The global transition toward deeply electrified economies has reached a pivotal structural inflection point. For the past decade, institutional capital heavily prioritized downstream original equipment manufacturers (OEMs) and utility-scale renewable deployment. However, as global lithium-ion battery deployment scales up dramatically driven by electric vehicles accounting for more than 70% of total battery demand and Battery Energy Storage Systems (BESS) contributing over 15% investors are recognizing that the true bottleneck, and the most lucrative value capture opportunity, lies upstream.

Battery chemicals, active raw materials, and functional components are no longer treated as simple raw commodities. Instead, they represent the foundational technology stack determining the energy density, safety, lifecycle economics, and supply chain viability of the next generation of energy storage systems.

The Macro Market Architecture: A Half-Trillion Dollar Horizon

According to deep-dive data compiled by DataM Intelligence, the capital appreciation runway across the battery value chain is bifurcating into two massive market opportunities:

1. The Battery Chemicals and Materials Market

Comprising active cathode materials (CAM), anode active materials (AAM), specialized electrolyte formulations, binders, and separator coatings, this sector was valued at US$ 82.75 billion in 2025. Propelled by structural chemistry shifts and exponential capacity expansion, it is projected to skyrocket to US$ 257.01 billion by 2035, sustaining a compounding annual growth rate (CAGR) of 12.0%.

2. The Battery Components and Core Material Infrastructure

Encompassing cell elements (separators, current collectors, casings) alongside module and pack architectures (Battery Management Systems, busbars, connectors, and thermal management enclosures), the broader battery material and systems infrastructure is forecast to hit US$ 105.84 billion by 2035, advancing at a reliable CAGR of 6.0% as packaging, interconnects, and pack-level integration demand increases.

| Market Core Segment | Value Baseline (2025) | Projected Valuation (2035) | Compounding Annual Growth Rate (CAGR) |

|---|---|---|---|

| Battery Chemicals | US$ 82.75 Billion | US$ 257.01 Billion | 12.0% (2026-2035) |

| Battery Materials & Pack Systems | ~US$ 59.1 Billion (2026) | US$ 105.84 Billion | 6.0% (2026-2035) |

Ready to Unlock the Full Market Blueprint?

The battery chemicals landscape is transitioning from a high-growth narrative into a highly competitive, multi-billion dollar infrastructure scale-up. With the global market projected to surge from US$ 82.75 billion in 2025 to US$ 257.01 billion by 2035, keeping pace with structural shifts in LFP dominance, sodium-ion commercialization, and localization mandates requires precise, validated data.

Get ahead of the curve and gain exclusive access to primary market metrics, competitive positioning landscapes, and granular regional growth trajectories.

Download the Sample Research Report Here

Core Catalysts Driving Institutional Capital into Battery Chemistry

1. The Utility-Scale BESS Acceleration Factor

Sovereign grids are facing unprecedented balancing pressures as solar and wind penetrations pass critical thresholds. Solar and wind capacity are expanding faster than traditional grids can absorb them. Battery energy storage systems help shift electricity from high-generation periods to peak-demand periods, reduce renewable curtailment, and improve grid stability. Globally, utility-scale battery deployment is surging significantly, with gigawatt-scale capacity additions hitting record milestones month-over-month across China, North America, and Europe. This immense growth creates continuous, non-cyclical demand for specialized battery chemicals optimized for calendar longevity rather than sheer gravimetric density.

2. The Geopolitical Imperative of Supply Chain Localization

The geographic concentration of the battery value chain currently presents an acute vulnerability for Western markets. Asia-Pacific, led by China, dominates the landscape, commanding a massive 61.2% market share in 2025 due to its deeply connected ecosystem spanning raw mineral refining, precursor production, and cell manufacturing.

Consequently, resource nationalism and regulatory trade restrictions have accelerated dramatically. Automakers, utilities, and cell makers want alternative supply chains, prompting governments to deploy capital directly into domestic infrastructure:

- India: Driven by a target of 500 GW of non-fossil fuel energy deployment by 2030, the market for energy storage and EVs is triggering local manufacturing initiatives to support a stable grid and reduce import reliance.

- Europe & North America: Capital flows are actively pivoting to build regionalized lithium conversion, chemical synthesis, and closed-loop recycling plants driven by localized tax credits and strict sourcing rules.

