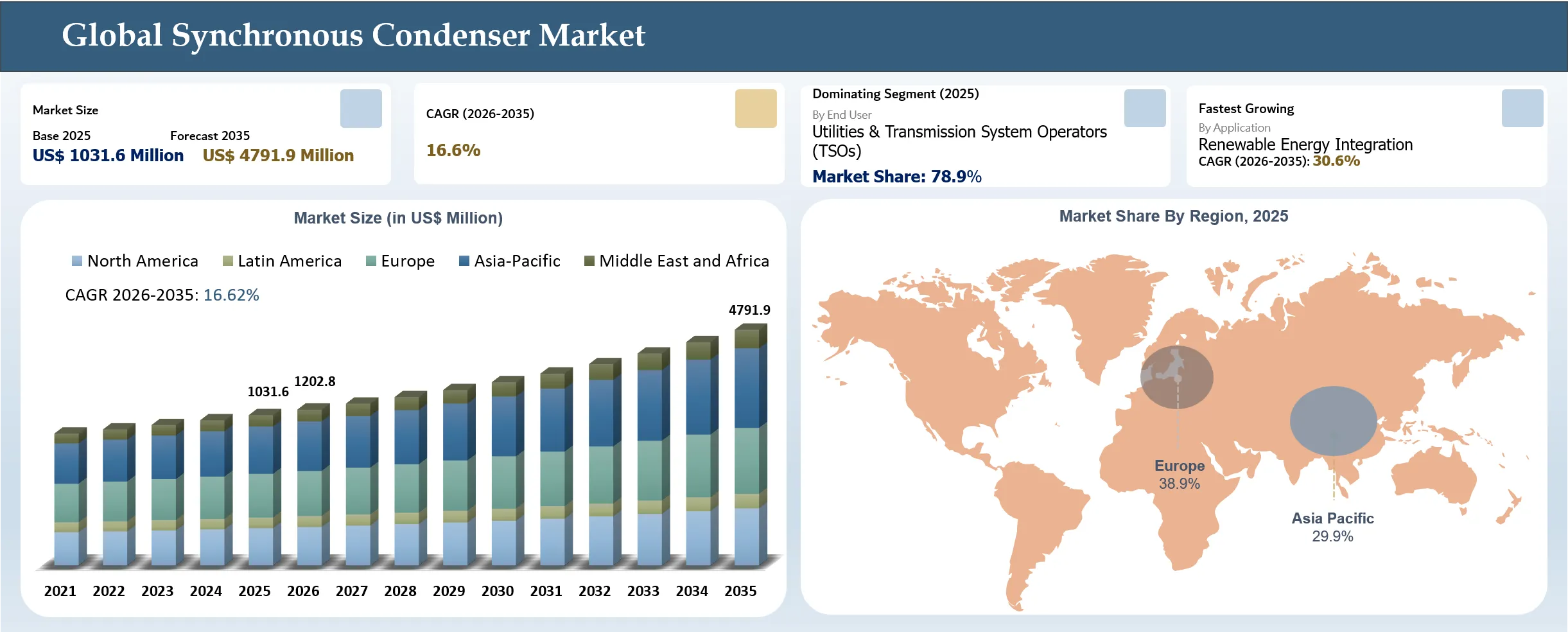

Synchronous Condenser Market Size and Forecast 2035

The global synchronous condenser market reached US$ 1031.6 million in 2025 and is expected to reach US$ 4791.9 million by 2035, growing with a CAGR of 16.6%, due to the increasing adoption of renewable energy as an alternate source of electricity, which requires grid stability, inertia support, and voltage regulation. In light of the shutdown of old power plants, which use coal, gas, and nuclear power that provide inertia and fault current levels, synchronous condensers are being used more often to make up for the shortfall. Technology has become an essential element in ensuring the stability of grids, especially in those dominated by renewable energy, which uses inverters for electricity generation from the sun and wind without any inertia.

