Turning Tools Market Size & Forecast

The global turning tools market Size was US$ 0.58 billion in 2025 and forecasted to reach US$ 1.02 billion by 2035, growing with a CAGR of 5.8% during the forecast period 2026-2035. The growing need for precise machining in various industries such as the automotive, aerospace, industrial machinery, medical equipment and energy industries is leading to an increased use of high-quality turning tools globally. Current manufacturing processes rely more on computer numerical control lathes, multi-axis machining centers and automated machining lines that require the use of high-speed carbides, ceramics, CBN and PCD turning tools that can provide superior performance in terms of precision, superior finish quality and long service life. Smart factories supported by industry 4.0 are also driving the need to incorporate monitoring systems into turning tools.

Governments globally are promoting their manufacturing sector and machining abilities through industrial modernization and investments in semiconductors, automobiles, and aerospace. The Green Deal Industrial Plan by the European Union and the “Make in India” policy by the Indian government are promoting localized manufacturing of industrial machines and automobile parts. It will lead to an increased demand for robust and fast-turning tools in factories. Recently, the Indian government has approved manufacturing subsidies exceeding US$ 26 billion for various PLI programs for sectors including automobiles, aerospace, electronics, and engineering products.

Turning Tools Industry Trends and Strategic Insights

- The increasing use of CNC machine machining systems in automotive and aerospace plants has spurred the need for intelligent cutting tools that can monitor their wear and offer predictive maintenance options; thus, the Asia-Pacific led the market in 2025, with the largest revenue share owing to its well-developed manufacturing sector and investments in industrial automation.

- The increased use of hard-to-machine materials like titanium alloys, Inconel, hard metals and carbon fiber reinforced polymers in the manufacture of electric vehicles and in aerospace operations is driving the need for coated carbide, ceramic and CBN turning tools used in high-speed machining operations.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 0.58 Billion | |

| 2035 Projected Market Size | US$ 1.02 Billion | |

| CAGR (2026-2035) | 5.8% | |

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Tool Grade | Solid Carbide, Cermet, Ceramics, Cubic Boron Nitride (CBN) and PCBN Tools, Diamond Tools | |

| ByMachine Type | CNC Turning Machines (Turning Center), Swiss Type Automatic Lathes (Sliding Head Lathes), Multi-Tasking Machines (Mill Turn Machines), Other | |

| By Workpiece Detail | P Steel, M Stainless Steel, K Cast Iron, N Non Ferrous Metals, S Super Alloys and Titanium, H Hardened Materials, Plastic, Optical Materials and Glass | |

| By End-User | Automotive and Electric Vehicles, Aerospace and Defense, General Machining, Job Shops, Die and Mold, Industrial Machinery, Construction and Agriculture Equipment, Energy and Power Generation, Oil and Gas, Mining, Rail, Marine and Shipbuilding, Electronics and Consumer, Appliances, Semiconductor Equipment and Precision Parts, Medical Devices, Dental, Bearing Manufacturing, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Strategic Indicators For Turning Tools

High Regulation Impact

Regulation has begun to fundamentally alter cutting tool demand, specifically in Germany, United States, China, and Japan. The EU CBAM system places indirect cost pressure on steel tooling supply chains through carbon emissions compliance costs. U.S. export regulations regarding advanced machining tools targeting Chinese importers remain stringent, affecting the flow of carbide insert tooling. Indian government programs such as the “Make in India” program are encouraging greater domestic substitution of CNC machining tools. Japanese METI environmental regulations encourage lower-emission precision tooling manufacture. Chinese dual circulation policies have increased localization pressures on imported high-performance tool inserts.

High Investment Activity

Investments are primarily focused in Germany, United States, China, India and South Korea due to increased automation-driven manufacturing and onshore capacity building of precision machining capabilities. Global Original Equipment Manufacturers (OEMs) are ramping up capital expenditures for CNC compatible carbide insert manufacturing and digital tooling solutions. In United States, the resurgence of automotive manufacturing is driving investments in advanced machining cells. In Germany, investments continue within the Industrial 4.0 ecosystem in intelligent tooling integration and sensor-driven cutting technologies. In China, there are aggressive investments being made to replace carbide tools domestically.

