From Waste Management to Resource Security

Why Circularity Is Emerging as a Strategic Procurement Priority in 2026

Circularity is moving into the purchasing function because materials have become strategic. The earlier corporate waste agenda focused on disposal, diversion and basic compliance. The 2026 agenda is broader because procurement teams are being asked to secure secondary materials, reduce exposure to volatile virgin inputs and build resilience into supply chains that face policy pressure, price swings and geopolitical disruption.

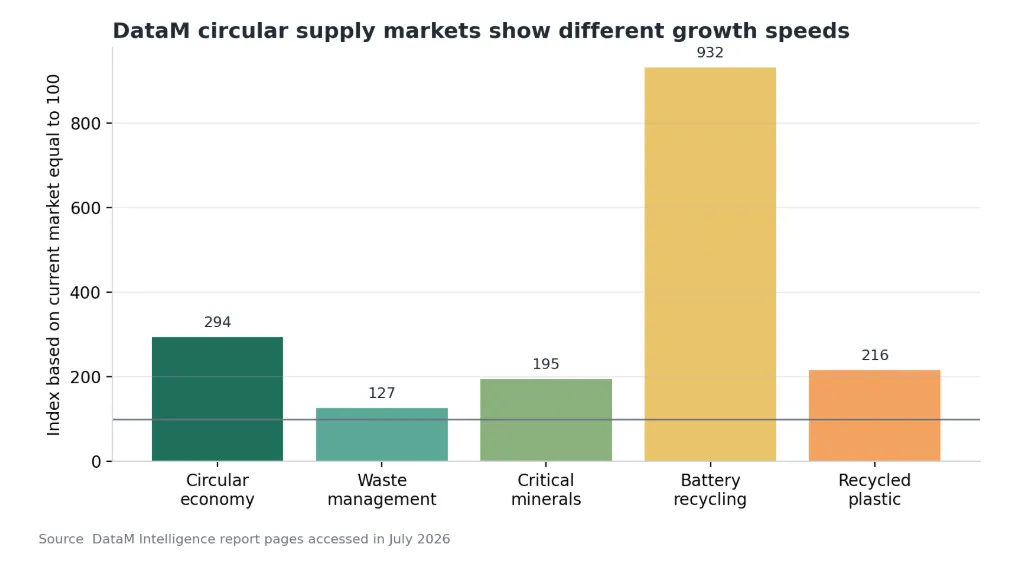

This shift is visible across packaging, batteries, electronics and critical minerals. Buyers that once treated recycled material as an environmental claim are now treating it as an input security tool. That matters because the world is still highly linear. Recent circularity analysis estimates that only 6.9 percent of the materials used by the global economy return as recycled inputs, while DataM Intelligence estimates the Circular Economy Market could grow from USD 166.95 billion in 2025 to USD 491.35 billion by 2035.

Explore the DataM Intelligence Circular Economy Market report

Circularity is becoming a sourcing discipline

The procurement logic is changing because circular materials can reduce dependence on fragile supply chains. Recycled polymers can reduce exposure to virgin resin volatility. Battery recycling can recover lithium, nickel, cobalt and manganese for future cell production. Electronics recovery can turn discarded devices into sources of copper, precious metals and specialty inputs. Industrial scrap can support lower carbon steel, aluminum and copper procurement.

The change is especially important for manufacturers that depend on strategic materials. In its 2025 critical minerals outlook, the International Energy Agency emphasized that price volatility, bottlenecks and geopolitical concentration make supply monitoring vital. That concern has moved directly into procurement. Companies are now building circular supply strategies to reduce import dependence, qualify secondary inputs and protect production schedules when primary material markets tighten.

