UK Private Healthcare Market Size & Industry Outlook

The UK Private Healthcare Market size reached US$ 14.22 billion in 2025 and is expected to reach US$ 18.56 billion by 2033, growing at a CAGR of 3.4% during 2026–2033, according to DataM Intelligence’s report listing. The market includes private acute care hospitals, private patient care clinics, private specialist services, diagnostics and imaging centres, urgent care centres, dental treatment clinics, and other private healthcare services.

The market is being shaped by long NHS waiting times, rising self-pay demand, employer-sponsored private medical insurance, faster access to diagnostics, and growing use of private providers for elective surgeries such as orthopaedics, ophthalmology, cardiology, and gynaecology.

The shift toward minimally invasive procedures, same-day surgery, and high-end diagnostics is accelerating the growth of the UK private healthcare market. Private providers are often the first to introduce new imaging platforms, robotic surgery systems, and digital health solutions because they are not tied to NHS procurement cycles.

For instance, several private hospital groups such as Spire Healthcare and Circle Health Group have invested in robotic-assisted orthopaedic surgery and rapid-access MRI/CT scanning, enabling faster turnaround times and a premium patient experience. This technological edge attracts both self-pay patients and NHS contracts for complex or high-volume procedures, making advanced technology and outpatient/ambulatory models a major driver of market expansion beyond traditional inpatient care.

Key Takeaways

- Steady market growth: The UK private healthcare market is projected to grow from US$ 14.22 billion in 2025 to US$ 18.56 billion by 2033 at 3.4% CAGR.

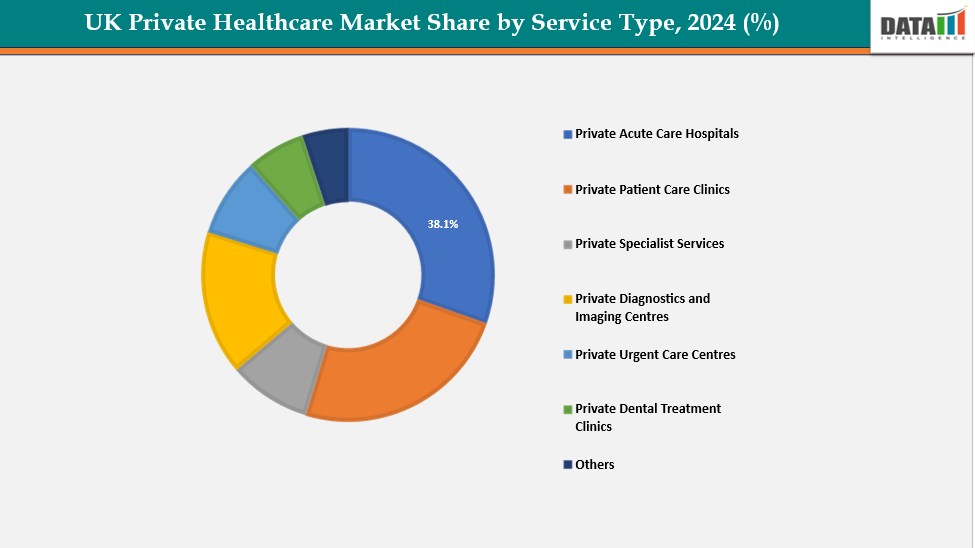

- Based on service type, the private acute care hospitals segment led the market with the largest revenue share of 38.1% in 2025.

- NHS waiting lists are a major demand trigger: Patients are increasingly choosing private treatment for faster access to diagnostics, consultations, and elective procedures.

- Private acute care hospitals are gaining traction: Demand is strong for orthopaedics, cardiology, ophthalmology, and other specialist procedures where NHS delays remain a concern.

- Insurance-funded care is expanding: Private medical insurance claims increased strongly between 2022 and 2025, with younger age groups also showing faster adoption of private healthcare services.

- Diagnostics and imaging are key growth areas: Faster access to MRI, CT, endoscopy, pathology, and specialist consultation is becoming a major reason patients choose private providers.

- The market is becoming more consumer-led: Patients expect transparent pricing, shorter waiting times, digital booking, clear treatment pathways, and a better service experience.