Supply Chain Disruption

The supply chain is still very susceptible due to the high concentration of carbide raw materials in China, tungsten procurement unpredictability and reliance on Germany, Japan and South Korea for grinding machinery logistics. The export limitations of tungsten carbide intermediate products have extended delivery periods for US and EU producers. India is minimizing its supply chain disruptions by increasing its carbide powder production within its own borders. The monopolization of China in the rare earth and tungsten upstream industries makes pricing and availability a threat. Disruptions in shipping from the Red Sea channels have disrupted the European tool imports schedule.

Pricing Volatility

Tools prices are very volatile owing to the cost changes of tungsten carbide, energy prices in Europe and unstable freight charges. High premium pricing occurs in Germany and Switzerland because of demand for precision cutting tools and labor costs. Base pricing is low in China, but there is price volatility associated with export restrictions. In United States, prices are determined by increased demand due to reshoring of aircraft machining operations. Prices in Japan remain stable, but expensive due to technological coatings. In India, there is price elasticity due to the presence of MSMEs involved in machining processes.

Procurement Pressure

Procurement teams operating in US, Germany, China and India are faced with growing pressures of balancing cost-efficiency and machining accuracy. The automotive original equipment manufacturers require longevity of their cutting tools and minimal machine downtimes, resulting in multi-sourcing comparisons. In aerospace procurement, certified carbide tools with traceable metallurgy have the topmost priority. Chinese domestic substitution strategies have added complexities to multinational procurement processes. Indian SMEs engaged in machining have a high cost sensitivity, leading to fierce pricing negotiations. German procurement has sustainability-oriented considerations in mind, consistent with the ESG manufacturing objectives.

New Technology Adoption

AI-powered turning solutions, IoT sensor technology, and digital twin machined parts are increasingly being adopted in Germany, the US, Japan, China, and South Korea. Smart inserts equipped with wear detection sensors are seeing increased adoption in the aerospace and electric vehicle industries. Predictive maintenance software is improving the efficiency of automotive machining operations in mass production settings. Japan is at the forefront of developing nano-coating systems that enhance thermal resistance capabilities. China is quickly expanding its automation-equipped CNC tooling ecosystem. The US is incorporating cloud-based dashboards to monitor tool performance.

Regional Expansion Opportunity

The Asia-Pacific provides the greatest potential for expansion due to growth in manufacturing in China, India and South Korea. The need for automotive electrification and semiconductor machining drives up the requirement for turning tools. The expansion of the MSME cluster in India will boost the demand for cheap tooling products. China’s localization policies make it easier for more domestic companies to enter the carbide insert market.

Europe's expansion will be driven by the precision engineering sector in countries like Germany, Italy and France. The aerospace industry and electric vehicle manufacturing drive the requirement for high-marginthe tooling products. Environmental policies have increased the use of long-life carbide tools.

Government Policy Support

Policies within China, India, Germany, the US and Japan are actively backing ecosystems of advanced tooling. Within China, there is an emphasis on the upgrading of industrial processes by promoting the substitution of domestically made carbide tools. In India, PLI schemes help back the creation of precision engineering hubs and CNC machining systems. Policies in US, through CHIPS reshoring programs, indirectly contribute to the promotion of demand for machining tools used in semiconductors production. In Germany, policies in the form of Industry 4.0 grants contribute to digital machining processes. Japan's METI programs promote energy-efficient machining processes.

