How AI rack density, modular power design and real time telemetry are reshaping PDU demand through 2035

AI data centers are changing the role of the power distribution unit. For years, PDUs were treated as rack hardware that distributed electricity after the larger design decisions had already been made. In GPU dense AI halls, the PDU is becoming a control point for capacity planning, load visibility, uptime protection and energy efficiency. This change is occurring because the bottleneck in AI infrastructure is shifting from data hall space to reliable power delivery across the full chain from grid connection to rack outlet.

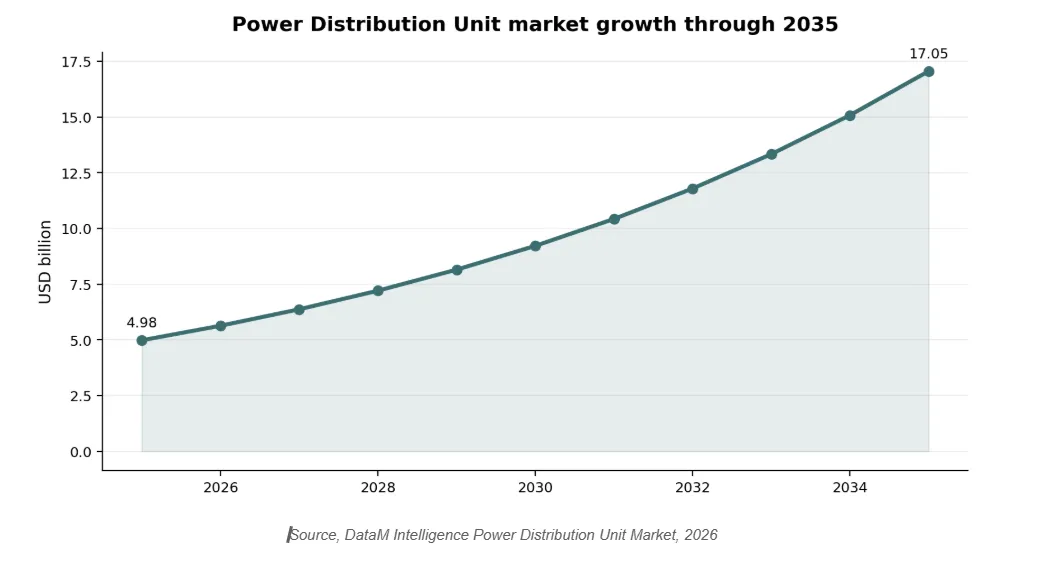

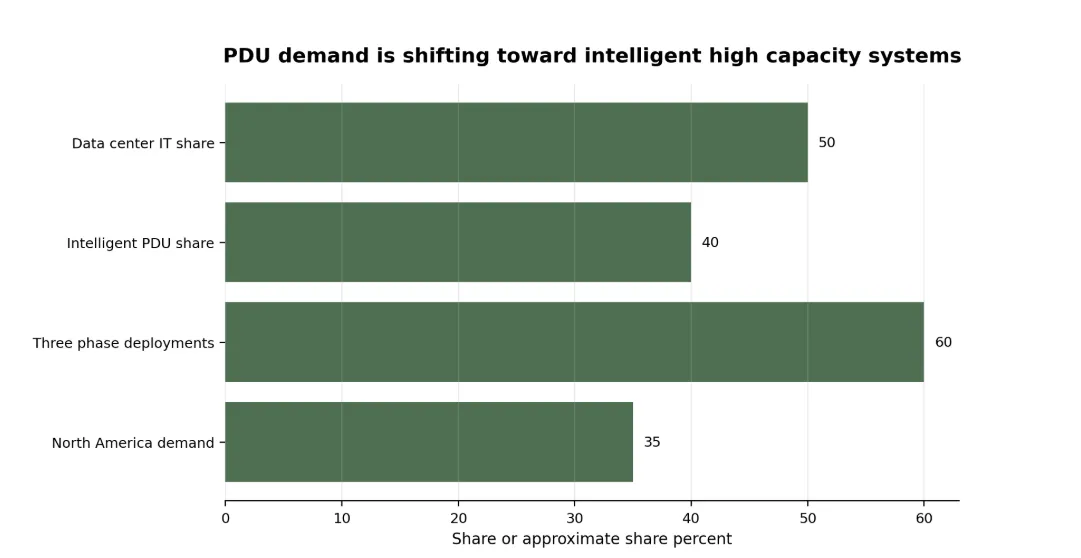

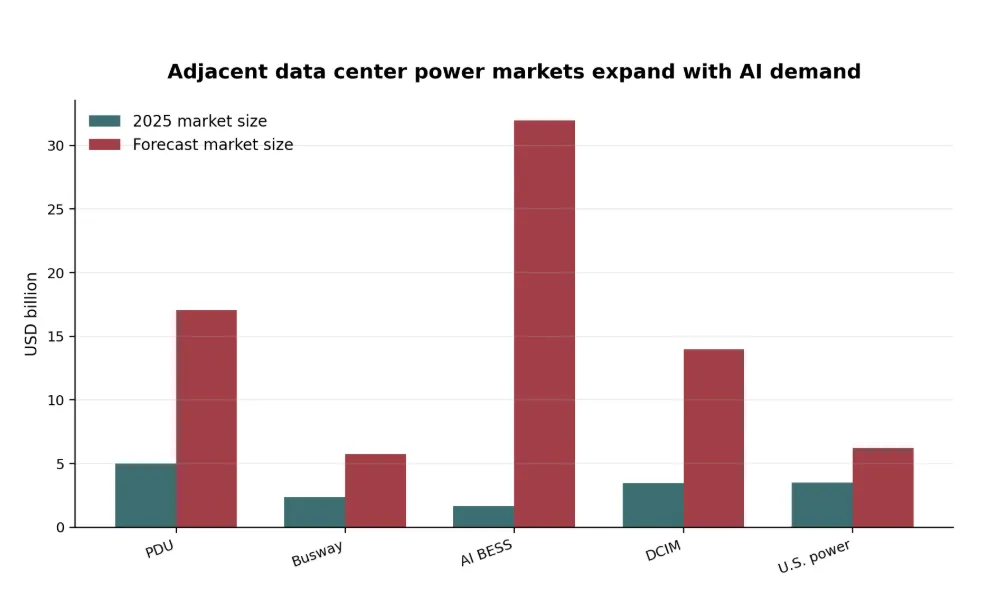

The latest market data supports this shift. DataM Intelligence estimates that the global Power Distribution Unit Market will grow from USD 4.98 billion in 2025 to USD 17.05 billion by 2035, registering a 12.89% CAGR. Data centers and IT infrastructure already contribute more than half of market revenue, intelligent and monitored PDUs represent more than 40 percent of new installations and three phase PDUs account for about 62% of enterprise deployments. These figures explain why rack power has become a strategic procurement category.

Understand the Future of Power Distribution Infrastructure

Explore the latest Power Distribution Unit Market trends, growth forecasts, intelligent PDU adoption, and how AI data centers are reshaping rack-level power management.

