Addiction Treatment Market Overview

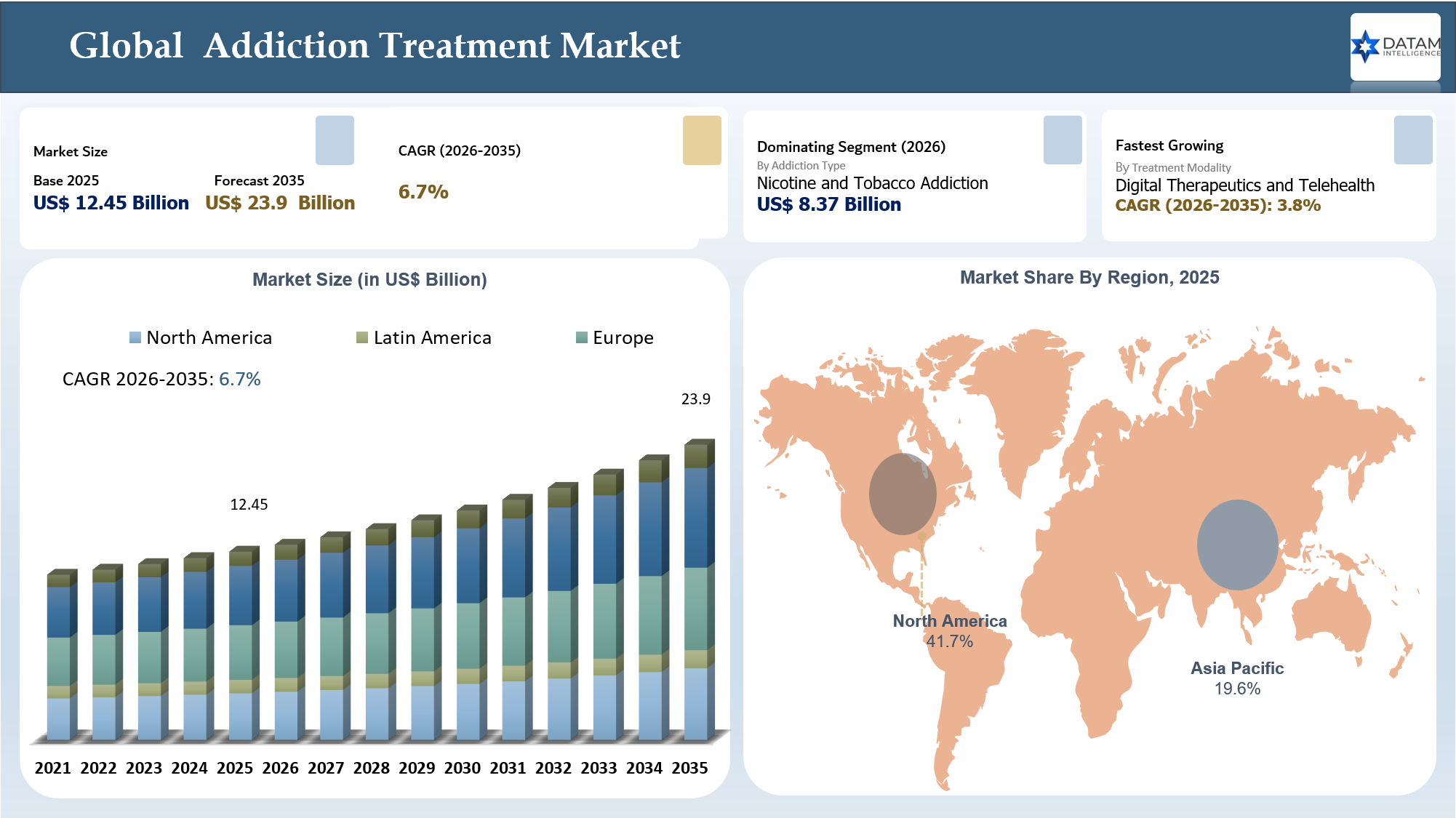

The global addiction treatment market stood at US$ 12.45 billion in 2025 and is expected to reach US$ 23.9 billion by 2035, growing with a CAGR of 6.7% during the forecast period 2026-2035.

The addiction treatment market is shifting from episodic detoxification and rehabilitation toward integrated, evidence-based recovery systems, driven by rising substance use disorder burden, overdose prevention needs and growing recognition of addiction as a chronic condition. In the U.S., SAMHSA reported that 48.4 million people aged 12 or older, or 16.8% of the population, had a substance use disorder in 2024, highlighting the scale of treatment need across alcohol, opioid, nicotine and polysubstance addiction.