Import Export And Pricing Intelligence

The global turning tool industry shows significant import-export flows where Germany, Japan, China and US hold the dominant position due to their highly developed machining systems. China is still considered the main country exporting competitive carbide inserts, whereas Germany and Japan are the leaders in the precision tools export market.

| Proxy Code | Reporter | Trade Flow | 2024 Trade Value (US$ Million) | Interpretation |

| HS 820780 | European Union | Import | 48.77 | Largest aggregated importer; strong industrial machining base across Germany, Italy, France drives demand |

| HS 820780 | Germany | Import | 48.37 | High precision engineering hub; automotive + CNC machining dominance fuels tool imports |

| HS 820780 | Singapore | Import | 41.09 | Re-export hub; supports electronics + precision manufacturing supply chains |

| HS 820780 | United States | Import | 36.06 | Strong aerospace + automotive machining demand; heavy CNC tooling consumption |

| HS 820780 | China | Import | 30.82 | Dual role: imports high-end tools while scaling domestic tooling industry |

The prices of turning tools are based on the volatile nature of carbide materials, coating technologies and the different grades of precision. Asian turning tools are cheap due to the low costs incurred during production whereas European tools are expensive because of the high tolerances involved in machining them.

Company Coverage Preview

Sandvik AB continues to be a dominant player in rotary tools globally, with a prominent market share in carbide inserts, intelligent machining systems and aircraft-specific cutting tools. The company's strategy centers around developing advanced ecosystems for smart tools featuring machine learning algorithms for predicting tool wear and cloud-based machining analysis systems. The company’s sales portfolio now includes a greater proportion of lucrative cutting tools and digital manufacturing technologies. Sandvik's business advantages include its substantial presence in the aerospace, electric vehicles and energy markets.

AI Impact Analysis

AI is revolutionizing turning tools with the help of predictive tool wear analytics, adaptive machining process control and autonomous CNC optimization. German, Japanese and American manufacturers are incorporating machine learning algorithms in order to decrease tool failure occurrences and increase the precision of surface finish. Digital twin technology using artificial intelligence will be used for simulation purposes prior to the actual machining process, thus eliminating scrap. The fast implementation of AI technologies for automated factory environments is taking place in China. India is slowly implementing cloud-based machining optimization solutions in MSME clusters.

Disruption Analysis

The most disruptive developments are the fast uptake of smart machining systems that incorporate industry 4.0 capabilities such as sensors, predictive maintenance and performance monitoring software. For example, large manufacturers like Sandvik Coromant and Kennametal Inc. are making major investments into connected tooling solutions for increased accuracy, reduced downtime and optimized tool life. Another disrupting development is the move towards the use of electric automobiles and lighter aerospace materials. The trend towards electric cars and light aerospace materials means that traditional tools meant for machining cast iron are increasingly being phased out for new tools that can handle titanium, composite materials and hardened materials such as carbide, ceramic, CBN and PCD.

Additive manufacturing and hybrid machining technologies have been disruptive to the traditional machining environments. While turning continues to be necessary for the machining of cylinders, in certain cases, selective application of 3D printing to achieve near-net shape parts results in a reduced machining effort. Sustainability considerations have also had an impact on manufacturing operations, driving changes such as the adoption of dry machining and technologies that reduce coolant usage along with carbides that are easily recycled.

Compliance with regulations concerning workplace safety and environmental protection necessitates the rethinking of the products and processes of tooling firms. Disruption is also being felt in the market through competition from the aggressive expansion of Asian tooling firms into regions where their lower-cost products compete favorably with those produced by Western and Japanese firms. It is forcing Western and Japanese companies to become more competitive with local manufacturing, digital and application engineering services.

BCG Matrix: Company Evaluation

The market is characterized by diversification among competitors, with major players being ranked within the BCG matrix according to their market shares, innovation capacity, global distribution capabilities and exposure to growth opportunities within the aerospace, automotive, medical and precision engineering sectors. Star organizations are classified as Stars because of their market dominance, innovative lineups of carbide and CBN tools and substantial investments in digital machining systems and artificial intelligence-based tooling optimization.

Cash cows have an existing clientele base, well-developed distribution channels and steady earnings derived from traditional auto and manufacturing industries. The wide range of inserts and tool holder lines ensures profitability despite relatively slow growth. Potentials are rapidly growing with competitive prices and local production capabilities. Potential players are becoming successful in emerging markets but are yet to close the technology and branding gap vis-à-vis the international competitors.