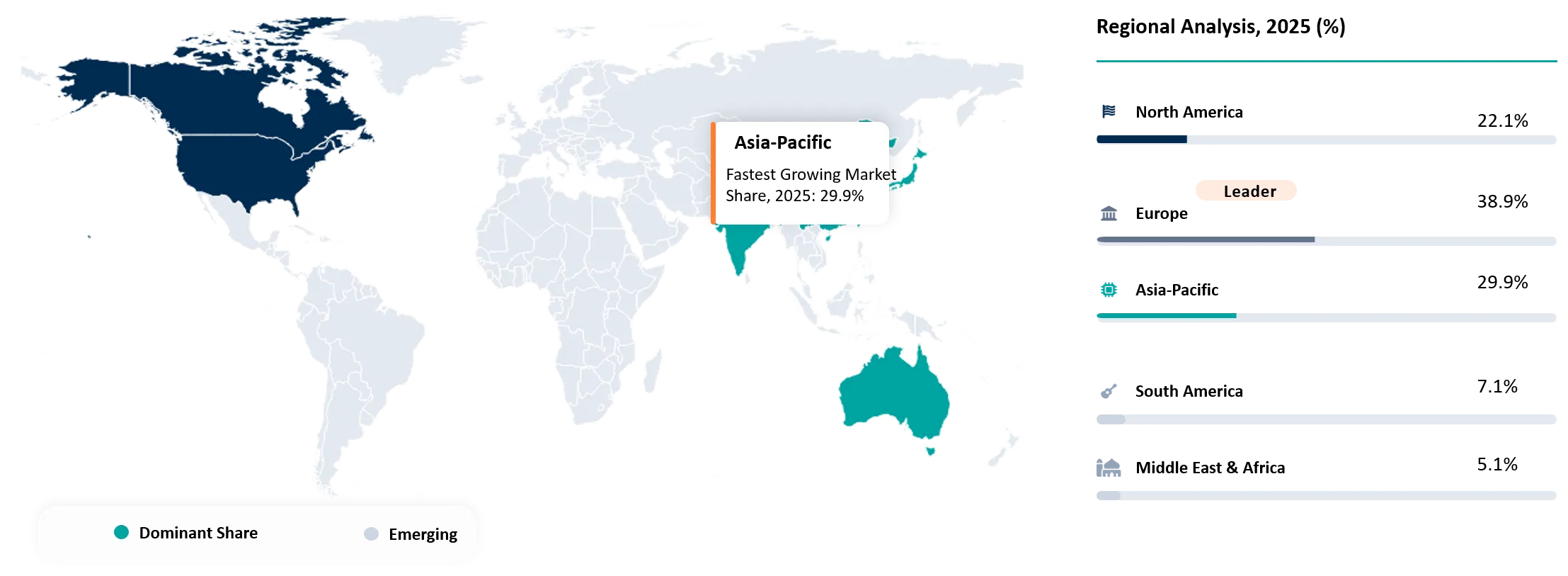

The global demand for synchronous condensers order volumes estimated to increase approximately from 68 units in 2025 to 377 units by 2035, supported by the rapid adoption of renewable energy sources and the retirement of thermal plants, coupled with grid strengthening efforts by utilities. Europe remained the leading regional market, worth about US$ 835.29 million in 2025, driven by growing penetration of renewables, decommissioning of thermal plants, and enhanced spending on power grids. The need for inertia support, reactive power compensation, and voltage regulation is expected to drive growth in Europe and other regions. Australia has also become one of the most popular deployment locations, where over 70% of power demands are supplied by renewable energy, prompting the use of huge synchronous condensers for improved grid performance. The synchronous condenser industry is poised to evolve into a crucial component of the global electrical power infrastructure sector, driven by growing adoption of renewable energy sources, retirement of conventional thermal power plants, grid upgrades, and the increased focus on maintaining system strength and frequency. With electricity grids across the world adopting more and more inverters in their generation profile, the synchronous condenser will become absolutely essential.

Key Takeaways

- The global order volume is forecast to rise from 68 units in 2025 to 377 units in 2035, reflecting the increasing demand for synchronous condensers from power utilities and grid companies looking for systems providing inertia, voltage control, and fault current capacity.

- Over 2,000 GW of fossil fuel-fired power generation capacity is expected to retire by 2040, while more than 760 GW was installed as new wind and solar energy systems during 2025, increasing the demand for synchronous condensers to provide rotational inertia and system strength.

- Europe is the largest regional market, which generating around US$ 835.29 million in 2025, backed by its strong decarbonization initiatives, closure of plants using fossil fuels, and adoption of wind and solar power.

- The synchronous condenser industry remained concentrated in the year 2025 with Siemens Energy AG at the helm of the market with an expected market share of 20.3%, GE Vernova Inc., 16.5%; ABB Ltd., 14.1%; Hitachi, Ltd., 9.4%; and ANDRITZ AG, 7.5%. The above firms continued to leverage their dominance in large-scale grid infrastructure projects, rotating machines, and transmission system operators worldwide.

Synchronous Condenser Market Scope

| Metrics | Details |

| CAGR | 2.4% |

| Size Available for Years | 2023-2033 |

| Forecast Period | 2026-2033 |

| Data Availability | Value (US$) |

| Segments Covered | Insulation, Cooling Technology, Reactive Power Rating, End-User, and Region |

| Regions Covered | North America, Europe, Asia-Pacific, South America and Middle East & Africa |

| Largest Region | North America |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth, Demand, Recent Developments, Mergers and Acquisitions, New Equipment Insulation Launches, Growth Strategies, Revenue Analysis, Porter’s Analysis, Pricing Analysis, Regulatory Analysis, Supply-Chain Analysis and Other key Insights. |

Synchronous Condenser Industry Trends and Strategic Insight

- Grid stability is becoming one of the key considerations in investments alongside renewable energy. As the uptake of renewable energy increases, there is greater investment in synchronous condensers for grid stability and reactive power support services.