Demand is increasing for medication-assisted treatment, behavioral therapy, counseling, relapse prevention, harm reduction, digital therapeutics and telehealth-based recovery support. Although U.S. drug overdose deaths declined by 26.2% in 2024, CDC still reported 79,384 overdose deaths, keeping opioid treatment, naloxone access and long-term recovery programs as public health priorities. The market is also gaining momentum from large nicotine dependence treatment demand, as WHO estimates around 1.3 billion tobacco users globally, supporting continued adoption of nicotine replacement therapies and smoking cessation programs. Overall, market growth is being shaped by integrated care models, digital access, public health funding and stronger focus on measurable recovery outcomes.

Key Takeaways

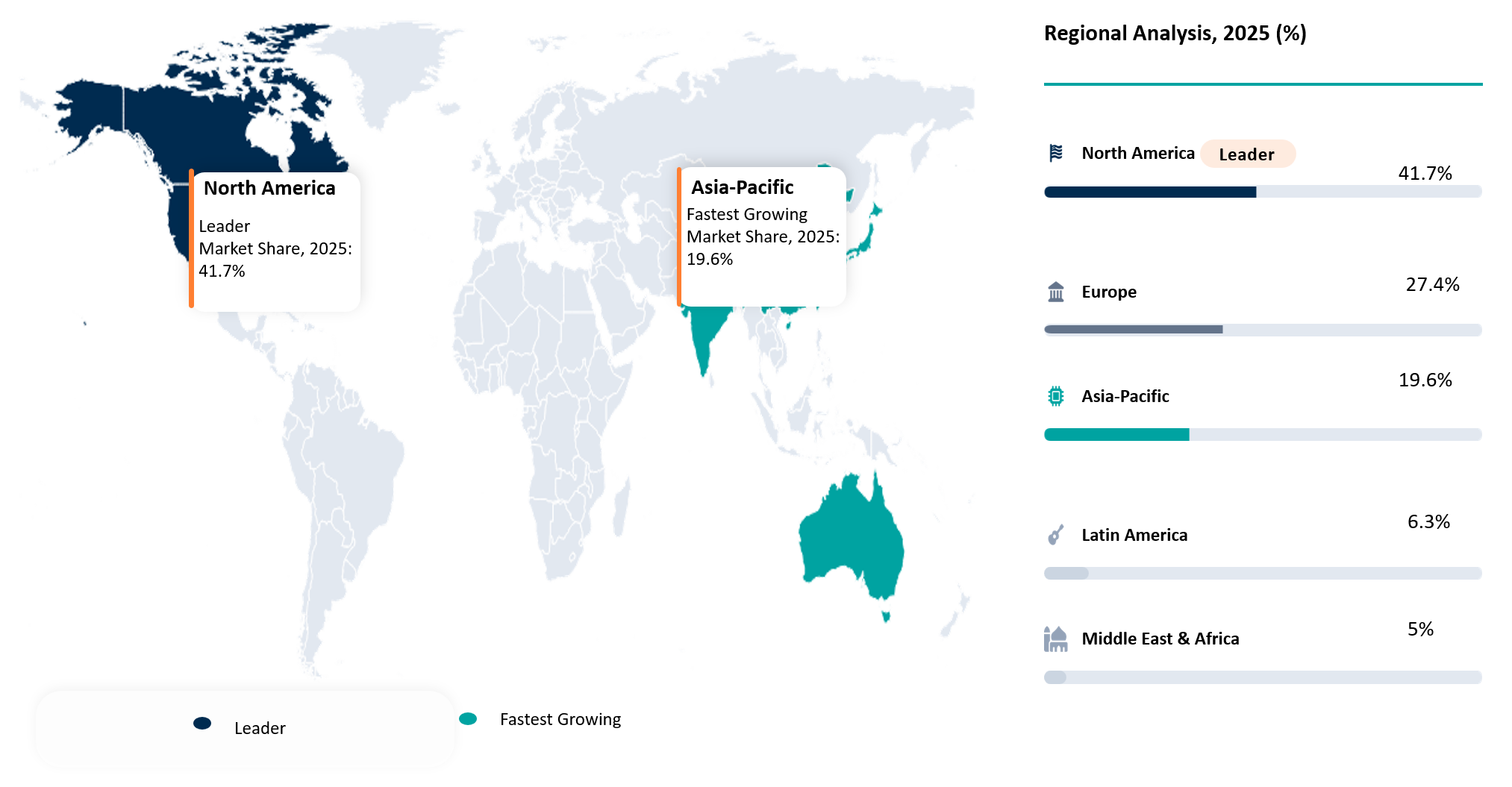

- North America held the highest market share at an estimated 41.7% in 2025, supported by strong medication-assisted treatment adoption, opioid treatment programs, naloxone access, reimbursement support and established rehabilitation infrastructure.

