United Stated Natural Caffeine Market Size & Forecast 2032

As per DataM Intelligence analysis, the United States natural caffeine market was US$ 629.49 million in 2025 and is expected to reach up to US$ 1,062.91 million in 2032, growing at a CAGR of 7.8% during the forecasting period (2026-2032).

The demand for caffeinated beverages continues to surge, driven by widespread consumer habits and cultural acceptance. Globally, around 2.25 billion cups of coffee are consumed daily and the National Coffee Association’s Spring 2024 report highlights that 67% of American adults consumed coffee in the past day, a 37% increase since 2004, marking the highest consumption in over two decades. This sustained popularity underscores coffee’s pivotal role as a primary source of natural caffeine.

This rising consumption aligns with a growing consumer preference for organic and natural products, further fueling the natural caffeine market. According to the Organic Trade Association, US sales of certified organic products grew by 5.2% in 2024, more than double the overall market growth of 2.5%. The 2025 Organic Market Report notes that organic product sales reached a record US$71.6 billion, signaling a strong shift toward healthier, sustainably sourced ingredients. Natural caffeine, being plant-derived, fits squarely within this trend.

On the supply side, global caffeine production remains concentrated in key coffee-producing countries, with Brazil, Vietnam, and Colombia together producing over 170 million 60-kg bags annually. This robust supply infrastructure ensures availability of natural caffeine for both beverages and functional food applications.

At the same time, workplace fatigue has become a pressing consumer concern. A survey of over 2,000 working adults found that 97% face at least one fatigue risk factor, while more than 80% experience two or more. This widespread need for sustained energy is driving demand for natural caffeine-based functional beverages and supplements.

Key Takeaways

- Market to Exceed US$ 1 Billion by 2032. The USA natural caffeine market is projected to grow from US$ 629.49 million in 2025 to US$ 1,062.91 million by 2032, registering a CAGR of 7.8%. Growing demand for clean-label and plant-based ingredients is accelerating market expansion.

- Coffee Remains the Dominant Natural Caffeine Source. Coffee continues to be the primary source of natural caffeine, supported by strong consumer demand. Nearly 67% of American adults consume coffee daily, making coffee-derived caffeine a critical ingredient for beverages, supplements, and functional foods.

- Functional Beverages Are Driving Ingredient Demand. The rapid growth of energy drinks, RTD beverages, and wellness drinks is creating substantial demand for natural caffeine. Younger consumers, particularly Gen Z and Millennials, increasingly prefer plant-based energy solutions over synthetic stimulants.

- Clean-Label and Organic Trends Are Reshaping Purchasing Decisions. Consumer preference for natural and transparent ingredients is strengthening market growth. Organic product sales in the U.S. reached US$ 71.6 billion in 2025, highlighting strong demand for naturally sourced ingredients such as coffee, tea, guarana, and yerba mate extracts.

- Beyond Beverages, New Growth Opportunities Are Emerging. Natural caffeine is expanding into dietary supplements, sports nutrition, pharmaceuticals, and personal care products. The U.S. beauty industry, valued at over US$ 646 billion, is increasingly incorporating caffeine into skincare and body care formulations, opening new revenue streams for ingredient suppliers.

MARKET DYNAMICS

Drivers

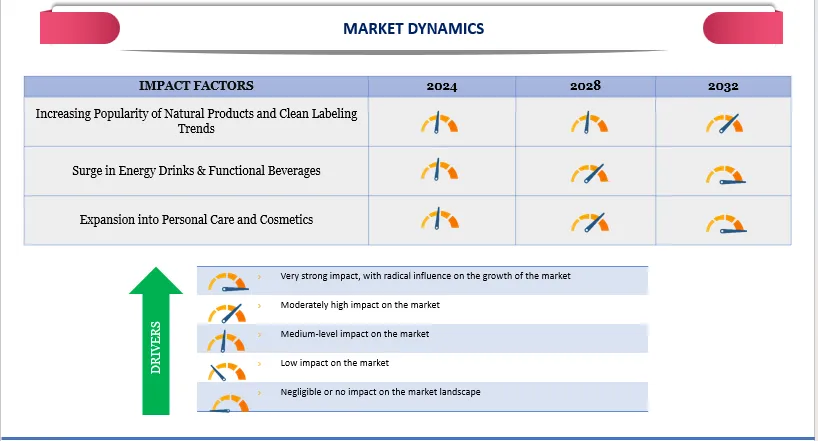

Increasing Popularity of Natural Products and Clean Labeling Trends

The increasing popularity of organic and natural products is a major driver of growth in the natural caffeine market. As consumers become more health-conscious, they are actively seeking products made with clean, plant-based, and non-synthetic ingredients.

