Thermoplastic Vulcanizate (TPV) Market Overview

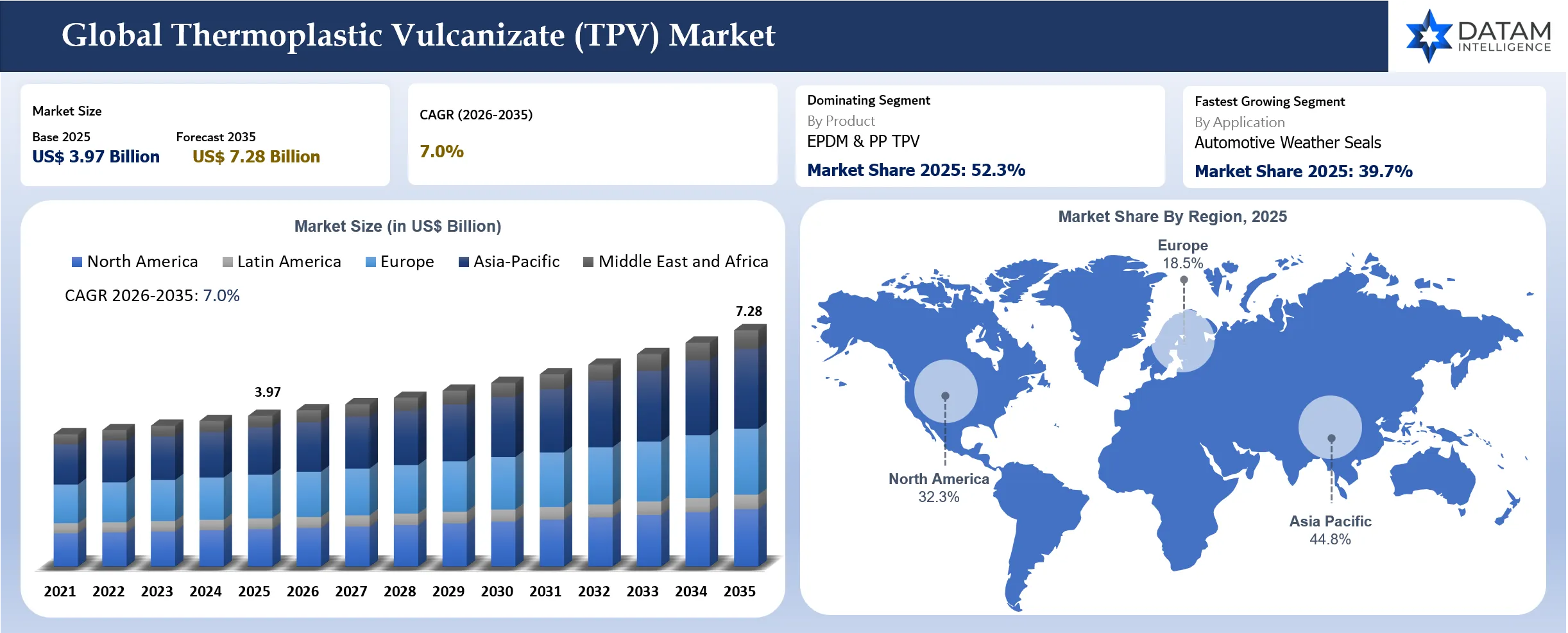

The global thermoplastic vulcanizate (TPV) market reached US$ 3.97 billion in 2025 and is expected to reach US$ 7.28 billion by 2035, growing at a CAGR of 7.0% during 2026 to 2035. Demand is driven by automotive weather seals, EV battery seals, hoses, air ducts, boots, gaskets, appliance parts, building seals, wire and cable jacketing and consumer goods. TPV is gaining share where buyers need rubber-like flexibility with thermoplastic processing, recyclability, lower part weight and shorter conversion cycles. Automotive suppliers value TPV where parts need sealing performance, chemical resistance, durability and easier processing compared with thermoset rubber.

Asia-Pacific will remain the largest and fastest-growing region as China, India, Japan and South Korea expand automotive production, EV platforms, appliances, electronics and construction material manufacturing. North America and Europe remain high-value markets because automakers, Tier suppliers and appliance brands are actively evaluating lightweight and reprocessable elastomer solutions. Supplier differentiation depends on grade consistency, automotive approvals, compression set performance, bonding behavior, color ability, processing support and recycled-content development.