AI Rack Density Is Forcing a New Power Distribution Model

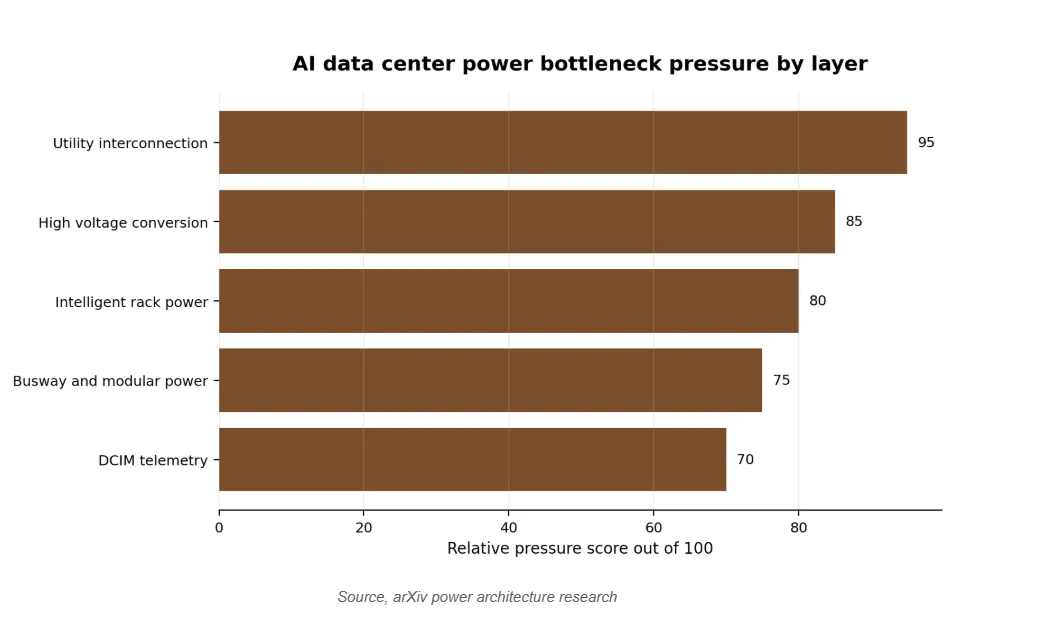

The AI data center power problem is becoming more visible at the rack. Traditional enterprise racks often operated at moderate power levels, while AI training and inference clusters are pushing facilities toward much higher rack densities. A recent arXiv paper on next generation AI data centers argues that AI workloads are exposing limitations in traditional 48 V rack architectures, low voltage AC distribution and line frequency transformer interfaces. The paper points toward higher voltage conversion and medium voltage solid state transformers as part of the next power architecture.

This creates a direct opportunity for advanced PDUs because higher rack density requires more than additional outlets. Buyers need outlet level monitoring, environmental sensors, branch level visibility, remote switching and integration with data center infrastructure management platforms. They also need PDUs that can support higher voltage, higher current and more complex redundancy designs without increasing failure risk. In AI environments, power distribution becomes a live operating system for the data hall.

Schneider and Foxconn Signal the Shift Toward Modular AI Power Infrastructure

The partnership between Schneider Electric and Foxconn shows how suppliers are responding to the data center power bottleneck. According to current deal coverage, the collaboration is aimed at helping customers build and operate AI infrastructure with greater speed and efficiency through closed loop energy optimization plus modular power and cooling assemblies. Production is expected to begin later in 2026. This type of partnership matters because AI data center buyers increasingly want factory built, pre integrated and repeatable power blocks that reduce field execution risk.

That shift reaches directly into the PDU market. Modular data centers still require rack level power control, but the buying process becomes more standardized. Instead of procuring PDUs as individual devices late in construction, buyers are starting to specify rack power, busway, monitoring software, UPS interfaces and cooling coordination as part of a single power architecture. This favors suppliers that can offer integrated electrical systems rather than isolated components.

Get the Latest U.S. Data Center Power Market Insights

Gain comprehensive insights of U.S. Data Center Power Market growth, power infrastructure trends, grid challenges, and the evolving strategies shaping the future of U.S. data center operations.

Busway, PDU and Monitoring Layers Are Converging

The data center power chain is becoming more modular from ceiling busway to rack outlet. DataM Intelligence estimates that the Data Center Busway Market will expand from USD 2.38 billion in 2025 to USD 5.76 billion by 2035. Busway systems are gaining relevance because they can reduce installation time, simplify power reconfiguration and support scalable overhead distribution in high density data halls. For AI customers, that flexibility becomes valuable when rack layouts change as GPU generations evolve.

