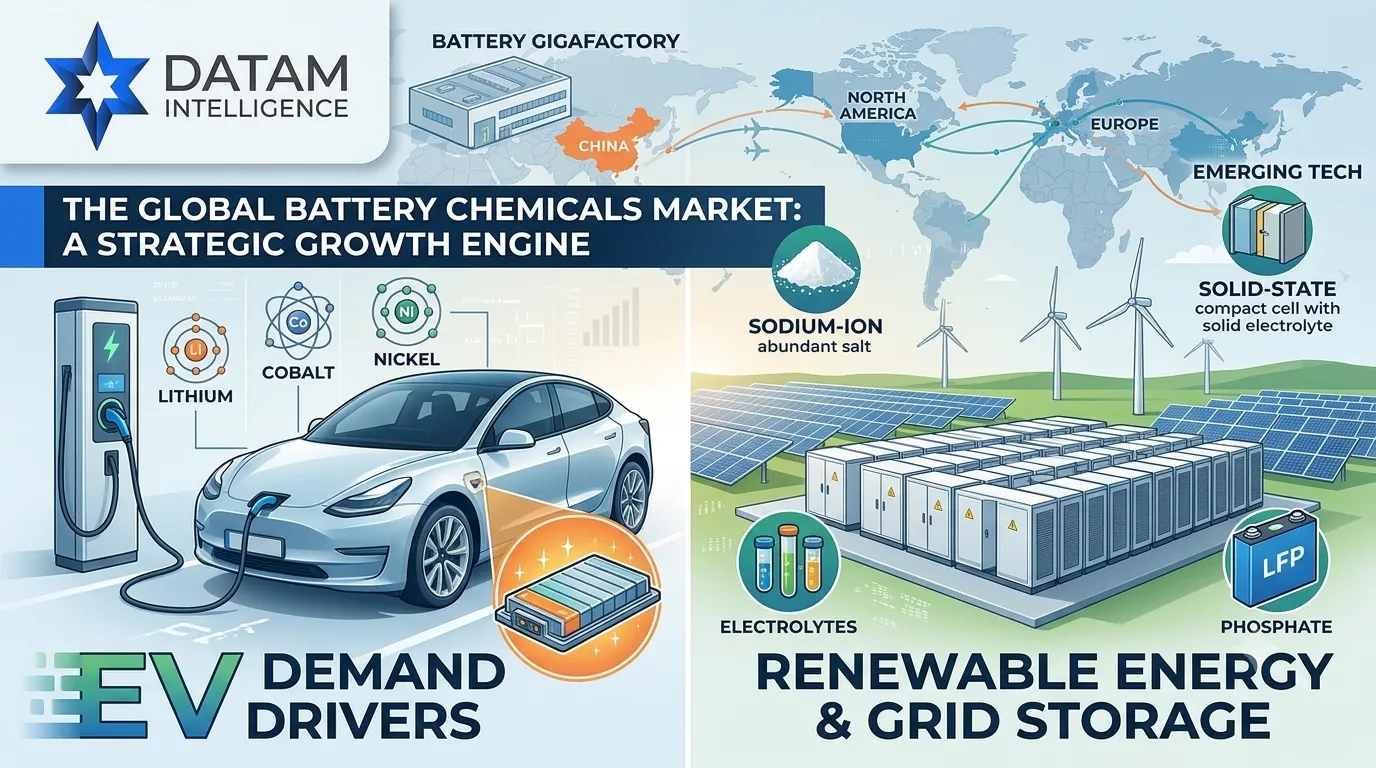

The global battery industry is undergoing one of the largest industrial transformations of the decade. As electric vehicles become mainstream and renewable energy deployment accelerates, battery chemicals have emerged as a strategic growth market powering the next generation of mobility and energy infrastructure.

Battery chemicals including lithium compounds, cathode active materials, electrolytes, anode materials, binders, conductive additives, and specialty performance chemicals are no longer viewed as commodity inputs. They are becoming critical enablers of battery performance, safety, energy density, charging speed, and cost competitiveness.

