refiners may have scale but not necessarily the product-control capability needed for specialty applications. Producers with high purity refining routes, engineered calcination, milling and classification systems will capture more value. Specialty alumina is therefore important not only because it grows faster but because it changes the margin profile of the alumina market.

Restraint Impact Analysis

| Restraint | Drag On Market Growth | Primary Impact Area | Impacted Use Case | Strategic Impact |

Energy and caustic soda costs pressure refinery margins | 3.2% | Alumina refining | Bayer process operations | Raises production cost volatility |

Bauxite residue storage increases environmental burden | 2.8% | Refinery permits and ESG | Residue management | Raises long-term compliance cost |

Aluminum price cycles affect alumina demand | 2.5% | Smelters | Smelter-grade alumina | Creates demand volatility |

Bauxite quality variation affects process efficiency | 2.1% | Refineries | Digestion and precipitation | Requires stronger process control |

Bauxite Residue Storage Increases Environmental Burden

Bauxite residue remains one of the most important restraints for the alumina industry because the Bayer process generates large volumes of alkaline residue that require long-term containment, monitoring and rehabilitation. Residue storage areas need land, engineered dams, water management, seepage control, dust suppression and closure planning. Refinery operators therefore face environmental, social and financial obligations long after alumina production has taken place.

Environmental pressure is rising because communities, regulators and investors are paying closer attention to tailings safety, land disturbance, groundwater protection and biodiversity impact. Alumina refineries located near populated areas, forests, farms or water catchments face more intense scrutiny. A refinery can remain technically productive but still face approval delays or higher operating costs when residue storage and bauxite mining impacts become contested.

Residue management also affects refinery economics. Storage expansion, rehabilitation provisioning, monitoring systems and closure obligations add cost that may not be visible in basic alumina price comparisons. Refineries with older residue storage areas or constrained land availability may face higher long-term liabilities. New residue technologies, dry stacking, neutralization and residue reuse can help but they require investment and customer or regulatory acceptance.

Bauxite residue risk can also influence supply reliability. When environmental approvals are delayed or when community opposition increases, refinery feedstock security and mining plans can be affected. Buyers evaluating alumina suppliers should therefore consider more than production capacity. Residue management capability, bauxite mining permits, closure liabilities and community acceptance are becoming practical supply-chain risk factors.

Segmentation Analysis

Smelter-Grade Alumina Will Continue to Dominate Demand

Smelter-grade alumina will continue to dominate because primary aluminum producers require continuous feedstock for electrolytic reduction. The material must meet strict chemistry, particle size, moisture and flowability requirements to support stable potline operations. Even small quality variation can affect smelter efficiency, power use, fluoride balance and operational stability. For smelters, alumina is not a discretionary raw material. It is the core input that determines whether aluminum output can be sustained.

Demand is strongest in regions with large aluminum smelting capacity. China, the Middle East, India, Russia and Canada remain key demand centers because smelters require large and uninterrupted alumina supply. Import-dependent smelters place high value on contract reliability, shipping schedules and product consistency. Refinery disruptions can tighten regional balances quickly because smelters cannot easily pause operations without significant cost.

Supply security is becoming more important as refinery closures, bauxite quality issues, caustic soda costs and energy constraints affect alumina availability. Kwinana’s permanent closure shows how aging assets and grade challenges can remove capacity from the market. Smelter-grade alumina will remain volume-dominant, but customer attention is moving toward stable supply, refinery cost position and low-carbon sourcing.

High Purity Alumina is Gaining Value in Battery and Electronics Applications

High purity alumina is gaining stronger strategic value because batteries, LEDs, semiconductor ceramics, sapphire substrates and advanced electronics require alumina grades with much tighter impurity control than conventional products. Buyers need purity levels, particle control and surface chemistry that support downstream processing and device reliability. This creates a market where qualification, not only production volume, determines supplier competitiveness.