- Europe remained the second-largest region with an estimated 27.4% share in 2025, driven by public healthcare funding, alcohol dependence treatment programs, smoking cessation initiatives and integrated mental health services.

- Asia Pacific accounted for an estimated 19.6% share in 2025 and is expected to be the fastest-growing region, supported by rising nicotine cessation demand, improving behavioral health infrastructure and expanding digital addiction care adoption.

- Nicotine and Tobacco Addiction was the largest addiction type segment in 2025, accounting for around 32.8% share, supported by high tobacco-user prevalence, OTC nicotine replacement therapy access and retail pharmacy penetration.

- Medication-Assisted Treatment dominated the treatment modality segment in 2025 with an estimated 38.5% share, driven by increasing use of buprenorphine, methadone, naltrexone and nicotine dependence therapies.

- Opioid partial agonists led the medication class segment with approximately 29.4% share, supported by strong adoption of buprenorphine-based therapies for opioid use disorder.

- Outpatient Clinics were the largest care delivery setting in 2025 with nearly 34.6% share, supported by recurring counseling visits, medication maintenance, lower treatment cost and better patient accessibility.

- Digital Therapeutics and Telehealth are expected to be the fastest-growing treatment modality during 2026–2035, driven by remote counseling, app-based relapse prevention, AI-enabled monitoring and hybrid care models.

- Buyers are increasingly shifting from standalone detoxification and rehabilitation services toward integrated recovery models combining medication-assisted treatment, behavioral therapy, digital monitoring, harm reduction and long-term aftercare.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 12.45 Billion | |

| 2035 Projected Market Size | US$ 23.9 Billion | |

| CAGR (2026-2035) | 6.7% | |

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Addiction Type | Alcohol Use Disorder, Opioid Use Disorder, Nicotine and Tobacco Addiction, Cannabis Use Disorder, Stimulant Use Disorder, Prescription Drug Addiction, Behavioral Addiction, Polysubstance Use Disorder and Others | |

| By Treatment Modality | Medication Assisted Treatment, Detoxification and Withdrawal Management, Behavioral Therapy and Counseling, Residential Rehabilitation, Outpatient Rehabilitation, Harm Reduction Programs, Digital Therapeutics and Telehealth and Recovery Management and Aftercare | |

| By Medication Class | Opioid Agonists, Opioid Partial Agonists, Opioid Antagonists, Alcohol Dependence Medications, Nicotine Replacement Therapies, Smoking Cessation Drugs and Adjunctive Psychiatric Medications | |

| By Care Delivery Setting | Hospitals, Specialty Addiction Treatment Centers, Residential Rehabilitation Centers, Outpatient Clinics, Community Health Centers, Digital Care Platforms and Correctional Facilities | |

| By Distribution Channel | Hospital Pharmacies, Retail Pharmacies, Online Pharmacies and Public Health and Government Supply Channels | |

| By End User | Individual Patients, Healthcare Providers, Government and Public Health Agencies, Employers and Workplace Wellness Programs, Correctional Health Programs and Community-Based Organizations | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

