DataM Intelligence, a global market intelligence and consulting firm, has released its latest analysis of synchronous condenser projects, indicating that the Global Synchronous Condenser Market is experiencing strong momentum, driven by rising renewable energy integration, increasing grid stability requirements, and expanding transmission infrastructure investments. Siemens Energy remains the leading supplier by project volume, while the United States and Australia continue to represent the most active markets. Growing investments from transmission system operators and the emergence of large-scale projects exceeding 1,000 MVAr highlight the increasing importance of synchronous condensers in supporting system strength, inertia, voltage regulation, and grid reliability across modern power networks. Additionally, the increasing integration of synchronous condensers with battery energy storage systems (BESS), STATCOMs, and HVDC infrastructure is accelerating the adoption of advanced hybrid grid-stability solutions, strengthening long-term growth prospects for the market.

Increasing use of renewable energy, increased modernization efforts for transmission networks, the need for high system strength, and investments from transmission system operators are all factors that are contributing to the growth of the global synchronous condenser market. The need for maintaining reliability in the power grid, along with the retirement of existing power plants and increased use of renewable energy, is continuously boosting the market.

Request for Exclusive Sample: https://www.datamintelligence.com/download-sample/synchronous-condenser-market

Key Takeaways

- Siemens Energy emerged as the leading supplier, securing the highest number of identified contracts and commissioned projects, demonstrating a dominant position across North America, Europe, Australia, and Asia.

