UV Cured Printing Inks Market Overview

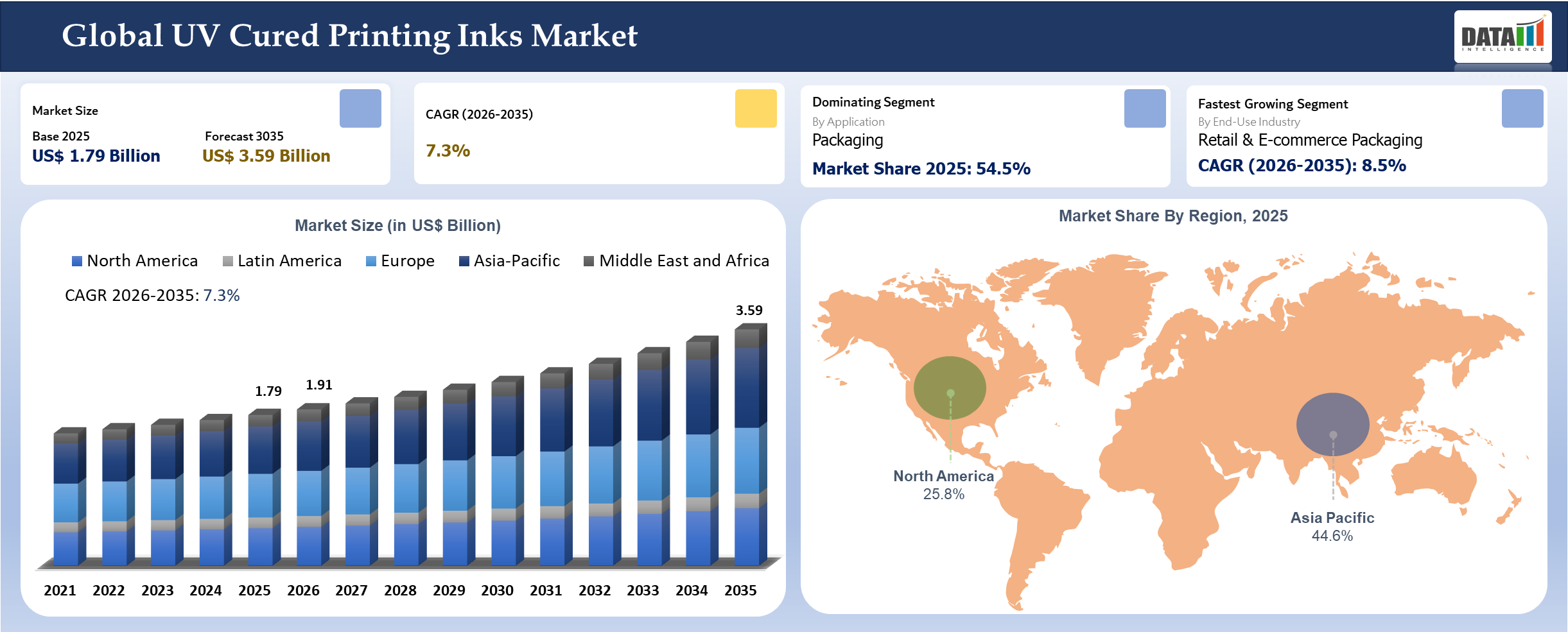

The global UV cured printing inks market reached US$ 1.79 billion in 2025 and is expected to reach US$ 3.59 billion by 2035, growing with a CAGR of 7.3% during the forecast period 2026-2035.

The market exhibits growth owing to rising demand for efficient and environmentally friendly print solutions in packaging, commercial, and industrial sectors. The instant drying capacity, lower volatile organic compounds (VOC) emissions, and adhesive quality offered by UV cured inks make them more favorable than solvent inks. In a statement by European Printing Ink Association, it is evident that the use of UV cured ink technology greatly lowers VOC emission levels compared to ordinary inks, which follows the EU Industrial Emissions Directive. On the other hand, VOC emissions from solvent printing cause ground-level ozone, hence making UV curable ink technology more popular.