According to the 2024 IFIC Food & Health SURVEY, 36% of shoppers associate food safety with products labeled as “Natural,” “Organic,” or “Healthy.” These clean-label claims are the top in-store safety signals, especially among older consumers and higher-income households.

Moreover, an overwhelming 50% of industry professionals identified clean label ingredients as the top trend in the food and beverage sector. This shift in consumer preference favors natural caffeine, which is derived from sources such as coffee beans, green tea, guarana, and yerba mate. These ingredients are often associated with organic farming practices and perceived as safer and healthier compared to synthetic caffeine.

Surge in Energy Drinks & Functional Beverages

The surge in energy drinks and functional beverages is significantly driving the natural caffeine market, underpinned by rising consumer demand for convenient, health-oriented energy solutions. Data from the British Soft Drinks Association shows that in 2024, the UK consumed 1.2 billion liters of sports and energy drinks, up from 1.1 billion liters in 2023, reflecting a rising reliance on these products for daily energy and performance. Glanbia’s research further highlights that 18 to 34-year-old consumers are more likely to consume functional beverages multiple times a day than older age groups, with 17% of women and 23% of men in this demographic reporting more than once-a-day consumption, underscoring the high frequency of intake.

This behavioral trend directly influenced product innovation, encouraging manufacturers to integrate natural caffeine sources into beverages. At SupplySide Global 2025 in Las Vegas, CREATEA debuted as a ready-to-drink canned beverage blending creatine, natural caffeine, and a non-sugar sweetener in a Mighty Mango flavor, demonstrating how brands are combining natural stimulants with performance-enhancing ingredients. By targeting both muscle and brain health, CREATEA exemplifies the market’s move toward multifunctional drinks, reinforcing natural caffeine’s role as a core component of energy and cognitive support formulations.

Expansion into Personal Care and Cosmetics

The expansion of natural caffeine into personal care and cosmetics is emerging as a strong growth driver for the USA natural caffeine market, supported by the rapid scale of the beauty industry. With the beauty market reaching US$646.2 billion by the end of 2024, brands are actively seeking functional, natural ingredients to differentiate products. Natural caffeine fits this demand due to its proven benefits for skin stimulation, cleansing, and rejuvenation. This creates a strong foundation for caffeine’s increasing adoption beyond food and beverages.

Building on this momentum, personal care brands are leveraging caffeine to transform routine skincare into performance-driven experiences. In October 2022, mCaffeine launched its biggest-ever body care range, introducing nine products infused with natural coffee and caffeine across pre-shower, shower, and post-shower categories. By combining caffeine with ingredients like hyaluronic acid, oils, clay, and shea butter, the brand showcased caffeine’s versatility. Such launches highlight how natural caffeine is becoming central to modern body care innovation. This shift reflects a broader consumer move toward clean-label, sensory-rich, and ingredient-led beauty products. Brands increasingly position caffeine not just as an active ingredient but as an emotional and experiential element tied to wellness and self-care.

Impact Factors

RESTRAINTS

Supply Chain Complexity & Raw Material Availability

The natural caffeine market heavily relies on plant sources like coffee beans, guarana, and tea leaves, which are predominantly grown in specific regions. The geographical dependency makes the supply chain vulnerable to local climate fluctuations, pests, and soil conditions. Any disruption in these regions can directly reduce the availability of raw materials. Consequently, manufacturers face challenges in maintaining a stable production schedule.

Seasonal variations further complicate the supply chain, as harvesting periods differ across regions and crops. A delayed or poor harvest in one area can create bottlenecks in raw material availability for global manufacturers. This inconsistency forces companies to either stockpile resources at high costs or face intermittent shortages. Therefore, the market struggles to maintain a continuous supply of natural caffeine for end products.