Market Dynamics

Rising Investments in Automotive and EV Manufacturing

The production of electric vehicles necessitates high-quality machining operations on electric drive trains, battery cases, transmission assemblies, shafts and aluminum structures, thereby demanding tougher and thermal-stable turning tools. As per International Energy Agency, the global sales volume of electric cars crossed 17 million units in 2024, whereas the proportion of electric vehicle sales in total car sales exceeded 20%. It surges in electrification trends is compelling automobile suppliers to modernize their machining equipment and invest in efficient turning technologies.

Furthermore, there is an increase in capital investments by automobile companies in smart machining facilities. Toyota Motor Corporation and Tesla Inc., for example, have been continuously growing their giga-factories and advanced parts factories, which utilize highly sophisticated metal cutting technology. Additionally, German automobile companies invested over €58 billion in R&D efforts in 2023, according to the German Association of the Automobile Industry, with a major share going to the automation of manufacturing and advanced machining technologies. Such trends are creating long-term opportunities for digital optimized turning tools that can function efficiently at high-speeds and continuous machining operations.

Volatility in Raw Material Costs and Tool Reconditioning Challenges

Market challenge is the uncertainty of prices for tungsten, cobalt, tantalum and rare earth elements employed in manufacturing carbides and superhard cutting tools. Tungsten carbide continues to be the leading alloy for cutting inserts due to its toughness and hardness; yet, interruptions in the distribution chain and political risks have led to price fluctuations. As per U.S. Geological Survey, China had more than 80% of globally tungsten refining capacity in 2024, making it increasingly difficult for cutting tools companies in Europe and North America to source tungsten.

Reconditioning and recycling of tools still pose operational difficulties to small and medium-scale machining firms. Advanced turning inserts and coated carbide tools are costly and incorrect re-grinding and re-conditioning may affect machining precision and tool efficiency. Manufacturers are increasingly being encouraged to meet environmental sustainability policies by minimizing the amount of industrial waste created by used cutting inserts and metal working fluids. The problem is causing manufacturers to put a lot of effort into circular economy strategies, carbide recycling services and sustainable coating solutions; however, the expenses involved in implementing these strategies are quite costly.

Segmentation Analysis

The global turning tools market is segmented based on the tool grade, machine type, workpiece detail, end-user and region.

Automotive Industry Leads Market Demand

The automobile industry remains the largest end-user application of turning tools owing to the extensive machining needs in the production of engine blocks, crankshafts, transmissions, wheels, braking systems and electric vehicle drive train parts. Manufacturing plants within the automobile industry are turning to CNC machine tools running 24/7 with the need for highly efficient inserts that reduce downtime.

Leading suppliers of automobile industry have been enhancing their machining operations in order to manufacture future generation automobiles. In the year 2024, for example, the German automotive supplier Robert Bosch GmbH has made further investments into the manufacturing plants for electric mobility components in Europe and Asia, thereby enhancing the need for precision turning machinery for the purposes of rotor shaft, stator and transmission components manufacturing. Japanese and South Korean auto-makers, on the other hand, have been increasingly using automated machining operations using AI-based systems.

Aerospace and Defense Applications Gain Momentum

The industry of aerospace and defense sector is being seen as one of the areas where the demand for advanced turning machines will be seen to rise owing to the high production of aircraft and defense equipment globally. The aerospace companies need precise machines which can manufacture parts such as turbine blades, landing gears, engine casing and titanium parts that function at an extremely high temperature and pressure.

The production rate of aircraft by firms like The Boeing Company and Airbus SE is continually rising due to high demands for commercial flights. Both of these industries utilize special turning tools that are ceramic and CBN inserts to be able to machine hard aerospace metal.