The packaging industry is considered one of the major growth engines considering rapid changes in the e-commerce and consumer goods industries. The UV ink is particularly preferred for usage in food and pharmaceutical packaging due to its low migration and compliance with the safety standards. Moreover, according to the Food and Agriculture Organization, there is an increasing rate of food consumption throughout the world that contributes to the growth of the packaging industry and consequently raises the need for advanced printing ink. Finally, the growing trend of flexible packaging requires ink that would be readily cured on different materials such as plastic, foil, and paper.

Industry regulations and sustainable activities are now becoming some of the most important variables affecting the operations within the industry. This has been demonstrated by such things as the REACH Act in Europe and other regulations in North America and Asia which encourage companies to embrace environmentally sustainable printing technology. According to reports by the International Energy Agency, the increase in energy efficiencies through such technologies as UV curing may result in energy savings up to 50%, as opposed to traditional thermal energy.

UV Cured Printing Inks Industry Trends and Strategic Insights

- The transition to UV LED technology for curing purposes continues to accelerate, resulting in decreased energy use and cost savings during production.

- Because of rising government restrictions regarding the release of volatile organic compounds (VOCs), there is an increasing demand for UV ink-based solutions globally.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 1.79 Billion | |

| 2035 Projected Market Size | US$ 3.59 Billion | |

| CAGR (2026-2035) | 7.3% | |

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Ink Type | Free Radical UV Inks, Cationic UV Inks, Hybrid UV Systems | |

| ByPrinting Technology | UV Flexographic Inks, UV Offset Inks, UV Screen Printing Inks, UV Gravure Inks, UV Digital / Inkjet Inks, Others | |

| By Curing Technology | Mercury Arc UV Curing, LED UV Curing, Electron Beam (EB) Curing, Dual Curing Systems | |

| By Substrate Type | Flexible Substrates, Rigid Substrates, Paper & Paperboard, Specialty Substrates | |

| By Curing Speed | Fast Curing UV Inks, Conventional Curing UV Inks | |

| By Adhesion Performance | High Adhesion UV Inks, Standard Adhesion UV Inks | |

| By Migration & Compliance | Low Migration UV Inks, Standard UV Inks | |

| By Performance Grade | High Performance UV Inks, Standard Performance UV Inks | |

| By Sustainability Profile | Bio-based UV Inks, Conventional UV Inks | |

| By Pigmentation & Opacity | High Opacity & Pigmented UV Inks, Standard UV Inks | |

| By Application | Packaging, Labels & Tags, Commercial Printing, Publication Printing, Industrial Printing, Others | |

| By End-Use Industry | Food & Beverage Packaging, Pharmaceuticals & Healthcare, Cosmetics & Personal Care, Consumer Goods, Electronics & Electrical, Automotive & Industrial Components, Retail & E-commerce Packaging, Printing & Publishing Industry | |

| By Distribution Channel | Direct Sales, Distributors & Dealers, Online B2B Chemical Platforms, Specialty Chemical Suppliers | |