Review the Critical Minerals Market Report for Strategic Sourcing Analysis

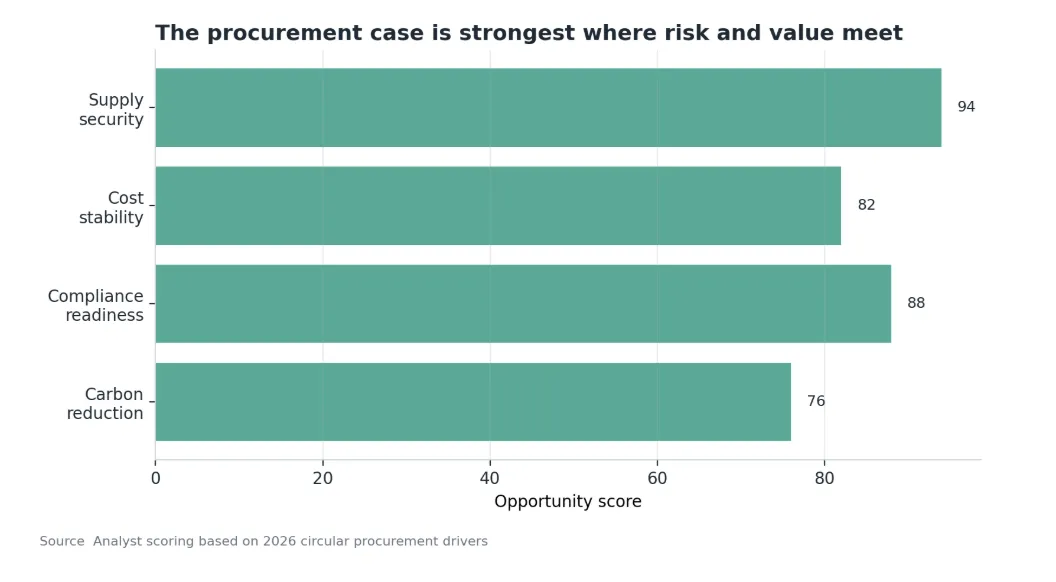

Waste costs are becoming board level commercial risks

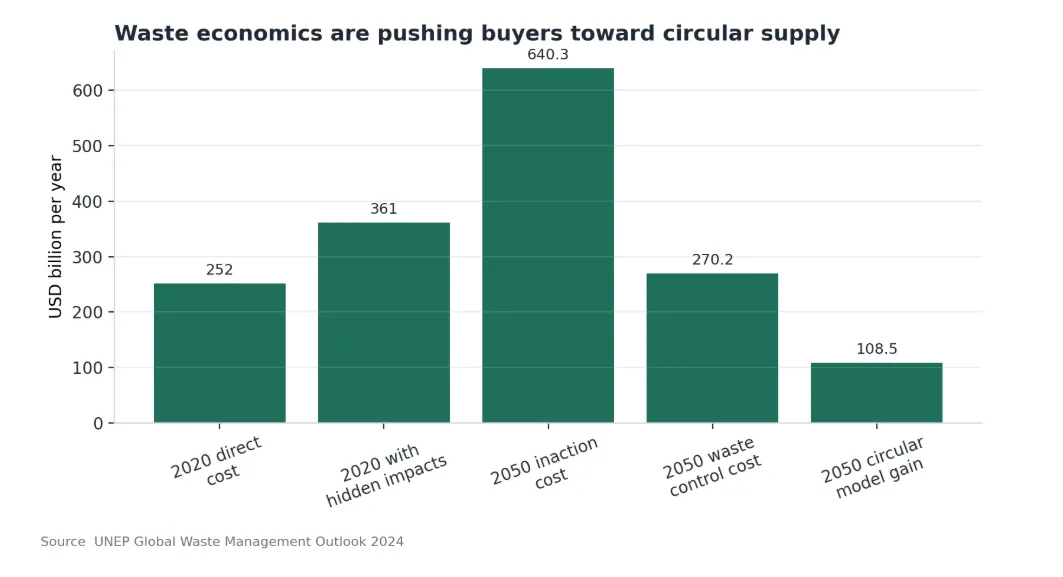

The financial case for circularity has strengthened because waste is becoming more expensive to ignore. UNEP estimates that municipal solid waste generation could rise from 2.1 billion tonnes in 2023 to 3.8 billion tonnes by 2050. The direct global cost of waste management was estimated at USD 252 billion in 2020, while the cost rises to USD 361 billion when pollution, health and climate impacts are included. Under an inaction scenario, annual costs could reach USD 640.3 billion by 2050.

