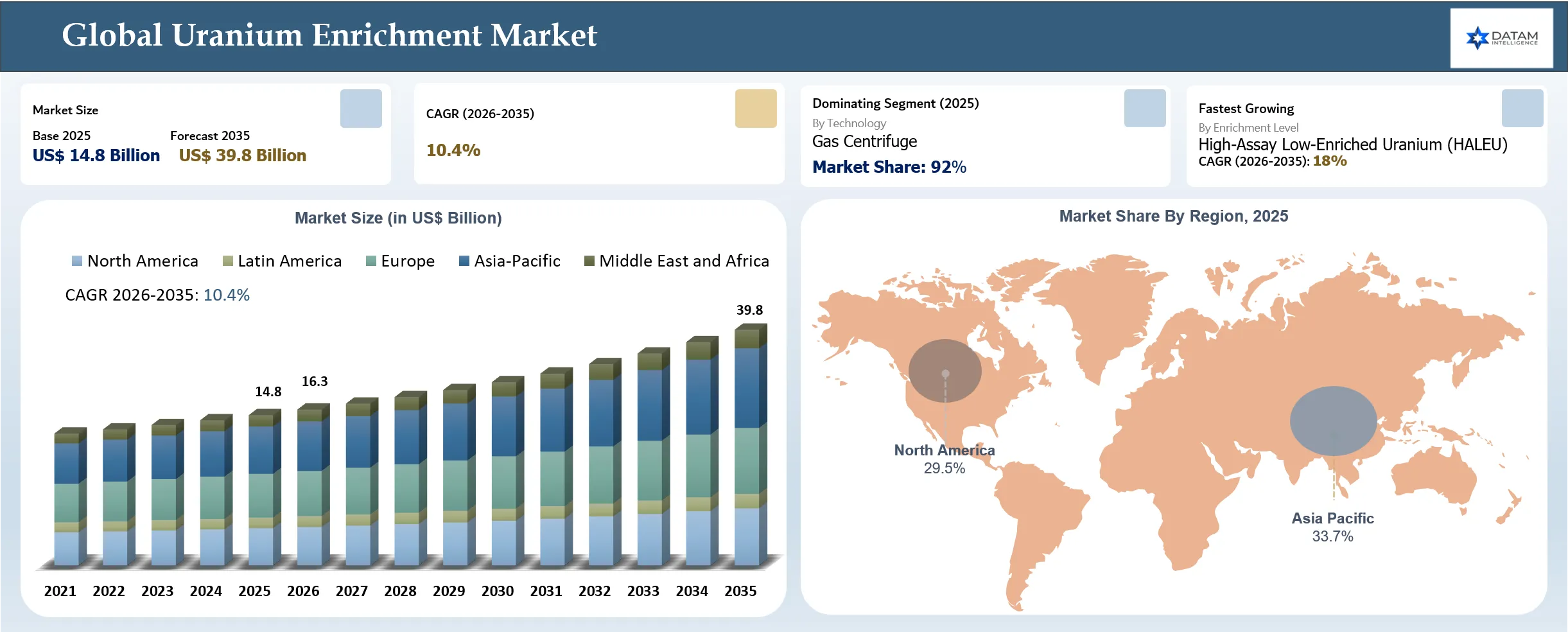

Uranium Enrichment Market Size

The global uranium enrichment market reached USD 14.8 billion in 2025 and is expected to reach USD 39.8 billion by 2035, growing with a CAGR of 10.4% during the forecast period 2026-2035, due to the renewed interest globally in nuclear energy as an efficient source of energy. Uranium enrichment is a crucial process in the fuel cycle that helps in developing nuclear fuel with higher amounts of uranium-235. With increased investments in energy security, life extension of reactors, and new builds in the Asia Pacific, North America, and Europe, there is an increase in demand for enriched uranium. The emergence of Small Modular Reactors (SMRs) and increased demands for High-Assay Low-Enriched Uranium (HALEU) are some of the factors that are helping the market grow at an accelerated rate. Companies are building up their capacities to ensure that future demand is met without depending on a few suppliers. Nevertheless, strict regulations and geopolitics of nuclear materials, among other factors, remain key determinants in the market.

Uranium Enrichment Market Strategic Takeaways

- The Gas Centrifuge technology held dominance in the market in 2025, as it constituted about 94.9% of the world's enrichment capacity, owing to its higher energy efficiency and reduced operating costs than other enrichment techniques.

- The High-Assay Low-Enriched Uranium (HALEU) segment is the fastest growing one and is expected to grow at a CAGR of 18% between 2026 and 2035 due to the rising use of Small Modular Reactors (SMRs).

- The Asia-Pacific region emerged as the leader in the regional landscape, capturing approximately 33% market revenue globally in 2025, owing to robust reactor constructions and investments in the fuel cycle.