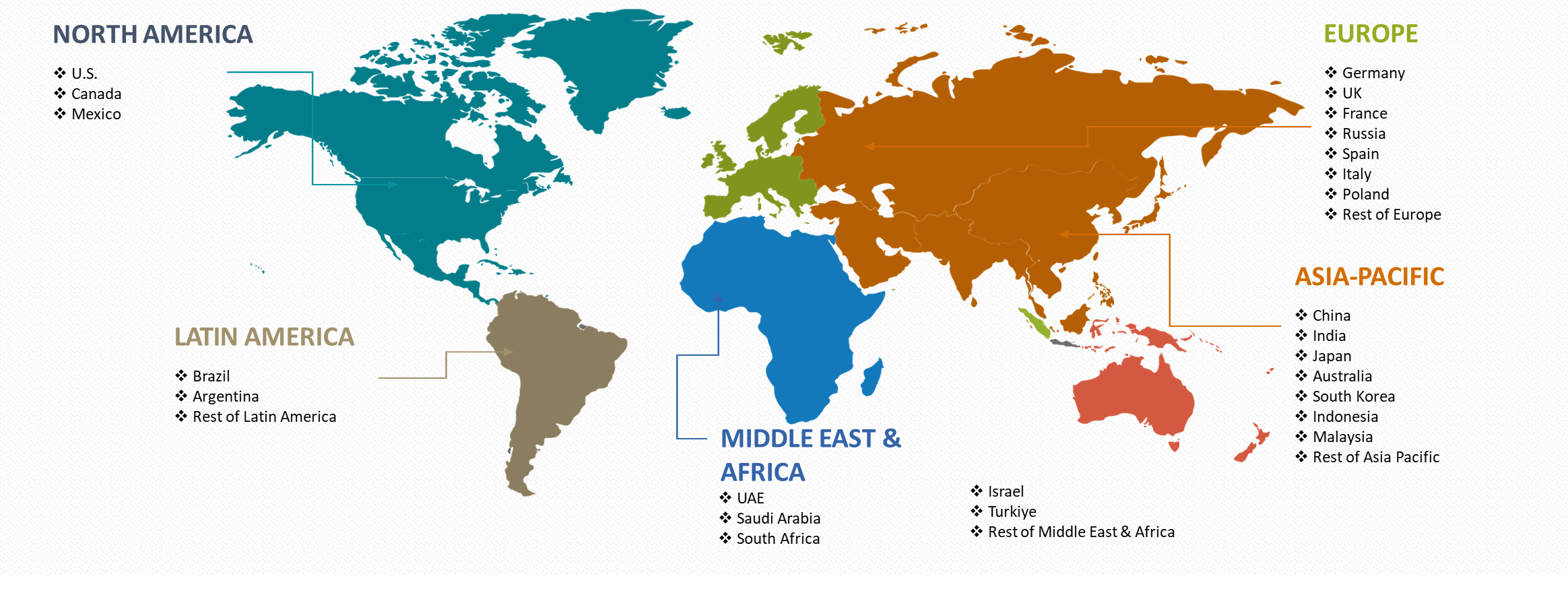

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

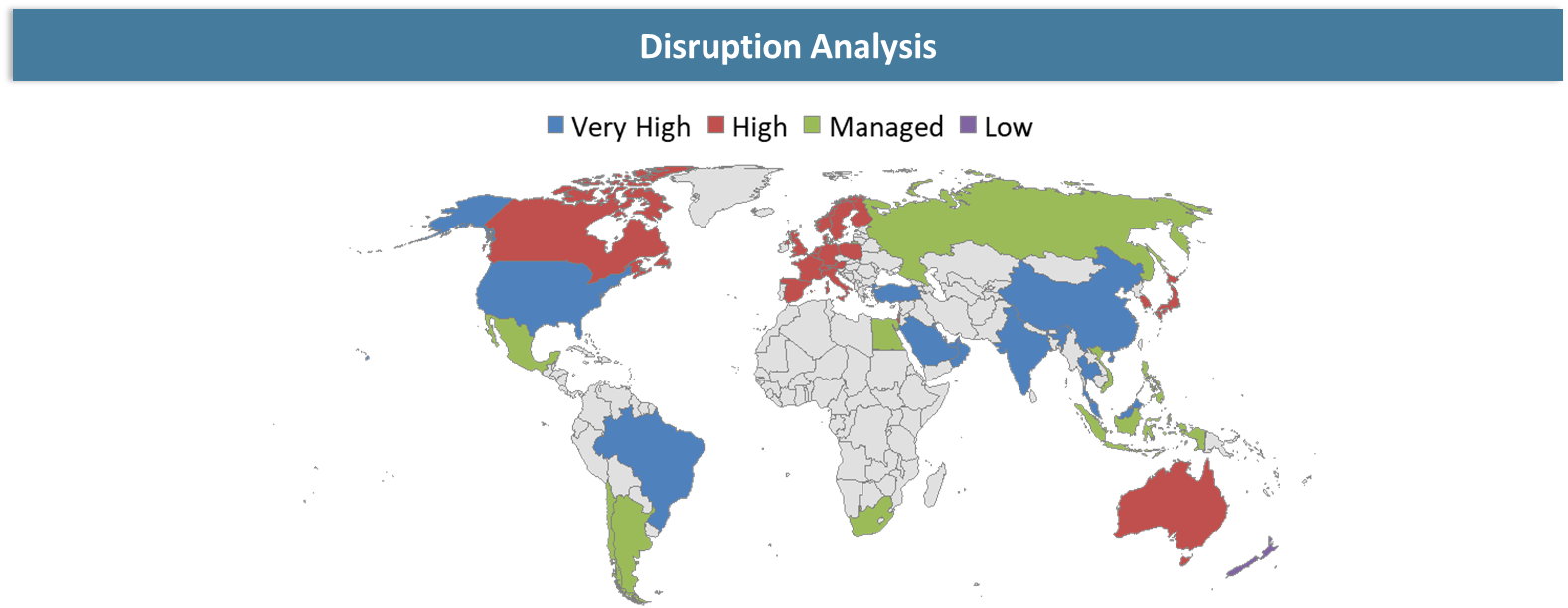

Disruption Analysis

The innovations in LED-UV curable ink technology has assisted in saving energy consumption and substrate application, consequently affecting the patterns of competition. The new regulations on sustainability concerning the VOCs will force ink manufacturers to give up solvent-based technology in favor of UV-curable options, thus fostering innovation and development of eco-friendly products. The rise of popularity of inkjet digital printing is shifting analog printing-related market structures, and, consequently, there is a need for fast-drying UV ink of high quality. High costs of the specialized machinery, volatility in pricing for basic materials, and disruptions in supply chains can also be highlighted as the main impediments to UV curved printing inks market growth.