Battery separator coating is one of the most important emerging applications. HPA can improve separator thermal stability and support safety performance in lithium-ion cells. Cell manufacturers and separator producers need consistent material because particle variation can affect coating uniformity, porosity and battery performance. As battery production scales, suppliers that can provide stable quality and customer-specific grades will be better positioned.

Semiconductor and electronics demand is also strengthening. High purity alumina can be used in thermal-management materials, ceramic parts and components exposed to demanding processing environments. Alpha HPA’s supply agreement for its Gladstone project reflects how advanced electronics customers are becoming more involved in alumina sourcing. High purity alumina is smaller than smelter-grade alumina but offers a higher-value growth route.

Calcined And Reactive Alumina Support Refractories and Technical Ceramics

Calcined and reactive alumina are important because they serve applications where thermal behavior, particle size, soda level and sintering response matter. Refractory producers use these grades in shaped and unshaped products for steel, cement, glass, petrochemical and non-ferrous metal processing. Technical ceramics use reactive and calcined grades where density, shrinkage, strength and wear resistance are critical.

Refractory demand is tied to heavy industry, but product requirements are becoming more demanding. Steel plants, cement kilns and glass furnaces require materials that can withstand thermal shock, corrosion and abrasion. Alumina suppliers serving these customers must offer stable chemistry and technical data because refractory formulation depends on consistency across batches.

Technical ceramics provide a higher-growth and higher-margin opportunity. Wear-resistant ceramics, electronic ceramics, kiln furniture and structural ceramics require alumina grades that behave predictably during forming and firing. Suppliers that combine calcination, milling, classification and application testing can gain stronger customer retention. This part of the market is less exposed to aluminum price cycles and more tied to manufacturing quality requirements.

Fused Alumina Remains Important in Abrasives and High-Performance Refractories

Fused alumina serves abrasive, blasting, grinding and refractory applications where hardness, toughness and thermal stability are required. Brown fused alumina is widely used in bonded abrasives, coated abrasives and blasting media, while white fused alumina is used where higher purity and sharper cutting behavior are needed. Demand is linked to metalworking, surface preparation, foundries and refractory production.

Abrasive manufacturers evaluate fused alumina through grain toughness, friability, purity, sizing and consistency. Cost matters, but tool performance and durability are equally important in demanding industrial applications. Suppliers with strong sizing control and stable fusion operations can maintain higher customer trust.

High-performance refractories also use fused alumina where thermal and mechanical stress is high. Steel, cement and petrochemical operations require refractory materials that protect furnaces and process equipment. Demand may fluctuate with industrial production, but fused alumina remains difficult to replace in many wear and heat-intensive applications.