According to DataM Intelligence, the global battery chemicals market reached approximately US$82.75 billion in 2025 and is projected to expand to US$257.01 billion by 2035, growing at a CAGR of 12% during the forecast period. The growth is primarily fueled by EV adoption, energy storage deployment, battery gigafactory investments, and next-generation battery innovation.

Get Exclusive Insights into the Future of the Battery Chemicals Market

Understand the key market trends, growth opportunities, competitive landscape, and strategic developments shaping the global battery chemicals industry. Download the Battery Chemicals Market free sample report to access valuable insights on lithium chemicals, electrolyte materials, cathode and anode technologies, emerging battery chemistries, and market opportunities through 2035.

Why Battery Chemicals Have Become Strategic Assets

The battery industry has evolved beyond simple cell manufacturing. Today, battery performance is heavily influenced by chemical engineering and material science.

Battery manufacturers are competing on:

- Higher energy density

- Faster charging capability

- Improved thermal stability

- Longer cycle life

- Lower production costs

- Enhanced sustainability

Achieving these goals requires continuous innovation in battery chemistry. As a result, demand is increasing for:

- Lithium carbonate and lithium hydroxide

- Cathode active materials

- Electrolyte salts and solvents

- Graphite and silicon-based anodes

- Conductive additives

- Battery recycling feedstocks

Suppliers capable of delivering high-purity, performance-optimized materials are becoming essential partners within the battery value chain.

Electric Vehicles Remain the Largest Demand Driver for Battery Chemicals

The global transition toward electric mobility has become the most significant catalyst for the growth of the battery chemicals market. As countries implement stricter emissions regulations, governments introduce EV incentives, and automakers accelerate their electrification strategies, demand for advanced battery materials continues to expand rapidly.

Electric vehicles require high-performance batteries capable of delivering greater driving range, faster charging, improved safety, and longer operational life. These requirements are directly increasing consumption of critical battery chemicals, including lithium compounds, cathode active materials, electrolyte solutions, graphite-based anode materials, conductive additives, and specialty chemical formulations.

Automotive manufacturers and battery producers are investing billions of dollars into EV manufacturing facilities, battery gigafactories, and regionalized supply chains to secure access to critical materials. This expansion is creating significant opportunities across the battery chemicals ecosystem, from raw material suppliers and chemical manufacturers to battery technology developers.

Key trends accelerating battery chemical demand in the EV sector include:

1. Growth in Global EV Production Volumes

The rapid increase in electric vehicle production worldwide is one of the primary factors driving demand for battery chemicals. Automakers are expanding their EV portfolios across passenger vehicles, commercial fleets, buses, and two-wheelers to meet rising consumer adoption and regulatory requirements.

As EV sales continue to grow across major markets such as China, Europe, and North America, battery manufacturers are scaling production capacity through new gigafactory developments and expansion projects. This growth directly increases demand for essential battery materials, including:

- Lithium compounds: Lithium carbonate and lithium hydroxide required for lithium-ion battery production.

- Cathode materials: Nickel, cobalt, manganese, iron phosphate, and other active materials that determine battery performance.

- Electrolyte chemicals: Solvents, salts, and additives that enable efficient ion movement within battery cells.

- Anode materials: Graphite, silicon-based materials, and other advanced solutions that improve energy storage capacity.

The expansion of EV manufacturing creates a multiplier effect across the battery chemicals supply chain, increasing the need for high-purity materials, advanced formulations, and reliable long-term supply agreements.

2. Shift Toward Cost-Efficient Battery Chemistries

Battery manufacturers are increasingly adopting cost-effective and durable battery chemistries to improve EV affordability while maintaining safety and performance. Among these technologies, Lithium Iron Phosphate (LFP) batteries have gained significant market traction due to their economic and technical advantages.

LFP batteries are becoming increasingly popular in electric vehicles and energy storage applications because of their:

- Lower manufacturing costs compared with nickel-rich battery chemistries.