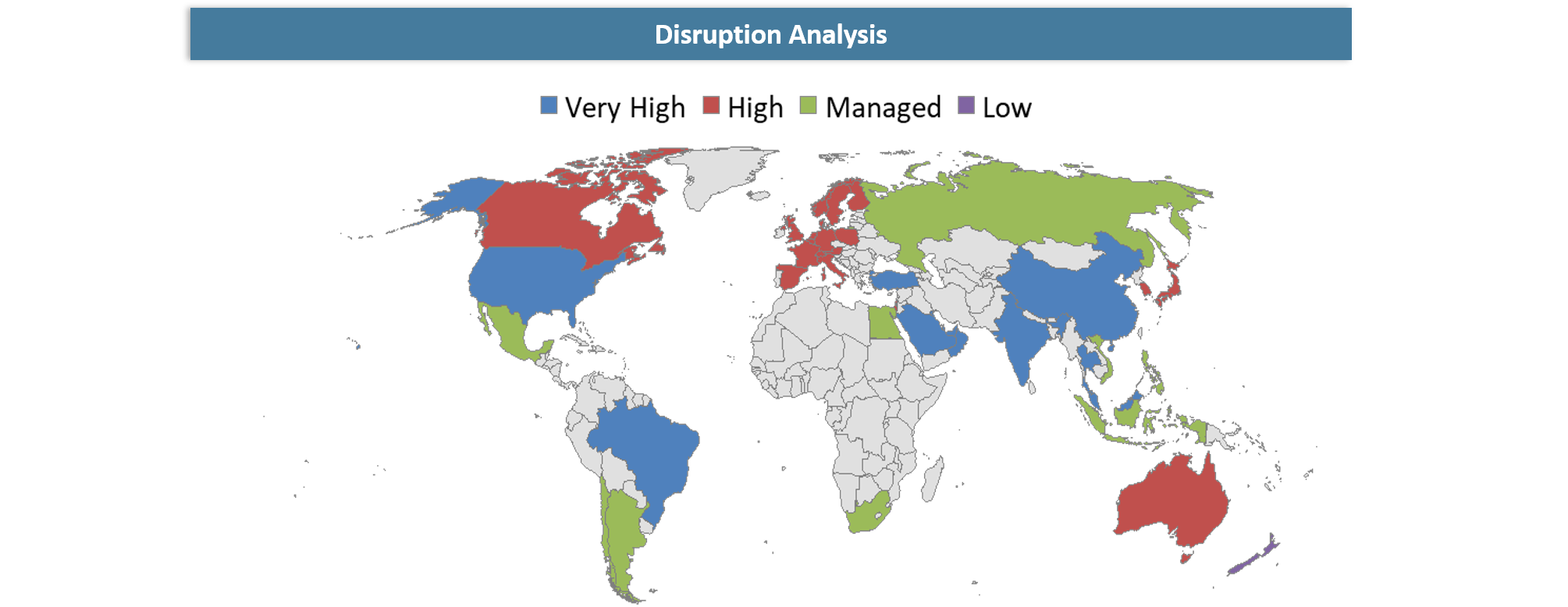

Disruption Analysis

Integrated Recovery Models Are Disrupting Traditional Addiction Treatment Pathways

The market for addiction treatment is being revolutionized by the trend from episodic rehabilitation to sustained, scientifically supported recovery management. The development of medication-assisted treatments, long-acting injections, nicotine replacements, overdose rescue medications and digital therapeutics represents a disruption to traditional rehabilitation models that rely on behavioral interventions, as these advancements help with patient adherence, access and measured benefits. Regulatory changes such as increased approval based on one successful pivotal study plus confirmatory data could help streamline the process of developing addiction treatments where recruiting subjects and monitoring relapse prove challenging. Telemedicine is another avenue through which access can be expanded outside hospital and rehabilitation facilities to offer virtual counseling, digital relapse management and employee substance abuse management. However, stigmatization, inadequate payment structure, a lack of addiction professionals and high relapse rates still pose a challenge to innovation. Organizations capable of delivering solutions that include pharmacotherapy, behavior modification and digital monitoring along with post-treatment support programs have a greater chance of succeeding than those providing only detox or rehabilitation services.

