Global Virtual Reality in Healthcare Market – Industry Trends & Outlook

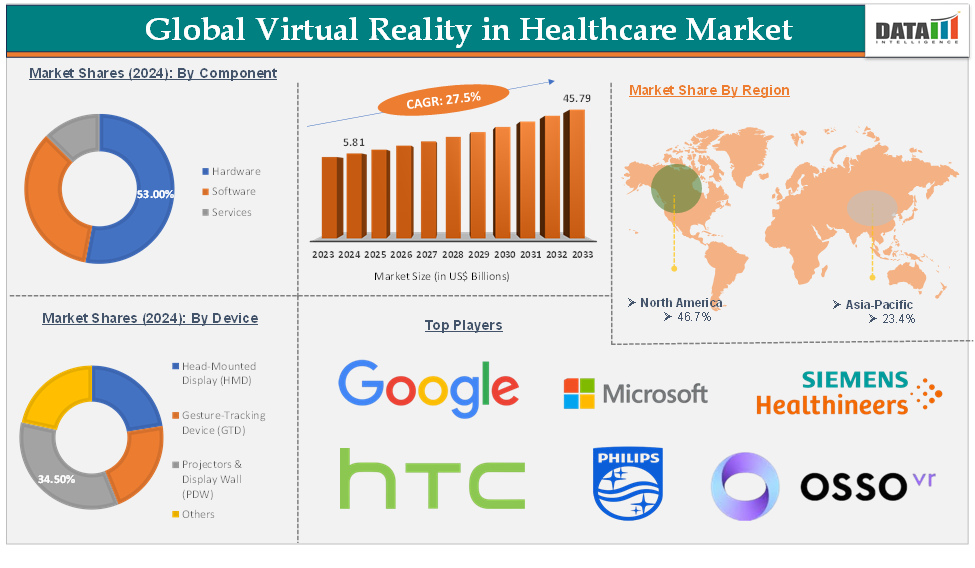

The global virtual reality in healthcare market reached US$ 5.81 Billion in 2024 and is expected to reach US$ 45.79 Billion by 2033, growing at a CAGR of 27.5% during the forecast period of 2025-2033.

The global virtual reality (VR) in healthcare market encompasses the application of immersive, computer-generated environments and simulations across a spectrum of medical uses, such as medical education, surgical rehearsal, patient therapy, pain relief, rehabilitation, and remote healthcare delivery. By enabling both healthcare professionals and patients to interact with realistic 3D scenarios, VR offers a safe, controlled space for learning, diagnosis, and treatment.

Growth is propelled by the increasing demand for advanced healthcare services, cost-efficiency imperatives, continuous improvements in VR technology, and the broader adoption of telemedicine. Additionally, an aging global population and the rising incidence of chronic diseases are driving the search for innovative solutions like VR to enhance eldercare, cognitive therapy, and chronic disease management.

Emerging trends include the convergence of VR with artificial intelligence and 5G for instant remote diagnostics, the widespread adoption of head-mounted displays (HMDs) for immersive training and patient engagement, and the extension of VR into mental health, pain management, and exposure therapy for disorders such as PTSD and phobias.

Opportunities within the VR healthcare sector are vast. There is growing enthusiasm for immersive, simulation-based medical education and training, as well as for patient-centered therapies that enhance clinical outcomes and experiences. The ongoing development of more accessible, cost-effective VR devices and tailored medical applications is making the technology more widely available.

Global Virtual Reality in Healthcare Market – Executive Summary

Global Virtual Reality in Healthcare Market Dynamics: Drivers

Adoption of telemedicine and remote care

The growing adoption of telemedicine and remote care is a significant catalyst for the expansion of the global virtual reality (VR) in the healthcare market. As more healthcare providers embrace digital tools to deliver services outside conventional clinical environments, VR is being woven into telemedicine platforms to elevate experiences such as remote diagnostics, virtual consultations, and tele-rehabilitation.

This integration enables both patients and clinicians to engage in immersive, lifelike interactions regardless of their physical locations, thereby improving access to quality care, particularly for individuals in remote or underserved regions. The increasing reliance on remote healthcare is driven by factors like the rising incidence of chronic illnesses, an aging global population, and the urgent need for more affordable and accessible healthcare solutions.

VR addresses these challenges by facilitating remote patient monitoring, virtual therapy, and interactive educational sessions, all conducted securely and efficiently from afar. Technological advancements, including artificial intelligence, wearable health devices, and faster internet connectivity, are further strengthening the effectiveness and attractiveness of VR-enabled telemedicine.

For instance, in April 2025, CADIS HealthTech unveiled EziExpert, an advanced telehealth platform featuring virtual & augmented reality for remote consultations. This innovative solution transforms any connected healthcare assistant into an extension of the remote physician, enabling more interactive and effective virtual care.