- Countries where renewable energy generation exceeds 50% tend to use synchronous condensers to ensure reliable power supply. Spain produced 59% of its power through renewable energy sources in 2025, Greece exceeded 60%, while the UK produced 54.5% of its total power output using renewable sources of energy in 2025.

- There was an addition of over 760 gigawatts in 2025 globally in terms of wind and solar power capacities; meanwhile, almost 2,000 gigawatts worth of coal and gas generation capacity is expected to retire by 2040, creating a strong demand for synchronous condenser-based stability assets

- In the past used for reactive compensation, synchronous condensers are currently being considered as key transmission assets. The utilities have come to realize that batteries and power electronics will not be able to substitute the historical contribution to inertia and short-circuit capacity made by conventional power plants.

- Synchronous condensers have been found to be more frequently associated with transmission line upgrade, renewable generation integration, and grid modernization initiatives in recent times. These trends can be observed in UHV development in China, NEM upgrading in Australia, and renewable generation integration in Europe.

Synchronous Condensers Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ million | |

| 2035 Projected Market Size | US$ million | |

| CAGR (2026-2035) | 6.50% | |

| Largest Market | Europe | |

| Fastest Growing Market | Asia-Pacific | |

| By Starting Method | Static Frequency Converter (SFC), Pony Motor, Direct-On-Line (DOL), Variable Frequency Drive (VFD) | |

| By Cooling Technology | Hydrogen-Cooled, Air-Cooled, Water-Cooled | |

| By Reactive Power Rating | Below 150 MVAr, 150–300 MVAr, Above 300 MVAr | |

| By Application | Electrical Utilities, Renewable Energy Integration, Industrial Power Systems, Railways & Transportation, Others | |

| By End-User | Utilities & Transmission System Operators (TSO), Industrial Facilities, Renewable Energy Developers, Government & Public Infrastructure | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| South America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Disruption Analysis

Transition Toward Renewable-Dominated Low-Inertia Power Systems Reshaping Grid Stability Infrastructure Requirements

The global market for synchronous condensers is currently facing severe disruption due to the shift from synchronous sources of electricity generation to renewable energy generated using inverters. The installation of renewables has led to a decline in the inherent rotating inertia provided by coal, gas, hydro, and nuclear plants in the past. The growing gap between the development of renewable power and the preparedness of the transmission network. This has been observed in China, where the rapid development of renewable power has led to higher levels of energy curtailment, where solar energy curtailment has increased from 6.6% in the first half of 2025. These changes are turning synchronous condensers into strategically valuable grid stability components that not only allow for greater use of renewable energy but also guarantee the reliability of future low inertia power grids.

Despite strong market momentum in this segment, the high levels of capital intensity are still an issue. The construction of such units would necessitate investments in rotating electrical equipment, transformers, protection systems, and even in civil works, often culminating in multi-million project costs, as well as prolonged periods required for obtaining various licenses. Nevertheless, the understanding of the fact that neither batteries nor solutions based on power electronics can completely substitute physical inertia and short-circuit power is adding significant value to the use of synchronous condensers.

