From Laboratory to Industrial Qualification

How buyers evaluate next generation advanced materials

Advanced materials are moving from research labs into a more demanding commercial environment. Buyers in aerospace, automotive, electronics and energy are interested in stronger, lighter, more heat resistant and more sustainable materials, yet they are also becoming more selective. A material that performs well in a lab sample still has to prove repeatability, manufacturability, regulatory readiness, supply security and cost visibility before it can enter a qualified industrial platform.

This is the real qualification challenge for next generation advanced materials. Discovery is getting faster because AI, high throughput experimentation and materials data platforms are expanding the number of candidate materials. Industrial adoption remains controlled by practical buyer questions. Can the supplier make the same material at scale. Can the material survive the customer production line. Can it meet standards, documentation requirements and lifecycle expectations. Can it reduce risk across a multi year product program.

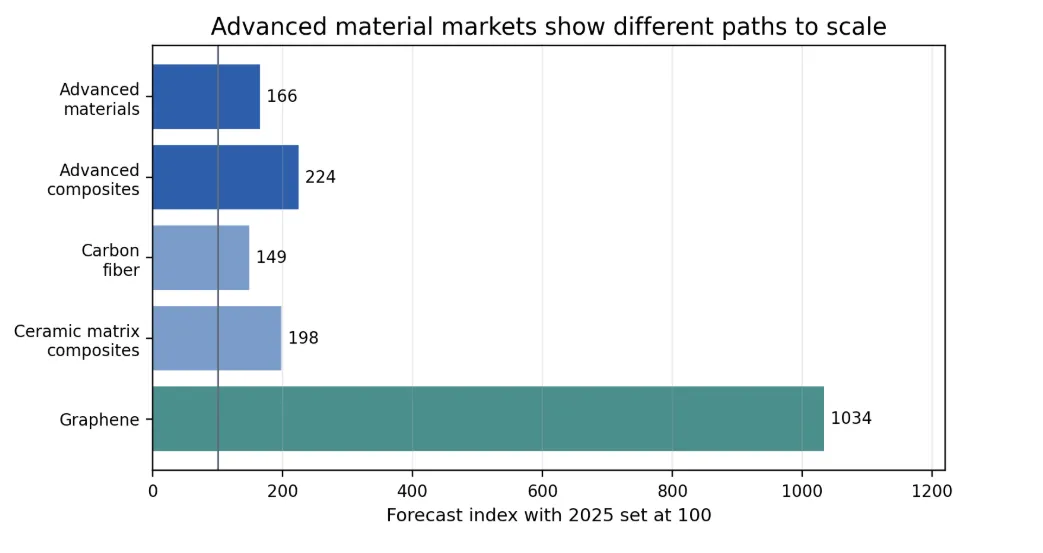

DataM Intelligence estimates that the global advanced materials market reached USD $73.92 billion in 2025 and will reach USD $132.34 billion by 2035. This growth reflects rising demand from sectors that need performance gains without adding weight, energy use or operating complexity. The strongest commercial opportunities will concentrate in materials that can move through qualification gates with proof, consistency and buyer confidence.

Explore the Advanced Materials Market Report

Gain deeper insights into market trends, growth opportunities, demand drivers, and emerging applications across advanced ceramics, composites, fibers, nanomaterials, resins, and polymers shaping the future of industrial innovation.

Data source DataM Intelligence report pages for advanced materials, advanced composites, carbon fiber, ceramic matrix composites and graphene. Forecast values are indexed to 2025.