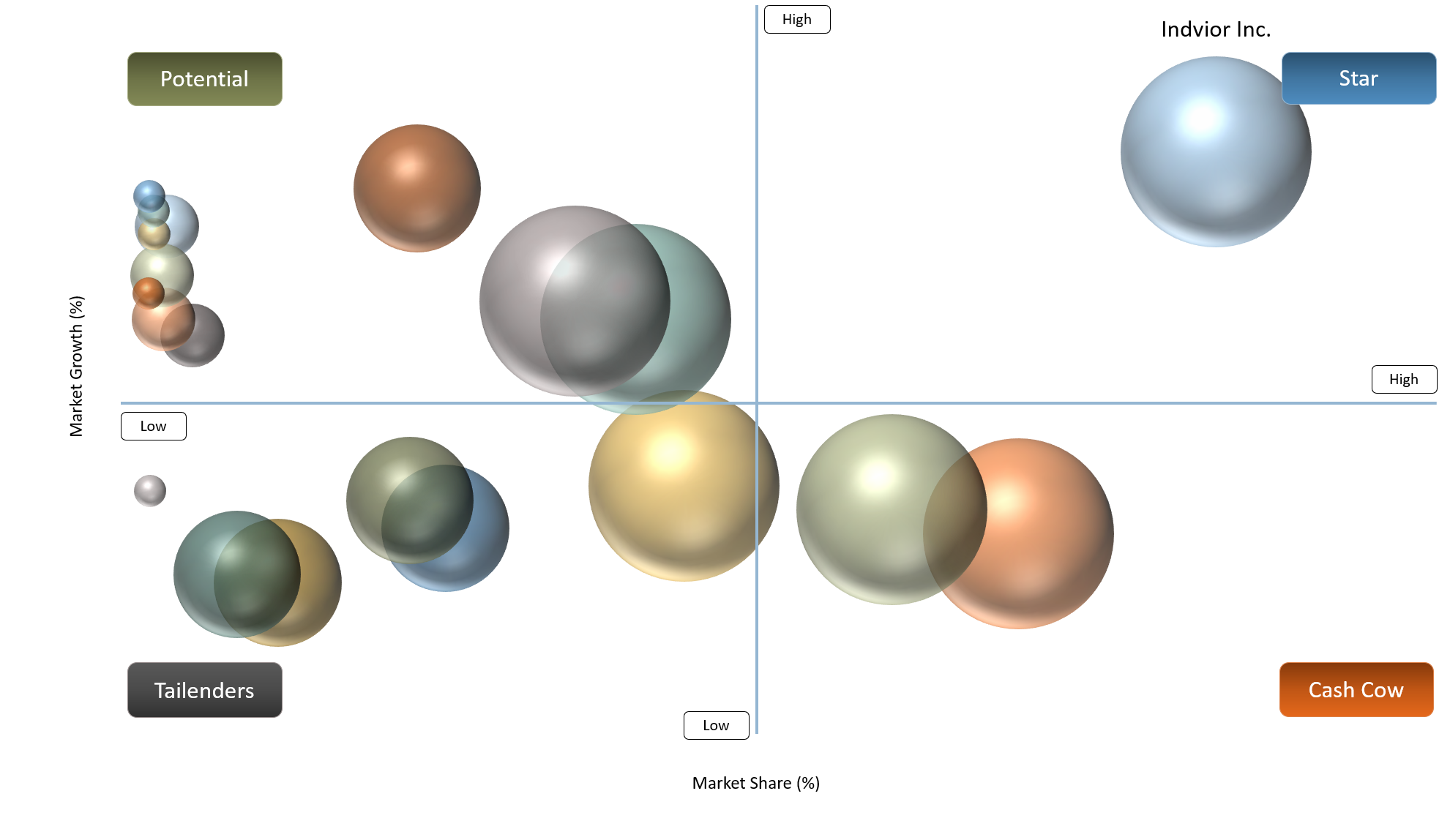

BCG Matrix: Company Evaluation

The Addiction Treatment Market Stars comprise of Indivior Inc., Alkermes plc, Camurus AB, Braeburn Inc. and Orexo AB. This is because they align highly with the high-growth addiction treatments such as opioid use disorder, alcohol dependence, medication-assisted treatment, long-acting injectable therapy and relapse prevention therapies. Their portfolios have more focus and higher clinical relevance in terms of addiction treatments. The Cash Cows in this market are Teva Pharmaceutical Industries Ltd., Viatris Inc., Hikma Pharmaceuticals PLC, Kenvue Inc., Dr. Reddy’s Laboratories Ltd., Perrigo Company plc and Cipla Ltd. They are backed by their existing portfolio of generics for addictions, nicotine replacement therapy, smoking cessation products, naloxone products, pharmacy availability and repeated treatment demand.

Question Marks will comprise of Emergent BioSolutions Inc. because their growth potential in addiction is heavily linked to the demand for the overdose reversal drugs, government purchases and access to naloxone program. Acadia Healthcare Company Inc. and BayMark Health Services are service-focused companies that should not be categorized among product innovation companies. This is due to their main focus being on offering addiction treatments through rehabilitation centers, outpatient programs, opioid treatment facilities and medication-assisted treatment.

Market Dynamics

Rising Burden of Substance Use Disorders Is Increasing the Need for Structured Treatment Pathways

The increasing prevalence of alcohol use disorder, opioid use disorder, nicotine dependence, and substance abuse disorders is creating high demands for structured treatment approaches. There is increasing understanding within healthcare organizations that addiction is not only a behavioral problem but a relapsing one, necessitating the move from isolated approaches such as detoxification to comprehensive solutions. This will facilitate the wider use of medication therapy, behavioral treatment, counseling, rehabilitation, and other forms of treatment and support services. The growing complexities of cases involving addictions – cases of patients with dual diagnosis, psychological complications and frequent episodes of relapse – also make clinical treatment necessary. In addition, the dangers of opioid overdose, lost worker productivity, burden on families and society, and public health expenses are making governments and corporations consider scalable treatment plans. These conditions are contributing to an increased relevance of providers who offer evidence-based and multi-disciplinary solutions to addiction.