Transportation and logistical challenges intensify the problem, as these raw materials often require careful handling and storage to preserve quality. Any disruption in shipping routes or customs procedures can delay delivery, affecting production timelines. The interconnectedness of production, storage, and distribution creates a fragile supply chain. This fragility increases operational costs and reduces market competitiveness against synthetic caffeine.

High Production Costs and Premium Pricing

The higher production cost inevitably leads to premium pricing, positioning natural caffeine products above their synthetic counterparts. Consumers, especially those sensitive to price, often hesitate to pay extra despite the perceived health benefits of natural sources. This price barrier limits mass adoption in key segments like beverages, energy drinks, and dietary supplements, where affordability is crucial for widespread use. As a result, even though demand for natural and clean-label ingredients is rising, the high retail price restrains the market’s growth potential.

The impact of premium pricing extends beyond end consumers to the business-to-business segment, affecting food and beverage manufacturers. Companies incorporating natural caffeine into their formulations face increased costs, which either reduce profit margins or get passed on to consumers. Smaller brands, in particular, struggle to compete with established players who can better absorb these costs, slowing the entry of innovative products into the market. The combined effect of limited affordability and cautious business investment further restrains the expansion of natural caffeine offerings.

Consumer Behavior Analysis

The natural caffeine market is experiencing robust growth driven by evolving consumer behaviors focused on health, wellness, and clean-label preferences. Consumers today are increasingly aware of the potential negative effects of synthetic caffeine and are shifting toward natural sources like green tea, guarana, yerba mate, and coffee bean extracts. There is a growing demand for beverages that not only provide energy but also offer additional health benefits such as antioxidants and improved mental focus. Younger demographics, particularly millennials and Gen Z, are leading this trend as they prioritize functional, natural, and sustainably sourced ingredients.

A 2024 survey by the National Coffee Association revealed that 67% of American adults drank coffee the previous day, reflecting nearly a 40% increase since 2004. Similarly, the Sleep Foundation reports that about 94% of American adults consume caffeinated beverages, with 64% doing so daily. This widespread daily caffeine use underscores a stable base of consumers who value caffeine’s stimulating effects. However, the growing awareness of health and wellness is driving many to seek natural caffeine sources, as people increasingly prefer clean-label, minimally processed, and plant-based options.

MARKET SEGMENTATION

BY SOURCE TYPE

- Coffee

- Tea

- Guarana

- Cocoa

- Kola Nut

- Yerba Mate

- Others

The US Department of Agriculture (USDA) projects global production to reach a record 178.7 million bags by 2025/26, driven primarily by recovery in Vietnam and Indonesia, alongside record output from Ethiopia. The segment faces structural challenges, with global consumption forecast at 169.4 million bags in 2025/26, creating persistent inventory tightness at 22.8 million bags.

The coffee sector generates over US$20 billion in annual production value globally, with total trade estimated at US$25 billion per year. In 2023, world production reached 11 million tonnes, with smallholder farmers accounting for 80% of global output. The coffee sector confronts a substantial research and development financing gap that threatens long-term sustainability. World Coffee Research (WCR) analysis reveals current global investment in coffee R&D stands at approximately US$115 million USD annually, representing merely 20% of the US$567 million required to meet consumer demand and maintain origin diversity amid climate change challenges.

The coffee supply chain demonstrates concerning fragility, with ending stocks projected at 20.9 million bags in 2024/25, down 1.5 million bags from the previous year. This inventory drawdown follows three consecutive years of decline, creating vulnerability to production shocks.

Forward market indicators suggest price moderation as production recovers, though structural challenges persist. The sector requires enhanced investment in climate-resilient varieties, improved disease management protocols, and strengthened seed distribution systems to ensure inclusive access to high-quality planting material.