Market Segmentation

- By Product

- Smelter Grade Alumina

- Standard Smelter Grade Alumina

- Sandy Alumina

- Floury Alumina

- Chemical Grade Alumina

- Hydrated Alumina

- Activated Alumina

- Alumina Trihydrate

- Calcined Alumina

- Low Soda Calcined Alumina

- Medium Soda Calcined Alumina

- Reactive Alumina

- High Purity Alumina

- 4N Alumina

- 5N Alumina

- 6N Alumina

- Tabular Alumina

- Fused Alumina

- Brown Fused Alumina

- White Fused Alumina

- Specialty Alumina

- Polishing Alumina

- Ceramic Alumina

- Catalyst Grade Alumina

- Flame Retardant Grade Alumina

- Others

- Smelter Grade Alumina

- By Manufacturing Route

- Bayer Process

- Sintering Process

- Combined Bayer Sintering Process

- Alkoxide Hydrolysis Route

- Hydrochloric Acid Leaching Route

- Others

- By Application

- Aluminum Smelting

- Refractories

- Shaped Refractories

- Unshaped Refractories

- Technical Ceramics

- Electronic Ceramics

- Wear Resistant Ceramics

- Structural Ceramics

- Abrasives

- Grinding Wheels

- Blasting Media

- Coated Abrasives

- Catalyst and Catalyst Supports

- Flame Retardants

- Polishing Compounds

- Battery Materials

- Battery Separator Coatings

- Cathode Material Support Uses

- Glass and Coatings

- Water Treatment

- Others

- By End-User

- Primary Aluminum Producers

- Refractory Manufacturers

- Ceramic Manufacturers

- Abrasive Manufacturers

- Chemical Companies

- Battery Material Producers

- Electronics Manufacturers

- Glass Manufacturers

- Water Treatment Companies

- Others

Geographical Penetration

U.S. Alumina Market Landscape

The U.S. alumina market is influenced by aluminum smelting, specialty ceramics, abrasives, catalysts and battery materials. Domestic smelting capacity is smaller than Asia, but specialty alumina demand remains important due to industrial and advanced material applications.

U.S. buyers are sensitive to import dependence and supply reliability. Alumina used in specialty applications often requires consistent quality and technical documentation. This supports demand for trusted suppliers with application support.

Battery and electronics applications can create higher-value growth. High-purity alumina can be used in separators, ceramics and electronic substrates. Adoption depends on purity, particle control and customer qualification.

India Alumina Market Landscape

India is one of the strongest growth markets because aluminum demand is rising across power, transport, construction and packaging. Integrated producers are investing in bauxite mining, alumina refining and aluminum smelting to improve value-chain security.

Domestic alumina demand is tied to smelter expansion and downstream aluminum use. India’s growing industrial base supports long-term aluminum consumption. Alumina suppliers with low-cost bauxite and reliable energy access are better positioned.

Specialty alumina demand is also emerging from refractories, ceramics and battery materials. Growth will be gradual but attractive as India expands advanced manufacturing and energy storage supply chains.

Japan Alumina Market Outlook

Japan is a high-value alumina market despite limited primary aluminum production. Demand is focused on specialty alumina used in ceramics, electronics, polishing, catalysts and high-performance industrial materials.

Japanese customers prioritize purity, consistency and particle control. Suppliers need strong quality systems and technical support. Price matters but performance reliability is often more important in advanced applications.

Battery and semiconductor-related uses create additional opportunity. Japan’s advanced materials industry can support demand for high-purity alumina where product consistency is critical.

Competitive Landscape

- Competition is split between integrated bauxite and alumina producers, standalone alumina refinery, specialty alumina suppliers, high purity alumina developers and fused alumina producers. Smelter-grade alumina suppliers compete on refinery scale, bauxite security, energy cost, caustic efficiency, logistics and contract reliability. Specialty suppliers compete on purity, soda content, particle control, phase composition and technical support.

- Integrated producers such as Alcoa, Rio Tinto, South32, Chalco, Hindalco, Norsk Hydro and Emirates Global Aluminum have stronger positions in smelter-grade alumina because they control bauxite, refining assets or downstream aluminum demand. Refinery portfolio decisions, closures, energy arrangements and environmental approvals can directly affect market balance. These companies are evaluated by customers on supply stability as much as headline capacity.

- Specialty alumina companies such as Almatis, Alteo, Nabaltec, Sumitomo Chemical and Huber Advanced Materials compete differently. Their market strength comes from engineered products for refractories, ceramics, flame retardants, polishing, catalysts and electronics. Customers in these applications are less likely to switch suppliers quickly because formulation, qualification and performance history matter.

- High purity alumina is becoming a more distinct competitive arena. Producers serving battery separators, semiconductors and sapphire applications must prove purity, consistency, particle control and customer qualification. Competitive benchmarking should track technical grade depth, qualification status, production scale, regional customer access, low-carbon positioning and raw material security.