Geographical Penetration

U.S. Turning Tools Market Trends

The U.S. tools turning market is fueled by significant investments in the aerospace, defense, automotive, medical devices and precision engineering sectors. The country still retains its position as home to one of the largest ecosystems for advanced manufacturing operations, powered by widespread use of CNC machines and high demand for carbide, ceramic, CBN and coated turning inserts. The recovery of aerospace manufacturing, reshoring activities and investment in semiconductor manufacturing have led to growing demands for efficient turning systems that can machine titanium, nickel alloys, hardened steel and composites.

The emergence of more facilities for production through industry 4.0 manufacturing within US has been leading to an increase in the adoption of turning tools that are digital, come with wear monitoring features, have the capability for predictive maintenance and high-speed machining. Government backing in the form of policies such as the CHIPS and Science Act and advancements in manufacturing are driving capacity growth for manufacturing semiconductors, electric vehicles parts and defense machinery. U.S. is still an innovator in developing coating solutions for tooling, adding to the geometries for tooling and using artificial intelligence in machining optimization. Finally, automobile electrification has led to an increase in demand for tooling solutions especially for aluminum machining and precision machining of drive train components.

Japan Turning Tools Market Trends

Japan is among the leaders in the production of turning tools, mainly due to the competitiveness of its automotive, robotic, semiconductor equipment and industrial machinery industries. The Japanese are leading producers of highly precise machining techniques, super-hard carbide alloys, nanocoatings and high-speed turning. Japan's turning tools market enjoys a great deal of advantage owing to the competitiveness of the machine tools industry in the country, with players like DMG MORI, Mazak, Okuma and Makino taking center stage.

The trend for Japan's turning tools market has been towards energy-efficient and automated machining products. Demand for turning tools with ultra-high accuracy as well as those that can sustain their longevity when machining is due to the rise in investment in semiconductor production, EV parts manufacturing and aerospace precision machining. Foreign buyers continued to be the strongest players in this market, accounting for over 70% of Japan’s overall machine tool business in 2024, based on manufacturing industry reports. The country is also seeing an increasing number of smart machining systems being implemented in production processes, using sensor technology, adaptive machining and even artificial intelligence to optimize machining processes and increase output while minimizing downtime. Tooling companies in Japan have continued to focus significantly on sustainable machining practices through the use of recyclable carbide recycling and low-friction coating technologies.

China Turning Tools Market Trends

China is still one of the major turning tool manufacturing hubs globally because of its vast manufacturing sector that produces automobiles, electronic products, machinery, aerospace products and heavy machines. The fast-paced industrial automation and increased use of CNC machines in China have led to the ever-increasing use of turning inserts and carbide tools. In addition, the booming semiconductor equipment manufacturing, EV manufacturing and renewable energy equipment manufacturing industries in China have created a high demand for high-performance turning tools.

China is currently shifting fast from normal turning tool utilization to more premium and technology-oriented products. Domestic suppliers are currently focusing on producing more coated carbide tools, ceramic inserts and turning tools made from cubic boron nitride. Moreover, there are plans by the government towards automation through smart manufacturing and robotics, which have seen many companies embrace digitalized manufacturing platforms such as CNC turning centers with machine optimization software powered by artificial intelligence. With China being an innovator in electric vehicle manufacturing, the country's current focus on the production of vehicles with high performance will drive a high demand for more precise and advanced turning tools such as those used in batteries and motor assembly. Another area driving the demand for such advanced metal-cutting machinery includes rapid growth in the aircraft industry and fast-track projects for high-speed railway construction.

Competitive Landscape

- The global turning tools market features intense competition among multinational cutting tool manufacturers, precision engineering companies and advanced materials specialists competing through coating technologies, tool durability, machining efficiency and digital machining integration capabilities.