- The government-owned enrichment businesses accounted for the major market share of around 65%, comprising of state-owned firms like Rosatom and CNNC.

Uranium Enrichment Market Industry Trends and Strategic Insight

- Uranium enrichment industry is rapidly pivoting from the use of traditional LEU and embracing HALEU, making HALEU the critical bottleneck that will power the next generation of nuclear reactors and SMRs.

- The international nuclear renaissance, driven by nuclear construction in Asia-Pacific, fleet extension in the West, and stringent carbon reduction goals, is translating political momentum into long-term and continuous demand for enrichment capacity into the decades ahead.

- The voracious demand for electricity in AI data centers and energy-intensive industries has made nuclear power the ultimate baseload option for the carbon-constrained era, thus putting an indirect pressure on the supply-demand balance of enriched uranium.

- Enrichment capability is becoming crucial infrastructure for energy, backed by governmental financing, reserve stockpiling, and national security programs rather than commercial considerations alone.

- Early investors in modernizing centrifuge technologies and HALEU infrastructure stand to gain an outsized market share increase as next-generation reactors go into commercial operation within the coming decade.

Uranium Enrichment Market Scope

| Metrics | Details | |

| 2025 Market Size | USD 14.8 Billion | |

| 2035 Projected Market Size | USD 39.8 Billion | |

| CAGR (2026-2035) | 10.4% | |

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | North America | |

| By Technology | Gas Centrifuge, Gas Diffusion, Laser Isotope Separation, Other | |

| By Enrichment Level | Low-Enriched Uranium (LEU), High-Assay Low-Enriched Uranium (HALEU), Highly Enriched Uranium (HEU), Depleted Uranium (DU) | |

| By Ownership Type | Government-Owned Enrichment Enterprises, Private Enrichment Companies, Public-Private Partnerships | |

| By Application | Nuclear Power Generation, Research Reactors, Medical Isotope Production, Defence & Naval Propulsion, Other | |

| By End User | Nuclear Utilities, Government & Defence Organizations, Research Institutes, Medical Isotope Producers, Advanced Reactor Developers, Industrial Users, Other | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

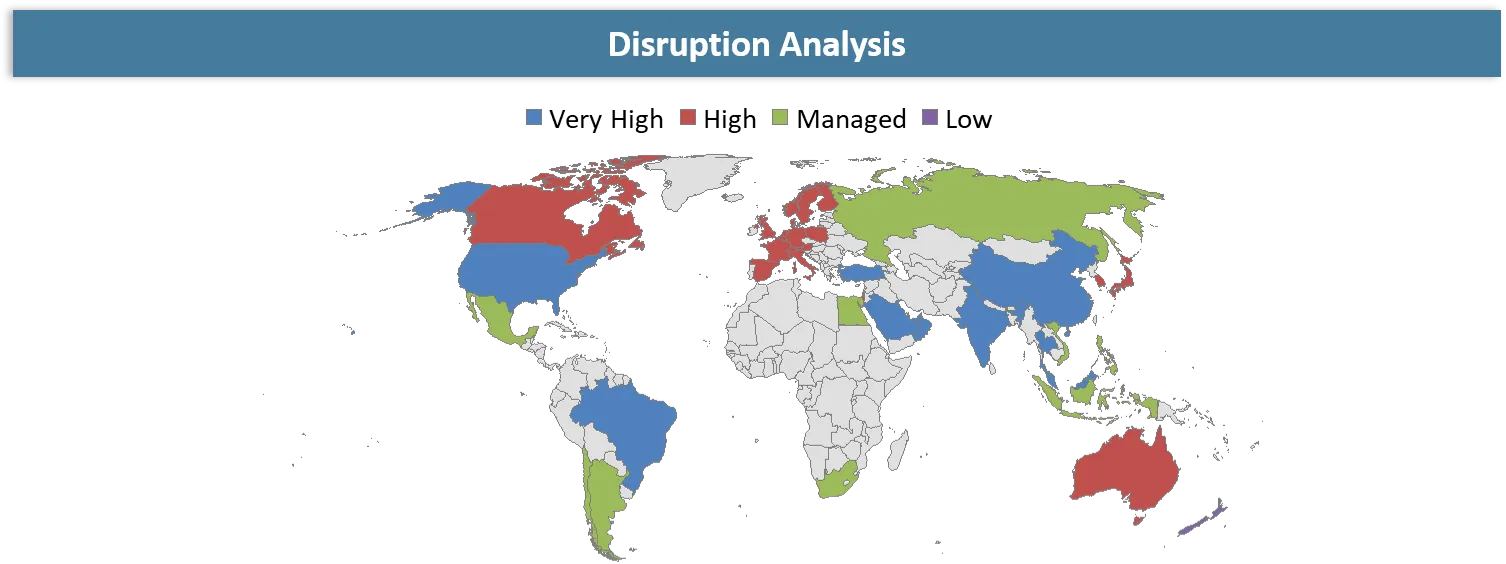

Uranium Enrichment Market Disruption Analysis

Geopolitical Realignment of Nuclear Fuel Supply Chains Disrupting the Uranium Enrichment Industry