Explore the Data Center Busway Market Report

Discover how scalable power distribution, overhead busway systems, AI-driven data center expansion, and high-density rack requirements are shaping the future of data center electrical infrastructure. Access detailed market insights, growth trends, and strategic opportunities driving the busway market through 2035.

PDUs and busway systems are also becoming data sources. Intelligent rack PDUs can feed real time load, temperature and alarm data into DCIM platforms. That makes them important for capacity planning because operators need to know which racks can safely accept additional compute and which circuits are approaching constraints. DataM Intelligence estimates that the Data Center Infrastructure Management Market will grow from USD 3.47 billion in 2025 to USD 13.98 billion by 2033, supported by demand for power monitoring, capacity planning and AI enabled operational intelligence.

Backup Power and Ride Through Are Becoming PDU Design Considerations

AI clusters create fast changing load profiles that can stress electrical infrastructure. A separate arXiv analysis of large AI clusters described power management across a 150 MW data center hosting 83,000 GB200 GPUs and argued that electric power supply has become a leading bottleneck in the AI infrastructure race. This creates a new requirement for PDUs, UPS systems and energy storage to work together more intelligently. The PDU is becoming part of a coordinated resilience stack that includes battery energy storage, generator interfaces, busway and power software.

This is why AI data center battery energy storage is becoming more relevant. DataM Intelligence estimates that the AI Data Center BESS Market will grow from USD 1.65 billion in 2025 to USD 31.97 billion by 2035, a 34.5 percent CAGR. BESS can support ride through, peak shaving, renewable firming and grid services. As storage becomes integrated with data center power architecture, intelligent PDUs will be expected to provide the rack level telemetry needed for fast load control and maintenance planning.

Discover the Future of the AI Data Center BESS Market

Explore the evolving role of battery energy storage systems in AI data centers, from backup power and peak shaving to grid resilience and energy optimization. Access market insights, growth trends, and emerging opportunities shaping the future of AI infrastructure power management.

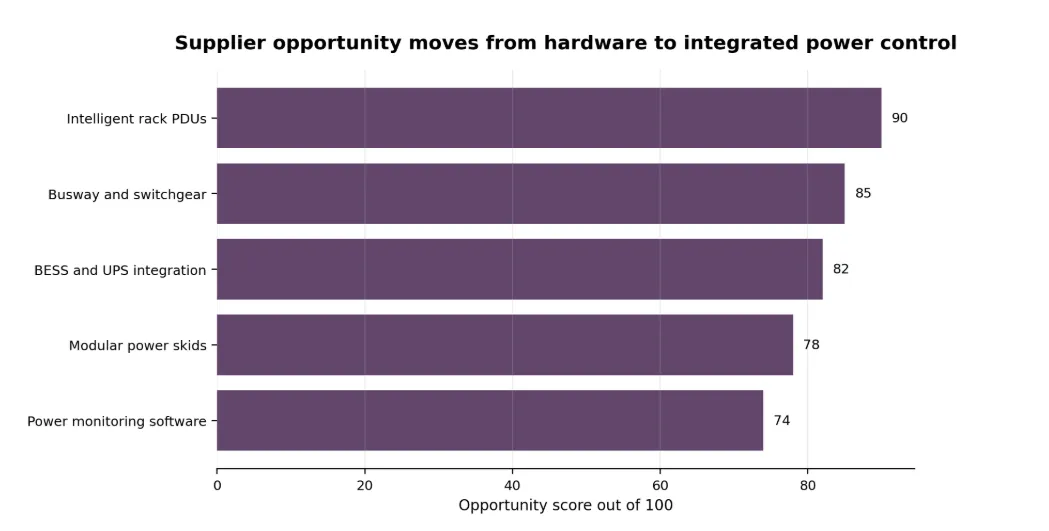

Where Suppliers Can Capture the Most Value

The strongest opportunities are emerging around intelligent rack PDUs, busway and switchgear, BESS integration and power monitoring software. Basic rack distribution will remain necessary, but margin expansion is likely to come from devices with software integration, cybersecurity features, remote management, environmental sensing and compatibility with higher density rack architectures. Suppliers that can help operators reduce commissioning time, improve visibility and lower downtime risk will be better positioned than those selling commodity rack hardware.