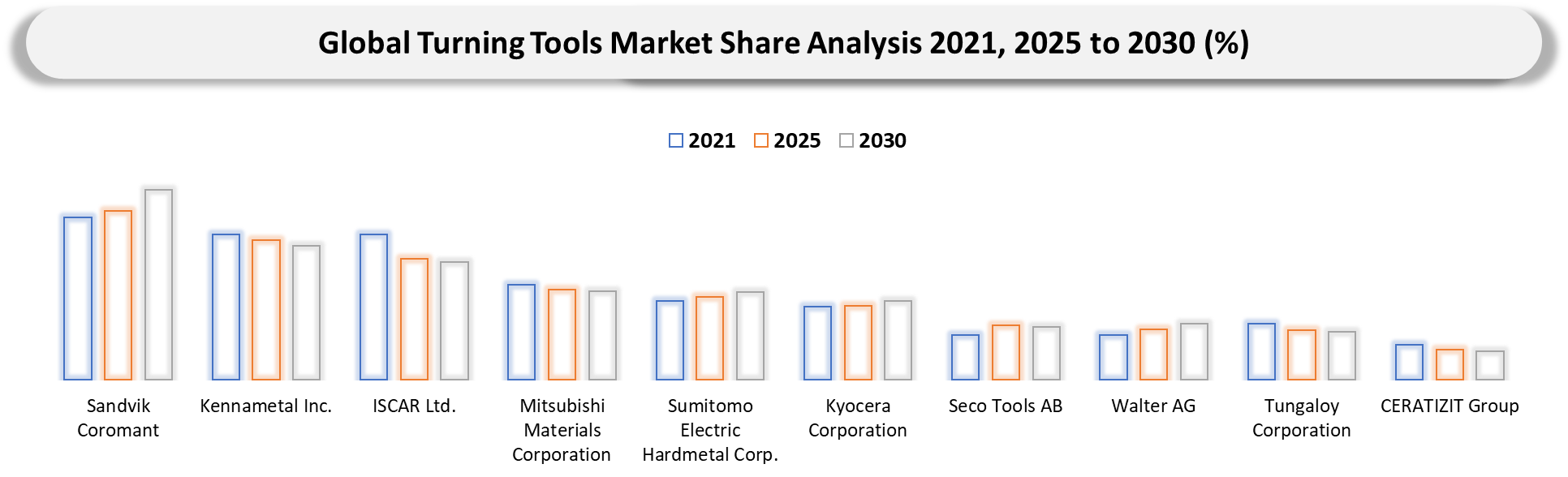

- Key players include Sandvik AB, Kennametal Inc., ISCAR Ltd., Mitsubishi Materials Corporation, Sumitomo Electric Industries, Ltd., Kyocera Corporation, Seco Tools AB, CERATIZIT S.A., Walter AG and Tungaloy Corporation.

- Companies are differentiating themselves through advanced coating technologies such as PVD and CVD coatings, AI-enabled tool monitoring systems, vibration reduction capabilities and customized insert geometries designed for high-speed and high-feed machining operations.

Strategic investments in carbide recycling, digital machining platforms, additive manufacturing-compatible tooling and sustainable machining technologies are becoming critical competitive factors as manufacturers prioritize operational efficiency, supply chain resilience and environmentally responsible production practices.

MAJOR PAIN POINTS

- Fluctuating raw material prices for tungsten carbide, cobalt, ceramics and high-speed steel increasing production costs and squeezing profit margins.

- Rapid tool wear and shorter tool life while machining hardened steels, titanium alloys, composites and aerospace-grade materials.

- Intense pricing competition from low-cost regional manufacturers creating margin pressure for premium turning tool suppliers.

- Shortage of skilled CNC machinists, tooling experts and automation specialists impacting operational efficiency and productivity.

- High upfront cost of advanced carbide, ceramic, CBN and coated turning tools limiting adoption among SMEs.

- Supply chain disruptions, import dependency and logistics delays affecting timely availability of cutting inserts and tooling components.

- Rising demand for high-precision machining requiring continuous investment in innovative tool geometries, coatings and smart tooling technologies.

- Downtime caused by frequent tool replacement, maintenance and re-sharpening reducing productivity in high-volume production environments.

- Transition toward electric vehicles and lightweight materials changing machining requirements and reducing demand for some conventional turning applications.

Economic slowdowns and fluctuating industrial production reducing capital expenditure on machine tools and consumable turning tools.