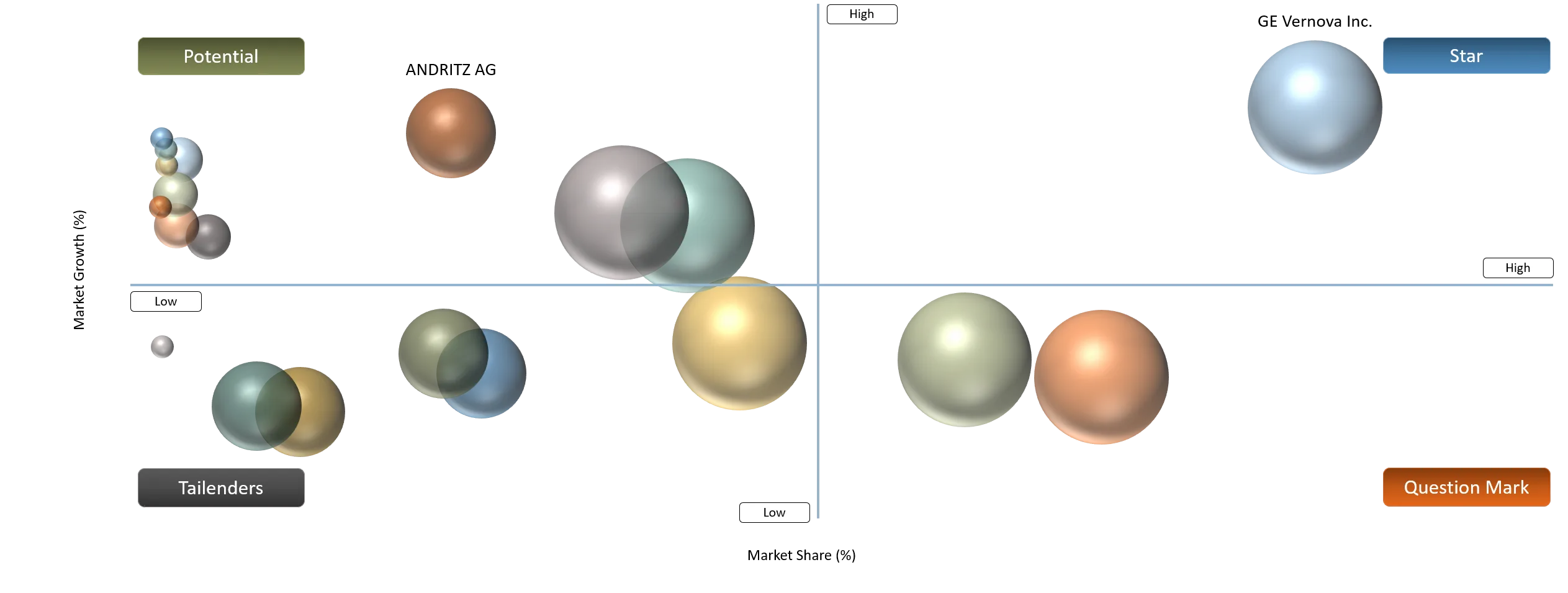

BCG Matrix: Company Evaluation

The star firms in the portfolio analysis include GE Vernova Inc., ABB Ltd, and Hitachi, Ltd because of their market strength, their association with utilities, and their strong portfolios in grid strengthening technologies. The firms directly benefit from growing investment in renewables integration, improved transmission, and strengthened system projects within Europe, North America, and Asia-Pacific. Question Marks Players include Mitsubishi Electric Corporation, Ansaldo Energia S.p.A., and WEG S.A.. While they have good engineering expertise and market presence in the regions, currently they have a relatively small market share than market leaders when it comes to deployment of synchronous condensers.

Potential players include ANDRITZ AG, Baker Hughes Company, and Toshiba International Corporation Pty Ltd. They will gain from the rising demands for rotating electrical machinery, modernizing power systems, and integrating renewable energy. Their technology prowess and current involvement in energy infrastructures make it easier for them to diversify to grid stability solutions. Other companies belonging to tailenders include IDEAL ELECTRIC POWER CO., given its niche position in the market and small involvement in major utility-scale grid stabilizer contracts. However, despite having specialized experience in the area of rotating electric machinery design, its geographic spread and size are relatively limited compared to major multinational corporations who dominate the industry.

Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

Increasing investment in transmission and distribution networks modernization is growing in North America. | 24% | Utilities, Transmission System Operators (TSOs), Grid Modernization Projects | Grid voltage regulation, reactive power compensation, transmission reliability enhancement | Accelerates deployment of advanced grid-support equipment and strengthens grid resilience amid aging infrastructure upgrades. |

Increase in the use of renewables projects that demand grid stability and voltage support. | 35% | Renewable energy integration zones, wind farms, solar parks, utility-scale power projects | Renewable integration, inertia support, frequency stabilization, voltage control | Creates sustained demand for synchronous condensers as critical infrastructure for renewable-heavy power systems. |

Closure of existing synchronous generator plants due to global decarbonization initiatives, especially in Europe. | 30% | Europe, Australia, UK, Germany, regions retiring coal and gas plants | Replacement of lost inertia, fault current support, system strength maintenance | Drives replacement investments and positions synchronous condensers as essential substitutes for retiring thermal generation assets. |

More reliance on renewable- dominated grids, which cause system strength problems and the need for reactive power provision. | 40% | High-renewable penetration grids in Europe, Asia-Pacific, North America, and Australia | System strength enhancement, reactive power provision, fault ride-through capability | Supports long-term market expansion as grid operators increasingly require dedicated stability solutions for low-inertia networks. |

Increase in the use of renewables projects that demand grid stability and voltage support

Rapid growth of the transition to renewables across the world is among the factors that stimulate the growth of the synchronous condenser industry. Traditional power generating units that were using coal, natural gas, or hydropower are gradually phased out and replaced by modern units utilizing renewable resources of energy based on inverter technology, such as solar and wind power facilities. Such sources of energy lack natural inertial properties of rotating machinery as well as proper provision for reactive power. This causes difficulties associated with system inertia, voltage stability, and fault level of the grid.