- Enhanced thermal stability and safety performance.

- Longer cycle life, making them suitable for high-use applications.

- Reduced dependence on expensive metals such as nickel and cobalt.

In 2025, LFP batteries accounted for approximately 42.7% of the battery chemicals market, making them one of the leading battery chemistries globally. The growing adoption of LFP technology is increasing demand for lithium compounds, iron phosphate materials, electrolyte chemicals, and other supporting battery components.

This shift toward cost-efficient chemistries is also influencing investment strategies across the battery supply chain, with manufacturers focusing on scalable production, material availability, and cost optimization.

3. Rising Demand for Fast-Charging and High-Performance Batteries

Consumer expectations for electric vehicles are rapidly evolving, with buyers seeking longer driving ranges, shorter charging times, and improved battery durability. These requirements are accelerating innovation in battery chemistry and increasing demand for advanced battery materials.

To enhance charging performance and energy density, battery manufacturers are investing in next-generation chemical solutions, including:

- Advanced electrolyte formulations designed to improve ion conductivity, charging speed, and thermal stability.

- Silicon-enhanced anode materials that offer higher energy storage capacity compared with traditional graphite anodes.

- High-performance cathode materials that enable greater energy density and improved battery efficiency.

- Specialty battery additives that enhance cycle life, safety, and overall battery performance.

The growing competition among EV manufacturers to deliver superior vehicle performance is expected to drive continued investment in advanced battery chemical technologies. As battery technology evolves, demand for innovative chemical solutions will remain a critical growth factor for the global battery chemicals market.

Strategic Impact on the Battery Chemicals Market

The expansion of the electric vehicle industry is transforming battery chemicals into a strategically important sector within the global energy transition. As EV adoption accelerates, companies involved in the development, production, and supply of advanced battery materials are positioned to benefit from long-term market growth.

Key opportunities emerging from EV-driven battery chemical demand include:

- Expansion of lithium chemical production capacity.

- Development of advanced cathode and anode materials.

- Innovation in electrolyte technologies.

- Growth of localized battery supply chains.

- Increased investment in sustainable battery material production and recycling.

With electric mobility expected to remain a major growth engine over the coming decade, battery chemicals will continue to play a critical role in enabling the next generation of electric vehicles and supporting global decarbonization goals.

Energy Storage Systems Are Creating a Second Demand Wave

While EVs dominate battery demand today, utility-scale and commercial energy storage systems are rapidly emerging as a major growth engine.

Grid operators increasingly rely on battery storage to:

- Balance renewable energy generation

- Improve grid stability

- Reduce peak demand costs

- Support energy resilience

As solar and wind installations expand globally, battery energy storage systems (BESS) are becoming indispensable infrastructure assets. Industry forecasts indicate substantial growth in global energy storage deployments over the next decade.

This trend is significantly increasing demand for:

- LFP cathode materials

- Electrolyte chemicals

- Graphite anodes

- Battery additives

- Thermal management chemicals

Energy storage applications also favor battery chemistries that prioritize safety, cycle life, and cost efficiency, further accelerating adoption of LFP-based systems.

Electrolyte Chemicals Are Emerging as a High-Growth Segment

Among all battery chemical categories, electrolytes are experiencing some of the fastest growth.

Electrolytes play a crucial role in:

- Ion transport

- Battery efficiency

- Charging performance

- Thermal stability

- Safety characteristics

According to DataM Intelligence, electrolyte chemicals are projected to be the fastest-growing product segment, with a CAGR of approximately 15.3%.

As battery manufacturers pursue faster charging and higher energy density, electrolyte innovation is becoming a major area of R&D investment. Advanced electrolyte systems are expected to be essential for next-generation lithium-ion, sodium-ion, and solid-state batteries.