Disruption in the uranium enrichment industry is mainly caused by the geopolitical reorganization of the nuclear fuel supply chain after the Western countries’ attempt to minimize their reliance on Russian enrichment facilities. The state-owned nuclear company in Russia provides about 45% of the world’s uranium enrichment capability and nearly 35% of the world’s uranium conversion capacity. Thus, there exists a significant amount of concentration in the market and sensitivity to the geopolitical environment. As a result of trade restrictions and sanctions, utilities in North America and Europe had to reconsider their fuel purchasing strategy.

Such disruptions have brought about significant supply-side pressures, especially in the market of enriched uranium and HALEU. There has been an increased focus by governments in the United States, Canada, France, the United Kingdom, and Japan on investments to bolster their domestic enrichment capacity and strategic fuel stocks. For instance, in 2024, the United States government spent $2.7 billion in efforts to increase domestic enrichment and HALEU production capacity, while leading enrichment firms have rolled out capacity expansion plans to counter anticipated shortfalls. This has forced utilities to engage in long-term enrichment agreements instead of short-term procurement arrangements.

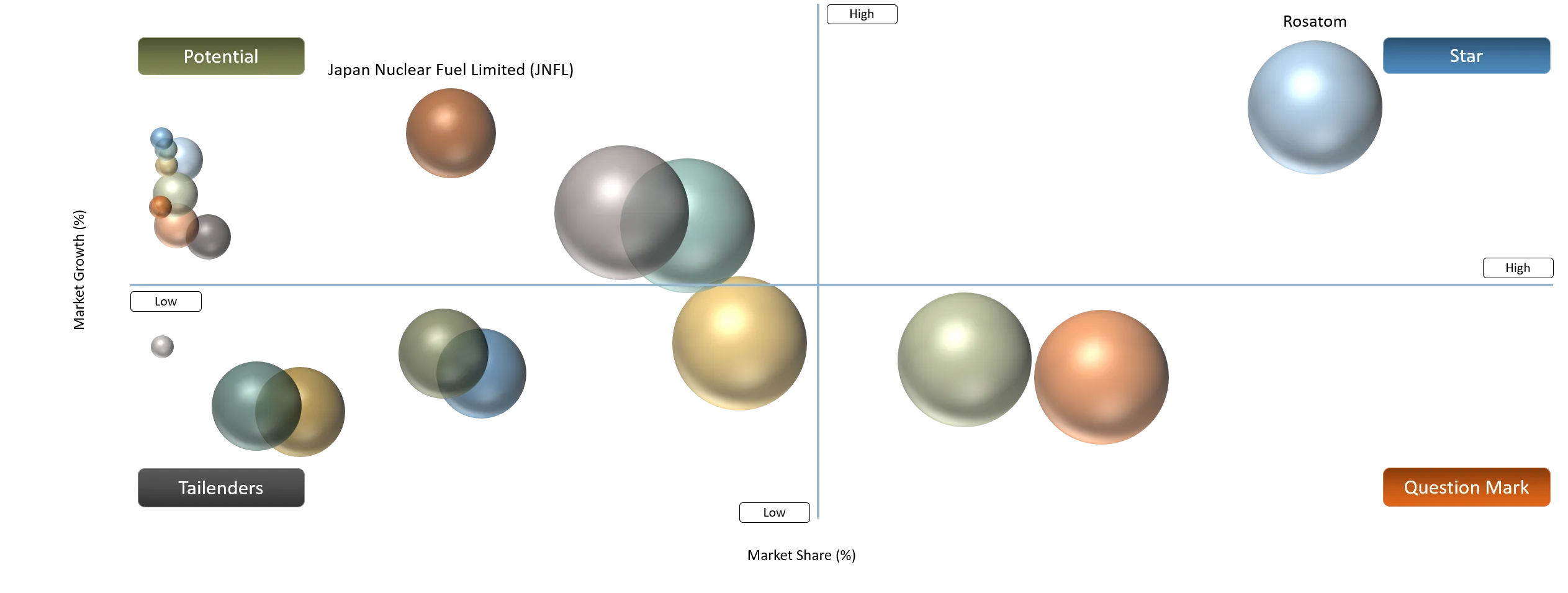

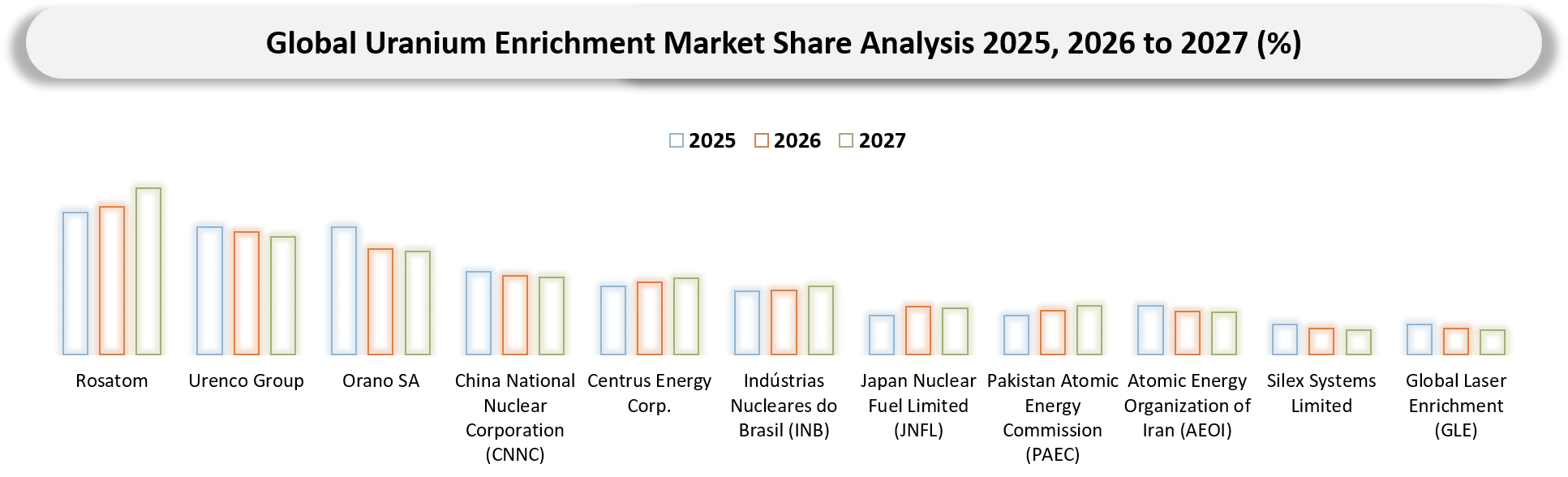

Uranium Enrichment Market BCG Matrix: Company Evaluation

Stars companies include Rosatom, Urenco Group, and Orano SA have been selected is due to the fact that together, these firms dominate in terms of controlling the majority of the commercial uranium enrichment capacity around the globe. On its own, Rosatom dominates around 44.9% of global uranium enrichment capacity between 2025-2026, while on the other hand, Urenco and Orano combine to account for another 39.8% of commercial enrichment capacity within the West. It is important to mention here that these companies are currently investing in their centrifuge facilities and securing long-term utility contracts for future HALEU demand. Question Marks are China National Nuclear Corporation (CNNC), Centrus Energy Corp., and Global Laser Enrichment (GLE). CNNC is rapidly increasing domestic capacity of enrichment to fuel the Chinese reactor building program and is expected to constitute 15% of world’s total capacity for enrichment. Centrus Energy owns only a small portion of commercial enrichment capacity (less than 2%) but occupies a strategic place in the rising HALEU market thanks to the funding from the U.S. government.

Potential Players consist of Japan Nuclear Fuel Limited (JNFL), Indústrias Nucleares do Brasil (INB), and Silex Systems Limited. JNFL runs the enrichment facilities of Japan and is positively impacted by the slow restart of nuclear reactors in Japan; however, JNFL's market reach is very small at below 2%. Examples for tailenders are Pakistan Atomic Energy Commission (PAEC) and Atomic Energy Organization of Iran (AEOI). These bodies have enrichment plants that work to fulfill strategic purposes and domestic energy needs but do not take part in the international uranium enrichment business.

Uranium Enrichment Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

A proliferation in global numbers of nuclear reactors and increased reactor operational lives has contributed significantly to the rising need for enriched uranium for power generation. | 35% | Very High | Commercial Nuclear Power Generation, Reactor Life Extension Programs

| Creates long-term recurring demand for LEU fuel, drives enrichment capacity expansion, and secures multi-decade fuel supply contracts. |

Rising geopolitical risks and the overdependence on a small group of enrichment service providers is driving government and utility organizations to focus on energy security. | 25% | High | Strategic Fuel Reserves, Domestic Fuel Supply Chains, Utility Procurement | Accelerates investments in domestic enrichment facilities, fuel diversification strategies, and government-backed enrichment projects. |

Rising deployment of Small Modular Reactors (SMRs) and advanced reactors is creating new demand for specialized enriched uranium products. | 22% | Medium to High | HALEU Production, SMRs, Generation IV Reactors | Establishes a new premium fuel market, encourages HALEU infrastructure development, and creates high-margin growth opportunities for enrichment providers. |