Social Stigma and Low Treatment-Seeking Behavior Continue to Restrict Patient Enrollment

Stigma continues to be among the biggest barriers in the Addiction Treatment Market as people tend to avoid receiving treatment due to the fear of being stigmatized, pressures from families and employers, and social rejection. In many societies, addiction continues to be perceived as either a moral or behavioral failure rather than a chronic illness; therefore, early detection and engagement in treatment programs are quite difficult. This is even more problematic in cases where the patient suffers from conditions such as alcohol use disorder, opioid use disorder, tobacco dependence, and polysubstance abuse because in such situations early intervention can prevent overdoses and other complications. The low seeking of treatment further restricts patient access to hospitals, rehabilitation centers, clinics, and even online treatment services. Besides, lack of knowledge about the disease, privacy concerns, and skepticism towards rehabilitation programs also act as barriers in enrolling individuals in treatment programs.

Segmentation Analysis

The global addiction treatment market is segmented based on addiction type, treatment modality, medication class, care delivery setting, distribution channel, end user and region.

Nicotine and Tobacco Addiction Dominates Treatment Demand Due to Large User Base and Wider OTC Access

Nicotine and tobacco addiction has the greatest potential to dominate the addiction treatment market in terms of addiction type, as it enjoys the highest addressable market size, wide over-the-counter distribution, and deep penetration in retail pharmacies. According to the WHO, there are about 1.3 billion people who use tobacco globally, with nearly 80% residing in low- or middle-income countries. The segment will be driven by recurring sales of nicotine gums, patches, lozenges, prescription stop smoking medications, and quit smoking programs. In comparison with opioid addiction and alcohol dependency, nicotine addiction treatments enjoy less stigmatization, greater consumer reach, and higher engagement among individuals seeking self-care through pharmacies and via online platforms. Nonetheless, the opioid addiction treatment segment will continue to be the most strategic, high-intensity focus area, as it is influenced by drug overdose prevention measures, evidence-based treatment, and medication-assisted treatment (MAT). Buprenorphine, methadone, and naltrexone have been identified by FDA as medications to treat opioid use disorder.

Geographical Penetration

North America Dominates Due to Strong Treatment Infrastructure and Public Health Funding

North America is at the forefront in the addiction treatment market due to the high prevalence of substance use disorders, a well-established system of medication-assisted treatments, greater availability of insurance coverage, and public health financing. In the U.S., based on the 2024 NSDUH survey from the SAMHSA report, about 48.4 million adults aged 12 years or above, accounting for 16.8% of the total population, had suffered from substance use disorders, pointing to a large pool of individuals requiring treatment. Additionally, there is high demand for opioids, overdose reversal solutions, and relapse prevention programs. Although overdose deaths have reduced by about 27%, the figure is estimated to stand at about 80,391 in 2024. Therefore, the field remains crucial in the healthcare sector. The opportunities in the region are driven by increased access to products such as naloxone, buprenorphine, methadone, naltrexone, residential rehab services, outpatient centers, and telemedicine for addiction treatment. Companies like Indivior, Alkermes, Emergent BioSolutions, Acadia Healthcare, and BayMark also contribute to the leadership of North America.

U.S. Addiction Treatment Market Trends

The United States is a key player in the addiction treatment market due to the significant substance use disorder population, highly developed behavioral health system, and extensive adoption of medication-assisted therapy. According to data from SAMHSA's 2024 NSDUH report, 48.4 million individuals aged 12 or more, or 16.8% of the total population in the country, have a substance use disorder, thereby providing a huge patient base for opioid, alcohol, nicotine, and polysubstance addiction treatment services. Moreover, the country continues to maintain its focus on overdose prevention despite better mortality trends. CDC stated that there were 79,384 drug overdose deaths in 2024; however, the age-adjusted drug overdose death rate was 26.2% lower than in 2023. This indicates high demand for medications such as naloxone, buprenorphine, methadone, naltrexone, outpatient facilities, rehabilitation centers, and telehealth-based addiction treatments.

Japan Addiction Treatment Market Outlook

Japan is an example of a relatively controlled yet commercially meaningful Addiction Treatment Market characterized primarily by the treatment of nicotine and tobacco cessation and alcohol dependence and mental health-related rehabilitation. The market sees relatively low usage of illegal substances compared to the Western market, which means that the demand is less driven by opioids and more driven by smoking cessation treatments and alcohol interventions. The treatment of tobacco cessation continues to be one of the main drivers of the Japanese addiction treatment market due to an estimated 18.3 million smokers in 2024 among adults. Japan's policies aim to decrease the proportion of adult smokers to 12%, and thus, the current percentage stands at 14.6% of the total population. Additionally, it can be stated that the treatment of alcohol dependence is still lacking due to a relatively small number of cases receiving treatment.