Key Takeaways

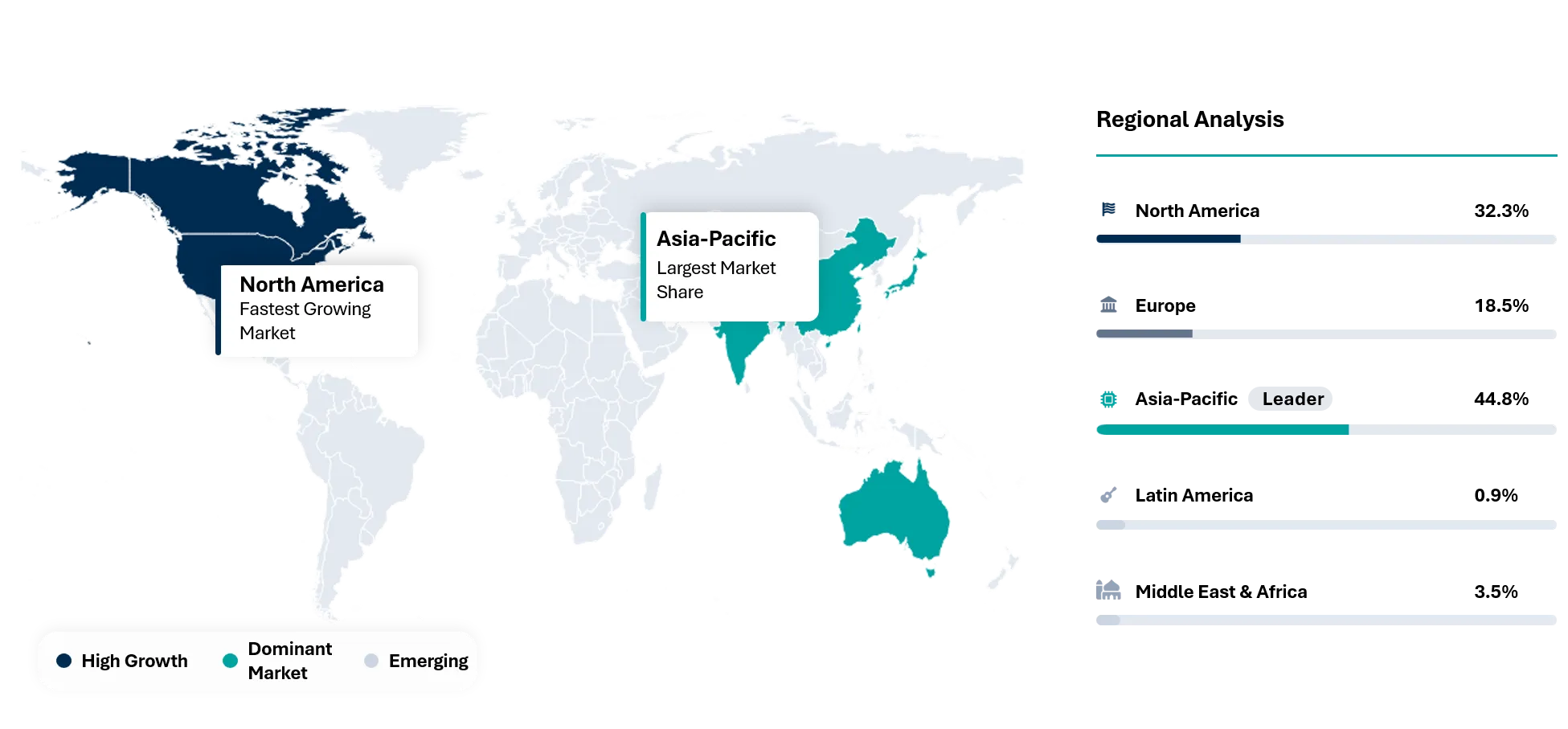

- Asia-Pacific dominated with 44.8% market share in 2025 and is expected to reach 54.4% market share by 2035, supported by automotive, EV appliance, electronics and building product manufacturing.

- Asia-Pacific is the fastest-growing region with 8.4% CAGR between 2026 and 2035 due to expansion in China, India, Japan and South Korea.

- EPDM and PP TPV remain the leading product because they provide a practical balance of elasticity, weather resistance, chemical resistance and thermoplastic processability.

- Specialty TPV is expected to grow fast as buyers need improved heat resistance, lower density, better bonding, softer touch, medical suitability and recycled-content options.

- Automotive weather seals remain the leading application because TPV can reduce weight, support extrusion and deliver durable sealing in static and semi-dynamic parts.

- EV battery seals are expected to be the fastest-growing application as battery packs, charging ports and thermal systems need flexible sealing with chemical and temperature resistance.

- Supplier differentiation is moving toward automotive approvals, low-emission grades, recycled-content development, consistent compression set and strong processing support.

Market Scope

| Metrics | Details | |

| Market Size In 2025 | US$ 3.97 Billion | |

| Market Size By 2035 | US$ 7.28 Billion | |

| CAGR During 2026 To 2035 | 7.0% | |

| Largest Region In 2025 | Asia-Pacific, 44.8% market share in 2025 | |

| Fastest Growing Region | Asia-Pacific, 8.4% CAGR between 2026 and 2035 | |

| Key Regional Shift | Asia-Pacific is expected to increase from 44.8% market share in 2025 to 54.4% market share by 2035 | |

| Leading Product | EPDM and PP TPV | |

| Fastest Growing Product | Specialty TPV | |

| Leading Application | Automotive Weather Seals | |

| Fastest Growing Application | EV Battery Seals | |

| Market Maturity | Growth Stage | |

| Key Buying Question | Which TPV grade can replace rubber while improving processing speed, weight and recyclability without losing seal performance? | |

| By Product | EPDM and PP TPV, Natural Rubber and PP TPV, Butyl Rubber and PP TPV, Specialty TPV, Others | |

| By Processing Method | Injection Molding, Extrusion, Blow Molding, Two-Shot Molding, Co-Extrusion, Others | |

| By Application | Automotive Weather Seals, EV Battery Seals, Air Ducts and Boots, Hoses and Tubing, Gaskets and O-Rings, Appliance Components, Building and Construction Seals, Wire and Cable Jacketing, Medical and Healthcare Components, Consumer Goods, Others | |

| By End-User | Automotive OEMs, Automotive Tier Suppliers, Electrical and Electronics Companies, Appliance Manufacturers, Building and Construction Product Manufacturers, Healthcare Product Manufacturers, Consumer Goods Manufacturers, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| South America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Why Does This Report Matter In 2026?