Why the qualification gate is becoming the real adoption bottleneck

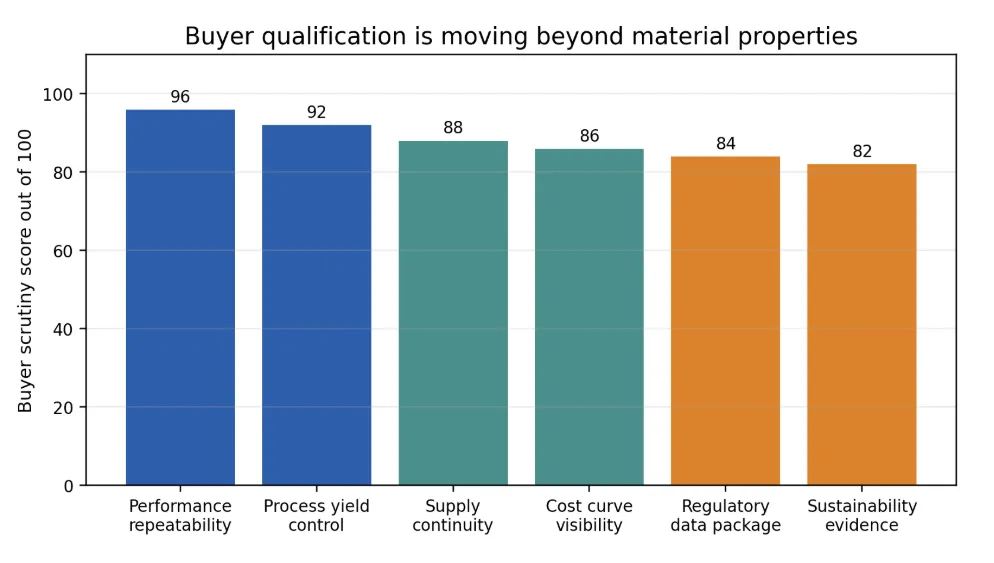

The advanced materials market is full of promising technologies, but buyers rarely approve a new material because of a single performance claim. Qualification decisions are usually made by cross functional teams that include engineering, procurement, quality, manufacturing and sustainability leaders. Each group evaluates a different type of risk, which makes industrial adoption slower than laboratory validation.

Engineering teams focus on strength, thermal stability, conductivity, fatigue performance and environmental resistance. Manufacturing teams focus on yield, process compatibility, waste rates and line downtime. Procurement teams focus on supplier capacity, secondary sourcing, price volatility and long term availability. Quality teams focus on standards, traceability, test methods and field failure risk. A material must satisfy all of these groups before it can become part of an industrial program.

This is why the strongest suppliers are building qualification packages instead of selling material samples. Buyers want full data sets, pilot scale evidence, validated processing windows and proof that the supplier can support production demand over the life of a platform. The commercial value is shifting toward companies that can connect material science with process engineering and documentation discipline.

Author assessment based on buyer qualification criteria used in industrial material adoption.

From material properties to production repeatability

The first buyer question is usually about repeatability. A material may deliver strong performance in one test coupon, but buyers need to know whether the same result can be reproduced across multiple batches, production runs and operating environments. For aerospace structures, battery materials, semiconductor chemicals or high temperature components, small variation can create large performance risk.

This makes process control a central part of the value proposition. Suppliers need statistical evidence on purity, morphology, strength, conductivity, thermal behavior and defect levels. They also need to explain how those properties change under real manufacturing conditions. A material that depends on fragile laboratory methods will struggle unless the process can be translated into robust industrial production.

Carbon fiber shows why this matters. DataM Intelligence estimates the carbon fiber market reached USD $24.18 billion in 2025 and could reach USD $40.97 billion by 2035. The market benefits from demand in aerospace, wind energy and mobility, but buyer adoption depends on tow quality, resin compatibility, production consistency, recycling pathways and long term supplier confidence.

Get the Carbon Fiber Market Insights Report

Access comprehensive insights into carbon fiber market trends, demand growth, key suppliers, application areas, production developments, and emerging opportunities across aerospace, automotive, energy, and advanced manufacturing industries.