Global efforts to reach decarbonization goals and zero net commitments are elevating the strategic importance of nuclear energy. | 20% | High | Clean Baseload Electricity Generation, Energy Transition Projects | Strengthens government support for nuclear power, encourages reactor construction, and reinforces long-term uranium enrichment demand. |

The rapid expansion of AI data centers, electric vehicle manufacturing, and industrial electrification is driving global demand for nuclear energy | 15% | Medium

| AI Data Centers, Industrial Electrification, Grid Reliability Applications | Increases electricity demand, improves the investment case for nuclear generation, and indirectly supports future enrichment capacity growth. |

Rising deployment of Small Modular Reactors (SMRs) and advanced reactors is creating new demand for specialized enriched uranium products

The rise in deployment of small modular reactors (SMRs) and advanced nuclear reactors is fast becoming one of the critical growth factors for the enrichment of uranium market, especially through an increase in the need for high-assay low-enriched uranium (HALEU). This is due to the fact that, while conventional reactors make use of uranium that is not enriched beyond 5%, many advanced reactors need HALEU which ranges from 5% to 19.75% according to World Nuclear Association. As of 2025, there are more than 80 advanced reactor designs and SMR programs that are under development across the globe, according to the International Atomic Energy Agency (IAEA). There have been many developments towards commercializing some of these reactors in the US, Canada, UK, China, and other nuclear countries.

Based on the findings of the International Atomic Energy Agency (IAEA), it is predicted that the growth of the nuclear power generating capacity will be sustained up until 2050, with SMRs contributing significantly in the future. For instance, in 2026, Multidisciplinary Digital Publishing Institute (MDPI), which is an open-access scientific journal from, reported in its article that due to the widespread use of Small Modular Reactors and advanced reactors, there has been an increase in the demand for specific nuclear fuels like HALEU. Most advanced reactors need to have uranium with a concentration between 10% and 20% U-235 as compared to regular reactors that have 3%-5% U-235 concentration.

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

Excessive concentration of global uranium enrichment capacity on the part of relatively few companies leads to considerable exposure to geopolitical friction and possible shortages in supply. | 5% | Fuel Supply Security & Enrichment Capacity Availability | Commercial Nuclear Power Generation, Utility Fuel Procurement | Increases supply-chain risk, creates procurement uncertainty, drives enrichment price volatility, and accelerates investments in domestic enrichment capabilities. |

Inadequate development of infrastructure and facilities for the production of HALEU on an industrial scale results in important gaps in supply. | 3.5% | HALEU Production Infrastructure | SMRs, Generation IV Reactors, Advanced Nuclear Systems | Delays commercialization of advanced reactors, constrains HALEU availability, and slows adoption of next-generation nuclear technologies. |

Advanced technology methods for enrichment, such as laser enrichment, have numerous technological, commercial, and regulatory obstacles to overcome before implementation. | 2.5% | Technology Commercialization & Innovation | Advanced Enrichment Facilities, Future Fuel-Cycle Projects | Limits productivity improvements, delays cost reductions, and slows diversification beyond conventional centrifuge technology. |

Restrictions on the export of technology, sanctions, and nuclear technology transfers are hampering international cooperation and delaying important enrichment projects around the world. | 3% | International Collaboration & Project Development | Cross-Border Enrichment Projects, Nuclear Fuel-Cycle Partnerships | Restricts technology deployment, delays capacity expansion projects, and increases regional fragmentation of enrichment supply chains. |

Excessive concentration of global uranium enrichment capacity on the part of relatively few companies leads to considerable exposure to geopolitical friction and possible shortages in supply

The primary constraint that is seen to impact the uranium enrichment market includes the over-concentration of enrichment capacity in the hands of a few suppliers around the world. This can be attributed to the very concentrated nature of the industry in which Russia accounts for about 44% of all uranium enrichment capacity in the world in 2025, while only a handful of providers including Rosatom, Urenco, and Orano account for most of the commercial uranium enrichment in the world. This over-concentration in the hands of just a few makes the utilities and the governments susceptible to geopolitical constraints, trade bans, sanctions, and other such risks that make the fuel procurement process difficult. The supply challenge is further intensified by the lengthy timelines and substantial investment required to develop new enrichment infrastructure.

In 2025–2026, several Western governments announced initiatives to expand domestic enrichment capabilities and reduce dependence on Russian fuel-cycle services; however, new centrifuge facilities and fuel-cycle projects typically require multiple years before reaching commercial operation. For example, in 2025, according to the Charles River Associates (CRA), a U.S. based consultancy firm, in the year 2025, the services related to uranium conversion and uranium enrichment are still very concentrated within the few hands of suppliers.

Uranium Enrichment Market Segment Analysis

The global Uranium Enrichment market is segmented based on technology, enrichment level, ownership type, application, end user, and region.