Global Virtual Reality in Healthcare Market Dynamics: Restraints

High cost of VR equipment and implementation

The high cost of VR equipment and implementation poses a major challenge for the global virtual reality (VR) in healthcare market. Initial investments in VR hardware, including headsets and related devices, can range from US$ 1,500 to over US$ 17,000 for just a few units.

Software development and customization expenses can add anywhere from US$ 12,000 to US$ 150,000 or more, depending on the complexity and specific healthcare applications. Additional costs such as licensing fees, integration with existing hospital infrastructure, staff training, and ongoing maintenance can further increase the total expenditure, with basic setups for small-scale deployments costing between US$ 26,500 and US$ 110,000 or higher.

These significant upfront and recurring costs often deter smaller clinics and healthcare providers with limited resources from adopting VR technology. Besides the financial burden, organizations must also invest time and effort into training personnel, providing technical support, and integrating VR solutions into existing workflows, which adds to operational challenges.

For more details on this report, Request for Sample

Global Virtual Reality in Healthcare Market - Segment Analysis

The global virtual reality in healthcare market is segmented based on component, device, technology, deployment, application, end-user, and region.

Component:

The hardware component segment is expected to hold 53.0% of the global virtual reality in healthcare market in 2024

The hardware component segment in the global virtual reality (VR) in healthcare market comprises the essential physical devices and equipment that enable immersive VR experiences for medical applications. This segment includes a variety of devices such as head-mounted displays (HMDs), smart glasses, 3D sensors, gesture-tracking devices like data gloves, projectors, display walls, as well as semiconductor components including controllers, processors, integrated circuits, cameras, and sensors such as accelerometers, gyroscopes, magnetometers, and proximity sensors.

The dominance of hardware is driven by the widespread use of these devices in critical applications like surgery, diagnostics, telemonitoring, patient care, and medical training. The availability of commercially mature VR hardware, particularly in developed regions, has accelerated adoption by healthcare providers integrating these technologies into their clinical workflows.

Key factors propelling growth in the hardware segment include the versatility of these devices across multiple healthcare uses, ongoing technological advancements improving device performance and usability, and the ability to deploy a single hardware platform for diverse medical tasks from immersive training and simulation to rehabilitation and pain management.

The continuous innovation and commercialization of VR hardware have made it a foundational element for expanding VR’s role in healthcare, enabling more interactive, realistic, and effective medical solutions. For instance, in April 2024, the FDA's "Home as a Health Care Hub" initiative is a comprehensive effort to reimagine the home as a central part of the healthcare system, aiming to make healthcare more equitable and accessible, especially for underserved populations.

This initiative leverages augmented reality (AR) and virtual reality (VR) technologies to help integrate medical devices and digital health solutions into everyday home environments. These factors have solidified the segment's position in the global virtual reality in healthcare market.

Global Virtual Reality in Healthcare Market – Geographical Analysis

North America is expected to hold 46.7% of the global virtual reality in healthcare market in 2024

North America stands at the forefront of the virtual reality (VR) in healthcare market, propelled by several powerful drivers. The region benefits from a mature healthcare infrastructure and early adoption of digital technologies, particularly in the United States, which enables the swift integration and scaling of VR solutions across clinical environments.

The presence of major VR and healthcare technology companies, coupled with robust government and private investment, accelerates innovation and the development of new VR applications. Regulatory support, such as FDA approvals for VR-based medical devices like EaseVRx for pain management, further boosts confidence and adoption among healthcare providers.

A strong demand for advanced medical training and improved surgical precision is another key driver, as VR allows practitioners to visualize complex anatomical structures in 3D and practice procedures in immersive environments, leading to better outcomes.

The expansion of telemedicine and remote care is also significant, with VR enabling remote consultations, rehabilitation, and therapy, crucial for reaching underserved and rural populations. Cost reduction and efficiency gains are realized by minimizing surgical errors, shortening hospital stays, and streamlining training, all of which contribute to a more effective healthcare system.

Additionally, the market is fueled by a growing emphasis on personalized, patient-centric care, with VR offering tailored therapy experiences that enhance patient engagement. Ongoing advancements in VR hardware and software, as well as integration with other digital health solutions, continue to broaden the range and effectiveness of VR in healthcare. Collectively, these drivers ensure North America’s leadership in the VR healthcare market, supporting sustained growth and ongoing innovation in the sector.

For instance, in May 2024, AppliedVR, a pioneer in immersive therapeutics advancing a novel approach to medicine, launched its flagship RelieVRx prescription therapeutic into workers’ compensation. The RelieVRx device is the first comprehensive, immersive adjunctive virtual reality treatment for chronic lower back pain to ever be FDA-authorized. Thus, the above factors are consolidating the region's position as a dominant force in the global virtual reality in healthcare market.