The increasing size of renewables’ deployment is creating an increased need for grid support infrastructure. Global installations of wind and solar have surpassed 760 GW in 2025, and inverter-based generation accounts for more than 40% of installed capacity in a number of advanced electricity markets such as the UK, Ireland, Australia, Spain, and certain regions in the US. In addition, over 2,000 gigawatts of thermal power plants using coal and natural gas are scheduled to retire by 2040, hence eliminating any significant sources of built-in grid inertia. Therefore, many utilities and grid operators are increasingly relying on synchronous condensers for grid frequency control, maintaining inertia, and facilitating smooth integration of renewable energy sources.

For instance, in 2026,Quinbrook Infrastructure Partners advanced the developments in the construction of synchronous condensers in the United Kingdom and bought out the 960 MVA Wexford Synchronous Condenser Project in Ireland. This shows the increasing significance of these resources within the energy grids with high concentrations of renewables.

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

| High Capital and Maintenance Costs | 5.4 | Project Economics & Utility Investment Decisions | New synchronous condenser installations in transmission substations and renewable integration projects | Delays project approvals, extends payback periods, and limits adoption among budget-constrained utilities and grid operators |

Lengthy Regulatory Approval and Cost-Recovery Processes | 3.0% | Regulatory & Infrastructure Planning |

Transmission network reinforcement and grid stability procurement programs | Slows project deployment timelines, creating gaps between grid stability requirements and infrastructure implementation |

Competition from Alternative Grid-Stability Technologies | 3.5% | Technology Selection & Capital Allocation | Reactive power compensation, voltage regulation, and frequency support applications | Encourages utilities to favor STATCOMs, SVCs, and BESS solutions, reducing synchronous condenser market penetration |

Limited Adoption in Cost-Constrained Emerging Markets | 2.5% |

Emerging Market Infrastructure Development | Renewable energy integration projects in developing economies | Restricts market expansion opportunities in high-growth regions despite increasing grid modernization needs |

High Capital and Maintenance Costs

High capital and maintenance costs remain a significant restraint on the global synchronous condenser market, despite their growing importance for grid stability. Verified cost benchmarks show that a new synchronous condenser installation costs typically depend on configuration, cooling system, foundation requirements and grid-connection complexity. When auxiliary equipment such as step-up transformers, protection systems and civil works are included, total project costs can rise further, pushing investment decisions into the multi-million-dollar range for a single site. For transmission operators operating under regulated tariffs, such high upfront capital outlays often require lengthy regulatory approvals and long cost-recovery timelines.

In addition to capital expenditure, ongoing operation and maintenance costs add to the economic burden. Public utility engineering references indicate that synchronous condensers typically incur annual maintenance costs of around USD 0.4–0.8 per kVAr, equivalent to roughly USD 40,000–80,000 per year for a 100 MVAr unit. The costs arise from periodic bearing replacement, rotor inspections, cooling system servicing and excitation equipment maintenance. Over a typical asset life of 30–40 years, cumulative maintenance expenditure can account for a meaningful share of total lifecycle cost, reducing the relative attractiveness of the technology.

For instance, in 2025, according to the IEEE Power & Energy Society through IEEE Xplore pointed out that the use of synchronous condensers in weak power networks and those dominated by renewables calls for optimization in unit sizing and location in order to make it economically feasible and stable. Incorrect distribution will result in an increase in overall costs and inefficiency, forcing utilities to do extensive power systems modeling and evaluation before carrying out their projects.

Segment Analysis

The global Synchronous Condenser market is segmented based on Starting Method, Cooling Technology, Reactive Power Rating, End-User, Application, and Region.

Utility-Led Demand Accelerates Deployment of Synchronous Condensers Across Modern Power Grids

Electrical utilities segment within global synchronous condenser market generated order value of 906.4 million in 2025 and is estimated to reach US$ 7540 million by 2035, growing at a CAGR of 16.9% during the forecast period from 2025-2035. Electrical utilities under end-user type of segment within global synchronous condenser market generated order volume of 54 units in 2025 and is estimated to reach 162 units by 2035, growing at a CAGR of 11.8% during the forecast period from 2025-2035.

The electrical utilities segment remains the dominant end-user profile within the global synchronous condenser market, driven by profound shifts in power system dynamics. As renewable penetration expands rapidly notably with global renewable electricity generation growing to provide 36.9% of total electricity in 2025, with 630 GW solar PV and 156 GW wind additions grid operators face increasing intermittency and reduced synchronous inertia from conventional generators. Conventional synchronous generators historically provided the bulk of system inertia, inherently stabilizing frequency and voltage following disturbances. With renewable sources lacking rotating mass, grids confront reduced inertia margins, increasing the risk of frequency deviations and voltage swings.