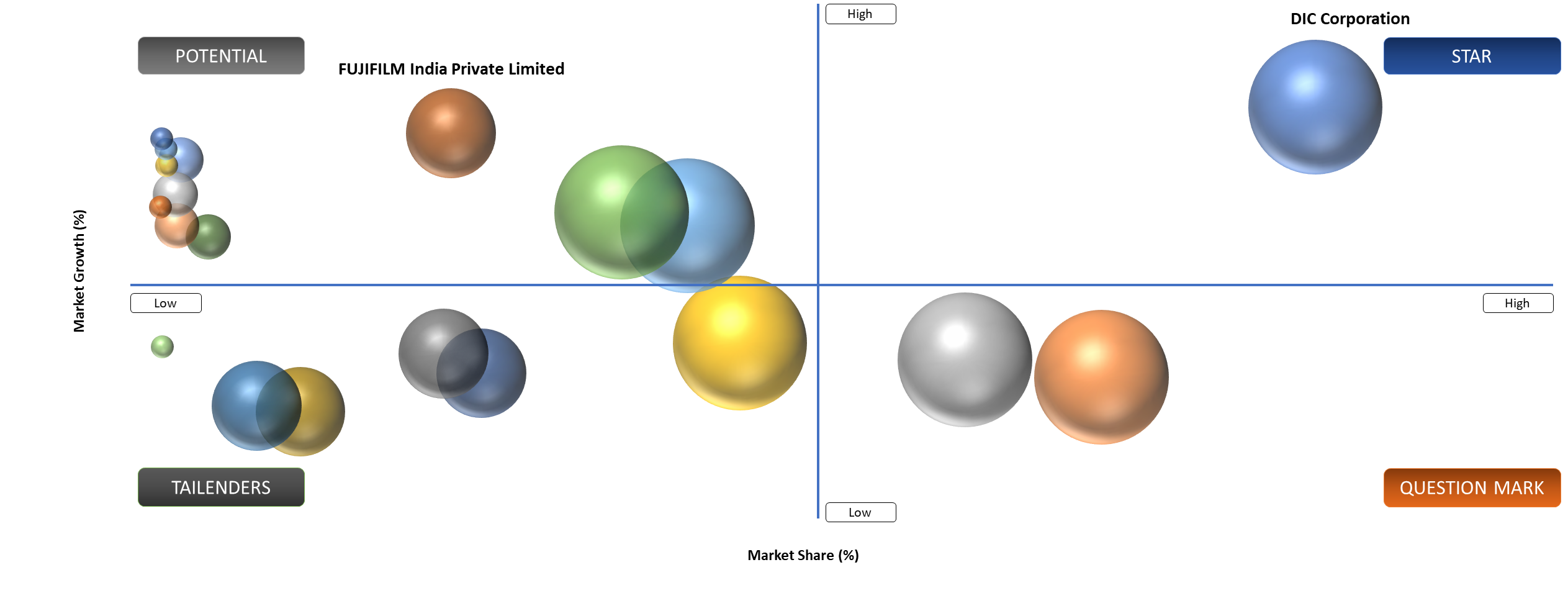

BCG Matrix: Company Evaluation

The global market for UV-cured printing ink can be analyzed via the BCG Matrix considering the growth and market shares of the application segments. The stars are the application segments in packaging, especially in packaging of food & beverages and e-commerce packaging, which is characterized by an increase in demand for fast and eco-friendly printing techniques. The cash cows are traditional applications in commercial printing and publications since UV inks have achieved widespread usage in them, thus producing steady revenue despite slow growth. The question marks are new applications in electronics printing, 3D printing, and industrial coatings, which demonstrate high growth potential and need to overcome adoption barriers regarding cost and technology. The dogs are application segments that generate low growth, such as conventional offset printing moving gradually from solvent-based printing inks.

Market Dynamics

Rising Adoption of Sustainable Printing Technologies

The shift towards sustainable manufacturing on a global scale plays a crucial role in propelling the growth of the market for UV cured printing inks. Solvent inks pose health hazards to the environment by emitting dangerous pollutants, whereas UV cured inks are environmentally friendly with negligible emissions and minimal wastage. As stated by the United Nations Environment Programme, the adoption of sustainable production methods is key to decreasing emissions from industrial activities, with printing being among sectors currently experiencing fast change.

Raw Material Price Volatility and Regulatory Compliance Challenges

Although there is great potential for expansion in the market, certain difficulties exist in relation to the volatile pricing of raw materials and strict regulations. Photo initiators, oligomers, and speciality resins which form key raw materials in the development of the products are characterized by high price fluctuations. It is largely because they are sourced through complex supply chains and involve reliance on petrochemicals. According to the International Monetary Fund, commodity price volatility continues to be a significant problem for manufacturing industries throughout the world. There is also greater regulatory scrutiny in some cases for the photo initiators and other chemical composition used in UV ink products.

Segmentation Analysis

The global UV cured printing inks market is segmented based on the ink type, printing technology, curing technology, formulation type, substrate type, curing speed, adhesion performance, migration & compliance, performance grade, sustainability profile, pigmentation & opacity, application, end-use industry, functionality, distribution channel and region.

Packaging Segment Leads Market Demand

Packaging sector makes the biggest share of UV printing ink industry because of the massive usage in label printing, flexible packing materials, and hard packing. As per the World Packaging Organization, there is a growing need for packaging products in the entire world on account of urbanization and changing lifestyles of the people. UV printing ink is used extensively for food packaging products due to the quality and healthiness of print that can be obtained through UV printing. Since 2023, there has been significant investment in UV printers by most leading packaging firms because of higher demands for sustainability and production speed.

Digital Printing and Industrial Applications Gain Traction

The use of digital printing technology will further increase the demand for UV curing inks. UV inkjet printing has been used extensively in various industrial processes like electronics, automotive parts, and decorative printing. The International Data Corporation claims that usage of digital printing technology has been increasing in various industrial sectors due to its customized production and decreased costs of setting up the process. UV ink allows printing even on non-porous material like metals, plastics, and glass, which makes it more useful in industries. In electronic products, UV ink can be used for printing on circuit boards and labeling.

Geographical Penetration

North America Leads in Enterprise Adoption and Platform Investment

North America is an example of a developed market with extensive use of sophisticated printing technology and rigorous environmental laws. The Printing Industries of America highlights the continent’s commitment to innovative and high-quality products with considerable spending on UV LED curable inks. The USA is at the forefront of innovations, especially in industry and specialized printing. The government’s sustainability programs and emission control measures have also facilitated the adoption of UV curable inks in different industries.