Gas Centrifuge Technology Maintaining Dominance Through Superior Efficiency and Commercial-Scale Deployment

Gas Centrifuge segment still retains its dominant position in the market of uranium enrichment, making up 94.9% of all global enrichment capacities in 2025-2026 years. This dominance is explained by much lower energy use, greater efficiency and better scalability in comparison with old gaseous diffusion process. The modern enrichment plants owned by leading companies such as Rosatom, Urenco, Orano, and CNNC mostly utilize gas centrifuges in the process of Low-Enriched Uranium (LEU) and new HALEU fuel production. With rising nuclear fuel demand worldwide, gas centrifuges are used more frequently since it allows obtaining mass production at the competitive cost level. The World Nuclear Association states that gas centrifuge plants use 95% less energy than the outdated gaseous diffusion facilities; therefore, the gas centrifuges are currently the most economically efficient method of uranium enrichment.

With rapid global expansion of projects on reactor building, reactor extension, and HALEU production, the gas centrifuges continue to be the most profitable part of the business. For instance, in 2026, Industrial Info Resources, which is a U.S.-based company, stated that URENCO USA declared an expansion of its National Enrichment Facility located in New Mexico with the installation of 2.1 million SWU of uranium enrichment capacity in 24 gas centrifuges. It is evident that this particular project will expand the capacity of the facility from 4.3 million SWU to 7 million SWU in the coming decade.

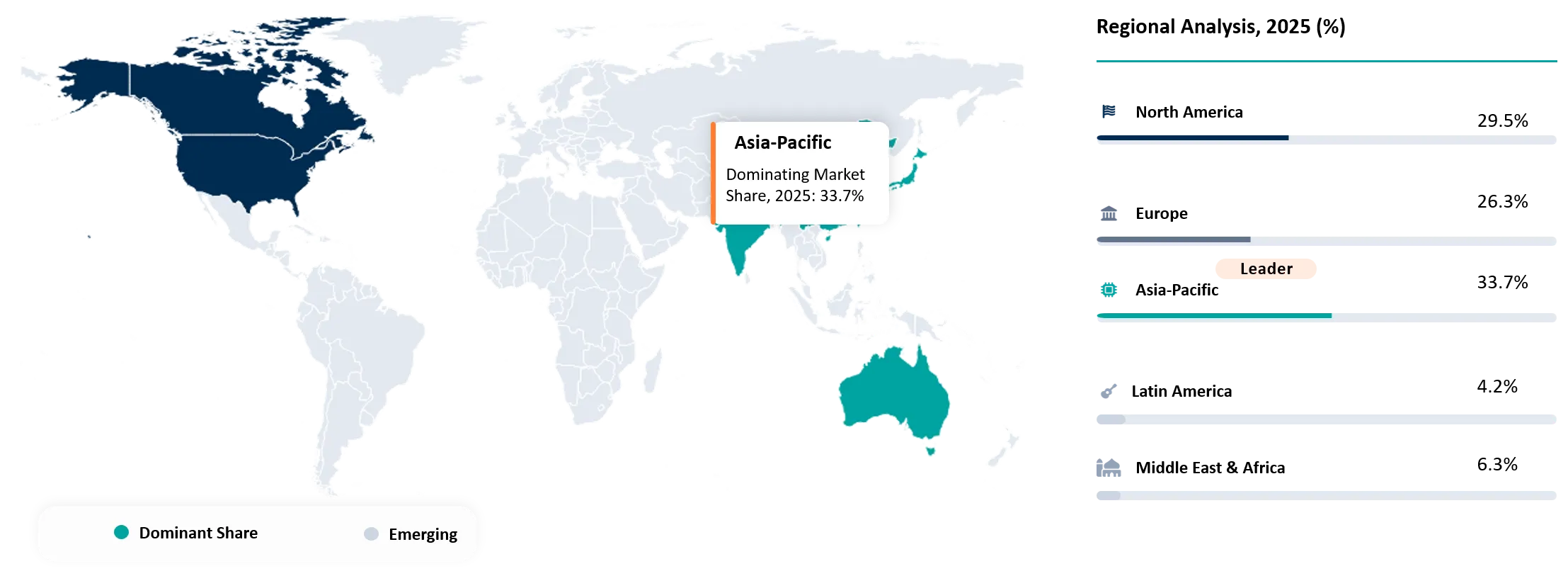

Uranium Enrichment Market Geographical Penetration

Expanding Nuclear Reactor Fleet and Fuel-Cycle Investments Strengthening Asia-Pacific Leadership

Asia Pacific region holds a dominating position in the uranium enrichment market and generates around 33% of total revenue in the global market from 2025-2026. This regional dominance can be attributed to the presence of the world’s biggest nuclear reactor construction pipeline, heavy investment in local nuclear fuel cycle facilities, as well as increased demand for energy security and clean electricity production. Such countries as China, India, Japan, and South Korea keep adding their nuclear power generating capacities in order to increase electricity production and minimize the use of fossil fuels. As reported by the International Atomic Energy Agency (IAEA), the Asian continent dominates the world's nuclear reactor construction industry, thereby making it the largest consumer of enriched uranium in the upcoming ten years.