These numbers matter for procurement because waste costs are increasingly embedded in supplier pricing, compliance fees, packaging obligations and product design requirements. Extended producer responsibility, recycled content rules and landfill diversion targets are pushing buyers to consider the full material lifecycle before they sign supplier contracts. Procurement teams that wait for disposal costs to appear at the end of the

Secondary materials are becoming strategic reserves

Circular procurement becomes most powerful when recovered material replaces an input that is expensive, constrained or exposed to policy risk. This is why batteries and critical minerals are moving quickly into the resource security discussion. DataM Intelligence estimates the Battery Recycling Market at USD 4.37 billion in 2026 and projects it to reach USD 40.72 billion by 2035. That growth reflects the rising value of recovered metals as electric vehicle batteries and energy storage systems begin to create larger end of life material streams.

Recycled plastics are following a different path. The drivers are compliance, brand commitments and packaging economics. DataM Intelligence estimates the Recycled Plastic Market will reach USD 62.81 billion in 2026 and grow to USD 135.89 billion by 2035. Procurement teams are now negotiating for food grade recycled PET, recycled polyethylene and higher quality recycled polypropylene because availability can determine whether packaging targets are achievable.

Download the Battery Recycling Market Sample for Circular Battery Supply Forecasts

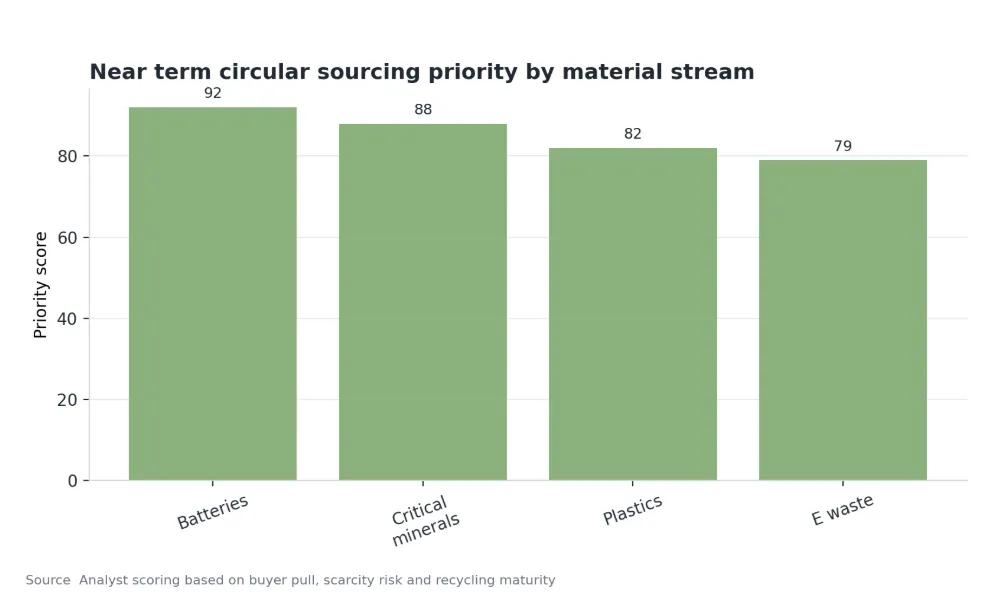

The strongest opportunities sit where scarcity meets scale

The highest priority circular sourcing pools in the near term are batteries, critical minerals, plastics and electronic waste. Each has a different value profile. Battery recycling is attractive because recovered materials can support future cell manufacturing. Critical minerals recovery is attractive because supply concentration creates geopolitical risk. Plastics circularity is attractive because regulation and brand commitments are already pulling demand. Electronic waste is attractive because valuable metals are embedded in fast growing device waste streams.

Explore the Recycled Plastic Market Report for Recycled Resin Demand Signals

Circular supply models will scale at different speeds because the economics depend on collection density, contamination levels, processing technology, quality standards and buyer qualification. Procurement teams therefore need to separate circularity claims from bankable feedstock. The winners will be suppliers that can provide consistent material quality, traceable origin, reliable volume and documented carbon or compliance benefit.