Emerging Battery Chemistries Are Expanding Demand for Advanced Battery Chemicals

The future growth of the battery chemicals market is not limited to conventional lithium-ion technologies. While lithium-ion batteries currently dominate electric vehicles and energy storage applications, increasing demand for higher performance, improved safety, cost reduction, and supply chain diversification is accelerating the development of alternative battery chemistries.

Emerging technologies such as sodium-ion batteries and solid-state batteries are creating new opportunities for chemical manufacturers, material suppliers, and technology developers. These next-generation battery systems require innovative materials, advanced electrolytes, specialized cathode formulations, and novel anode solutions, further expanding the scope of the global battery chemicals industry.

As battery manufacturers explore alternatives to traditional chemistries, demand is expected to increase for a broader range of raw materials and specialty chemicals that can support improved battery efficiency, scalability, and sustainability.

Sodium-Ion Batteries: Creating New Opportunities Beyond Lithium-Based Systems

Sodium-ion batteries are emerging as a promising alternative to lithium-ion technology, particularly for applications where cost efficiency, resource availability, and supply chain stability are critical factors.

Unlike lithium, sodium is widely available globally and can be sourced from more abundant raw materials. This advantage has attracted significant interest from battery manufacturers seeking to reduce dependence on lithium supply chains and mitigate exposure to raw material price fluctuations.

Sodium-ion technology offers several key advantages:

- Reduced dependence on lithium resources: Sodium-ion batteries use sodium-based materials, helping manufacturers diversify battery material supply chains and reduce reliance on lithium markets.

- Greater raw material availability: Sodium is one of the most abundant elements, providing long-term resource security compared with limited critical minerals used in some lithium-ion chemistries.

- Improved supply chain resilience: The availability of sodium-based materials can support regional battery production and reduce geopolitical risks associated with concentrated mineral supply chains.

- Attractive economics for stationary energy storage: Sodium-ion batteries are particularly suitable for grid-scale energy storage applications where cost, safety, and cycle life are more important than achieving maximum energy density.

The commercialization of sodium-ion batteries is creating new demand opportunities across multiple chemical segments, including:

- Sodium-based cathode materials that determine battery capacity and performance.

- Hard carbon anode materials designed to improve sodium-ion storage efficiency.

- Advanced electrolyte formulations optimized for sodium-ion chemistry.

- Specialized additives and conductive materials that enhance battery stability and operational life.

As battery manufacturers continue to improve sodium-ion performance and production scalability, this technology is expected to complement lithium-ion systems in specific applications, especially large-scale energy storage and cost-sensitive mobility markets.

Solid-State Batteries: Driving Innovation in Advanced Electrolyte Materials

Solid-state batteries represent one of the most promising next-generation battery technologies, offering the potential to overcome several limitations associated with conventional lithium-ion batteries.

Unlike traditional lithium-ion batteries that use liquid electrolytes, solid-state batteries utilize solid electrolytes, which can improve safety, energy density, and battery performance. The development of this technology is driving significant research into advanced materials, specialty chemicals, and next-generation electrolyte systems.

Solid-state batteries are expected to deliver several important advantages:

- Higher energy density: Solid-state designs can potentially store more energy within a smaller and lighter battery pack, enabling longer driving ranges for electric vehicles.

- Improved safety: Solid electrolytes reduce risks associated with liquid electrolyte leakage, flammability, and thermal runaway events.

- Faster charging capability: Advanced solid electrolyte materials may enable faster ion movement, supporting shorter charging times.

- Longer battery lifespan: Improved chemical stability can help extend battery cycle life and maintain performance over extended usage periods.

The commercialization of solid-state batteries is creating significant opportunities for suppliers involved in advanced battery chemicals, including:

- Solid electrolyte materials such as sulfide, oxide, and polymer-based systems.

- High-performance cathode materials.

- Lithium metal-compatible anode solutions.

- Specialty additives that improve conductivity and stability.

As automotive manufacturers and battery developers continue investing in solid-state technology, suppliers with expertise in advanced chemical formulations and high-purity materials are expected to play a critical role in accelerating commercialization.

