A 2026 market article on where farm automation can create the earliest economic payback across spraying, weeding, drones, autonomous hauling, seeding, tractors and harvesting.

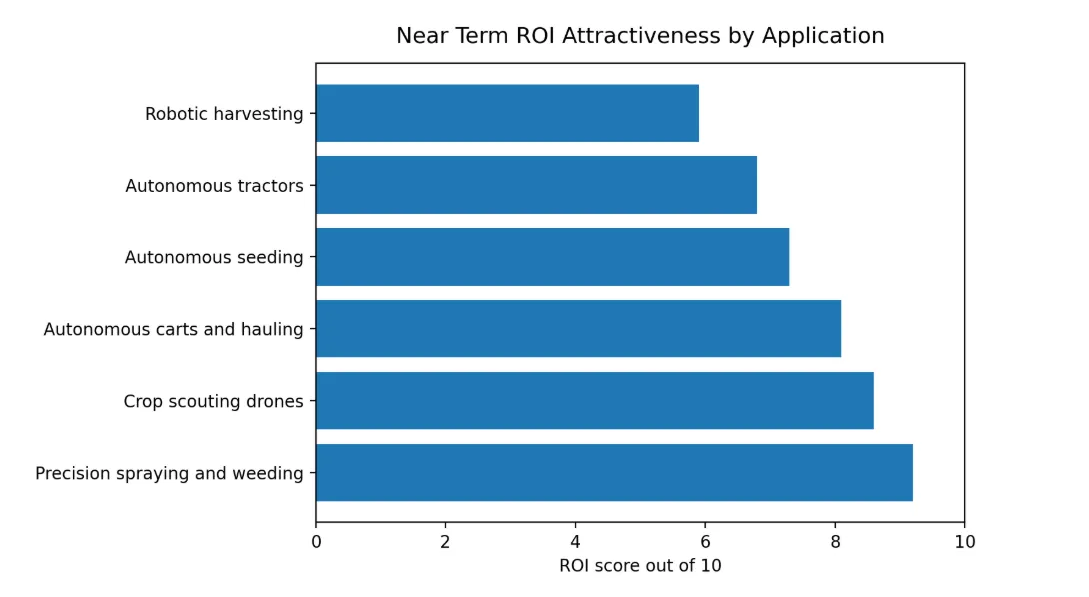

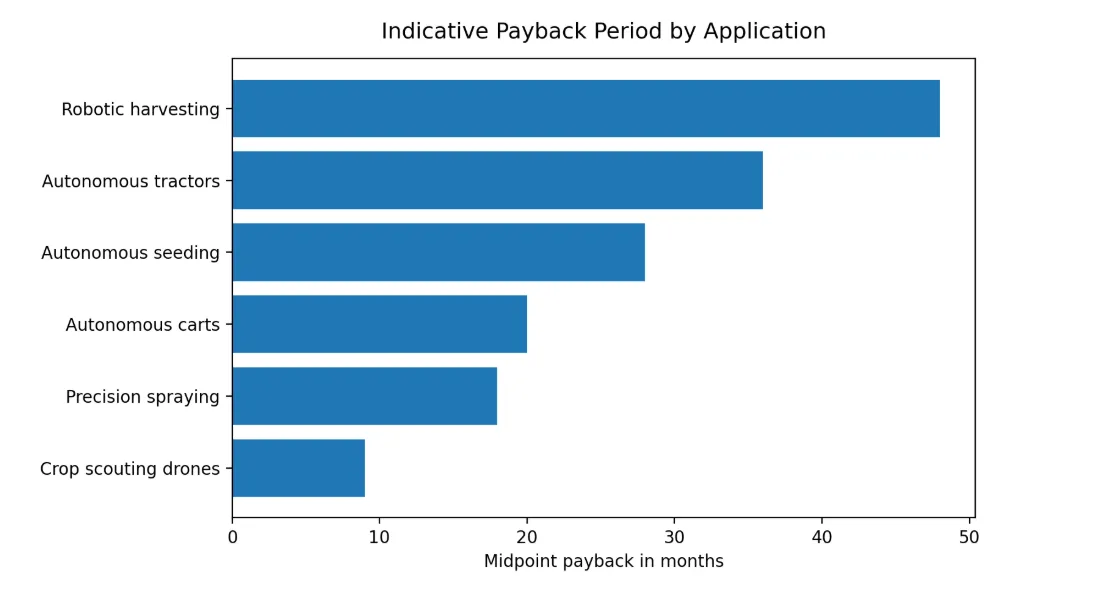

Autonomous farming equipment is moving from experimental deployment into ROI led adoption. The applications that can deliver the fastest returns are those that reduce repetitive field labor, cut chemical usage, extend operating windows and improve input accuracy without forcing growers to redesign the entire farm. In 2026, the strongest near term business case is emerging around precision spraying, autonomous weeding, drone based scouting and autonomous hauling. Full robotic harvesting and large scale autonomous tractors remain important, although payback can take longer because capital cost, crop variability and integration complexity remain higher.

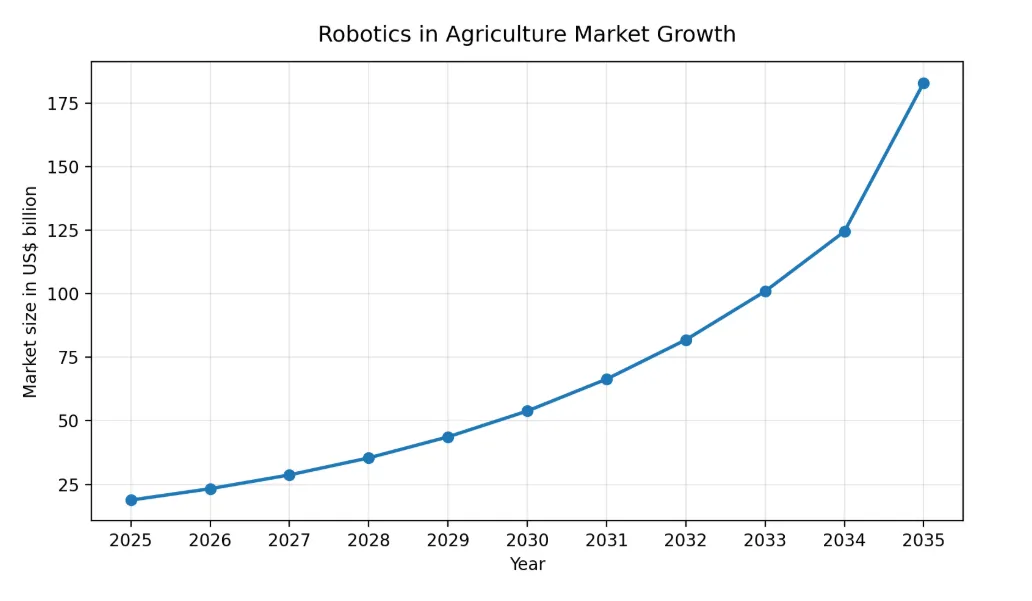

DataM Intelligence estimates the Robotics in Agriculture Market at US$ 23.31 billion in 2026, rising to US$ 183.03 billion by 2035 at a CAGR of 23.28%. The same shift is visible across agricultural drones, AI in agriculture, precision agriculture and autonomous farm equipment, where growers are prioritizing measurable savings over broad automation claims.

Explore the DataM Intelligence Robotics in Agriculture Market report.

Why ROI Is Becoming the Main Adoption Filter

Farmers are evaluating autonomous equipment in a more disciplined way in 2026. The question is no longer whether autonomy can work in a field environment. The sharper question is which application pays back quickly enough to justify capital deployment, operator training and service support. This is important because farms are facing higher input costs, persistent labor constraints, tighter residue rules and pressure to improve yield without expanding cultivated land.

The strongest ROI cases share four characteristics. They replace labor that is hard to schedule, they lower input usage in a measurable way, they work across many crop cycles, and they can be integrated into existing machinery or workflows. This is why precision spraying and autonomous weeding are ahead of many other categories. They create chemical savings, reduce rework and improve weed control at a time when herbicide resistance and labor availability are both becoming commercial concerns.