BY FORM

- Powder

- Granules

- Liquid

- Encapsulated / Microencapsulated

- Others

The powder segment of the USA natural caffeine market is a critical format for industrial use because it enables standardized dosing, long shelf life, and efficient integration into large-scale food, beverage, supplement, and pharmaceutical manufacturing systems. Powdered natural caffeine is typically obtained through extraction from coffee beans or tea leaves, followed by purification and drying. This form allows manufacturers to accurately control caffeine concentration, which is essential for compliance with food safety regulations and for maintaining consistency across high-volume production runs. Regulatory authorities globally emphasize precise caffeine labeling and intake transparency, which further reinforces the preference for powdered caffeine formats in commercial formulations.

Powdered natural caffeine is favored because it enables accurate dosing and uniform dispersion across formulations, which is critical under regulatory frameworks governing added caffeine. The US Food and Drug Administration (FDA) requires clear declaration of added caffeine in foods and supplements and emphasizes consistency between labeled and actual caffeine content. Powdered caffeine allows manufacturers to meet these requirements more reliably than liquid or extract forms, particularly in dry blends, capsules, tablets, and instant beverage mixes. Agricultural production data further support the structural foundation of powdered natural caffeine supply. The FAO also reports that coffee cultivation supports the livelihoods of around 25 million farming households globally, enabling sustained upstream investment in extraction.

Beyond pharmaceuticals, dietary supplements represent another important granules-driven demand channel. Regulatory authorities such as the US FDA and European Food Safety Authority (EFSA) require clear caffeine dose declarations when used in supplements. Granulated caffeine allows manufacturers to meet these requirements by enabling precise micro-dosing, reducing variability during high-speed production.

BY DISTRIBUTION CHANNEL

- Direct sales

- Indirect Sales

BY APPLICATION

- Food & Beverages

- Dietary Supplements & Nutraceuticals

- Pharmaceuticals

- Cosmetics & Personal Care

- Others

In the United States, a mature and well-documented market, approximately 69% of the population consumes at least one caffeinated beverage daily. Coffee alone accounts for 69% of caffeine intake, soft drinks contribute 15.4%, tea 8.8%, and energy drinks, though smaller in share, represent an emerging segment. These statistics from national surveys highlight both the depth of caffeine penetration and the shifting dynamics among beverage categories, driven by evolving consumer preferences and lifestyle trends. Natural caffeine, derived from plant sources such as coffee beans, tea leaves, guarana, and yerba mate, is increasingly preferred over synthetic variants due to its association with clean-label and plant-based formulations. Beyond providing caffeine, these ingredients impart flavors and phytochemicals that align with health-conscious consumer expectations, making them highly relevant in food and beverage formulations.

Key Companies

Major companies listed in the report are Plant Lipids, Coffein Compagnie GmbH & Co. KG, Botanic Healthcare Pvt. Ltd., Shri Ahimsa Naturals Ltd., Cymbio Pharma Private Limited, Natura Vitalis Industries Pvt Ltd, AVT Natural, Applied Food Sciences, Inc., Sivaroma Naturals Pvt. Ltd., OmniActive Health Technologies Limited, NutriScience Innovations, LLC, Cepham, Vita Forte Inc, Vita Forte Inc, Anderson Global Group, LLC, Derivados Industrializados del Café S.A., UNICORN NATURAL PRODUCT LIMITED, CR3-Kaffeeveredelung GmbH, Descafeinadores Mexicanos S.A., EPC Natural Products Co., Ltd., Herbo Nutra Extract Private Limited, Hangzhou Muhua Bio-Tech Co., Ltd, Umang Global, and Elementa.

Applied Food Sciences, Inc.

Applied Food Sciences, Inc. is one of the prominent companies in the development and supply of functional, organic, and plant-based ingredients for the food, beverage, and nutraceutical industries. The company emphasizes ethical sourcing, sustainability, and transparency, working closely with rural farmers to ensure responsible supply chains.

It specializes in botanical extracts such as organic turmeric, ginger, acerola vitamin C, and lion’s mane mushroom, alongside its caffeine portfolio.

Its credibility is built on organic certifications, GRAS status, and non-GMO standards, making it a trusted partner for global brands seeking natural performance ingredients. AFS’s flagship PurCaf Organic Caffeine is an ingredient for brands targeting natural energy, focus, and endurance.