This also explains why power infrastructure partnerships are accelerating. Schneider Electric, Vertiv, Eaton, ABB, Legrand and other electrical infrastructure suppliers are competing to own more of the data center power stack. Foxconn and other manufacturing partners bring scale, systems integration capability and speed to deployment. Hyperscale customers are looking for standardized building blocks that can be replicated across regions while still adapting to local grid constraints.

Supplier opportunity is strongest where rack power connects to software and modular deployment

Source note, analyst scoring based on DataM Intelligence market data, AI data center power research and current industry developments

Regional Demand Will Follow Power Availability

The U.S. remains the most important market because it combines hyperscale cloud demand, AI model development, colocation expansion and a large electrical infrastructure supplier base. DataM Intelligence estimates that the U.S. Data Center Power Market reached USD 3.50 billion in 2025 and is expected to reach USD 6.25 billion by 2033. The report also highlights grid upgrades, transmission bottlenecks, space scarcity and utility power delivery delays as constraints that can slow growth in key markets.

The global picture is moving in the same direction. Europe faces grid congestion and sustainability pressure in established hubs. Asia Pacific is expanding quickly as cloud, AI and digital sovereignty projects increase demand in China, India, Japan, South Korea and Southeast Asia. The Middle East is building large AI and sovereign cloud campuses where power access, cooling design and modular infrastructure are being evaluated together. Across regions, data center growth will increasingly follow locations that can provide firm power, scalable electrical infrastructure and reliable supplier ecosystems.

The Next PDU Cycle Is About Control and Distribution Intelligence

The PDU market is entering a new cycle because AI data centers are changing what buyers expect from rack power. The next generation of PDUs will be selected based on capacity, telemetry, cybersecurity, remote operations and compatibility with broader power architectures. High density racks will require more precise circuit visibility. Modular data centers will require faster integration. Grid constrained sites will require better coordination between facility power, storage and compute operations.

The market direction is clear. PDUs are moving from the edge of the rack bill of materials toward the center of AI data center infrastructure strategy. The companies that benefit most will be those that treat power distribution as part of a connected control layer across racks, busways, UPS systems, storage and DCIM platforms. In a market where power availability can determine which AI campuses get built first, rack level power intelligence will become a competitive advantage.

DataM Intelligence Reports Relevant to This Topic

| Report | Why it fits | CTA |

| Power Distribution Unit Market | PDU market sizing, intelligent PDU adoption, rack power distribution and end user demand | Open report |

| U.S. Data Center Power Market | Power distribution, power backup, cabling infrastructure, utility delays and data center power strategy | Open report |

| Data Center Busway Market | Overhead busway systems, scalable power distribution, PDUs and AI ready data center infrastructure | Open report |

| AI Data Center BESS Market | Battery energy storage, ride through, peak shaving, renewable firming and backup power for AI data centers | Open report |

| Data Center Infrastructure Management Market | Power monitoring, capacity planning, environment monitoring, analytics and AI enabled infrastructure visibility | Open report |

Source Notes Used for the Article

DataM Intelligence, Power Distribution Unit Market, June 2026.

DataM Intelligence, U.S. Data Center Power Market, April 2026.

DataM Intelligence, Data Center Busway Market, July 2026.

DataM Intelligence, AI Data Center BESS Market, May 2026.

DataM Intelligence, Data Center Infrastructure Management Market, June 2026.

Wall Street Journal coverage of Schneider Electric and Foxconn partnership on AI data centers, June 2026.

arXiv 2606.25095, Toward Next Generation AI Data Centers, June 2026.

arXiv 2605.24461, Provisioning to Runtime Optimization of a 100 MW plus AI Cluster, May 2026.