Geographical Penetration

Europe Maintains Leadership Through Grid Synchronization Initiatives and Renewable Energy Integration

The Europe synchronous condenser market remains dominant on a global scale because of significant investments made in modernizing its grid systems and developing renewable energy integration projects. The shift towards sustainable energy sources is increasing the demand for grid stability services that include the provision of inertia and regulation of voltage in order to replace the decreasing amount of synchronous generation. The market is expected to have an order value of about US$ 462.3 million in 2025, which will be further expanded to almost US$ 3.26 billion by 2035, with a CAGR of 16.2%. By volume, the market is expected to have an average of 20 units in 2025, and by 2035, the number will touch 145 units, achieving a CAGR of 12.5%.

For instance, in February 2025, the synchronization of the power grid of Estonia, Latvia, and Lithuania to CESA marked a significant event concerning energy security and grid independence in Europe. The investment in infrastructure in relation to this development amounted to more than €2 billion, where out of this, more than €1.2 billion came from the Connecting Europe Facility of the EU. Grid stabilization technologies, such as synchronous condensers and other frequency control techniques, have played an important role in these developments.

Germany Synchronous Condenser Market Trends

Germany emerges as an exemplary example of one of the strategically significant markets in the European synchronous condenser market due to its increased adoption of renewable energy sources and phase out of traditional synchronous generators. The higher integration of renewable energy sources with the grid has led to the rising need for solutions that provide grid stability through inertia and fault current injection. The synchronous condensers market in Germany is expected to be valued at roughly US$ 18.5 million in 2025 and is further expected to touch nearly US$ 768.8 million by 2035, with a CAGR of 22.9% over the forecast period. By volume, the market is expected to be at roughly 1.7 units in 2025 and is expected to reach roughly 8 units by 2035, with a CAGR of 16.5%. Growth in the market is being fueled by investments in technologies that strengthen the grid as more renewables displace conventional energy generation technologies.

For example, the TenneT corporation whereby in 2025, Siemens Energy installed synchronous condensers in Großkrotzenburg (in Hessen) and Würgassen (in North Rhine-Westphalia) to offer inertia response, voltage control, reactive power management, and short circuit capabilities. Such cases are indicative of the increased use of synchronous condensers in efforts to ensure the reliability of the grid.

UK Synchronous Condenser Market Outlook

The United Kingdom continues to be a prominent market in Europe for implementing synchronous condensers owing to efforts geared towards improving its power grid and integrating renewable energy resources at an accelerated pace. As the country shifts to adopting a low-carbon electricity system, there is growing demand for solutions that can maintain power grid stability by offering services such as inertia, reactive power, and voltage control as traditional thermal sources reduce.The UK market for synchronous condensers is expected to generate an order size of about US$ 118.9 million in 2025, while the market is expected to reach about US$ 1.38 billion in 2035, with a growth rate of 12.8% in the forecasted period. Considering the volume of sales, the market size is expected to be about 7 units in 2025, while it is expected to witness an increase to about 40 units in 2035, growing at a CAGR of 9.8%.

For instance, in 2026, Pulse Clean Energy was able to raise £52.5m to finance the construction of two synchronous condenser plants at Pontypridd in South Wales through the Stability Pathfinder Program. This is intended to deliver much-needed inertia, short-circuit strength, and reactive power into the grid network as renewables become more dominant.

Competitive Landscape

The global market of synchronous condensers include power equipment companies, grid infrastructure companies, and industrial electromechanical solution providers. Competition within this market sector is highly based on the technological capability of reactive power compensation, grid stabilizing, system strength improvement, and renewable energy application. Some prominent competitors like Siemens Energy AG, GE Vernova Inc., ABB Ltd., Hitachi, Ltd., and ANDRITZ AG hold a competitive advantage within the market due to large project portfolios, global reach, and advanced grid stability technologies. On the other hand, competitors like Mitsubishi Electric Power Products, Inc., Ansaldo Energia S.p.A., WEG S.A., Baker Hughes Company, and IDEAL ELECTRIC POWER CO. create stiff competition within the market through unique rotating machinery capabilities, power system solutions, and infrastructure projects within various regions.

Key players involved in the international market of synchronous condensers are GE Vernova Inc., Siemens Energy AG, ABB Ltd, Hitachi, Ltd., Mitsubishi Electric Power Products, Inc., Ansaldo Energia S.p.A., ANDRITZ AG, WEG S.A., Baker Hughes Company, and IDEAL ELECTRIC POWER CO..