The autonomous farm equipment market is also becoming more buyer segmented. Large row crop farms are looking at autonomous tractors, variable rate application and high capacity spraying. Specialty crop farms are focusing on weeding, scouting, harvesting support and autonomous carts. Greenhouse and controlled environment farms are more open to robotic harvesting and monitoring because field variability is lower. This creates different ROI timelines by crop, farm size and region.

Explore the DataM Intelligence Autonomous Farm Equipment Market report for comprehensive insights into market segmentation by equipment type, autonomy level, farm size, application areas, and regional adoption trends. Gain a deeper understanding of evolving automation strategies, technology deployment patterns, and growth opportunities shaping the future of autonomous agriculture.

Precision Spraying and Autonomous Weeding Offer the Fastest Payback

Precision spraying and autonomous weeding are the strongest near term ROI opportunities because they attack two major cost centers at the same time. Chemical inputs are expensive, and field labor is difficult to secure during tight seasonal windows. Autonomous systems that identify weeds, spray only where needed or remove weeds mechanically can reduce chemical waste while lowering repeated labor requirements.

This category benefits from a clear economic story. Growers can calculate baseline herbicide use, labor hours, skipped passes, yield loss from weed pressure and the cost of manual crews. Once autonomous equipment reduces any combination of these cost lines, ROI becomes easier to defend. Recent field reports around laser weeding and AI enabled weed control point to strong savings potential in high value crops, especially where manual weeding has become difficult to schedule or where chemical reduction has direct commercial value.

The best early markets are vegetables, vineyards, orchards and specialty crops because labor intensity is high and weed pressure can have a direct effect on yield quality. Row crops are also becoming attractive as camera based spraying, machine vision and variable rate application improve. For growers, the near term opportunity is to target weed control and chemical use first, then expand into wider autonomy once field data, service routines and operator confidence improve.

Gain insights from the DataM Intelligence Precision Agriculture Market report on how guidance systems, remote sensing, and variable rate application technologies are reshaping agricultural productivity, reducing input waste, and enabling smarter precision farming practices.

Drones Can Deliver Fast ROI Through Scouting, Mapping and Targeted Spraying

Agricultural drones remain one of the fastest ROI categories because they require lower capital outlay than heavy autonomous machinery and can cover multiple use cases. Crop scouting, stand counts, pest detection, irrigation stress mapping and targeted spraying are all attractive because they turn field visibility into faster decisions.

The biggest advantage is speed. Drones can reduce the time required for field inspection and can help growers identify specific zones requiring treatment. This improves scouting productivity and can reduce unnecessary full field applications. In regions where labor is expensive or where fields are geographically dispersed, drone based monitoring can become one of the quickest steps into autonomous farming.

Drone spraying also has strong potential, especially in Asia Pacific and parts of North America where regulatory pathways and service provider networks are improving. The model is especially powerful when it is offered as a service. Farmers can access aerial autonomy without owning the full hardware stack, while drone operators can increase utilization across many farms and seasons.

Explore the DataM Intelligence Agricultural Drone Market report for market sizing, regional adoption and application level demand analysis.

Autonomous Carts and Hauling Solve a Practical Labor Bottleneck

Autonomous carts, field transport robots and follow me platforms are often overlooked, yet they can deliver faster ROI than more complex robotic systems. Harvest support, in field material movement, crate transport and equipment repositioning consume significant labor time. These tasks are repetitive, predictable and easier to automate than delicate crop picking.

This is why autonomous hauling can be attractive for orchards, vineyards, berry farms, nurseries and vegetable operations. The equipment does not need to solve every farming task. It only needs to remove wasted walking time, improve crew productivity and keep harvested product moving. When one robot supports multiple workers, the ROI can be faster than a full robotic harvesting system that must identify, pick and handle fragile produce independently.

The service model will matter here. Growers may prefer lease, rental or seasonal deployment because carts and hauling robots need to match harvest cycles. Companies that combine hardware, maintenance, route mapping and operator support are likely to win faster adoption than vendors selling hardware alone.

Autonomous Tractors Are Strategic, Although Payback Depends on Utilization

Autonomous tractors remain central to the future of farm automation because they can influence tillage, seeding, spraying and transport. Their ROI depends heavily on fleet utilization, field size, operator availability and the ability to run for longer operating windows. For large farms, the value is strongest when autonomy increases machine hours during critical planting or spraying periods.