TPV demand matters in 2026 because automakers and industrial brands are under pressure to reduce weight, improve processing efficiency and increase recyclability without sacrificing sealing performance. Thermoset rubber remains strong in many high-heat and dynamic applications, but TPV is gaining where thermoplastic processing can reduce cycle time, enable part integration and support rework or scrap reuse. EV platforms are creating new sealing requirements. Battery packs, cooling circuits, charging interfaces, wire harnesses and underbody components need flexible materials that can handle moisture, chemicals, compression and long service life. TPV suppliers that can meet automotive validation requirements will benefit as EV programs scale across Asia-Pacific, Europe and North America.

Appliance, building and electrical applications also support demand. Manufacturers want flexible parts that can be molded or extruded with predictable quality. TPV offers design flexibility for gaskets, grips, seals, hoses and cable jackets. A strong market study must therefore evaluate material substitution, processing economics, automotive qualification and regional manufacturing trends.

Strategic Indicators For TPV

High Regulation Impact

Regulation affects TPV demand through vehicle emissions, recyclability expectations, chemical safety, food contact, medical device requirements and building material performance. Automotive buyers need materials that meet OEM specifications, low volatile emission requirements, weathering standards and long-term durability. Medical and healthcare applications require tighter biocompatibility and extraction controls. Chemical compliance is increasingly important. TPV suppliers must manage restricted substances, flame retardants, additives and regional chemical rules. Customers selling into Europe, North America and Japan require documentation that supports regulatory review. Suppliers with strong compliance systems can move faster through qualification.

Automotive platforms add another layer of approval. A TPV grade selected for a weather seal or battery seal must meet physical property, aging, compression set, color, emission and processability requirements. Qualification delays can slow adoption, making technical support and consistent production essential.

High Investment Activity

Investment is concentrated in EV sealing materials, recycled-content TPV, low-density compounds, medical-grade elastomers, over molding solutions and specialty automotive grades. Compounders are developing TPV grades with improved bonding, softness, surface finish and processing stability. Automotive suppliers need grades that work across extrusion, injection molding and co-extrusion. EV investment supports long-term TPV demand. Battery packs, charging systems, cable management and thermal circuits require seals and flexible components. TPV can gain where it replaces thermoset rubber in non-extreme applications. Suppliers that secure early program approvals can benefit throughout vehicle platform life.

Asia-Pacific investment is strong because automotive and appliance production are concentrated in the region. China’s EV ecosystem, India’s automotive manufacturing and Japan and South Korea’s high-quality materials supply chains create growth opportunities. Local technical support and compounding capacity matter for fast qualification.

Supply Chain Disruption

TPV supply risk is tied to PP, EPDM, process oils, fillers, additives, compounding capacity and automotive qualification. Feedstock volatility can affect compound cost. Automotive customers require consistent grades, so material changes must be tightly controlled. A supplier cannot easily change formulation without risking requalification. Regional supply security is becoming important. Automakers and Tier suppliers want materials available close to production plants. Long-distance supply can expose projects to freight delays, tariffs and inventory risk. Compounders with regional plants in Asia-Pacific, North America and Europe have an advantage.

Specialty additives can create bottlenecks. Flame retardants, bonding modifiers, low-emission packages and color systems must remain stable. If a specific additive becomes unavailable, revalidation may be required. Suppliers with robust sourcing and formulation control can reduce disruption.

Pricing Volatility

TPV pricing is affected by PP, EPDM, process oil, additives, filler content, hardness, performance grade and order volume. Automotive and medical grades command premium pricing because qualification and documentation requirements are higher. Commodity-like TPV grades face more price competition from TPO, SEBS compounds and thermoset rubber. Processing economics are central to pricing. TPV may cost more per kilogram than some rubber compounds, but it can reduce cycle time, scrap and secondary finishing. Buyers evaluate total part cost, not only resin price. Faster molding, co-extrusion and recycling of process scraps can improve business cases.

EV applications may support premium pricing where performance requirements are stricter. Battery and charging interfaces need reliable sealing and durability. Suppliers that deliver validated grades and technical support can defend pricing.

Procurement Pressure

Automotive Tier suppliers face pressure to reduce weight, cost and processing complexity. A TPV grade must pass OEM validation, run reliably on production equipment and meet long-term aging requirements. Procurement decisions involve engineering, quality, production and purchasing teams. Appliance and building product buyers focus on consistency and processing speed. Materials that cause dimensional variation or poor surface finish can increase scrap. Suppliers need to support mold design, extrusion settings and processing troubleshooting.

Recyclability is also influencing procurement. TPV can be reprocessed like thermoplastics, which supports scrap reduction. Buyers increasingly ask for recycled content, carbon footprint data and closed-loop potential. Suppliers need credible data, not only broad sustainability claims.

New Technology Adoption

Technology adoption is strongest in low-density TPV, recycled-content TPV, medical-grade TPV, improved over molding grades, high-flow injection molding grades and EV sealing grades. Low-density materials help automakers reduce part weight. Over molding grades help integrate soft and rigid components. Recycled-content TPV is gaining attention, although performance consistency remains challenging. Automotive buyers need proof that recycled material does not compromise compression set, odor, color or long-term durability. Closed-loop manufacturing scrap is easier to use than post-consumer material.