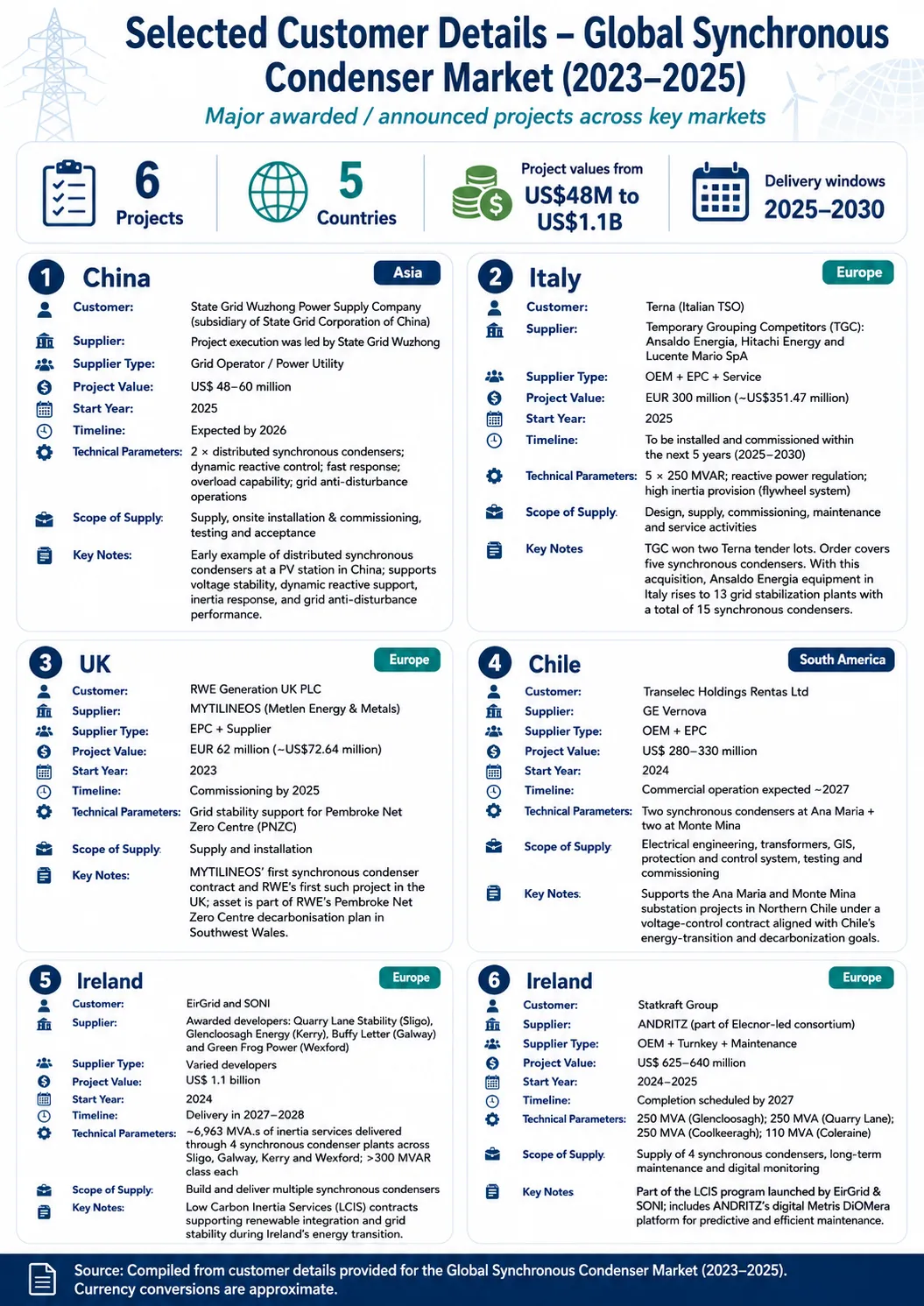

Global Synchronous Condenser Market: Historical and Current Customer Projects Database, Contract Wins, Supplier Involvement, and Investments Analysis

Market Leadership Through an Extensive Project Portfolio

Analysis of the 81 synchronous condensers projects shows that Siemens Energy is holds the strong market position on a global scale, owing to the largest number of projects won and implemented in North America, Europe, Australia, and Asia. ABB and GE Vernova are other major competitors with GE Vernova participating in the Transelec Project in Chile, featuring around 1,000 MVAr synchronous condensers.

The leading markets for synchronous condenser projects include the USA and Australia due to the need to enhance grid stability, integrate renewable energy resources, and increase system strength. The pipeline of projects is rather robust, featuring many projects under planning, implementation, and execution phases. Terna's project in Italy, which entails the implementation of five 250 MVAr synchronous condensers, is one of such examples with the total capacity being about 1,250 MVAr.