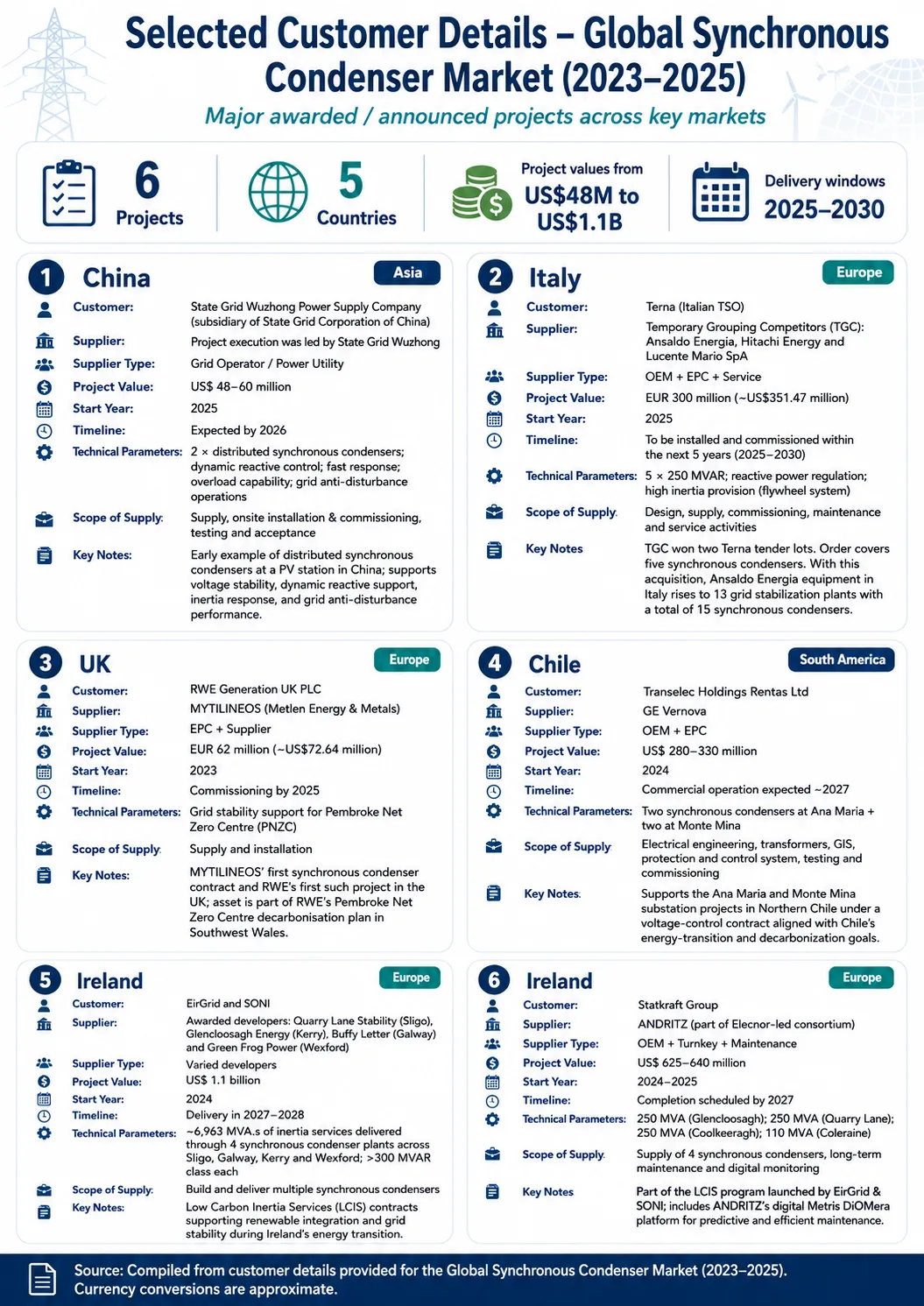

- One of the largest identified developments is Terna's project in Italy, comprising five 250 MVAr synchronous condensers totaling approximately 1,250 MVAr, awarded to a consortium including Ansaldo Energia and Hitachi Energy.

- ABB and GE Vernova ranked among the most active competitors, with GE Vernova notably participating in the Transelec project in Chile, which includes approximately 1,000 MVAr of synchronous condenser capacity.

- An emerging industry trend is the integration of synchronous condensers with Battery Energy Storage Systems (BESS), STATCOMs, and HVDC infrastructure, enabling advanced hybrid grid-stability solutions for renewable-dominated power systems.

- 81 synchronous condenser projects were identified in the database, highlighting strong global investment in grid stability, renewable energy integration, and transmission network modernization.

Major Synchronous Condenser Projects Worldwide

Rising Renewable Energy Integration Drives Demand for Grid Stability Solutions

With increasing penetration of renewable energy, growing investments in transmission networks and strengthened system strength needs, the need for synchronous condensers is becoming more and more prevalent on a global scale. Synchronous condensers are used to ensure the stability of the electric grids, provide physical inertia, voltage control, and increase short circuit strength when fossil fuel-based generation units are phased out.

Analysis of the 81 projects identified in this analysis, it is evident that there is a high level of investment activities in the United States, Australia, and Europe, with several utility-scale projects having installed more than 1,000 MVAr of synchronous condensers. The notable ones are the Terna project in Italy, which has five units of 250 MVAr each, totaling about 1,250 MVAr of synchronous condensers, and the Transelec project in Chile with about 1,000 MVAr of synchronous condenser capacity. With increasing integration of renewables into the grids, the use of synchronous condensers is coupled with BESS, STATCOMs, and HVDC systems.

Utility-Scale Synchronous Condenser Projects Gain Momentum Through Rising Grid Stability Requirements and Renewable Energy Integration

Larger-scale synchronous condenser installations are becoming one of the most promising growth segments in the global synchronous condenser market owing to rising usage of renewable energy, increased transmission grid construction and rising demand for system strength products. There is an increasing trend amongst utilities and transmission grid operators towards investments in large scale installations that can offer inertia, voltage control and fault current capability.

Analysis of the identified databases reveals that there are an increasing number of utility-scale projects having capacities exceeding 1,000 MVAr. Examples of these projects are the Transelec project in Chile, which has a capacity of around 1,000 MVAr of synchronous condensers. With such large-scale installations, along with the incorporation of these installations with BESS, STATCOMs, and HVDC systems, the importance of synchronous condensers is being strengthened. In 2025, Terna, which is the National Transmission System Operator in Italy, contracted out a large grid reinforcement program to a consortium that comprised both Ansaldo Energia and Hitachi Energy; this program was for five synchronous condensers with each having a rating of 250 MVAr, totaling up to 1,250 MVAr.

U.S. Maintains Leadership in the Synchronous Condenser Market Through Extensive Grid Modernization and Renewable Energy Integration Projects

The U.S. continues to maintain its leading position within the synchronous condenser market owing to significant investment in transmission infrastructure, rapid adoption of renewable power, and the growing need for grid stabilization. The North American region is favored by the large number of grid upgrade projects and investments in utilities, as well as the increasing need for inertia, voltage control, fault current injection, and system strength.

The USA is home to the greatest number of identified projects found in the database. Some examples of major projects include the Intermountain Power Project, among others, as well as various transmission systems strengthening projects that demonstrate growing installation of synchronous condensers in the region. In addition, continued investment by transmission systems operators and utilities, along with implementation of renewable energy sources and grid technologies, will only help to maintain U.S. dominance in the synchronous condenser market.

Competitive Landscape and Strategic Developments

The global synchronous condenser market is moderately concentrated, with competition primarily driven by technological expertise, project execution capabilities, grid modernization requirements, and long-term service offerings. Market participants are focusing on large-scale transmission projects, renewable energy integration programs, system-strength initiatives, and strategic partnerships to strengthen their market positions. Based on the analysis of 81 identified projects in 2025, Siemens Energy held the leading position with approximately 28.4% of total identified project activity (23 projects), followed by ABB (8.6%), GE Vernova (7.4%), ANDRITZ (2.5%), and Linxon (2.5%). Other market participants collectively accounted for approximately 50.6% of identified projects, highlighting a competitive market structure with opportunities for regional expansion and project-based growth.