KEY DEVELOPMENTS

- April 2026: Kennametal Inc. expanded KENGold coated turning insert portfolio, improving wear resistance, thermal stability and productivity for precision turning applications.

- March 2026: Sandvik Coromant released CoroTurn PI internal turning family featuring enhanced chip evacuation, coolant configurations and improved process security.

- January 2026: Sandvik Coromant collaborated with ZF Friedrichshafen developing CoroTurn Hard PrimeTurning process for drive bevel gears, improving hard-turning productivity significantly.

- November 2025: Sumitomo Electric Hardmetal Corp. expanded turning insert lineup with wear-resistant carbide grades enhancing machining efficiency for heat-resistant alloy applications globally.

- November 2025: Kyocera Corporation enhanced internal threading and turning insert offerings, targeting stainless-steel machining applications requiring superior chip-control and durability.

- November 2025: Seco Tools AB launched TS0501 Duratomic finishing grade for superalloy turning, improving tool life, reliability and surface-finish consistency significantly.

- November 2025: Walter AG released WL Copy Turn system improving insert indexing accuracy, vibration reduction and process stability in copy-turning operations.

- October 2025: Walter AG introduced 1,600 machining products including turning technologies focused on productivity, coating innovation and serial-production reliability improvements.

- October 2025: Mitsubishi Materials Corporation introduced advanced CVD-coated turning grades supporting stable machining performance across automotive and aerospace precision manufacturing applications.

September 2025: ISCAR Ltd. expanded LOGIQ turning solutions portfolio supporting higher metal-removal rates, improved insert stability and extended tool-life performance.

ANALYST VIEW / OPINION

- Precision machining demand from electric vehicles accelerates advanced turning tools adoption globally.

- Coated carbide inserts dominate product innovation through enhanced wear resistance capabilities.

- Aerospace manufacturing expansion increases requirement for ultra-precision and high-speed turning solutions.

- Smart manufacturing integration drives adoption of sensor-enabled and digitally monitored turning tools.

- Asia-Pacific manufacturing growth strengthens regional production and consumption of turning tools significantly.

- Multi-axis CNC machining trends encourage development of customized and modular turning tools.

- Sustainability initiatives promote recyclable tool materials and longer lifecycle cutting technologies globally.

- Rising automation investments increase demand for high-performance tools minimizing machine downtime efficiently.

- Additive manufacturing complements turning operations through hybrid machining and finishing applications growth.

- Competitive differentiation increasingly depends on tooling efficiency, precision consistency and productivity optimization.

TARGET AUDIENCE

| INDUSTRY | WHO SHOULD BUY THIS REPORT? | REASON TO BUY THIS REPORT |

| Automotive & EV Manufacturers | CNC Turning Operations Teams, Manufacturing Engineers, Production Heads | Analyze turning tool demand for engine components, shafts, transmission systems and EV drivetrain machining applications |

| Aerospace & Defense Companies | Precision Machining Engineers, Tooling Specialists, Aerospace Production Teams | Evaluate advanced turning solutions for titanium alloys, aerospace-grade materials and high-tolerance components |

| Industrial Machinery Manufacturers | Plant Operations Managers, Industrial Engineering Teams, CNC Programming Departments | Optimize turning operations, machining productivity and tooling lifecycle management |

| General Engineering & Metal Fabrication Companies | Workshop Supervisors, Fabrication Managers, Production Planning Teams | Identify efficient turning tools for large-scale metal cutting and fabrication processes |

| CNC Machine Tool Manufacturers | Product Development Teams, Automation Engineers, Strategic Partnerships Teams | Understand demand trends for CNC-compatible turning tools and smart machining integration |

| Oil & Gas Equipment Manufacturers | Heavy Machining Teams, Reliability Engineers, Procurement Managers | Evaluate wear-resistant turning tools for valves, pipelines and drilling equipment manufacturing |

| Energy & Power Generation Companies | Turbine Manufacturing Teams, Plant Engineering Departments, Sourcing Teams | Assess turning tool requirements for turbines, generators and critical power equipment components |