The transmission system operators including Terna, EirGrid, Transgrid, Powerlink, and Transelec continue to dominate investment in the industry, underscoring the increasing significance of synchronous condensers in delivering grid stability services previously offered by thermal generation plants. Going forward, renewable energy incorporation, power plant decommissioning, and rising grid standards will drive market expansion through 2030, while hybrid systems featuring battery energy storage systems (BESS), STATCOMs, and HVDC systems attract attention.

Key Developments

- February 2025: Ansaldo Energia S.p.A. obtained a contract to provide five synchronous condensers for Italy’s transmission grid, which were intended to increase inertia, voltage, and reactive power support in the grid as renewable energy usage grows.

- May 2025: Siemens Energy AG collaborated with ACEREZ on deploying seven units of flywheel-integrated synchronous condensers in the Central-West Orana Renewable Energy Zone of Australia, enabling 4.5 GW of renewable energy deployment.

- October 2025: GE Vernova Inc. obtained a contract with Transgrid to supply two large synchronous condensers for use in New South Wales, Australia, contributing to the provision of stability services that were earlier delivered by traditional power plants.

- October 2025: ANDRITZ AG received contract of four synchronous condenser units to Statkraft, which will be deployed in Ireland and Northern Ireland to facilitate increased inertia and reactive power capability in renewable electricity networks.

- November 2025: ABB Ltd collaborated with VoltaGrid on implementing synchronous condenser technology in support of artificial intelligence data centers across America.

Key Procurement Priorities and Buyer Evaluation Criteria

- Organizations which are making their investments on synchronous condensers are giving preference to vendors who have strong experience in stabilizing grids, providing reactive power compensation and inertia support, and voltage control. The choice made regarding procurement is greatly dependent on whether the company is able to offer reliable equipment for utility-scale renewable power applications.

- Purchasing practices are becoming more influenced by the ongoing phase-out of traditional synchronous generation equipment, higher penetration levels of renewable generation, and increased demand for fault level support. It is preferable for utilities and transmission system operators to source suppliers who can offer high-quality synchronous condenser units with effective control systems and fast-response mechanisms.

- By the multiple factors that buyers consider in assessing the suitability of suppliers, which include reactive power generation, contribution to system inertia, voltage regulation capabilities, improvement in short circuit strength, efficiency in the systems, cost and maintenance aspects of the systems among others. Compatibility with existing transmission systems is also very important.

- End users also consider aspects like the experience with implementation of projects, engineering and commissioning abilities, digitalized monitoring systems, after-sales services, equipment dependability, and overall cost of ownership. Those companies that have an impressive track record when it comes to working on renewable-dominated electricity networks, major transmission works, and grid modernization projects receive preference due to lower levels of risk associated with their activities.

Why Choose DataM?

- Technological Innovations: Explores advancements in Fan-Out Wafer-Level Packaging including high-density RDL, panel-level packaging, and heterogeneous integration, enabling improved performance, reduced power consumption, and smaller form factors for AI, 5G, and high-performance computing applications.

- Product Performance & Market Positioning: Evaluates how different players deliver packaging solutions based on I/O density, thermal performance, miniaturization, and cost efficiency, highlighting how leading companies differentiate through advanced integration and scalability across consumer electronics and automotive applications.

- Real-World Evidence: Highlights adoption of FOWLP in smartphones, wearables, automotive electronics, and AI chips, demonstrating benefits such as enhanced processing speed, reduced footprint, improved energy efficiency, and optimized system-level performance.

- Market Updates & Industry Changes: Tracks key developments such as capacity expansions, new packaging platforms, panel-level innovations, and regional semiconductor investments across Asia-Pacific, North America, and Europe, supporting the shift toward advanced packaging ecosystems.

- Competitive Strategies: Analyzes how leading companies expand through capacity scaling, technology innovation, strategic partnerships, and integration of advanced packaging with chip design to address rising demand from AI and high-performance computing markets.

- Pricing & Market Access: Explains pricing variations based on complexity, wafer size, and integration level, along with access through OSAT providers, foundries, and integrated device manufacturers supporting global supply chains.

- Market Entry & Expansion: Identifies growth opportunities driven by AI, 5G, automotive electronics, and data centers, while outlining strategies such as regional capacity expansion, technology differentiation, and ecosystem partnerships to scale globally.

Target Audience

- Electric Utilities & Power Generation Companies

- Transmission System Operators (TSOs) & Grid Operators

- Renewable Energy Developers

- Power Equipment Manufacturers & EPC Contractors

- Industrial Power Users

- Government Agencies & Energy Regulators

- Investors, Infrastructure Funds & Private Equity Firms