UK Private Healthcare Market Scope

| Metrics | Details | |

| CAGR | 3.4% | |

| Market Size Available for Years | 2023-2033 | |

| Estimation Forecast Period | 2026-2033 | |

| Revenue Units | Value (US$ Bn) | |

| Segments Covered | Service Type | Private Acute Care Hospitals, Private Patient Care Clinics, Private Specialist Services, Private Diagnostics and Imaging Centres, Private Urgent Care Centres, Private Dental Treatment Clinics, Others |

| Application | General Surgery, Trauma and Orthopedics, Oncology Cardiology, Urology, Dental, Others | |

| End User | International Tourists, NHS Referrals & PMI, Self-pay Individuals | |

Market Dynamics

Drivers: Rising self-pay and private medical insurance uptake is significantly driving the UK private healthcare market growth

Over the past five years, the UK private healthcare market has seen a significant increase in self-pay procedures and employer-funded private medical insurance (PMI), boosting revenue for hospital operators. Spire Healthcare reported that self-pay revenue reached one-third of its total UK income in 2025, while large employers expanded PMI benefits to support staff retention and reduce sickness absence. This has fueled growth at insurers like Bupa, AXA Health, and Vitality Health, and pushed more insured patients into private hospital networks. This has led to a larger flow of privately funded patients and insured referrals, underpinning capital investment in new facilities.

For instance, UK's Private Healthcare Information Network (PHIN) reported 238,000 more private hospital admissions in January to March 2024 compared to any previous quarter. The majority of these admissions were funded using private medical insurance (PMI), with the largest increases in the 20-29 and 30-39 age groups by 13%.

Restraints: High treatment costs & affordability issues are hampering the growth of the UK private healthcare market

Private healthcare costs remain a significant barrier to access, especially for self-pay patients and small-to-medium enterprises offering PMI. Complex procedures like joint replacements and advanced cancer therapies can cost thousands of pounds, limiting access to higher-income segments. Even with insurance coverage, high excesses or co-payments reduce affordability, constraining volume growth. This challenge affects private hospitals' ability to expand beyond premium and insured populations, driving competition around price transparency, bundled-care packages, and elective day-case procedures to attract cost-conscious patients.

For more details on this report – Request for Sample

3 Fast Growing Use Cases for Private Healthcare in the UK

1. Private Diagnostics and Imaging

Private diagnostics and imaging is one of the fastest growing use cases because patients want faster access to MRI, CT, ultrasound and specialist test results. Diagnostics often acts as the entry point into private treatment because it shortens the route from symptom concern to consultant decision. Growth is strongest among self pay patients and insured users seeking faster confirmation before treatment. Private providers are expanding imaging capacity because scans support orthopaedics, oncology, cardiology and general surgery referrals. The market is moving toward rapid access diagnostic centres with digital booking and fast reporting. Providers with advanced imaging and strong consultant links will capture higher conversion.

2. Elective Surgery and Day Case Procedures

Elective surgery and day case procedures are growing quickly because NHS waiting pressure has increased patient willingness to pay for faster treatment. General surgery and orthopaedics are leading areas because procedures are planned and outcomes are easy for patients to understand. Day case models are gaining share because they reduce inpatient stay and improve operating efficiency. Private hospitals are investing in surgical theatres and minimally invasive techniques to increase throughput. Growth will be strongest in procedures linked with pain relief, mobility improvement and faster return to work. Providers with bundled pricing and consultant availability will gain stronger self pay conversion.

3. Employer Funded Private Medical Insurance Pathways

Employer funded private medical insurance pathways are expanding as companies use healthcare benefits to reduce absence and improve employee retention. PMI is becoming more important as workers seek faster access to consultations, diagnostics and treatment. Private hospitals benefit from insured patient flow because referrals are more predictable than self pay demand. Growth is strongest among large employers and professional service sectors where workforce productivity is a major concern. Insurers are directing patients into preferred provider networks to control cost and improve treatment speed. The market is moving toward integrated pathways that combine digital triage, diagnostics and specialist referral. Providers with insurer relationships will capture stronger demand.