The combination of reactor building, nuclear power policy implementation, and fuel security strategies will ensure Asia Pacific's domination as the largest generator of income in the uranium enrichment industry. For instance, in January 2026, the South Korean government launched an interagency team to conduct negotiations with the US government regarding civil uranium enrichment and spent fuel reprocessing agreements.

China Uranium Enrichment Market Trends

China is the leading player in the Asia-Pacific uranium enrichment industry, thanks to its nuclear power capacity development plans, the presence of an entire nuclear fuel cycle infrastructure and investments in its enrichment capabilities. It boasts the largest nuclear reactor pipeline in the world, with 30 reactors planned for 2025-2026, which makes up more than 40% of the total number of reactors being constructed worldwide. The existence of vertically integrated nuclear enterprises such as CNNC allows efficient management of various stages of the process, including conversion of uranium, enrichment, fuel production and reactor operation, which promotes China’s independence in nuclear fuel provision. Moreover, there is a trend of sustainable enrichment demand in the country as the capacity to generate electricity through nuclear means grows to enhance energy security and reduce carbon emissions. The enrichment of uranium in China made up 49.5% of the total uranium enrichment in the Asia-Pacific region in 2025-2026 because of the increasing demand for LEU.

For example, in September 2025, China National Nuclear Corporation (CNNC), a nuclear energy firm based out of China, embarked upon a cooperation program with the government of Uzbekistan for developing uranium resources, geological surveys in prospective regions, transfer of technology, and growth of peaceful nuclear energy ventures in the region.

India Uranium Enrichment Market Outlook

India is set to become the fastest growing nation in terms of Asia Pacific uranium enrichment market because of the country’s aggressive nuclear power expansion plans, increased investments in domestic fuel cycle facilities, and the increasing need for reliable electricity. The country is building more nuclear generation capacities through eight reactors that are being constructed in the year 2025 – 2026. This is one of the biggest nuclear power plants construction projects other than China. There are government-led efforts to expand the country’s nuclear energy capacity and build indigenous fueling capabilities. There are also various organizations such as NFC and DAE in India that support fuel cycle and reactor fuel facilities. According to the World Nuclear Association, the objective of India is to significantly augment its nuclear power generation capacity in the upcoming years, aided by domestic reactor development efforts and superior nuclear technology.

This has ensured India's emergence as the fastest-growing region for demand for uranium enrichment in the Asia Pacific region, with a projected market CAGR of 14% between 2026-2035. For example, in 2025, TVEL, which is an international organization that produces nuclear fuel in Russia, delivered nuclear fuel assemblies for Kudankulam unit 4 in India based on the terms of the long-term supply contract with NPCIL.

Uranium Enrichment Market Competitive Landscape

- The major participants in the market of uranium enrichment include three distinct groups: large commercial enrichment services providers; state-owned nuclear fuel cycle enterprises and new advanced technologies providers for enrichment. The leading firms in the market of commercial enrichment services include Rosatom, Urenco Group, Orano SA and China National Nuclear Corporation (CNNC). All these four companies own approximately 89.8% of the world’s enrichment capacity in 2025-2026. Thus, Rosatom has almost 44% share of global enrichment capacity, whereas Urenco and Orano are the largest suppliers of Western enrichment services. Government-owned organizations like JNFL, INB, PAEC, and AEOI are engaged in meeting the nuclear fuel demands of their countries. Moreover, these firms provide nuclear fuel for strategic needs of their states. At the same time, Centrus Energy Corp, GLE and Silex Systems Limited are concentrated on HALEU manufacturing and advanced laser enrichment technologies. This provides an additional technology-based competitive element in the market.

- Key players include Rosatom, Urenco Group, Orano SA, China National Nuclear Corporation (CNNC), Centrus Energy Corp., Indústrias Nucleares do Brasil (INB), Japan Nuclear Fuel Limited (JNFL), Pakistan Atomic Energy Commission (PAEC), Atomic Energy Organization of Iran (AEOI), Silex Systems Limited, and Global Laser Enrichment (GLE).

Key Developments

- January 2026: The U.S. Department of Energy (DOE) awarded USD2.7 billion to American Centrifuge Operating, General Matter, and Orano Federal Services in order to enhance uranium enrichment capabilities domestically.

- May 2025: A strategic alliance was formed between Urenco and Ubaryon Pty Ltd for rapid development and commercialization of new uranium enrichment technology.