PRODUCT Portfolio

PurCaf by Applied Food Sciences is a, 100% organic-certified natural caffeine ingredient designed for the clean-label beverage and supplement market. Sourced from green coffee beans, it is uniquely water-soluble, non-GMO, and standardized to >95% caffeine content. As a plant-based, GRAS-affirmed ingredient, PurCaf offers brands a transparent and sustainable energy solution that meets the growing consumer demand for botanical transparency and performance.

Expansion

Applied Food Sciences (AFS) has partnered with Dempsey Corporation to expand the distribution of its functional ingredients, including PurCaf organic caffeine, across Canada. This collaboration leverages Dempsey’s extensive market reach and technical expertise to provide Canadian food, beverage, and supplement manufacturers with high-quality, science-backed, and clean-label botanical solutions.

OmniActive Health Technologies Limited

OmniActive Health Technologies Limited manufactures pharmaceuticals, medicinal chemicals, and botanical products. The company has established itself as a global supplier of science-backed nutritional and wellness solutions, with operations spanning India, North America, and Europe.

Its portfolio includes branded ingredients such as Lutemax for eye health, CurcuWIN for bioavailable curcumin, and Gingever for ginger extracts, serving the dietary supplement, functional food, and beverage industries.

With a strong R&D base and advanced manufacturing facilities, the company continues to expand its footprint in the global health and wellness market.

OmniActive’s Natural Caffeine meets European Commission guidelines for pesticide residues, solvent residues, mycotoxins, and heavy metals.

Product Portfolio

OmniActive’s natural caffeine is a 100% pure ingredient sourced directly from coffee seeds through a clean, solvent-free water extraction process. This excipient-free and fully water-soluble powder enhances mental alertness and physical performance while meeting stringent global safety standards for purity. It offers a premium, clean-label energy solution for dietary supplements and functional beverages without using synthetic additives or any carriers.

Recent Developments

Growing Regulatory Focus on Caffeine Transparency and Labeling

The proposed Sarah Katz Caffeine Safety Act in the U.S. seeks stricter caffeine labeling requirements, including disclosure of caffeine content, identification of natural vs. added caffeine, and consumer safety warnings. This reflects increasing regulatory attention on caffeine-containing foods, beverages, and dietary supplements.

FDA Reinforces Oversight of Highly Concentrated Caffeine Products

The FDA continues to strengthen guidance regarding highly concentrated caffeine used in dietary supplements and functional products. Manufacturers are being encouraged to improve dosage control, labeling, and consumer safety measures, which directly impacts natural caffeine ingredient suppliers.

OmniActive Expands Consumer Wellness Portfolio

OmniActive Health Technologies launched a refreshed global brand strategy in 2026 centered on Performance & Active Nutrition, Everyday Wellness, and Healthspan solutions. Natural caffeine remains a key ingredient supporting the company's functional beverage and dietary supplement offerings.

Applied Food Sciences Expands PurCaf Organic Caffeine Distribution

Applied Food Sciences expanded the distribution of its flagship PurCaf Organic Caffeine through a partnership with Dempsey Corporation, increasing market reach across North America and supporting growing demand for clean-label energy ingredients. (Referenced in company profile and expansion activities within the market.)

Rising Innovation in Functional and Ready-to-Drink Beverages

Manufacturers are increasingly incorporating natural caffeine into multifunctional beverages that support energy, cognitive performance, hydration, and wellness. Product innovations launched during 2025–2026 reflect strong demand for clean-label, plant-based energy solutions across the U.S. beverage sector.

Why Purchase the Report?

- To visualize the global natural caffeine market segmentation based on type, form, application, distribution channel and region, as well as understand key commercial assets and players.

- Identify commercial opportunities by analyzing trends and co-development.

- Excel data sheet with numerous data points of the natural caffeine market with all segments.

- PDF report consists of a comprehensive analysis after exhaustive qualitative interviews and an in-depth study.

- Product mapping available as excel consisting of key products of all the major players.

The global natural caffeine market report would provide approximately 70 tables, 64 figures and 146 pages.

Target Audience

- Manufacturers/ Buyers

- Industry Investors/Investment Bankers

- Research Professionals

- Emerging Companies