U.S. UV Cured Printing Inks Market Outlook

The use of UV curable printing ink in the United States is motivated more by packaging and labeling and high-performance printing purposes than traditional publishing. Pressure from regulating bodies such as the U.S. Environmental Protection Agency is leading to the transition into lower VOCs and more energy-efficient ink solutions. UV inks produce less volatile organic compounds than solvent inks, thus conforming to the national clean air regulations. The top companies operating within the segment, including Sun Chemical and INX International Ink Co., are developing LED-UV ink technologies that consume up to 50 percent less energy than mercury bulbs as confirmed by data from the U.S. Department of Energy. Moreover, the packaging market in the United States, which is supported by rapidly growing e-commerce activity, depends heavily on UV inks for faster and highly durable printing processes as highlighted by the Flexible Packaging Association.

Canada UV Cured Printing Inks Market Outlook

The Canadian market for UV-cured printing inks continues to grow due to the environmental sustainability regulations and improved printing technologies. With the support of Environment and Climate Change Canada in terms of environmental regulations, many industries use UV ink due to their low emission properties. Moreover, to cut down carbon emissions and costs, many Canadian companies in the field of packaging and labeling are using UV LED ink technology. There is an active industrial program to encourage LED technology in printing due to less electricity usage and prolonged operation of lamps. In addition, companies including Flint Group and Siegwerk Druckfarben AG & Co. KGaA manufacture specific UV inks for food packaging in accordance with the requirements of Health Canada.

Asia-Pacific: The World’s Fastest-Growing Region

Asia-Pacific occupies the highest market share in the global market for UV-cured ink. The reasons include industrialization, development in the packaging sector, as well as effective manufacturing. From the Asian Development Bank report, the region is still dominant in the world’s production capacity of manufacturing goods. Countries making up the market share in this region include China, India, Japan, and South Korea among others. In China, there is widespread use of UV ink in the packaging and electronics manufacturing industries.

India UV Cured Printing Inks Market Insights

The Indian market stands out as a promising market for UV cured printing inks on account of the booming packaging, labeling, and commercial printing market. The efforts of the government towards the growth of domestic industries under “Digital India” and “Make in India” programs have contributed towards increasing demand in these sectors. Moreover, the regulation by Central Pollution Control Board is also promoting the use of environmentally friendly ink solutions. In addition, India has a large annual production capacity for packaging estimated at more than 20 million tons per year where flexible packaging is experiencing high growth rate. The preference for instant curing and non-waste producing UV ink solutions has increased due to high-speed printing machines. Players such as Toyo Ink SC Holdings and DIC Corporation are focusing on the growth opportunities in this market via research and localized production of inks

China UV Cured Printing Inks Industry Growth

In terms of the Asia Pacific region, China occupies a dominant position in the use of UV cured printing inks due to the large-scale production capabilities of the country and its commitment to sustainable and green development. Policies that have been set within the framework of the "Blue Sky Protection Campaign" by the Ministry of Ecology and Environment of China have controlled the emissions of VOCs, thus stimulating the shift from solvent-based inks to UV curable formulations. The Chinese nation leads in the global market on the packaging production, which produces more than 120 million tons annually, as estimated by the China Packaging Federation, generating huge demand for effective inks. Foreign and local companies, such as FUJIFILM, T&K TOKA Corporation, focus on advanced UV ink production as well as its compatibility with digital printing.