The challenge is that autonomous tractors involve higher capital cost and greater integration needs. They require navigation, connectivity, safety systems, implement compatibility and support from dealers or service networks. This makes them more attractive for large commercial farms first. Smaller farms may adopt autonomy through retrofit kits, guided implements or service based models before buying fully autonomous tractors.

The strongest near term use cases are repetitive field operations where routes are predictable and human supervision can be reduced. Night operations, long duration tillage, controlled traffic farming and large field spraying are likely to develop before complex mixed operations. The ROI improves when a farm can keep the equipment working across many weeks rather than using it for a narrow seasonal task.

Robotic Harvesting Has High Potential, Yet ROI Is Crop Specific

Robotic harvesting has one of the largest long term opportunities because harvest labor is expensive, seasonal and increasingly difficult to secure. However, it is also one of the hardest applications to scale. Crop variability, ripeness detection, gentle handling, speed and field conditions all affect performance. A robot that works well in one crop or protected environment may need significant adaptation for another.

The fastest ROI for robotic harvesting is more likely in controlled environments, high value specialty crops and farms with severe labor gaps. Greenhouses, tomatoes, berries and orchard systems with standardized layouts are better early candidates than highly variable open field crops. Even in these markets, semi autonomous harvesting support may scale faster than fully independent picking because it lowers operational risk.

This is why growers should evaluate harvesting automation carefully. The ROI can be strong when labor cost is high and product value is high, but payback is slower when the robot has limited picking speed or requires major crop system changes. Investors should also look beyond picking arms to enabling technologies such as machine vision, grippers, end effectors, crop analytics and fleet orchestration software.

Where Investors Should Focus in the Next Two Years

The best near term investment opportunities are in technologies that convert autonomy into measurable operational savings. This includes precision weed control, smart spraying, drone analytics, autonomous carts, retrofit autonomy, machine vision, farm robotics software and service networks. These areas can scale faster because they do not always require the grower to replace the entire equipment base.

Component suppliers also stand to benefit. Cameras, lidar, radar, GPS modules, controllers, batteries, hydraulic actuation, electric drives and edge AI processors are becoming essential to autonomous farming equipment. As adoption expands, the supplier base will become as important as the equipment brand because uptime and field reliability will determine buyer trust.

The most attractive business models are likely to combine hardware with recurring revenue. Autonomy as a service, drone spraying services, seasonal robotic leasing, software subscriptions, agronomic analytics and maintenance contracts can reduce upfront cost for growers while creating predictable revenue for technology providers.

Application ROI Ranking for 2026 Deployment Planning

| Application | ROI speed | Best fit farms | Primary value lever | Key constraint |

| Precision spraying and weeding | Fast | Vegetables, vineyards, row crops | Chemical and labor savings | Weed detection accuracy and service support |

| Crop scouting drones | Fast | Large farms, dispersed fields | Faster field intelligence | Data integration and flight rules |

| Autonomous carts and hauling | Fast to moderate | Orchards, berries, nurseries | Crew productivity | Terrain navigation and seasonal utilization |

| Autonomous seeding | Moderate | Large row crop farms | Operating window expansion | Implement compatibility |

| Autonomous tractors | Moderate | Large commercial farms | Labor replacement and machine utilization | High upfront cost |

| Robotic harvesting | Slower but strategic | Greenhouses, specialty crops | Labor availability and harvest continuity | Crop variability and picking speed |

Final Outlook

The fastest ROI in autonomous farming equipment will come from focused automation rather than broad farm replacement. Precision spraying, autonomous weeding, drone scouting and autonomous hauling can create visible value because they reduce labor pressure, cut input waste and improve the timing of farm operations. Autonomous tractors and robotic harvesting will remain strategic, although adoption will depend on utilization, service support, crop compatibility and financing models.

The next phase of competition will be shaped by who can prove ROI at the farm level. Equipment suppliers, robotics startups, drone operators, software providers and agricultural service companies that can translate autonomy into seasonal savings will be best positioned. The opportunity is not only to automate farming, it is to make every labor hour, chemical application and equipment pass more productive.