Advanced compounding and process control are improving TPV quality. Better dispersion, dynamic vulcanization control and additive packages improve consistency. Suppliers that can tailor hardness, surface feel, bonding and aging behavior will gain share in higher-value applications.

Regional Expansion Opportunity

Asia-Pacific offers the strongest regional expansion opportunity because automotive, EV, appliances and electronics manufacturing are concentrated in China, India, Japan, South Korea and Southeast Asia. Local production and technical support are crucial because OEM approvals and Tier supplier trials require fast response. North America remains important due to automotive, appliance, healthcare and building product demand. EV and battery investments create new sealing opportunities. Buyers value technical support, regulatory documentation and supply continuity.

Europe remains a premium market due to automotive quality expectations, sustainability pressure and material substitution activity. German, French, Italian and UK manufacturers evaluate TPV for weather seals, interior soft-touch parts, appliance components and building seals. Regulatory documentation is especially important.

Government Policy Support

EV policies support TPV demand indirectly by increasing demand for battery seals, charging interface seals, cable jackets and thermal system components. Vehicle efficiency rules also support lightweight material substitution. TPV benefits where automakers replace heavier or less recyclable rubber parts. Circular economy policies support interest in reprocessable elastomers. Thermoset rubber recycling remains difficult, while TPV processing scrap can be reused more easily. Regulations and brand sustainability goals encourage evaluation of thermoplastic elastomers.

Industrial policy supporting local automotive and appliance manufacturing can also benefit TPV suppliers. Regional compounding and material availability are important as manufacturers localize supply chains. Suppliers with regional production can respond better to government-supported manufacturing growth.

Pricing Intelligence

Pricing is driven by formulation complexity, hardness, EPDM content, PP grade, process oil, additives, color, performance requirements and order volume. Automotive grades usually carry higher pricing due to validation, documentation and long-term commitment. Specialty medical or low-emission grades also command premiums. Buyers compare TPV against EPDM rubber, TPO, SEBS compounds and TPU depending on application. TPV wins where processing speed, recyclability, weight reduction and part integration offset higher material cost. Rubber remains strong where heat, compression and dynamic performance exceed TPV capability.

AI Impact Analysis

AI can improve TPV formulation by accelerating grade development. Formulators must balance hardness, compression set, flow, tensile strength, aging, chemical resistance and bonding behavior. AI-based material models can help predict how polymer ratios, oils, fillers and additives will affect performance. It can reduce trial cycles. AI can also improve compounding quality. TPV performance depends on dynamic vulcanization control and dispersion of rubber particles in a thermoplastic matrix. Process analytics can detect variation in torque, temperature, pressure and pellet quality. Better control helps reduce batch variation.

Automotive suppliers can use AI to predict seal performance across weather, compression and aging conditions. Such tools can help select grades faster during vehicle platform development. Human validation and physical testing will remain essential, but modeling can shorten early screening. AI-driven demand forecasting can also help suppliers manage volatile automotive and appliance cycles. EV program timing, platform delays and feedstock price changes affect demand. Better forecasting can improve inventory planning and customer service.

Disruption Analysis

EV platforms are disrupting TPV demand because sealing requirements are changing. Battery packs, charging ports, cable systems and thermal loops create new elastomeric part needs. TPV can gain where it meets durability and processing requirements without the cost and cure time of rubber. Recyclability is disrupting material selection. Thermoset rubber is difficult to reprocess, while TPV can use process scrap more easily. Automotive and appliance manufacturers are increasingly evaluating materials through circularity and production waste reduction. TPV suppliers with recycled-content grades can gain attention.

Processing speed is another disruption. TPV can be injection molded, extruded and co-extruded using thermoplastic equipment. Shorter cycle times and reduced curing steps can lower conversion cost. Suppliers that help customers redesign parts for thermoplastic processing can capture more value. Performance limits remain disruptive in the opposite direction. EPDM rubber and silicone still outperform TPV in some high-heat, high-compression and dynamic sealing environments. TPV growth depends on correct application targeting rather than broad replacement claims.