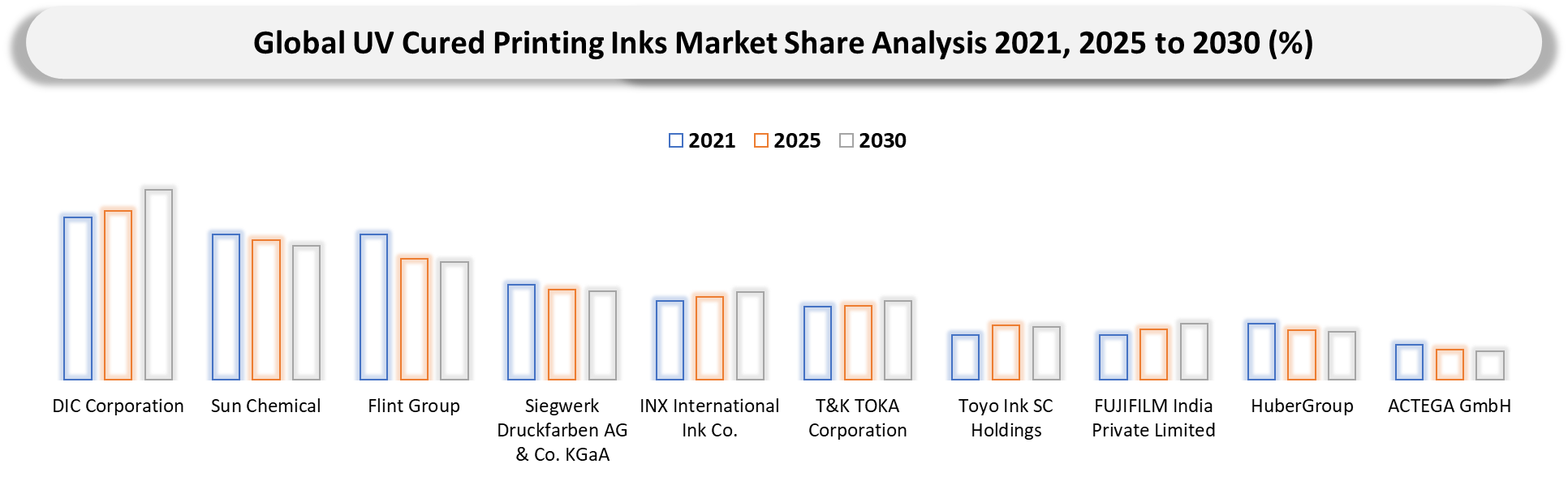

Competitive Landscape

- The global market for UV ink used for printing purposes has a very competitive environment, with players concentrating primarily on innovating, being environmentally sustainable, and producing high-quality products.

- Some of the leading companies in this market include DIC Corporation, Sun Chemical, Flint Group, Siegwerk Druckfarben AG & Co. KGaA, INX International Ink Co., T&K TOKA Corporation, Toyo Ink SC Holdings, and FUJIFILM Holdings Corporation.

- There have been increased activities by many of these firms in terms of conducting research and developing new low migration inks and ink systems suitable for LED applications.

- Mergers, acquisitions, and collaborations have become common trends among many organizations within this market due to expansion needs.

Key Developments

- April 2026: HuberGroup announced development of UV LED inks with reduced migration and improved sustainability, targeting food-safe packaging and regulatory compliance across global markets.

- March 2026: Sun Chemical expanded sustainable UV ink portfolio focusing on low-migration formulations for food packaging, aligning regulatory compliance and circular economy commitments globally.

- March 2026: Toyo Ink SC Holdings expanded production capacity for UV-curable inks in Asia, addressing growing packaging demand and strengthening regional supply chain resilience and customer responsiveness.

- February 2026: Van Son Ink Corporation developed high-performance UV offset inks with improved press stability and color consistency, targeting premium packaging and commercial printing applications globally.

- January 2026: Flint Group launched advanced UV LED curing inks for flexible packaging, enhancing energy efficiency, curing speed, and print durability across high-speed printing applications.

- January 2026: SICPA Holding SA advanced UV security inks with enhanced anti-counterfeiting features, integrating digital authentication technologies for banknotes and secure packaging applications.

- December 2025: T&K TOKA Corporation developed UV offset inks with improved adhesion and low migration properties, targeting food packaging compliance and high-performance commercial printing segments.

- November 2025: DIC Corporation developed next-generation UV-curable overprint varnish combined with oil-based inks for paper containers, improving sustainability, recyclability, and performance in terms of packaging significantly.