Segmentation Analysis

The UK private healthcare market is segmented based on service type, application, and end user.

Service Type: The private acute care hospitals from service type segment to dominate the UK private healthcare market with a 38.1% share in 2024

The private acute care hospital segment is gaining popularity due to increased demand for elective surgeries, specialist care, and NHS outsourcing. Long waiting times for orthopaedic, cardiology, and ophthalmology interventions have led to patients choosing private hospitals like Spire Healthcare, Ramsay Health Care UK, and Bupa Cromwell. Growth in employer-sponsored private medical insurance and self-pay packages has provided a steady revenue stream for hospitals, enabling investment in advanced surgical theatres, robotic-assisted surgery, and diagnostic imaging.

Moreover, private acute care hospitals are at the forefront of adopting cutting-edge medical technologies. Investments in robotic-assisted surgeries, advanced imaging systems, and state-of-the-art surgical theatres have enhanced the quality and efficiency of care. For instance, Spire Healthcare has reported a 12.7% increase in revenue, partly attributed to its investment in technology and expansion of services, including orthopaedic surgeries and cancer treatments.

Application: The general surgery segment is estimated to have a 40.1% of the UK private healthcare market share in 2025

The UK private healthcare market is experiencing growth in the general surgery segment due to rising demand for elective procedures, technological advancements, and the flexibility of private care providers. Patients are choosing private hospitals like Spire Healthcare, Ramsay Health Care UK, and Bupa Cromwell for procedures like hernia repairs and minor abdominal surgeries to avoid long NHS waiting times. The adoption of minimally invasive and laparoscopic techniques makes private general surgery more attractive to self-pay and insured patients. NHS outsourcing contracts and corporate health schemes support this growth. Rising awareness of preventive care and patient-centric services also drives demand in this segment.

For instance, in August 2025, Bupa has completed the acquisition of New Victoria Hospital, an independent private facility located in Kingston upon Thames. This marks Bupa’s first hospital acquisition in the UK since 2008 and allows for more integrated patient pathways, linking primary care services directly with secondary care. The hospital features 33 beds and offers specialised care in orthopaedics, gynaecology, general surgery, and gastroenterology. Its state-of-the-art infrastructure includes a 128-slice CT scanner, a fluoroscopy suite, and a 1.5‑tonne MRI system.

Competitive Landscape

Top companies in the UK private healthcare market include Bupa Cromwell Hospital, Althea Group, The London Clinic, GenesisCare, Great Ormond Street Hospital (GOSH), Ramsay Health Care UK, Aspen Healthcare (Tenet Healthcare), Spire Healthcare Group plc, the Bournemouth Private Clinic Limited, Circle Health Group (PureHealth) and among others.

Bupa Cromwell Hospital:- Bupa Cromwell Hospital is a leading UK private acute care facility, offering specialist services in cardiology, orthopaedics, oncology, and paediatrics. It bridges the gap between NHS capacity and patient demand, providing faster access to complex procedures for both self-pay and insured patients. With advanced diagnostic and treatment infrastructure like MRI, CT, and state-of-the-art surgical theatres, it supports high-quality, consultant-led care. Bupa Cromwell contributes significantly to the growth and development of the UK's private healthcare sector.

Major Recent UK Private Healthcare News

- In April 2026, Bupa and Spire Healthcare signed a four year strategic partnership giving Bupa UK insurance customers access to Spire’s 38 hospitals and more than 60 clinics. This strengthens insurer provider alignment and improves Spire’s access to insured patient flow.

- In May 2026, Toscafund proposed a £1 billion buyout of Spire Healthcare, following earlier private equity interest in the company. This shows that UK private hospital assets are gaining investor attention due to capacity value and private patient revenue potential.

- In June 2026, PHIN’s private market update showed that insured and self pay admissions remain structurally important with different procedure trends by payer type. This confirms that UK private healthcare demand must be evaluated by payer mix and procedure economics.

Where is the UK Private Healthcare Market Headed?

- Private healthcare activity continues to rise through insured and self pay channels. PHIN’s 2026 market updates show private medical insurance funded admissions and self pay activity rising in recent reporting periods. Buyers need the report now because demand is shifting across payer groups and procedure types.