BCG Matrix: Company Evaluation

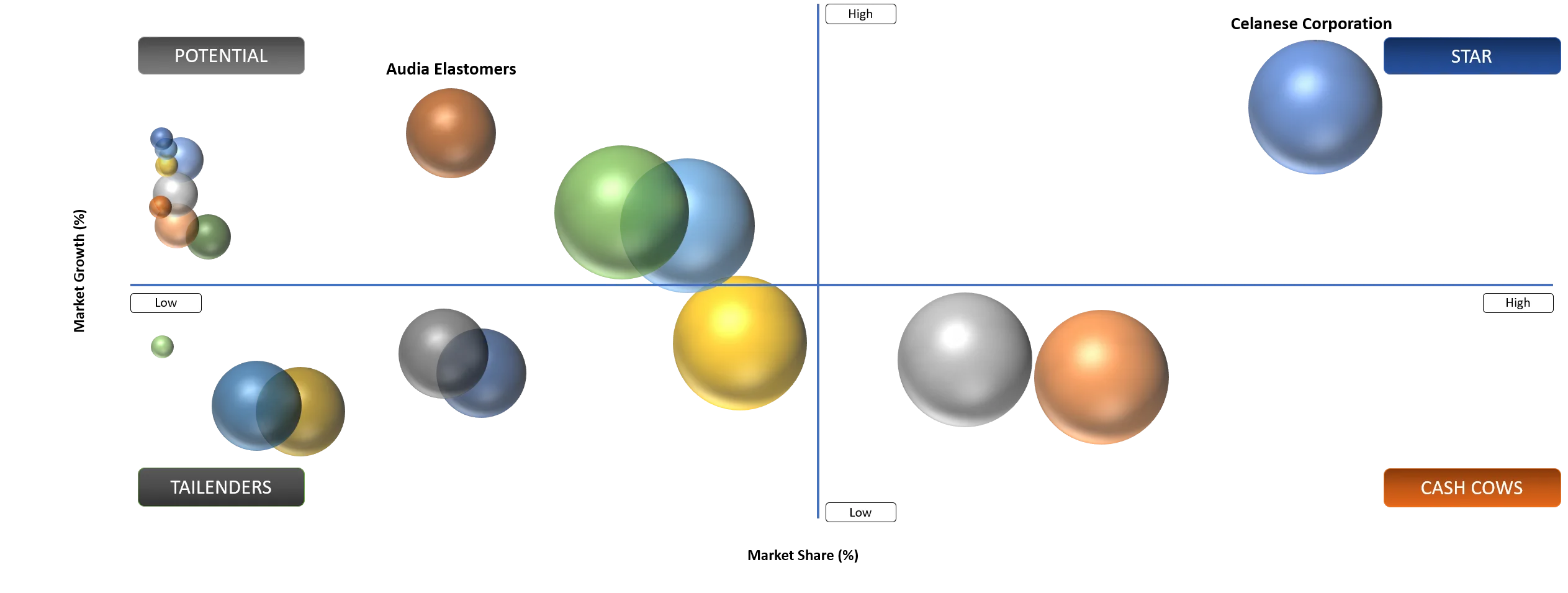

Star

Star players include Celanese Corporation, Teknor Apex Company, Mitsui Chemicals, Inc., Mitsubishi Chemical Group Corporation, RTP Company, Ravago Group, HEXPOL AB, KRAIBURG TPE GmbH and Co. KG and Elastron Kimya Sanayi ve Ticaret A S. The companies have strong compounding capability, recognized elastomer portfolios, automotive exposure and technical service depth.

Potential

Potential companies include Audia Elastomers, LCY Chemical Corp. and TSRC Corporation. Audia Elastomers will grow through custom compounding and specialty elastomer solutions. LCY Chemical and TSRC will benefit from Asia-Pacific elastomer supply chains, automotive growth and demand for regional material alternatives if they expand performance and documentation capability.

Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact | Demand Concentration | Impacted Use Case | Strategic Impact |

Automotive Weather Seals Shift Toward Lightweight Re-processable Elastomers | High | Asia-Pacific, North America and Europe | Weather Seals | Supports TPV substitution for selected rubber parts |

EV Battery and Thermal Systems Need Flexible Durable Sealing | High | China, U.S., Europe, Japan and South Korea | EV Battery Seals | Creates new grade development demand |

Appliance Manufacturers Reduce Rubber Curing and Assembly Complexity | Medium | Asia-Pacific and North America | Gaskets and Hoses | Supports injection molded and extruded TPV parts |

Building Seals Require Long-Term Weathering and Compression Performance | Medium | Europe, North America and Asia-Pacific | Construction Seals | Supports durable profile extrusion |

Automotive Weather Seals Shift Toward Lightweight Reprocessable Elastomers

Automotive weather seals remain the largest TPV demand driver because automakers need durable sealing with lower weight and efficient processing. Door seals, glass run channels, roof seals and body plugs need flexibility, weather resistance and stable compression performance. TPV is attractive where it can replace selected EPDM rubber parts without sacrificing durability. Weight reduction supports adoption. Automakers are looking for lighter materials to improve vehicle efficiency and EV range. TPV compounds can help reduce part weight while supporting design flexibility. Low-density grades are particularly relevant for large seal profiles.

Thermoplastic processing creates cost advantages. TPV parts can be extruded or molded without rubber curing, reducing cycle time and allowing process scrap reuse. Co-extrusion and two-shot molding also support part integration. Tier suppliers value these benefits when they reduce labor and scrap. Automotive qualification remains demanding. A TPV grade must pass aging, odor, fogging, compression set, weathering and OEM-specific performance tests. Suppliers with proven automotive approvals and technical support have a strong advantage.

Restraint Impact Analysis

| Restraint | Drag On Market Growth | Primary Impact Area | Impacted Use Case | Strategic Impact |

EPDM Rubber Cost Advantage Limits TPV Conversion | High | Automotive and Building Seals | Weather Seals and Profiles | Restricts substitution in price-sensitive parts |

High-Heat Applications Still Require Thermoset Rubber | Medium To High | Underhood and Industrial Parts | Boots, Hoses and Seals | Limits addressable applications |

Grade Qualification Delays Slow Automotive Platform Adoption | Medium | Automotive OEM Programs | Weather Seals and EV Components | Lengthens sales cycle |

Feedstock Price Volatility Affects Compound Margins | Medium | Compounders | All Applications | Raises pricing pressure |

EPDM Rubber Cost Advantage Limits TPV Conversion

EPDM rubber remains a strong competitor because it is well established, cost-effective and trusted in many sealing applications. Automotive suppliers have decades of processing experience with EPDM. TPV must prove clear value through weight reduction, processing speed, recyclability or part integration to justify conversion. High-heat and high-compression environments also limit TPV adoption. Some under hood, industrial and dynamic sealing applications still require thermoset rubber or silicone. Overstating TPV performance can create qualification failures. Suppliers need to target the right applications carefully.