- November 2025: Marabu GmbH & Co. KG introduced UV digital inks for industrial inkjet applications, enhancing adhesion, chemical resistance, and compatibility with diverse substrates including plastics and metals.

- October 2025: INX International Ink Co. commercialized UV LED inks for digital and metal decorating markets, improving energy efficiency and enabling faster curing for industrial printing applications.

- September 2025: ACTEGA GmbH launched sustainable UV coatings and inks portfolio emphasizing recyclability, low VOC emissions, and compatibility with circular packaging systems globally.

- August 2025: FUJIFILM India Private Limited introduced UV inkjet solutions for commercial printing, enhancing color gamut, curing efficiency, and productivity for digital printing applications in India.

- June 2025: Wikoff Color Corporation expanded UV ink production capabilities focusing energy-efficient curing technologies, supporting commercial printing customers transitioning to sustainable printing solutions.

Why Choose DataM?

- Technological Innovations: Explores the latest advancements in UV cured printing inks, including improved photo initiator systems, low-migration formulations, LED UV curing compatibility, enhanced adhesion technologies and sustainable raw material integration that drive faster curing speeds, superior print quality and reduced energy consumption across packaging and commercial printing applications.

- Product Performance & Market Positioning: Evaluates how different manufacturers perform across packaging, labels, commercial printing and industrial printing environments. The analysis compares curing speed, color vibrancy, substrate compatibility, chemical resistance, durability and regulatory compliance, highlighting how leading players differentiate through high-performance and eco-friendly formulations.

- Real-World Evidence: Highlights practical use cases of UV cured printing inks across flexible packaging, label printing, publication printing and specialty applications. It demonstrates measurable improvements in production efficiency, reduced drying time, enhanced print consistency and minimized waste generation in high-speed printing operations.

- Market Updates & Industry Changes: Tracks key industry developments such as new product launches, advancements in LED UV curing systems, increasing adoption of low-VOC and sustainable inks, regulatory shifts (food safety and environmental compliance) and evolving demand patterns across regions including North America, Europe, APAC and emerging markets.

- Competitive Strategies: Analyzes how leading ink manufacturers are expanding their footprint through product innovation, strategic collaborations with printing equipment manufacturers, regional production expansion, sustainability-focused product lines and digital printing integration to strengthen competitive positioning.

- Pricing & Market Access: Explains pricing structures across standard, specialty and high-performance UV ink formulations, including bulk procurement, contract-based supply and distributor-driven sales models. It also reviews regional availability, supply chain dynamics and pricing strategies influenced by raw material costs and regulatory requirements.

- Market Entry & Expansion: Identifies growth opportunities in emerging markets driven by expanding packaging industries, e-commerce growth, rising demand for high-quality printing and regulatory push for sustainable inks. It outlines strategies for manufacturers to scale through localized production, partnerships with converters and investments in advanced curing technologies.

Target Audience 2026

- Packaging & Labeling Companies: Flexible packaging converters, label manufacturers and carton producers utilizing UV cured inks for high-quality, durable and fast-curing print applications.

- Commercial Printing Firms: Offset, digital and screen-printing companies adopting UV inks for superior print quality, faster turnaround and reduced drying time.

- Publication & Graphics Industry: Magazine publishers, advertising agencies and graphic designers leveraging UV inks for vibrant colors, gloss effects and enhanced visual appeal.

- Industrial & Specialty Printing Providers: Electronics, automotive and 3D printing firms using UV inks for functional coating, circuit printing and product decoration.

- OEMs & Printing Equipment Manufacturers: Press manufacturers and ink formulators focusing on UV curing technologies, innovation benchmarking and product differentiation strategies.

- Raw Material & Chemical Suppliers: Photo initiator, oligomer and pigment suppliers supporting UV ink formulations and advancing sustainable, low-VOC solutions.

- Investors & Private Equity Firms: Investment entities tracking growth in sustainable printing technologies, digital printing adoption and regulatory-driven ink innovations.

- Distributors & Channel Partners: Ink distributors, dealers and aftermarket service providers managing supply chains, technical support and regional market penetration.