Contracts are changing before recycling capacity catches up

Circularity is now changing how procurement contracts are written. Buyers are adding recycled content requirements, traceability clauses, takeback provisions and long term offtake commitments. These terms are designed to solve a practical problem. Circular infrastructure needs predictable demand before investors can finance collection, sorting and processing capacity.

The contract shift is also visible in supplier qualification. Procurement teams increasingly want proof of material origin, chain of custody data, contamination thresholds and audit ready reporting. Digital product passports, material passports and recycling certification systems are becoming part of procurement infrastructure. These tools help buyers confirm that circular inputs are real, compliant and usable in regulated supply chains.

Resource security will reward integrated recovery platforms

The supplier landscape is moving toward integrated recovery platforms. Traditional waste companies are expanding into resource recovery, recyclers are moving closer to manufacturers and technology providers are improving sorting, tracing and processing performance. This creates opportunities for companies that can combine collection networks, processing assets, quality control and buyer access.

The market will also reward local and regional loops. Long global supply chains can undermine the resilience benefits of circularity when recovered material must travel across multiple regions before reuse. Regional recycling hubs, industrial symbiosis networks and closed loop supply agreements can reduce transport cost while improving material availability. This is why circularity is becoming a practical procurement strategy with measurable commercial value.

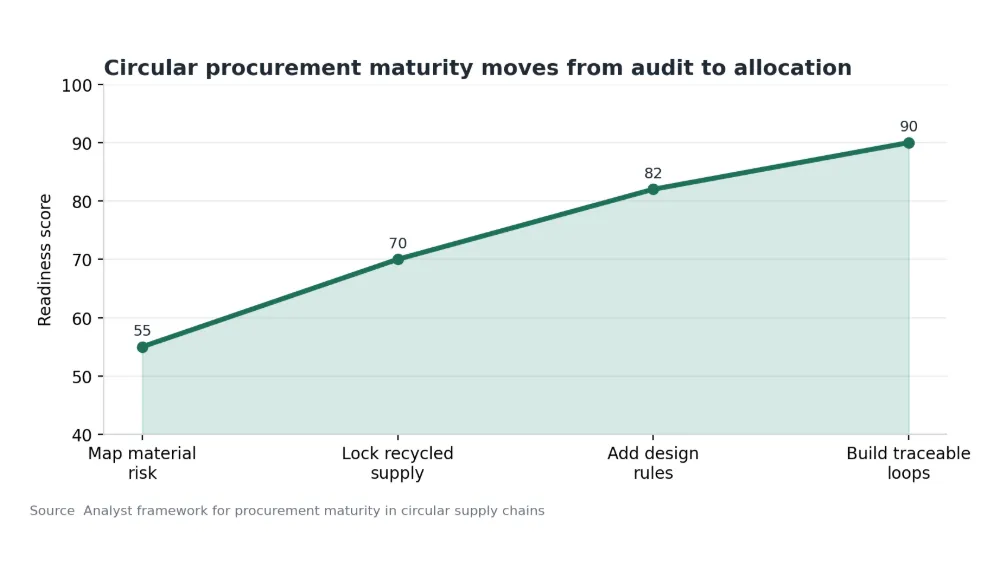

What procurement teams should build now

Procurement teams should begin with material risk mapping. The goal is to identify which inputs face the greatest exposure to price volatility, import dependence, regulation or end of life obligations. Once those inputs are ranked, buyers can decide where recycled content, reuse, repair, remanufacturing or takeback models offer the strongest commercial value.

The next step is supplier development. Circular supply chains require different capabilities from linear purchasing. Buyers need partners that can guarantee quality, document compliance and scale volumes over time. For strategic materials, long term offtake agreements may become as important as spot purchasing. For packaging, design for recyclability and recycled resin access must be managed together. For electronics and batteries, recovery programs should connect directly with future material needs.

Circularity is becoming a procurement strategy because companies need more secure access to materials. Waste reduction still matters, but the larger commercial opportunity is resource control. Companies that build circular procurement capabilities early will be better positioned to manage volatility, comply with new rules and capture value from materials that competitors still treat as waste.