Automotive approval timelines slow adoption. New grades must pass OEM and Tier supplier validation. Materials can be technically suitable but still delayed by platform timing, testing requirements or production line qualification. It creates long sales cycles. Feedstock price volatility affects margins. TPV compounds rely on PP, EPDM, oils, fillers and additives. Cost increases can squeeze compounders if contracts do not allow quick pass-through. Buyers may reconsider rubber or TPO alternatives when TPV pricing rises.

Segment Analysis

EPDM and PP TPV Will Continue To Dominate Demand

EPDM and PP TPV will remain the leading products because it offers a strong balance of elastomeric behavior and thermoplastic processability. EPDM provides weathering and sealing performance, while PP enables melt processing. This combination is widely used in automotive, appliance, building and industrial applications. Automotive weather seals are the largest application base. TPV can provide stable sealing performance in static and semi-dynamic parts. It also supports extrusion and co-extrusion, which helps Tier suppliers produce complex profiles. The ability to reuse process scrap improves manufacturing economics.

Appliance components also use EPDM and PP TPV where heat, moisture and chemical resistance are required. Dishwasher, washing machine and refrigerator components can benefit from sealing and processing advantages. Material selection depends on temperature, detergent exposure and compression needs. Building and construction seals support additional demand. Window gaskets, glazing seals and expansion profiles require long-term weatherability. TPV can compete where extrusion quality, color stability and service life matter. Cost competition from EPDM remains strong.

EV Battery Seals Are the Fastest-Growing Application

EV battery seals are expected to be the fastest-growing application because battery packs require protection from moisture, dust, vibration and thermal exposure. Sealing systems around packs, modules, cooling channels and charging interfaces need reliable elastomeric materials. TPV can gain where processing efficiency and recyclability matter. Battery pack design varies across automakers. Some applications require high heat or flame performance, while others focus on water resistance and compression stability. TPV suppliers need application-specific grades rather than generic elastomer claims. Strong technical collaboration with OEMs and Tier suppliers is essential.

Charging port seals, cable glands and connector gaskets need flexibility, weatherability and repeated-use durability. TPV can be suitable where electrical and environmental requirements are manageable. EV infrastructure and vehicle charging systems create related opportunities. Thermal management systems provide another growth route. Coolant hoses, seals and flexible connectors need chemical resistance and dimensional stability. TPV can compete in selected applications, although high-temperature or aggressive-fluid environments may still need other elastomers.

Injection Molding and Extrusion Will Remain Core Processing Routes

Injection molding and extrusion will remain the core processing routes because TPV is designed for thermoplastic processing. Injection molding supports gaskets, plugs, caps, handles and complex soft parts. Extrusion supports seals, profiles, tubing and weatherstrips. These methods create cost advantages compared to rubber curing. Two-shot molding is gaining demand for integrated soft-touch and sealing parts. TPV can bond with selected rigid polymers, helping manufacturers reduce assembly steps. Consumer goods, automotive interiors and appliance controls use this capability. Bonding behavior is a key supplier differentiator.

Co-extrusion is important in automotive profiles. Multiple materials can be combined to provide rigid support and soft sealing in one part. This improves design flexibility and reduces secondary assembly. Suppliers must help customers tune processing settings. Processing support is critical. TPV grades can differ in flow, shrinkage, surface finish and bonding. A material supplier that provides processing guidance can reduce scraps and accelerate qualification. Technical service is therefore a major competitive factor.

Geographical Penetration

Asia-Pacific TPV Market Trends

Asia-Pacific dominated the TPV market with 44.8% market share in 2025 and is expected to reach 54.4% market share by 2035. The region is also the fastest growing with 8.4% CAGR between 2026 and 2035. Growth is supported by automotive, EV, appliance, electronics and construction material manufacturing. China is the largest regional demand center. EV production, appliance manufacturing and local automotive supply chains support TPV consumption. Domestic compounders are improving capabilities, while global suppliers remain important for high-performance and automotive-approved grades.

India is growing through automotive production, EV components, appliances and building products. Cost pressure is high, but TPV adoption increases where processing efficiency, weight reduction and part integration improve total cost. Local technical support will be important. Japan and South Korea support premium demand. Automakers and electronics companies require high-quality grades and strong documentation. Suppliers with proven automotive approvals and consistent production are well positioned in these markets.

North America TPV Market Outlook

North America is a high-value TPV market due to automotive, EV, appliance, healthcare and building product demand. The U.S. is the main country market because automakers, Tier suppliers and compounders have strong technical requirements. EV investments support new sealing opportunities. Automotive weather seals remain a key demand base. Suppliers need grades that meet OEM specifications for compression set, aging, odor and weathering. TPV competes with EPDM rubber, so conversion depends on clear processing or weight benefits.

Appliance demand is also important. U.S. and Mexican appliance manufacturing uses TPV in seals, hoses, gaskets and vibration control parts. Processing speed and design flexibility support adoption. North American buyers value technical support and supply security. Regional compounding, reliable logistics and documentation matter. Suppliers with local service teams will win automotive and healthcare projects more effectively.