- Bupa and Spire signed a four year strategic partnership. The agreement gives Bupa UK insurance customers access to Spire’s 38 hospitals and over 60 clinics, strengthening insurer provider alignment. Buyers need updated competitive analysis because payer relationships are becoming a major capacity and referral moat.

- Spire takeover activity signals rising investor interest in UK private care. Toscafund proposed a £1 billion buyout of Spire Healthcare in 2026, following earlier private equity interest. Buyers need the report now because investor appetite, NHS backlog exposure and private patient growth are changing valuation dynamics.

NHS Waiting List to Private Healthcare Conversion Analysis

The UK private healthcare market is being shaped by the conversion of NHS waiting list pressure into private demand. Long waiting times for orthopaedics, general surgery, cardiology and diagnostics are pushing patients toward private hospitals and clinics. Self pay demand is strongest where procedures are predictable, scheduled and linked with quality of life improvement. Private medical insurance is also gaining traction as employers use healthcare access as a workforce retention tool. Acute care hospitals benefit most because they can absorb elective surgery demand and specialist referrals. Diagnostics and imaging centres gain from patients seeking faster MRI, CT and ultrasound access before specialist consultation. The market is moving toward quicker pathways, bundled pricing and same day treatment models. Providers with theatre capacity, consultant networks and strong diagnostics will capture the largest share of demand migrating from delayed public care.

UK Private Healthcare Service Line Profitability Analysis

Service line profitability in UK private healthcare is concentrated in acute care hospitals, diagnostics, orthopaedics and general surgery. Acute care hospitals lead because they combine consultant led treatment, surgical infrastructure and insured patient flow. General surgery has strong volume because procedures such as hernia repair and abdominal interventions are common among self pay and insured patients. Orthopaedics remains attractive because joint pain and mobility issues create urgent patient willingness to pay. Diagnostics has a high growth profile because faster scans shorten the patient journey and support specialist referrals. Oncology and cardiology command premium positioning but require specialist infrastructure and high clinical governance. Dental and urgent care serve wider consumer demand but face stronger price sensitivity. The most profitable providers will balance high volume elective procedures with premium specialist services. Revenue resilience will depend on payer mix, theatre utilization and diagnostic throughput.

UK Private Healthcare Payer Mix Analysis

The UK private healthcare market is increasingly defined by payer mix. Private medical insurance and NHS referrals create recurring patient flow, while self pay demand expands when public wait times rise. Affordability remains the key constraint because complex procedures and specialist care carry high out of pocket costs. Self pay growth is strongest in procedures with clear pricing and shorter recovery cycles. Private medical insurance demand is supported by employer benefits as companies address workforce absence and staff retention. NHS funded referrals remain important because they fill capacity and support provider revenue stability. Price transparency is becoming a competitive factor as patients compare hospitals, consultant fees and treatment packages. Providers are responding with bundled procedure pricing and financing options. The strongest operators will manage a balanced payer base across insured patients and self pay individuals while maintaining margin discipline.

UK Technology Led Patient Experience Analysis

Technology is becoming a major differentiator in UK private healthcare because patients are paying for speed, certainty and better experience. Private providers are investing in robotic assisted surgery, advanced MRI, CT platforms and digital patient pathways. These technologies support faster diagnosis, shorter recovery and higher consultant confidence. Robotic orthopaedic surgery strengthens premium positioning because it aligns with precision, mobility outcomes and patient willingness to pay. Advanced imaging reduces diagnostic delays and increases referral conversion. Digital booking, virtual consultation and patient portals improve convenience for insured and self pay users. The strongest providers are building technology around the full patient journey from consultation to imaging and surgery. Market leadership will shift toward hospitals that combine consultant access and high end infrastructure. Technology adoption will remain a key driver of private patient conversion.