Competitive Landscape

The addiction treatment market is moderately concentrated with competition driven by companies dealing with treatments for opioid use disorders, alcohol dependency therapy, nicotine replacement treatments, reversal of overdose drugs, and rehabilitation. Indvior Inc., Alkermes plc, Camurus AB, Braeburn Inc., and Orexo AB are well placed players in treatments for opioids addiction due to their portfolio that includes buprenorphine, naltrexone, and long-acting treatments. Additionally, Teva Pharmaceutical Industries Ltd., Viatris Inc., and Hikma Pharmaceuticals PLC enhance the competition with their addiction medicines, naloxone treatment, and wide range of pharmaceutical distribution. Emergent BioSolutions Inc. is an important player in harm reduction treatments via its opioid reversal treatments. In terms of nicotine addiction treatment, Kenvue Inc., Dr. Reddy’s Laboratories Ltd., Perrigo Company plc, and Cipla Ltd. drive the competitive rivalry through nicotine gums, patches, lozenges, and smoking cessation drugs. Service providers like Acadia Healthcare Company Inc. and BayMark Health Services offer competing rehabilitation centers and outpatient treatments.

Recent Developments

- February 2026: FDA moved toward a more flexible approval framework, positioning one adequate and well-controlled pivotal trial supported by confirmatory evidence as the new default approach for drug approvals. This may support faster development of addiction treatment drugs where recruitment, adherence and relapse tracking are challenging.

- February 2025: Indivior Inc. received FDA approval for label changes to SUBLOCADE, allowing rapid initiation after a single transmucosal buprenorphine dose and one-hour observation period. The update also added alternative injection sites such as abdomen, thigh, buttock and back of upper arm.

- January 2025: FDA approved JOURNAVX by Vertex Pharmaceuticals as a first-in-class non-opioid oral treatment for moderate to severe acute pain in adults. Although not an addiction treatment drug, it is relevant because non-opioid pain management can reduce reliance on opioid prescribing.

- December 2024: Orexo AB resolved ZUBSOLV U.S. patent litigation with Sun Pharmaceutical Industries. The agreement allows Sun to enter the U.S. market with generic versions of ZUBSOLV in September 2030, while ZUBSOLV remains protected by multiple patents with expirations from 2027 to 2032.

- November 2024: Indivior Inc. presented clinical data supporting rapid initiation with once-monthly SUBLOCADE and alternative injection-site administration, including thigh, upper arm and buttocks, strengthening its positioning in opioid use disorder treatment convenience.

- June 2024: Camurus AB announced publication of effectiveness data showing that weekly and monthly buprenorphine injections are effective in treating opioid dependence, including in individuals using fentanyl, supporting broader confidence in long-acting injectable treatment models.

AI Impact Analysis

AI technology is anticipated to have profound implications for the Addiction Treatment Market through advanced identification of risk factors, customized treatment programs, enhanced relapse prediction and patient engagement strategies. With the help of machine learning technology, an AI platform would be able to identify behavioral risks, digital biomarkers, prior use of prescribed medications, signs of psychological problems, and compliance issues that could lead to high risks of relapse and overdose. Such a solution would aid healthcare professionals and clinics in delivering more personalized services. Regarding medication-assisted therapy, artificial intelligence would allow patients' progress monitoring, timely alert for drug omission, telemedicine consultations, and retention improvements. Digital therapeutics companies and virtual counselors also leverage AI chatbots, automated screening services, and personalized programs to provide wider access to their products. For healthcare payers and corporate customers, AI would enable the risk assessment of patients and outcome monitoring of different therapy programs. Data protection, algorithm bias, lack of evidence, and trust issues are major obstacles.

White Space Opportunities

There is abundant white space in the Addiction Treatment Market in areas where existing models are fragmented or insufficiently developed. One such area of huge importance is stimulant use disorders because the current pharmacological therapies are not as numerous as those for opioids, alcohol, and nicotine addiction treatment. The white spaces also include the integration of care for substance abuse along with mental diseases; patients with this type of dual diagnosis are in great need. Another promising trend involves long-acting formulations of medications. As for digital addiction treatment, the market here is not yet saturated, and there is an abundance of white spaces to fill in. They may include counseling, artificial intelligence to prevent relapse, workplace addiction treatment, outpatient care, among other things. Women, adolescents, correctional healthcare, and post-release services are among other white space markets to explore.