Asia Pacific is expected to hold 23.4% of the global virtual reality in healthcare market in 2024

The Asia-Pacific region is rapidly emerging as a key player in the virtual reality (VR) healthcare market, fueled by several important factors. Significant investments in healthcare infrastructure, supported by both the government and private sectors, are paving the way for the widespread adoption of VR technologies. With a large and growing population, the region faces high demand for accessible, affordable, and high-quality healthcare, making VR solutions particularly valuable for expanding medical training and delivering specialized care to remote and underserved communities.

Government support is a major catalyst, with countries like China, Japan, and India rolling out national policies and funding initiatives to promote digital health and VR integration. For instance, China’s Health China 2030 plan and similar strategies across the region are accelerating the adoption of immersive technologies in clinical practice.

Moreover, the integration of VR with other digital health trends such as big data, cloud computing, and the Internet of Things (IoT) is transforming healthcare delivery by enabling advanced diagnostics, personalized treatment, and real-time data visualization.

For instance, in July 2024, MediSim VR established Chennai’s first Virtual Reality (VR)-based Center of Excellence (CoE) for medical training at Sri Ramachandra Institute of Higher Education and Research (SRIHER). This advanced facility provides immersive and interactive VR training, allowing medical students from across India to engage in realistic medical scenario simulations within a safe, controlled environment. Thus, the above factors are consolidating the region's position as a dominant force in the global virtual reality in healthcare market.

Global Virtual Reality in Healthcare Market – Competitive Landscape

The major global players in the virtual reality in healthcare market include Google LLC, Microsoft, Siemens Healthineers AG, HTC Corporation, Koninklijke Philips N.V., Osso VR, Inc., Augmedix, VirtaMed AG, XRHealth Inc., Virtually Better Inc., CAE Inc., Fundamental Surgery, and MindMaze, among others.

Global Virtual Reality in Healthcare Market – Key Developments

In May 2025, UAE-based tech startup X-Technology unveiled its new immersive virtual reality (VR) platform, specifically developed to enhance emotional and cognitive well-being in clinical and rehabilitation environments.

In January 2025, the Indian Institute of Technology Delhi (IIT Delhi) launched a six-month Executive Programme in Virtual and Augmented Reality through its Continuing Education Programme (CEP). This blended learning course is designed for professionals and recent graduates who want to gain advanced knowledge and hands-on skills in AR and VR technologies.

In December 2024, Sony and Siemens are collaborating to launch a new virtual reality (VR) headset specifically designed for industrial applications. Unlike consumer-focused VR headsets like the Apple Vision Pro or Meta Quest Pro, this device is tailored for professionals in engineering, product design, and manufacturing.

In November 2024, Meta introduced the Meta for Education beta program, a new initiative aimed at colleges and universities that provides education-specific extended reality (XR) services using the Meta Quest portfolio of virtual reality (VR) and mixed reality (MR) headsets.

In April 2024, Osso VR launched its Healthcare XR (extended reality) training application specifically for the Apple Vision Pro, a cutting-edge spatial computing headset from Apple. The Vision Pro offers advanced features such as high-resolution displays, precise hand tracking, and spatial awareness, making it an ideal platform for immersive training.

In February 2024, MediThinQ, a pioneering Korean startup, became the first Asian company to globally launch extended reality (XR) wearable surgical displays designed for use in live surgeries. These innovative devices, such as Scopeye and MetaSCOPE, present critical surgical information directly in front of the surgeon’s eyes, eliminating the need to look away at external screens.

Global Virtual Reality in Healthcare Market – Scope

Metrics | Details | |

CAGR | 27.5% | |

Market Size Available for Years | 2022-2033 | |

Estimation Forecast Period | 2025-2033 | |

Revenue Units | Value (US$ Bn) | |

Segments Covered | Component | Hardware, Software, Services |

Device | Head-Mounted Display (HMD), Gesture-Tracking Device (GTD), Projectors & Display Wall (PDW), Others | |

Technology | Non-Immersive VR, Semi-Immersive VR, Fully Immersive VR, Others | |

Deployment | Standalone VR Systems, Tethered VR Systems, Cloud-Based VR Solutions, Custom VR Solutions, Others | |

Application | Medical Training & Education, Mental Health, Surgical Assistance, Telemedicine and Remote Care, Fitness & Wellness, Pain Management, Patient Care Management, Rehabilitation and Therapy Procedures, Others | |

End-User | Hospitals & Clinics, Rehabilitation Centers, Pharmaceutical Companies, Others | |

Regions Covered | North America, Europe, Asia-Pacific, South America, and the Middle East & Africa | |

The global virtual reality in healthcare market report delivers a detailed analysis with 95 key tables, more than 96 visually impactful figures, and 173 pages of expert insights, providing a complete view of the market landscape.