Pilot scale manufacturing is where many materials lose momentum

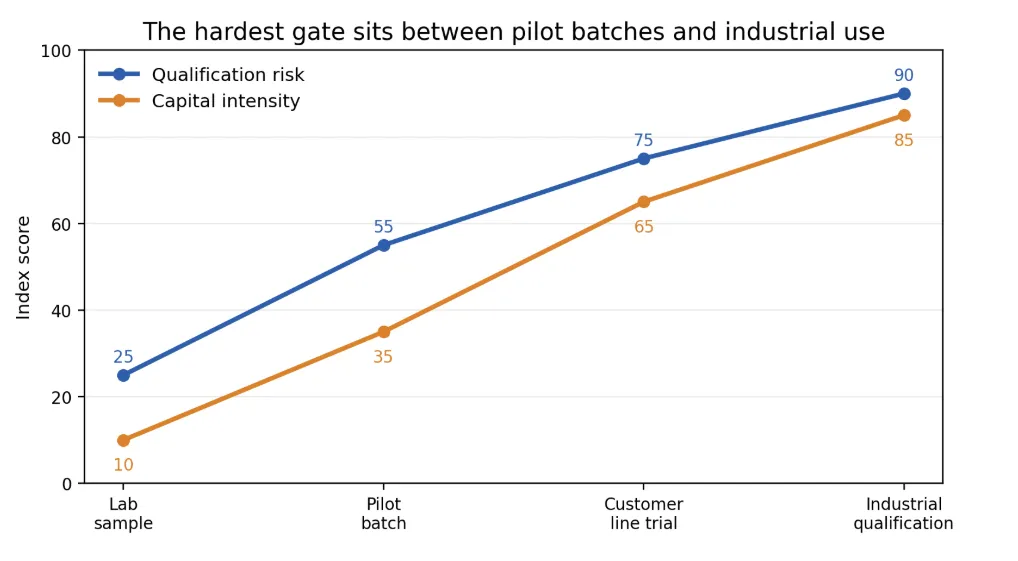

The move from grams to kilograms or from kilograms to tonnes is often where next generation materials face their hardest test. Pilot production exposes problems that laboratory work can hide. Inputs vary, equipment behaves differently, reaction times change, defects appear and quality control becomes more difficult. Buyers treat this stage as a stress test for the supplier as much as the material.

This is especially important for advanced composites and ceramic matrix composites.. Both markets are expanding because buyers need weight reduction, heat resistance and durability, although qualification demands remain high.

For composites, buyers evaluate fiber availability, resin chemistry, cure cycle control, automation fit and repairability. For ceramic matrix composites, they evaluate high temperature performance, oxidation resistance, process yield, inspection methods and lifecycle cost. The supplier that can explain manufacturability clearly often has a stronger commercial position than the supplier with the best isolated lab result.

Access the Advanced Composites Market Analysis

Gain comprehensive insights into advanced composites adoption trends, market growth drivers, key applications, and industry developments across aerospace, automotive, energy, and industrial sectors.

Author assessment of risk and capital intensity during advanced material qualification.

High temperature materials face the strictest proof requirements

Materials used in hot zones, aircraft engines, power systems and industrial thermal equipment face some of the strictest buyer scrutiny. These applications require high confidence because failure can affect safety, downtime and warranty exposure. Buyers want data across temperature cycling, oxidation, creep, fatigue, shock resistance and inspection reliability.

Ceramic matrix composites are a good example of this qualification challenge. Their value comes from lightweight performance at high temperatures, which can improve efficiency in engines and energy systems. Their adoption still depends on production yield, joining methods, nondestructive inspection, repair pathways and long term field evidence. A supplier must prove the material works as part of a system, with manufacturing and maintenance realities included.

The near term winners in this part of the market will likely be suppliers that can support joint engineering programs with OEMs. Buyers need materials partners that can provide design data, testing support, process knowledge and production planning. The qualification burden is high, but approved materials can become durable revenue streams once they enter mission critical platforms.

AI discovery is expanding the funnel before qualification catches up

AI is changing the front end of materials innovation. Google DeepMind reported that its GNoME system identified 2.2 million new crystal structures, including 380,000 stable candidates, while the Materials Genome Initiative describes a federal effort to accelerate advanced materials discovery, manufacturing and deployment. These programs show how digital tools can expand the discovery funnel dramatically.

The challenge is that more candidate materials also create more qualification work. Stability predictions and lab synthesis are important early signals, but buyers still need practical evidence on scale up, failure modes, process compatibility, raw material access, environmental impact and lifecycle economics. AI can help shorten screening cycles, but industrial qualification still requires real evidence from production relevant environments.

Graphene highlights this gap between promise and qualification. DataM Intelligence estimates the graphene market at USD 855.63 million in 2025 with a forecast of USD 8.85 billion by 2033. The growth potential is significant because graphene can support batteries, electronics, composites and coatings. Buyer adoption still depends on consistent grade definitions, dispersion control, purity, toxicology data and repeatable manufacturing processes.

Explore the Graphene Market Insights Report

Gain comprehensive insights into graphene demand, application trends, technology developments, and growth opportunities across electronics, energy storage, biomedical, and advanced composite industries.