DMI Opinion

According to DMI, the current state of affairs in the Addiction Treatment Market reveals that the market is transitioning from its current fragmented approach centered around rehabilitation to an integrated recovery ecosystem with high levels of evidence-based practice adoption. Commercial success will be achieved by organizations specializing in a combination of pharmacotherapy, behavioral therapy, electronic monitoring, relapse management, and aftercare services. Addictions to nicotine and tobacco products will generate volumes because of their wide availability in OTC markets and through retail pharmacies; however, opioid use disorder will retain its strategic significance due to risks of overdosing, government financing, and high demand for buprenorphine, methadone, naltrexone, and naloxone solutions. Digital therapeutics, telemedicine, and AI-powered relapse monitoring will increase adherence rates and improve treatment continuity in underserved communities. Nevertheless, stigma, non-adherence rates, staffing shortages, and limited reimbursement will still hinder treatment access.

Why This Report Matter in 2026?

Addiction Treatment Market report will be particularly significant in 2026 as addiction treatment will evolve from short-term rehabilitation to well-structured, evidence-based approaches. Increasing burden of substance use disorders, opioid overdose risks, smoking addiction, alcohol use disorder, polysubstance abuse, etc., have driven healthcare institutions, employers, and governments to fund their efforts for medication-assisted treatments, behavioral interventions, relapse prevention strategies, digital health, and harm reduction services.

Also, the market will gain strategic importance for several reasons in 2026 as far as regulations and innovations are concerned. The FDA’s decision on accepting one pivotal trial based on confirmatory evidence might benefit the drug development process for addiction drugs where it is challenging to recruit participants and monitor adherence and relapses. Simultaneously, AI, telemedicine, digital health interventions, and long-lasting drugs are revolutionizing the approach towards screening, monitoring, and retention of patients in treatment programs. This report can help businesses find high potential addiction types, approaches, delivery sites, drug types, regions, etc.

Why Choose DataM?

- End-to-End Addiction Treatment Ecosystem Assessment: DataM provides detailed insights across addiction types, medication-assisted treatment, behavioral therapy, detoxification, rehabilitation services, digital therapeutics, harm reduction programs and aftercare models, helping clients understand where treatment demand is actually scaling.

- Commercially Feasible Segmentation: Our segmentation is built around measurable revenue pools such as addiction type, treatment modality, medication class, care delivery setting, distribution channel, end user and region, reducing overlap and improving market-sizing accuracy.

- Competitive and Ecosystem Mapping: DataM tracks direct addiction treatment pharmaceutical companies, nicotine replacement therapy providers, overdose reversal product manufacturers, digital addiction care platforms, rehabilitation service providers and outpatient treatment networks to provide a clear competitive view.

- Treatment Pathway-Led Market Intelligence: The report evaluates demand across opioid use disorder, alcohol use disorder, nicotine dependence, polysubstance abuse, medication-assisted treatment, behavioral counseling, relapse prevention, telehealth-based treatment and long-term recovery management.

- Decision-Ready Strategic Add-Ons: Clients receive actionable insights such as BCG matrix, white space opportunities, AI impact analysis, disruption analysis, market dynamics, recent developments, regulatory shifts and treatment adoption priorities to support business planning.

- Client-Specific Growth Support: DataM helps companies identify high-growth addiction types, priority geographies, treatment gaps, partnership opportunities, target care settings, public health channels and commercialization strategies across the evolving Addiction Treatment Market..

Key Procurement Priorities and Buyer Evaluation Criteria

- Buyers in the Global Addiction Treatment Market are increasingly prioritizing providers that can deliver clinically validated treatment outcomes, improved recovery rates, relapse reduction and proven experience across opioid use disorder, alcohol use disorder, nicotine dependence and polysubstance abuse.

- Procurement decisions are shifting from standalone detoxification or rehabilitation services toward integrated recovery models that combine medication-assisted treatment, behavioral therapy, counseling, digital monitoring, harm reduction and long-term aftercare support.

- Hospitals, rehabilitation centers, public health agencies and correctional health programs are evaluating vendors based on access to approved medications such as buprenorphine, methadone, naltrexone, naloxone, acamprosate, disulfiram and nicotine replacement therapies.

- Buyers are also giving higher importance to telehealth capability, remote relapse monitoring, app-based recovery support, patient engagement tools, privacy protection and secure health data management to improve treatment continuity.

- Government agencies, employers, insurers and community-based organizations are assessing providers based on geographic reach, trained clinical workforce, reimbursement support, patient retention, crisis response capability and ability to deliver measurable outcomes across high-risk populations.