Organizations are adopting a strategy of entering into strategic alliances and making investments in infrastructure and other measures to bolster their competitive advantage through technology that allows them to harness energy generated from renewable sources. In 2025, Terna’s award of a grid reinforcement project to a consortium of companies comprising Ansaldo Energia and Hitachi Energy in 2025 for the installation of five 250 MVAr synchronous condensers with a total capacity of 1,250 MVAr.

Key Developments:

- In January 2025, Terna awarded a big grid reinforcement project to a joint venture involving Ansaldo Energia and Hitachi Energy for the installation of five 250 MVAr synchronous condensers, which sum up to about 1,250 MVAr. This is one of the largest installations of synchronous condensers in the world and is aimed at increasing the stability of the grid.

- In March 2025, GE Vernova made further progress with the Transelec transmission development in Chile, including about 1,000 MVAr of synchronous condensers. This project aims at improving system robustness, voltage stability, and reliability with the growth of renewable energy sources.

- In June 2026, the transmission system operators in the United States and Australia were moving forward with numerous projects involving synchronous condensers that went through construction and implementation stages. Such initiatives seek to resolve issues related to system strength, grid resiliency, and replacement of stability services from thermal plants.

Leading Company Profiles and Strategic Developments

Siemens Energy (Germany)

Siemens Energy had around 28.4% share of project involvement in the global synchronous condenser market in 2025, which made it the leading company with respect to the analysis of 81 projects. It has created a solid base through its wide range of synchronous condenser products and grid stabilization systems as well as transmission system strengthening projects. Siemens Energy has been engaged in significant renewable energy integration and transmission system development projects in North America, Europe, Australia, and Asia. The company is set up for success owing to its strong pipeline of projects up to 2030.

In May 2025, Siemens Energy partnered with ACEREZ for the Central-West Orana Renewable Energy Zone (REZ) in New South Wales, Australia, following the award of a contract to deploy seven synchronous condensers. The project is designed to support the integration of up to 4.5 GW of renewable energy while enhancing grid stability, voltage regulation, and system inertia across one of Australia's largest renewable energy zones.

Analyst Opinion

Based on the analysis of 81 identified synchronous condenser projects, the market is entering a period of sustained growth driven by accelerating renewable energy deployment, transmission network modernization, and increasing grid stability requirements. The growing retirement of conventional thermal power plants is creating a structural need for technologies capable of delivering inertia, fault current contribution, voltage regulation, and system-strength services, positioning synchronous condensers as critical assets within modern power systems. From a regional perspective, the two most suitable investment environments would be the US and Australia. This is due to a high concentration of projects, increased renewable power capacity, and demanding system strength criteria. An example of such a project is that of Terna with a capacity of 1,250 MVAr located in Italy and a project in Chile with a capacity of 1,000 MVAr operated by Transelec. The substantial volume of projects under development, planned, and being executed demonstrates a strong pipeline that extends well beyond 2026. From the analyst's perspective, transmission system operators will continue to be the major end-user segment, and increasing integration of synchronous condensers with BESS, STATCOM, and HVDC systems will provide additional opportunities for growth.

Transmission System Operators (TSOs) – Primary Revenue-Contributing Buyer Segment

Transmission System Operators (TSOs) represent the largest buyer group in the synchronous condenser market. Analysis of 81 identified projects shows that organizations such as Terna, EirGrid, Transgrid, Powerlink, and Transelec are leading investments to improve grid stability, system strength, and renewable energy integration.

Utilities Integrating Renewable Energy and Grid Modernization Projects

Utilities are increasingly deploying synchronous condensers to manage higher renewable energy penetration and maintain network reliability. The United States and Australia account for the highest concentration of identified projects, driven by grid modernization and renewable energy expansion.

Renewable Energy Zone (REZ) Developers and Grid Infrastructure Investors

Renewable Energy Zone developers are emerging as key buyers as large-scale solar and wind projects require additional inertia and system-strength support. Growing renewable deployment is accelerating demand for synchronous condenser installations across transmission networks.

Grid Operators Seeking Utility-Scale Stability Solutions

Grid operators are increasingly investing in utility-scale projects exceeding 1,000 MVAr. Notable examples include Terna's 1,250 MVAr project in Italy and Transelec's 1,000 MVAr project in Chile, highlighting demand for large-capacity grid-support assets.

Utilities Deploying Hybrid Grid-Stability Infrastructure

Utilities are increasingly integrating synchronous condensers with BESS, STATCOMs, and HVDC systems to enhance grid flexibility and reliability. This trend is creating new opportunities for advanced grid-stability infrastructure deployments.