U.S. TPV Market Landscape

The U.S. TPV market is driven by automotive, EV, appliance, healthcare and building applications. Automakers and Tier suppliers need elastomeric materials that support lightweight design, reliable sealing and production efficiency. TPV is attractive where it can reduce curing steps and allow scrap reuse. EV battery and charging components are emerging growth areas. Battery seals, cable grommets, charging port seals and thermal system components need durable materials. TPV suppliers must prove long-term performance under moisture, chemical and temperature exposure.

Medical and healthcare applications are smaller but higher value. TPV can be used in selected seals and flexible components where regulatory suitability is demonstrated. Suppliers need strong documentation and quality systems to serve these applications. The U.S. market is competitive because buyers have multiple material choices. TPV must compete against EPDM, silicone, TPO, SEBS and TPU. Technical support and grade selection are critical for successful substitution.

Japan TPV Market Analysis

Japan is a premium TPV market where material consistency and long-term durability matter. Automotive and electronics buyers require strict quality control. Qualification cycles can be long, but approved materials often remain in use for years. Automotive weather seals and precision molded parts are important. Japanese automakers emphasize reliability, cabin comfort and low noise. TPV can support weather sealing and vibration control where it meets performance requirements.

Appliance and electronics applications also support demand. Japan’s manufacturing culture values stable processing and clean surface finish. Suppliers need technical credibility and strong local support. Sustainability and recyclability are becoming more relevant. TPV’s thermoplastic processing and scrap reuse potential can support manufacturer goals. Adoption will depend on proof that performance remains stable over product life.

Competitive Landscape

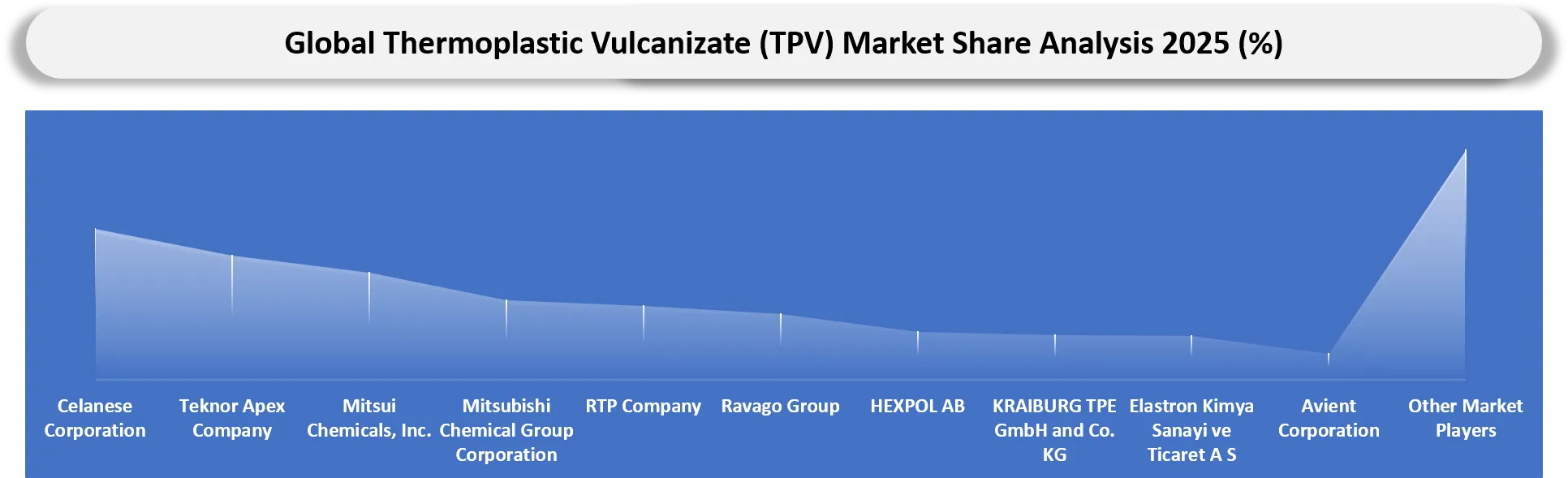

- Competition is split between global TPV leaders, custom compounders, specialty elastomer producers and regional material suppliers. Celanese remains the key benchmark through Santoprene TPV, while Teknor Apex, Mitsui Chemicals, RTP Company, KRAIBURG TPE and Elastron compete across specialty and custom grades.

- Automotive competition depends on OEM approvals, performance consistency, regional supply and technical service. A supplier with a qualified grade on a vehicle platform can retain business across the platform lifecycle. Switching is difficult after validation.

- Custom compounders compete by tailoring hardness, color, bonding, flow and application performance. Such flexibility matters in appliances, consumer goods, building products and industrial components. Smaller compounders can win where large suppliers are less flexible.

- Sustainability is becoming a competitive factor. Recycled-content TPV, lower-density grades and scrap reuse support customer sustainability goals. However, buyers will not accept performance loss in critical sealing parts.

- Competitive benchmarking should track compression sets, weatherability, oil resistance, bonding, low-temperature flexibility, density, recycled content, automotive approvals, regional production and technical service.

Key Companies

- Celanese Corporation

- Teknor Apex Company

- Mitsui Chemicals, Inc.