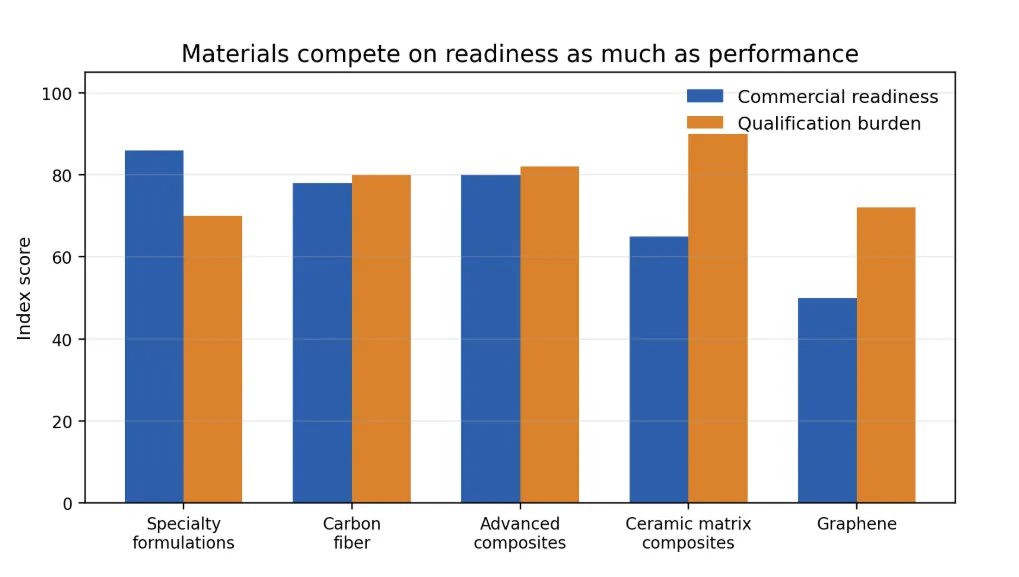

Author assessment comparing material platform readiness and qualification burden in industrial use cases.

Cost visibility is becoming a qualification requirement

Buyers are increasingly asking suppliers to show a credible cost curve. In early stage materials, unit economics can look unrealistic because yields are low, equipment is specialized and production volumes are limited. Industrial buyers understand this, but they want evidence that costs can decline as throughput improves.

A cost curve needs more than a future pricing target. It needs assumptions on raw materials, process yield, energy use, labor intensity, equipment utilization and scrap recovery. Buyers also want to understand whether cost reduction depends on uncertain capacity expansion or on process improvements that are already being demonstrated.

This is important in automotive, consumer electronics and construction, where material substitution decisions are highly cost sensitive. A next generation material may offer better strength, lower weight or improved thermal behavior, but it still needs a business case that survives procurement review. Performance opens the door, while credible economics keeps the material in the program.

Traceability and sustainability are becoming part of buyer approval

Advanced materials buyers are also placing more weight on traceability and sustainability. Aerospace and defense buyers want secure supply and documented provenance. Electronics buyers want tighter control of chemical inputs, emissions and restricted substances. Automotive buyers want lifecycle data that can support lower carbon claims and circularity targets. Energy buyers want materials that can withstand long operating lives with fewer replacement cycles.

This creates a new documentation burden for suppliers. Material qualification packages increasingly include carbon footprint data, recycled content evidence, responsible sourcing information, restricted substance declarations and end of life considerations. These requirements can slow adoption for suppliers that lack compliance infrastructure, although they can also create an advantage for companies with strong data systems.

The strongest suppliers will treat sustainability evidence as part of industrial qualification. Buyers are looking for materials that improve product performance while helping them manage regulatory exposure, customer commitments and procurement risk. This makes data quality, digital traceability and certification readiness part of the commercial offer.

Where buyers will move fastest through 2030

Buyer adoption will move fastest where the performance need is urgent and the business case is clear. Aerospace will continue to qualify lightweight and high temperature materials for efficiency and durability. Semiconductor manufacturing will demand ultra clean materials, coatings and chemicals that support advanced process nodes. EV platforms will need thermal materials, lightweight structures and battery adjacent components. Energy systems will require materials that support higher efficiency, longer life and harsher operating environments.

The common feature across these markets is that material value is tied to system performance. Buyers will approve next generation materials when they reduce weight, improve heat management, extend asset life or lower total cost of ownership. Materials that offer a performance gain without manufacturability evidence will face longer qualification cycles.

This is where advanced materials suppliers should focus their investment. Lab discovery should be connected early with pilot production, test method development, standards engagement and customer application engineering. Waiting until after a material is invented to plan industrial qualification adds time and risk.

Industrial qualification will decide the next advanced materials winners

The next advanced materials cycle will reward companies that can translate science into buyer confidence. The market has strong growth signals across advanced materials, composites, carbon fiber, ceramic matrix composites and graphene. The limiting factor is often the path from promising property data to qualified industrial use.

For material developers, the message is clear. Build qualification plans as early as discovery plans. Prove repeatability before customer trials. Invest in pilot scale manufacturing before large volume negotiations. Treat documentation, traceability and cost modeling as core product features.

For buyers, the opportunity is to engage earlier with suppliers that can solve specific performance bottlenecks. The best procurement teams will evaluate advanced materials through a structured lens that includes technical maturity, manufacturing readiness, supply resilience and lifecycle economics.

Advanced materials will continue to reshape aerospace, mobility, electronics, energy and industrial manufacturing. The companies that benefit most will be those that understand the central rule of the next cycle. Industrial qualification is where innovation becomes procurement reality.