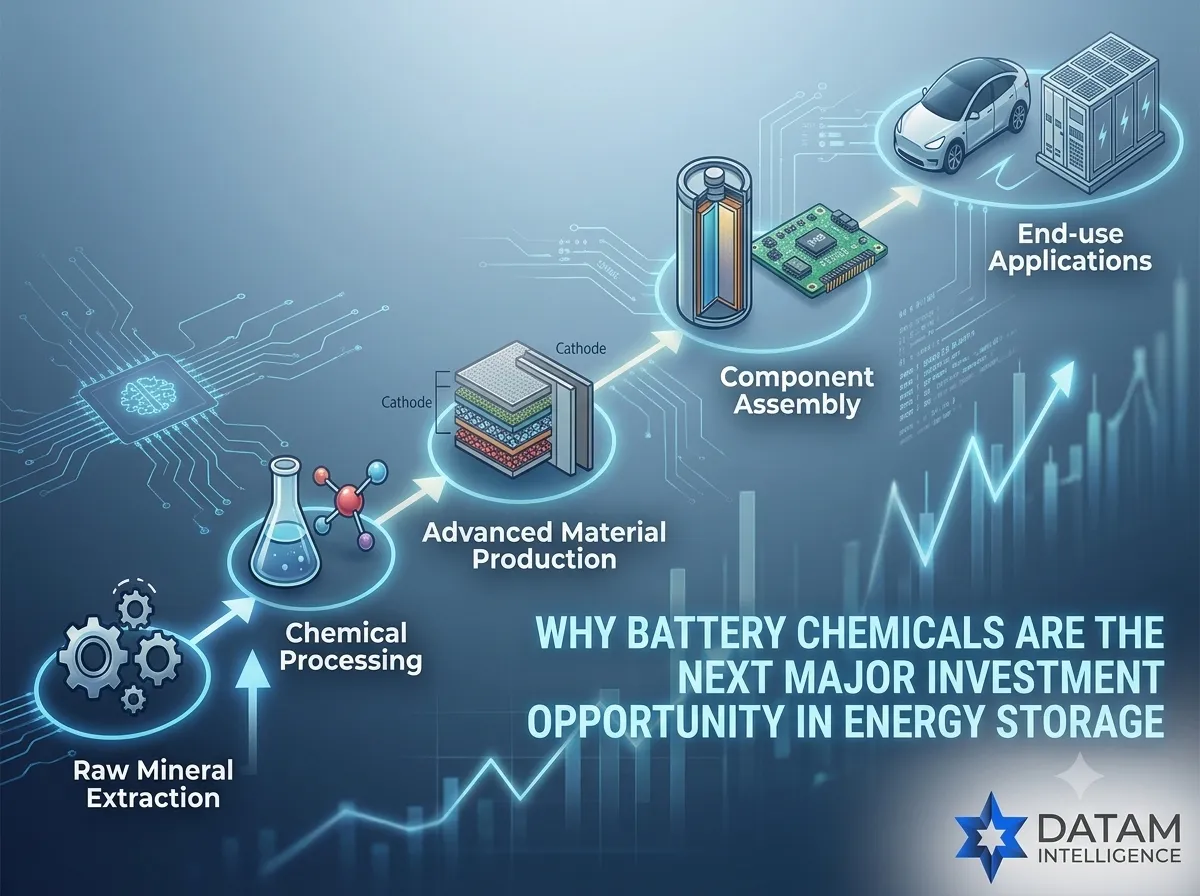

Upstream Extraction (Lithium, Nickel, Graphite, Cobalt)

│

▼

Advanced Chemical Refining (Lithium Salts, Sulfates)

│

▼

Active Materials Production (Cathodes, Anodes, Advanced Electrolytes)

│

▼

Functional Components Assembly (Separators, Current Collectors, BMS)

│

▼

Downstream Gigafactory Integration (Automotive EV & Grid BESS Systems)

Technological Disruptions: Where the Highest Value Lies

Investors looking to optimize their entry points must understand the critical chemistry transitions currently underway within the sector:

The Decisive Triumph of LFP and Cobalt-Free Formulations

Average battery pack prices have fallen dramatically due to manufacturing scale and lower component costs. Lithium Iron Phosphate (LFP) chemistry has experienced rapid traction, capturing 42.7% of the global battery chemicals market share in 2025. By eliminating volatile and expensive elements like cobalt and nickel, LFP offers better cost stability, exceptional thermal stability, and increased cycle life. This shift provides an excellent growth runway for providers of high-purity iron phosphate precursors, synthetic graphite, and advanced electrolyte additives tailored for stable solid-electrolyte interphase (SEI) performance.

The Ascent of Sodium-Ion Commercialization

To mitigate exposure to lithium price volatility, manufacturers are rapidly advancing sodium-ion battery technology for cost-sensitive mobility and long-duration stationary grids. Because sodium is abundant and less geographically concentrated than lithium, the sodium-ion battery market is projected to skyrocket from USD 1,263.70 million in 2025 to USD 8,643.11 million by 2035, at an aggressive 21.2% CAGR. The deployment of hard carbon anodes and specialized chemical cathode formulations presents a unique ground-floor opportunity for chemical suppliers capable of scaling raw sodium compounds.

Electrolytes and Smart Component Engineering

Electrolyte chemicals have emerged as the fastest-growing product type, advancing at a 15.3% CAGR. As battery manufacturers focus on fast-charging, safety, and high-energy density batteries, the need for superior electrolyte solutions and functional additives has accelerated. Concurrently, buyers increasingly prefer suppliers that can support advanced battery system integration, including structural enclosures, thermal management materials, and smart pack-level components.

Analytical Quality Control: The Unsung Investment Enabler

As battery gigafactories scale production volumes, the competitive advantage is shifting from simply securing raw materials to building an integrated, high-purity chemical ecosystem. The global capacity of lithium-ion battery manufacturing surpassed 4 TWh at the end of 2025, growing 30% year-over-year.

This massive manufacturing footprint has caused a sharp rise in the need for material characterization, process monitoring, and impurity analysis. Maintaining strict quality control is essential to ensure material consistency and safety. Consequently, specialized chemical companies focusing on advanced analytical testing validation and ultra-pure chemical output are commanding premium enterprise valuations.

Strategic Summary for Institutional Investors

The investment landscape for energy storage has permanently shifted from simple downstream asset collection to highly sophisticated upstream chemical engineering. To maximize value capture, capital allocation strategies should prioritize three main pillars:

- Vertical Value Chain Integration: Focus on refining and active chemical processing assets that bridge the gap between crude mineral mining and battery-grade precursor synthesis.

- Sovereign Geographies: Target manufacturing projects located in regions building localized battery material clusters to mitigate geopolitical supply risks.

- Next-Generation Chemistry Enablers: Direct capital toward advanced LFP cathode innovations, fast-growing electrolyte formulations, and commercial scaling of sodium-ion material supply chains.

The downstream energy storage revolution is fully underway, and its long-term commercial success is completely dependent on the upstream battery chemical companies that fuel it. Investors who recognize this structural reality today are positioning themselves at the center of the clean energy transition's most valuable sector.