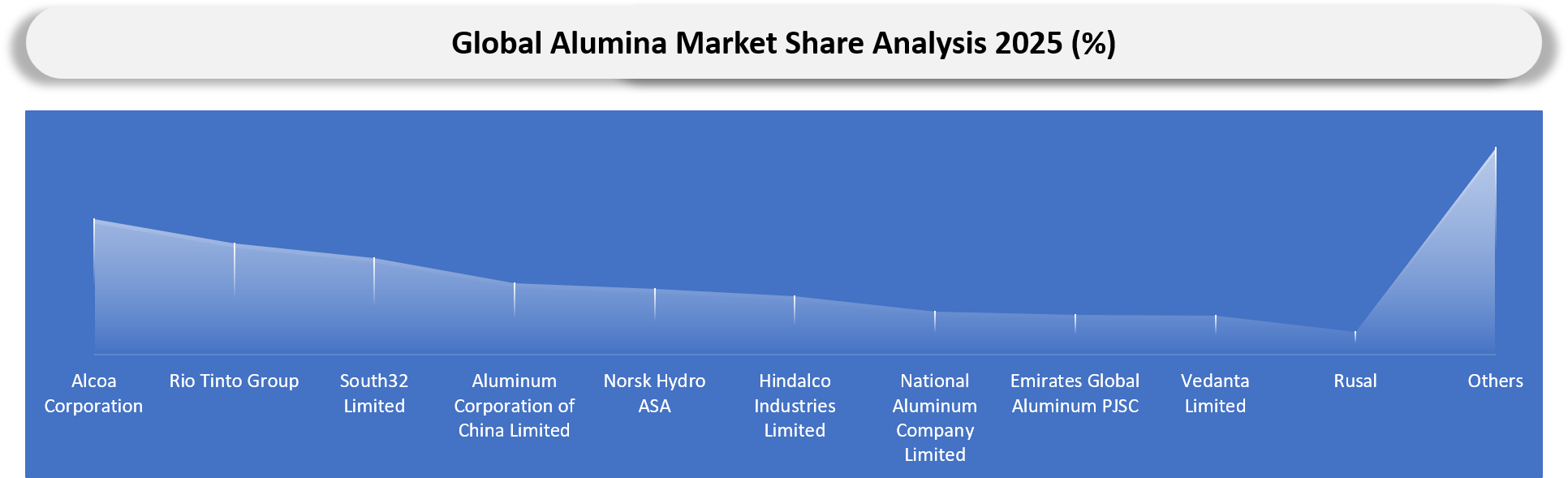

Key Companies

- Alcoa Corporation

- Rio Tinto Group

- South32 Limited

- Aluminum Corporation of China Limited

- Norsk Hydro ASA

- Hindalco Industries Limited

- National Aluminum Company Limited

- Emirates Global Aluminum PJSC

- Vedanta Limited

- Rusal

- Kaiser Aluminum Corporation

- Almatis GmbH

- Alteo Holding

- Nabaltec AG

- Sumitomo Chemical Co., Ltd.

- Sasol Limited

- Huber Advanced Materials

- Nippon Light Metal Holdings Company, Ltd.

- Zibo Honghe Chemical Co., Ltd.

- Shandong Aluminum Corporation

Alcoa Corporation

Alcoa Corporation is one of the most relevant alumina producers because it has a long-standing position in bauxite mining, alumina refining and aluminum smelting. The company’s alumina position is supported by integrated operations and a global customer base. Its refinery decisions are closely watched because capacity closures, restarts or efficiency programs can influence regional supply.

Rio Tinto Group remains important because its aluminum business includes bauxite, alumina and aluminum assets. The company’s advantage comes from raw material access, mining scale and integrated aluminum value-chain exposure. Rio Tinto is especially relevant in premium supply discussions where customers evaluate upstream security and ESG performance.

South32 Limited is relevant through Worsley Alumina and its broader aluminum value-chain exposure. Worsley is one of the important alumina operations serving global smelter customers. South32’s performance depends on refinery reliability, bauxite access, environmental approvals and operating-cost discipline.

Major Pain Points

- Bauxite residue storage creates long-term environmental liabilities and raises permitting complexity for alumina refineries.

- Declining bauxite grades can increase caustic consumption, residue volumes and refinery operating cost.

- Energy-intensive refining and calcination processes expose producers to power and fuel price volatility.