Regional Supply Chain Localization Is Accelerating Demand

Governments worldwide are increasingly prioritizing battery supply chain security.

Major economies are investing heavily in:

- Domestic battery manufacturing

- Critical mineral processing

- Cathode and anode production

- Recycling infrastructure

This localization trend is generating demand for battery chemicals across North America, Europe, and Asia-Pacific.

Asia-Pacific currently dominates the battery chemicals market, accounting for more than 61% of global demand due to its extensive battery manufacturing ecosystem and processing capabilities.

At the same time, North America and Europe are rapidly expanding local production capacity to reduce dependence on imported materials and strengthen supply chain resilience.

Why Investors Are Watching Battery Chemicals Closely

Investors increasingly recognize that the greatest value creation opportunity may not lie solely in battery manufacturing but in the upstream materials ecosystem.

Key investment themes include:

- Lithium refining

- LFP precursor materials

- Electrolyte manufacturing

- Silicon anode technology

- Battery recycling

- Graphite processing

- Sodium-ion material development

As battery deployment scales globally, material suppliers capable of meeting stringent purity, consistency, and sustainability requirements could capture significant long-term value.

Challenges Facing the Battery Chemicals Industry

Despite strong growth opportunities driven by electric vehicle (EV) adoption, energy storage expansion, and battery technology innovation, the battery chemicals industry continues to face several structural and operational challenges. The increasing complexity of battery supply chains, fluctuations in raw material availability, sustainability expectations, and rapid technological changes are creating new risks for manufacturers, investors, and material suppliers.

As the battery ecosystem expands, companies across the value chain must address these challenges to ensure reliable supply, maintain cost competitiveness, and support the transition toward sustainable energy technologies.

Raw Material Price Volatility

One of the most significant challenges facing the battery chemicals industry is the volatility of raw material prices. Critical battery materials such as lithium, nickel, cobalt, and graphite are highly influenced by global supply-demand dynamics, mining capacity, geopolitical conditions, and market speculation.

The rapid growth of electric vehicles and energy storage systems has created strong demand for these materials, but supply expansion often requires significant investment, long development timelines, and complex regulatory approvals. This imbalance between demand growth and supply availability can result in considerable price fluctuations.

Key factors contributing to raw material volatility include:

- Fluctuating lithium prices: Rapid EV adoption has increased demand for lithium compounds, while new mining and refining projects require several years to reach commercial production.

- Nickel and cobalt supply risks: Battery manufacturers using high-nickel chemistries remain exposed to price movements and supply constraints associated with these metals.

- Graphite market uncertainty: Natural graphite supply is affected by mining concentration, processing capacity, and export policies in major producing regions.

- Changing battery chemistry preferences: Shifts between nickel-rich batteries, LFP batteries, and emerging chemistries can significantly influence demand patterns for specific materials.

To manage these risks, battery manufacturers and chemical suppliers are increasingly focusing on long-term supply agreements, diversified sourcing strategies, and investments in alternative materials and recycling technologies.

Increasing Sustainability Requirements

Sustainability has become a critical priority across the battery chemicals value chain. As demand for batteries grows, manufacturers face increasing pressure from governments, customers, and investors to reduce environmental impacts associated with mining, processing, and battery production.

Battery chemical producers are being evaluated not only on product performance but also on their environmental footprint, ethical sourcing practices, and ability to provide transparent supply chains.

Major sustainability challenges include:

- High energy consumption during chemical processing: Production of battery-grade materials often requires significant energy inputs, creating pressure to adopt cleaner energy sources.

- Environmental impact of mining operations: Extraction of lithium, nickel, cobalt, and graphite can create concerns related to water usage, land degradation, and ecosystem disruption.

- Demand for material traceability: Automakers and battery manufacturers increasingly require visibility into the origin and processing history of raw materials.

- Circular economy requirements: Growing emphasis on battery recycling is driving investment in technologies that recover valuable materials and reduce dependence on primary resources.