UK Private Healthcare Access Gap Analysis

UK private healthcare demand is strongest where NHS pressure, household income and provider capacity overlap. London remains the premium private healthcare hub because of specialist hospitals, international patient demand and strong consultant concentration. South East England benefits from higher disposable income and access to established private hospitals. Large cities such as Manchester, Birmingham and Bristol are gaining importance as regional demand increases for diagnostics and elective procedures. Capacity gaps remain visible in areas where NHS waiting pressure is high but private infrastructure is limited. Regional expansion is likely to focus on diagnostic centres, outpatient clinics and day surgery facilities rather than large full service hospitals. Private providers will prioritize locations with insured populations and employer health coverage. The strongest regional growth will come from markets that can support fast access medicine and repeat elective demand.

UK Private Healthcare Provider Positioning Analysis

Competitive advantage in UK private healthcare is defined by consultant access, facility quality, payer relationships and service breadth. Bupa, Spire Healthcare, Ramsay Health Care UK, Circle Health Group and The London Clinic hold strong positions because they combine brand recognition and clinical infrastructure. Acute care providers gain advantage when they offer theatres, diagnostics and specialist care under one network. Insurer linked pathways create an additional moat because insured patients are directed through approved provider networks. Consultant loyalty also matters because leading specialists attract both self pay and insured patients. Providers with advanced imaging and robotic surgery strengthen their premium positioning. Reputation, patient experience and clinical outcomes will increasingly influence conversion. The market will favor operators that combine speed of access and high quality care with transparent pricing. Smaller clinics will need specialization or local convenience to compete effectively.

UK Private Healthcare Investor White Space Analysis

Investor white space in UK private healthcare is strongest in diagnostics, day surgery, specialist clinics and digital patient access platforms. Diagnostics offers scalable growth because private scans are often the first entry point into private care. Day surgery is attractive because it supports faster patient turnover and lower inpatient cost exposure. Specialist clinics in orthopaedics, cardiology and oncology offer premium positioning where consultant reputation drives demand. Digital access platforms create value by improving booking, triage and patient journey management. Strategic deal activity will focus on assets that expand regional coverage and strengthen referral pathways. Private hospital operators will pursue acquisitions that add diagnostics or outpatient capability. Insurers will favor integrated care assets that control patient flow and cost. The most attractive targets will combine clinical credibility, capacity availability and payer access. Market consolidation will continue as scale becomes more important.

What You Get Compared with Competitors

| Dimension | Traditional Market Research | DataM Intelligence |

| Product | Static PDF reports covering broad UK healthcare trends with limited depth on private hospitals, payer mix and patient demand conversion | Custom dashboards for UK private healthcare with interactive views across service type, application, end user, provider group and payer segment |

| Data Age | 6 to 12 months old with historical snapshots of private healthcare activity and limited updates on admissions, acquisitions or technology investment | Living data with continuous updates on self pay demand, PMI activity, NHS referrals, provider expansion and competitive moves |

| Engagement | One time transaction with limited follow up after delivery of market size, segmentation and company data | Continuous partnership with analyst support to track provider strategy, patient flow, investment activity and procurement triggers |

| Output | Raw market information with limited guidance on UK private healthcare strategy and commercialization decisions | Actionable insights with clear recommendations for service expansion, pricing strategy, provider benchmarking and investment evaluation |

| Customization | One size fits all syndicated templates with limited tailoring for service type, payer mix, regional access or procedure category | Tailored solutions through DMI Insights and DMI Connect built around each client context with 81% of our clients choosing a customized solution |

| Market Depth | General coverage of private healthcare with limited detail on acute care hospitals, diagnostics, elective surgery and insured patient pathways | Focused intelligence on UK private healthcare across demand conversion, profitability, affordability pressure and investor white space |

| Decision Support | Limited ability to compare providers, service lines, payer groups and regional capacity in one view | Dashboard based comparison of provider positioning, regional opportunity, service line attractiveness and investment readiness |

| Investor View | Limited insight into acquisition targets, payer access, technology differentiation and regional expansion potential | Investor focused tracking of provider moats, diagnostic growth, day surgery expansion and scalable care pathway opportunities |

| Retention | Low chance of re engagement once the report is delivered | Over 35% of our clients are repeat customers due to ongoing updates, customization and long term decision support |

The UK private healthcare market report delivers a detailed analysis with 62 key tables, more than 57 visually impactful figures, and 159 pages of expert insights, providing a complete view of the market landscape.