| Construction & Mining Equipment Manufacturers | Heavy Equipment Production Teams, Manufacturing Operations Managers | Analyze durable turning solutions for large-scale and abrasive material machining |

| Railway Equipment Manufacturers | Rail Component Manufacturing Teams, Operations Engineers, Procurement Departments | Understand tooling demand for wheelsets, axles and railway infrastructure component machining |

| Marine & Shipbuilding Companies | Shipyard Engineering Teams, Precision Machining Departments, Production Managers | Evaluate turning tools for marine engine parts and structural equipment manufacturing |

| Medical Device Manufacturers | Precision Component Engineers, Micro-Machining Teams, R&D Departments | Study ultra-precision turning technologies for miniature and high-accuracy medical components |

| Electronics & Semiconductor Equipment Manufacturers | Advanced Manufacturing Teams, CNC Precision Engineers, Product Innovation Teams | Assess micro-turning solutions for semiconductor and electronics equipment production |

| Tooling Manufacturers & Insert Producers | Product Innovation Teams, Competitive Intelligence Departments, Strategy Managers | Benchmark turning tool technologies, coatings, inserts and market positioning strategies |

| Carbide, Ceramic & Superhard Material Suppliers | Technical Sales Teams, R&D Engineers, Market Intelligence Teams | Analyze future demand for carbide, ceramic, CBN and PCD turning tool materials |

| Industrial Automation & Smart Factory Companies | Industry 4.0 Teams, Automation Integration Engineers, Smart Manufacturing Consultants | Evaluate integration opportunities between turning tools, CNC systems and automated machining platforms |

| Industrial Distributors & Tooling Dealers | Category Managers, Regional Sales Teams, Inventory Management Departments | Identify regional demand trends, high-growth applications and customer purchasing patterns |

| Contract Manufacturing & Job Shops | CNC Workshop Owners, Production Supervisors, Cost Optimization Teams | Assess profitable machining segments and tooling investments for precision turning applications |

| Research Institutes & Universities | Manufacturing Research Teams, Material Science Researchers, Industrial Engineering Faculties | Study innovations in turning tool materials, coatings and advanced machining technologies |

| Government & Defense Manufacturing Organizations | Defense Production Units, Railway Workshops, Industrial Development Authorities | Support industrial modernization, strategic manufacturing capabilities and domestic machining initiatives |

| Investors, Private Equity & Consulting Firms | Investment Analysts, Industrial Consultants, Market Intelligence Teams | Evaluate market growth opportunities, competitive landscape and technology adoption trends in turning tools industry |

WHY CHOOSE DATAM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

WHAT DATAM UNIQUELY PROVIDES

- Real-time procurement intelligence tracking OEM tooling contracts, supplier switching behavior and regional sourcing diversification across manufacturing hubs globally

- Price benchmarking models comparing carbide, ceramic and coated insert cost curves across automotive, aerospace and industrial machining segments

- Competitive heatmaps identifying share shifts among Sandvik, Kennametal, Mitsubishi Materials and regional Chinese tooling manufacturers

- Predictive demand forecasting integrating automotive EV transition, aerospace backlog cycles and semiconductor machining expansion trends globally

- Supply chain vulnerability scoring covering tungsten dependency, logistics disruptions and geopolitical export control exposure across regions

- Investment tracking dashboard monitoring CAPEX flows into smart machining, CNC automation and precision tooling manufacturing ecosystems globally

QUESTIONS THIS REPORT ANSWERS

- What is the current and forecast market size of the global turning tools market through 2035?

- Which end-users are driving demand growth and why?

- Which regions and tool categories present the highest growth and investment opportunities in the global turning tools market?

- How are investments in CNC machining, Industry 4.0 and smart manufacturing reshaping production efficiency and competitive dynamics in the turning tools market?

- How do trade regulations, raw material price volatility and geopolitical risks affect turning tools manufacturing and supply chain stability?

- Which tool materials and are shaping next-generation turning tools manufacturing?