- Mitsubishi Chemical Group Corporation

- RTP Company

- Ravago Group

- HEXPOL AB

- KRAIBURG TPE GmbH and Co. KG

- Elastron Kimya Sanayi ve Ticaret A S

- Avient Corporation

- Trinseo PLC

- Zeon Corporation

- Kuraray Co., Ltd.

- Exxon Mobil Corporation

- LyondellBasell Industries N.V.

- LCY Chemical Corp.

- China Petroleum and Chemical Corporation

- TSRC Corporation

- PolyOne Corporation

- Audia Elastomers

- WatchGuard Technologies, Inc.

Company Coverage Preview

Celanese Corporation is the leading benchmark company through Santoprene TPV. The company benefits from strong brand recognition, automotive approval history and broad use in weather seals, underhood components, appliance parts and industrial applications. Its advantage comes from material performance, long-term grade availability and established customer trust.

Teknor Apex Company competes through Sarlink TPV and broader custom compound capability. The company is relevant where customers need tailored hardness, color, processability and performance. Custom compounding strength helps Teknor Apex serve automotive, appliance, building and industrial applications.

Mitsui Chemicals, Mitsubishi Chemical Group, RTP Company, KRAIBURG TPE, Elastron, Avient, HEXPOL and Ravago compete across TPV and adjacent elastomer compounds. Competition depends on regional production, formulation flexibility, technical service and ability to support automotive and industrial qualifications.

Major Pain Points

- EPDM rubber remains cheaper in many weather seal applications.

- Automotive qualification cycles can delay TPV adoption by several years.

- High-heat applications may still require silicone or thermoset rubber.

- Feedstock price volatility affects compound cost and margins.

- Recycled-content TPV must prove consistent performance.

- Bonding to rigid polymers can vary by substrate and process conditions.

- Color and surface finish consistency can be difficult in premium visible parts.

- EV battery applications require careful chemical, thermal and compression validation.

- Regional supply gaps can create risk for global vehicle platforms.

- Buyers need processing support to reduce molding and extrusion scrap.

Recent Developments

- January 2026: Celanese continued positioning Santoprene TPV across automotive, industrial and consumer applications with emphasis on durable sealing and thermoplastic processability.

- October 2025: Teknor Apex continued promoting Sarlink TPV compounds for automotive, building, consumer and industrial elastomer applications.

- September 2025: KRAIBURG TPE expanded communication around customized elastomer compounds for mobility and industrial applications, supporting demand for application-specific alternatives.

- July 2025: Elastron continued strengthening TPV and TPE compound positioning for automotive and consumer applications across Europe and export markets.

Analyst View and Opinion

- TPV demand will grow steadily because automotive and appliance manufacturers need lighter and more process-efficient elastomeric materials.

- EPDM and PP TPV will remain the leading products due to strong use in weather seals and durable flexible parts.

- EV battery seals will be the fastest-growing application, but grade qualifications will be demanding.

- Asia-Pacific will remain the largest and fastest-growing region because automotive and appliance production is concentrated there.

- TPV will not replace thermoset rubber in every application because high-heat and dynamic performance limits remain.

- Recycled-content TPV will gain attention, but critical applications will require strong proof of performance consistency.

- Custom compounders will gain share where buyers need application-specific hardness, bonding or color.

- Celanese will remain the benchmark brand owner, but regional competitors will become stronger in cost-sensitive applications.

- Processing support will become a major differentiator because material substitution depends on stable molding and extrusion.

- Automotive platform approvals will protect established suppliers and slow new entrants.

Target Audience

| Industry | Who Should Buy This Report? | Reason To Buy This Report |

| Automotive OEMs | Materials Engineers, Purchasing Teams, Platform Engineers | Evaluate TPV use in weather seals, EV components and lightweight parts |

| Automotive Tier Suppliers | Product Development Teams, Process Engineers | Assess grade selection, processing economics and qualification risk |

| Appliance Manufacturers | Design Teams, Sourcing Teams | Understand TPV use in seals, gaskets, hoses and molded parts |

| Compounders | Strategy Teams, Sales Leaders, Product Managers | Identify growth opportunities across automotive, EV and industrial markets |

| Building Product Manufacturers | Product Managers, Technical Teams | Evaluate TPV use in glazing seals, gaskets and construction profiles |

| Healthcare Product Manufacturers | Regulatory Teams, Materials Teams | Assess TPV suitability for selected flexible healthcare components |

| Investors | Specialty Materials Investors, Polymer Funds | Track growth in reprocessable elastomers and automotive substitution |

| Consulting Firms | Chemicals and Materials Teams | Support market entry, supplier benchmarking and application strategy |

What DataM Uniquely Provides:

- DataM maps TPV demand by product, processing method, application, End-User and region.

- DataM separates automotive weather seal demand from EV battery seal and appliance component opportunities.

- DataM benchmarks suppliers by automotive approvals, compound flexibility, regional supply and technical support.

- DataM evaluates pricing pressure from PP, EPDM, process oils, additives and grade complexity.

- DataM analyzes TPV competition against EPDM rubber, TPO, SEBS, TPU and silicone.

- DataM tracks EV sealing demand and the material requirements shaping future TPV growth.

- DataM provides procurement-risk mapping for qualification delays, processing issues and feedstock volatility.

- DataM includes trade intelligence indicators for elastomer compounds, PP, EPDM and finished flexible components.