- October 2025: Snow Lake Energy made a acquisition of Global Uranium and Enrichment Limited (GUE). As a result, the new entity has become a nuclear fuel cycle firm focused on the US market. The deal has increased the share of Snow Lake in uranium enrichment via GUE's holding in Ubaryon Pty Ltd.

- March 2026: Oklo Inc. and Centrus Energy Corp. decided to form a partnership in Ohio aimed at offering nuclear fuel services such as HALEU deconversion and fuel fabrication and expand infrastructure supporting advance reactors and uranium enrichment-related fuel services.

- November 2025: Rosatom announced that it intended to increase its enrichment capacity by about 30 percent by 2030 due to increasing demands on nuclear fuel worldwide. The plan is aimed at manufacturing of uranium for regular nuclear power plants, SMRs and innovative nuclear power stations.

- September 2025: Snow Lake Energy Ltd. has made a definitive agreement to acquire Global Uranium and Enrichment Limited (GUE). This merger has resulted in the creation of a nuclear fuel cycle company with its operations focused on the United States. The acquisition helps increase the participation of Snow Lake in uranium enrichment due to the strategic stake of GUE in Ubaryon Pty Ltd.

- December 2025: Centrus Energy launched its commercial operation of enriching Low-Enriched Uranium (LEU) at its American Centrifuge Plant facility located in Ohio. This venture represents a major step in increasing the uranium enrichment capability within the United States, ensuring uranium fuel security as well as addressing the increased demand for enriched uranium.

Key Procurement Priorities and Buyer Evaluation Criteria

- Businesses that are putting money into the Uranium Enrichment Market are more inclined to select their suppliers on the basis of their capability to provide secure and uninterrupted supply of enriched uranium for the long term, owing to huge capacity of enrichment and diverse production plants.

- Procurement decision-making is being increasingly driven by the increasing use of nuclear power generation facilities, extended reactor operations, SMRs, and next-generation reactors, all of which need a secure source of Low-Enriched Uranium (LEU) and novel High-Assay Low-Enriched Uranium (HALEU) fuels.

- Purchasers consider issues including enrichment capability availability, fuel supply reliability, exposure to geopolitics risks, pricing stability, contract term flexibility, compliance with regulations and non-proliferation of nuclear when choosing enrichment services providers for uranium.

- It is increasingly common for utilities, fuel fabricators, and government bodies to place emphasis on suppliers who possess an integrated fuel cycle background, have production facilities either domestically or through allied countries, have the capability to produce HALEU, understand the intricacies of advanced centrifuges, and have the ability to operate commercial, SMR, and research reactors.

Why Choose DataM?

- Technological Innovations: Examines developments in uranium enrichment techniques such as gas centrifuge techniques in their next generation, laser-based enrichment studies, digital process control, artificial intelligence in plant monitoring, predictive maintenance, and cascade optimization, thus improving separation efficiency, reducing energy consumption, enhancing operational efficiency, and producing more nuclear fuel.

- Product Performance & Market Positioning: Identifies the ways that the top enrichment companies create differentiation in terms of their enrichment capabilities, SWU efficiency, fuel performance, safety, compliance with regulations, and supply reliability.

- Real-World Evidence: Features the application of the uranium enrichment technology in commercial nuclear fuel plants, government-run nuclear projects, and global fuel chain networks, providing advantages like increased fuel security, improved performance of reactors, lower costs of operation, and assured fuel supply to current and future nuclear reactors.

- Market Updates & Industry Changes: Highlights include capacity growth in enrichment operations, funding towards new technologies in centrifugation, fuel procurement deals, changes in nuclear energy policies, government encouragement towards indigenous fuel production, and investments made regionally in nuclear fuel production facilities.

- Competitive Strategies: Examines how leading firms use capacity building, long-term fuel sourcing agreements, modernization of technology, forming alliances with nuclear power firms, vertical integration along the nuclear fuel chain, and diversifying enrichments as strategies for maintaining a competitive edge in meeting rising demands for nuclear energy worldwide.

- Pricing & Market Access: Describes the pricing mechanisms according to SWU costs, price of uranium feedstock, enrichment rates, contract time frame, and regulatory needs, while analyzing market access through utility commitments, government purchases, international fuel agreements, and nuclear fuel services companies.

- Market Entry & Expansion: Highlights growth opportunities resulting from increased investments in nuclear power generation, small modular reactors (SMRs), energy security programs, decarbonization programs, and rising need for reliable low-carbon power supply through capacity additions, technology upgradation, strategic alliances, and diversification of fuel sources in various regions around the world.

Target Audience

- Nuclear Power Utilities and Plant Operators

- Nuclear Fuel Fabrication Companies

- Government Nuclear Energy Agencies

- Small Modular Reactor (SMR) Developers

- Advanced Reactor Technology Companies

- Research Reactor Operators and Nuclear Research Institutions

- Nuclear Infrastructure Investors and Project Developers