Companies that can develop low-carbon production methods, improve resource efficiency, and establish transparent supply chains are expected to gain competitive advantages as sustainability regulations become stricter globally.

Supply Chain Concentration and Geopolitical Risks

The battery chemicals industry remains highly dependent on a limited number of countries for the extraction, processing, and refining of critical materials. This concentration creates supply chain vulnerabilities and increases exposure to geopolitical uncertainties, trade restrictions, and regulatory changes.

Several battery materials face significant supply chain concentration risks:

- Lithium processing: A large share of global lithium refining capacity is concentrated in a few major markets, creating dependency concerns for battery manufacturers.

- Cobalt supply: Cobalt production remains geographically concentrated, increasing concerns related to supply security and ethical sourcing.

- Graphite processing: The graphite supply chain is particularly vulnerable due to the concentration of natural graphite mining and processing capabilities in specific regions.

These supply chain challenges are encouraging governments and companies to pursue strategies such as:

- Developing domestic battery material production capabilities.

- Establishing regional battery supply chains.

- Investing in alternative materials.

- Expanding battery recycling infrastructure.

- Creating strategic partnerships with mining and chemical companies.

Building a more diversified and resilient supply chain will remain a key priority as global battery demand continues to increase.

Technology Transition Risks

The rapid evolution of battery technology creates both opportunities and challenges for battery chemical manufacturers. While innovation is driving demand for advanced materials, it also creates uncertainty regarding which battery chemistries will dominate future markets.

Battery manufacturers are continuously exploring alternatives to improve cost, performance, safety, and sustainability. These developments can significantly impact demand for specific chemicals and materials.

Technology transition risks include:

- Changing material requirements: A shift from nickel-based batteries to LFP technology, for example, can reduce demand for certain materials while increasing demand for others.

- Emergence of alternative chemistries: Sodium-ion and solid-state batteries could create new material requirements and disrupt existing supply chains.

- Investment challenges: Chemical manufacturers must balance investments in current technologies while preparing for future battery platforms.

- Shorter innovation cycles: Faster advancements in battery technology require suppliers to continuously upgrade production capabilities and develop new chemical formulations.

To remain competitive, battery chemical companies must maintain strong research and development capabilities, develop flexible manufacturing systems, and closely monitor technological trends across the battery ecosystem.

Strategic Outlook for the Battery Chemicals Industry

While these challenges create uncertainty, they also present opportunities for companies capable of adapting to market changes. The future success of battery chemical suppliers will depend on their ability to secure raw material access, improve sustainability performance, diversify supply chains, and innovate alongside evolving battery technologies.

Companies that successfully address these challenges through advanced manufacturing processes, recycling solutions, sustainable sourcing, and next-generation material development will be better positioned to capture long-term growth opportunities in the expanding global battery market.

Future Outlook: Battery Chemicals Become the Foundation of Electrification

The next decade will be defined by electrification, renewable energy integration, and large-scale energy storage deployment.

Every EV produced, every solar farm connected, and every grid storage project commissioned increases demand for specialized battery chemicals.

The industry's future will be shaped by:

- Growth in EV adoption

- Expansion of energy storage systems

- Rising LFP battery deployment

- Sodium-ion commercialization

- Solid-state battery innovation

- Supply chain localization

- Recycling and circular economy initiatives

Companies positioned within the battery chemicals value chain stand to benefit from one of the most significant industrial growth opportunities of the energy transition era. As global demand for batteries continues to accelerate, battery chemicals will remain the foundational building blocks enabling cleaner transportation, smarter grids, and a more resilient energy future.

What is driving demand for battery chemicals?

Demand for battery chemicals is being driven by rapid growth in electric vehicles (EVs), battery energy storage systems (BESS), battery gigafactory investments, and next-generation battery technologies. Increased production of lithium-ion, LFP, sodium-ion, and solid-state batteries requires greater volumes of lithium compounds, cathode materials, electrolytes, and advanced battery additives.