- Smelter customers need consistent chemistry and reliable shipping because potline operations depend on continuous alumina feed.

- Specialty alumina customers require tight particle size, low impurity levels and long qualification timelines that limit supplier switching.

- High purity alumina producers face capital intensity, customer qualification barriers and strict quality expectations from battery and electronics buyers.

- Refinery closures or curtailments can tighten regional supply quickly because alumina cannot be replaced by alternative raw materials in aluminum smelting.

- Community opposition around bauxite mining, forest clearing, water catchments and residue storage can delay mine approvals and refinery feedstock plans.

- Caustic soda price movement can materially affect refinery margins, especially for producers processing lower-quality bauxite.

- Low-carbon alumina demand is rising, but buyers still need transparent emissions data and credible chain-of-custody systems before paying premiums.

Recent Developments

- February 2026: Alcoa received an 18-month national interest exemption linked to its Western Australia bauxite mining operations while agreeing to an enforceable environmental undertaking of AUD 55 million, keeping bauxite access and alumina refinery feedstock continuity central to the company’s Western Australia operating strategy.

- October 2025: The Alcoa and Sojitz Gallium Recovery Project in Wagerup, Western Australia secured up to USD 200 million in concessional equity finance under the U.S. and Australia critical minerals framework, positioning alumina refinery by-products as a strategic route for gallium supply.

- September 2025: Alcoa confirmed the permanent closure of the Kwinana alumina refinery in Western Australia, reducing its global consolidated refining capacity and shifting operational focus toward Wagerup and Pinjarra while creating long-term site remediation and residue management obligations.

- March 2025: Rio Tinto signed 20-year renewable power and battery agreements with Edify Energy for its Gladstone aluminum operations, supporting lower-carbon electricity supply for assets linked to the Boyne smelter and Yarwun alumina refinery.

- January 2025: Alpha HPA signed a letter of intent with a Japanese electronics manufacturer for high purity alumina supply from its Gladstone HPA First Project, supporting demand from semiconductor thermal-management and advanced electronics applications.

Analyst View And Opinion

- Smelter-grade alumina will remain the largest revenue pool because primary aluminum production depends on continuous alumina feedstock. Growth will follow aluminum demand in transportation, packaging, construction, electrical infrastructure and renewable energy equipment.

- Specialty alumina will grow faster than smelter-grade alumina because ceramics, refractories, batteries, catalysts, polishing and electronics require engineered grades. Margin opportunities will be stronger where suppliers can offer application-specific chemistry and particle control.

- High purity alumina will remain one of the most strategically important growth pockets. Battery separator coatings, semiconductor thermal-management uses and sapphire-related applications create demand that is less tied to aluminum metal cycles.

- Alumina refinery competitiveness will increasingly depend on bauxite quality, caustic efficiency, energy sourcing, residue management and logistics. Refinery age and feedstock access will decide which assets remain competitive during price downturns.

- Environmental approval risk is becoming a core supply-chain factor. Bauxite mining and residue storage can influence refinery continuity, especially in regions where operations intersect with forests, water catchments or nearby communities.

- China will remain the largest alumina demand center, but import opportunities will continue when domestic refinery economics, environmental restrictions or bauxite availability tighten supply.

- India offers long-term demand growth because aluminum consumption is rising and domestic smelters need secure alumina supply. Refinery expansion will depend on bauxite access, land approvals and energy cost.

- Specialty alumina suppliers will become more important in client procurement strategies because the market is shifting from tonnage-based supply toward performance-qualified materials in advanced manufacturing.

- Low-carbon alumina will move from a branding claim toward a procurement metric as aluminum buyers evaluate upstream emissions. Producers with renewable energy access and credible emissions data will have stronger positioning.

- Residue reuse remains a long-term opportunity but not a quick solution. Construction materials, cement additives and metal recovery routes will need scale, regulatory acceptance and consistent economics before materially reducing industry burden.

Target Audience

| Industry | Who Should Buy This Report? | Reason To Buy This Report |

| Aluminum Producers | Smelter Procurement Teams | Track alumina supply, pricing and regional trade flows |

| Alumina Refiners | Strategy Teams | Benchmark refining economics and specialty-grade opportunities |

| Battery Materials | Product Managers | Assess high-purity alumina demand |

| Ceramics and Refractories | Procurement Teams | Evaluate calcined and specialty alumina supply |

| Investors | Metals and Mining Analysts | Understand alumina value-chain risks and growth pockets |

| Consulting Firms | Metals Practice Teams | Support market sizing, supplier benchmarking and opportunity mapping |

What DataM Intelligence Uniquely Provides

- DataM Intelligence provides a split view of smelter-grade alumina, specialty alumina, calcined alumina, high purity alumina, fused alumina and alumina hydrate so clients do not rely on a single blended alumina number that hides product-level economics.

- DataM Intelligence maps alumina demand through aluminum smelter operations, refractories, ceramics, abrasives, catalysts, flame retardants, polishing, water treatment and battery material applications, helping client’s separate volume-led demand from margin-led opportunities.

- DataM Intelligence builds refinery-level supply understanding by evaluating bauxite source, refinery capacity, operating status, closure risk, energy exposure, residue management and logistics access. This helps procurement teams understand whether capacity is reliable or vulnerable.

- DataM Intelligence tracks specialty alumina qualification barriers across ceramics, refractories, battery separator coatings, electronic ceramics and polishing applications. This supports supplier screening where customer switching is slow and technical validation matters.

- DataM Intelligence provides import-export intelligence using HS 281820, HS 281810 and HS 281830 with country-level interpretation for smelter-grade alumina, artificial corundum and aluminum hydroxide flows.

- DataM Intelligence supports procurement teams with cost-driver analysis covering bauxite quality, caustic soda, energy, freight, calcination cost, particle-size control, purity requirements and application-specific price premiums.

- DataM Intelligence includes environmental and social risk mapping around bauxite mining, residue storage, refinery emissions, water use and community opposition, which are increasingly important for long-term supply reliability.

- DataM Intelligence helps clients benchmark companies across bulk refining strength and specialty product capability, including integrated aluminum producers, specialty alumina suppliers and high purity alumina developers.

Related Reports

The alumina industry is closely connected to the broader aluminum value chain, industrial minerals sector, advanced materials technologies, and battery manufacturing ecosystem. As demand grows from automotive, aerospace, construction, electronics, and clean energy applications, understanding adjacent markets becomes increasingly important for identifying investment opportunities and supply chain trends. Explore the following related reports for deeper insights into the industries driving future alumina demand and technological innovation.

Aluminum Market

Alumina is the primary raw material used in aluminum production, making the aluminum market one of the most closely connected industries. Growing demand from automotive, aerospace, construction, and packaging sectors continues to drive alumina consumption globally.

Bauxite Market

Bauxite serves as the primary feedstock for alumina refining. Understanding bauxite supply dynamics, mining investments, and regional production trends is critical for evaluating future alumina market opportunities and supply chain stability.

Refractories Market

Calcined alumina is widely used in refractory materials due to its high-temperature resistance and durability. Growth in steel, cement, glass, and industrial manufacturing industries continues to support demand for alumina-based refractory products.

Advanced Materials Market

High-purity alumina is becoming increasingly important in advanced materials applications, including LEDs, semiconductors, sapphire substrates, and electronic components. The growing demand for high-performance materials is creating new growth opportunities across the alumina value chain.

Electric Vehicle Battery Materials Market

High-purity alumina is increasingly used in lithium-ion battery separators to improve thermal stability, safety, and battery performance. The rapid growth of electric vehicles is creating significant long-term demand for specialty alumina products.

Mining Chemicals Market

Alumina production relies heavily on various mining and processing chemicals throughout the refining process. Developments in mining operations, sustainability initiatives, and mineral processing technologies directly influence alumina production economics.