TinyML Market Overview

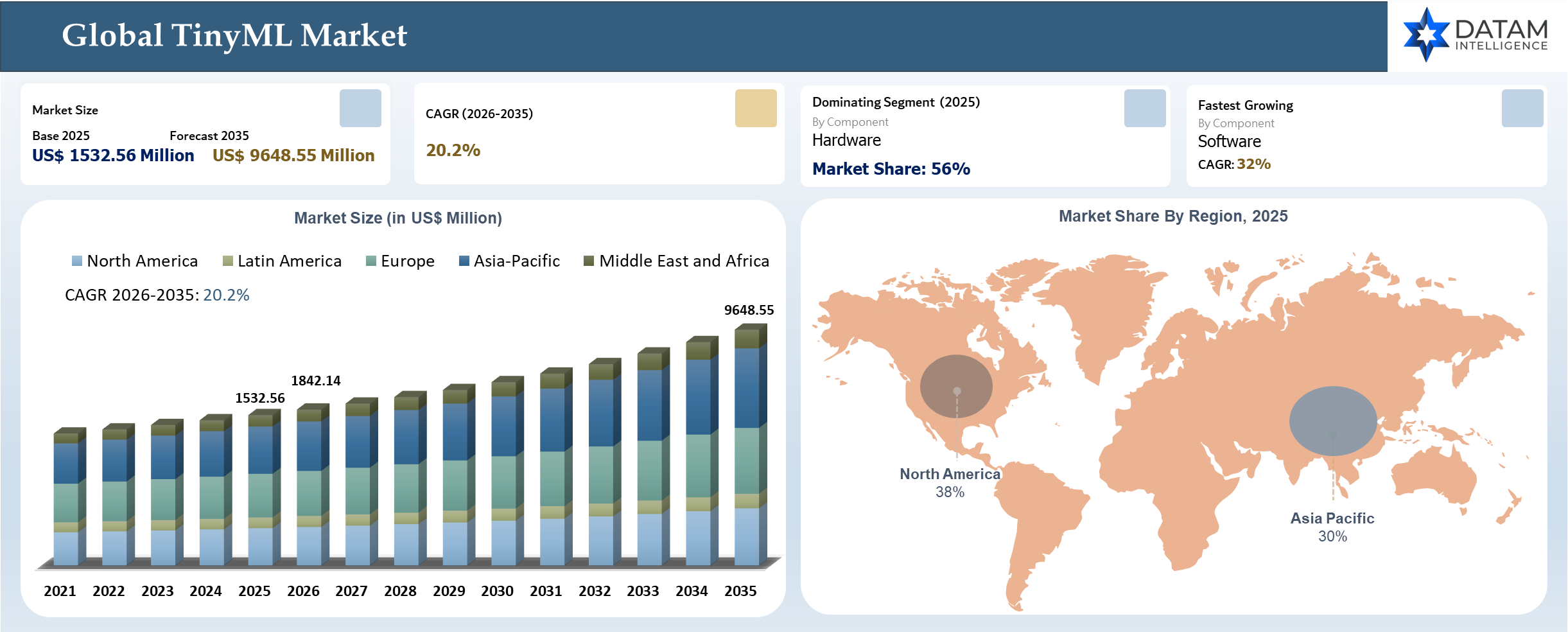

The global TinyML market reached US$ 1532.56 million in 2025 and is expected to reach US$ 9648.55 million by 2035, growing with a CAGR of 20.2% during the forecast period 2026-2035. TinyML allows machine learning models to be executed on constrained devices like microcontrollers, thus offering real-time computation capability without relying on cloud services. There is increasing adoption owing to the rising interest in edge computing, low latency, and efficiency in IoT deployments. Improvements in hardware design and model optimization are facilitating implementation of AI within constraints. For instance, in 2025, Nordic Semiconductor showcased ultra-compact ML models through its Neuton framework designed for wireless SoCs with minimal memory usage.

TinyML Industry Trends and Strategic Insights

- The TinyML market is witnessing a strong shift toward edge-native intelligence, driven by the need for ultra-low latency, energy efficiency, and real-time decision-making at the device level. Companies such as Google and Microsoft are expanding lightweight AI frameworks and edge platforms that enable seamless deployment of machine learning models directly on microcontrollers and embedded systems.

- Semiconductor leaders including STMicroelectronics and NXP Semiconductors are increasingly integrating AI capabilities into low-power chipsets, supporting on-device inference across industrial, automotive, and consumer applications. These advancements are enabling scalable adoption of TinyML by improving processing efficiency while minimizing energy consumption.

- Additionally, specialized platform providers such as Edge Impulse and SensiML Corporation are simplifying development workflows through end-to-end toolchains, accelerating deployment across diverse use cases. At the same time, growing convergence between IoT, edge computing, and connectivity technologies is fostering new business models centered around autonomous systems and distributed intelligence.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 1532.56 Million | |

| 2035 Projected Market Size | US$ 9648.55 Million | |

| CAGR (2026-2035) | 20.2% | |

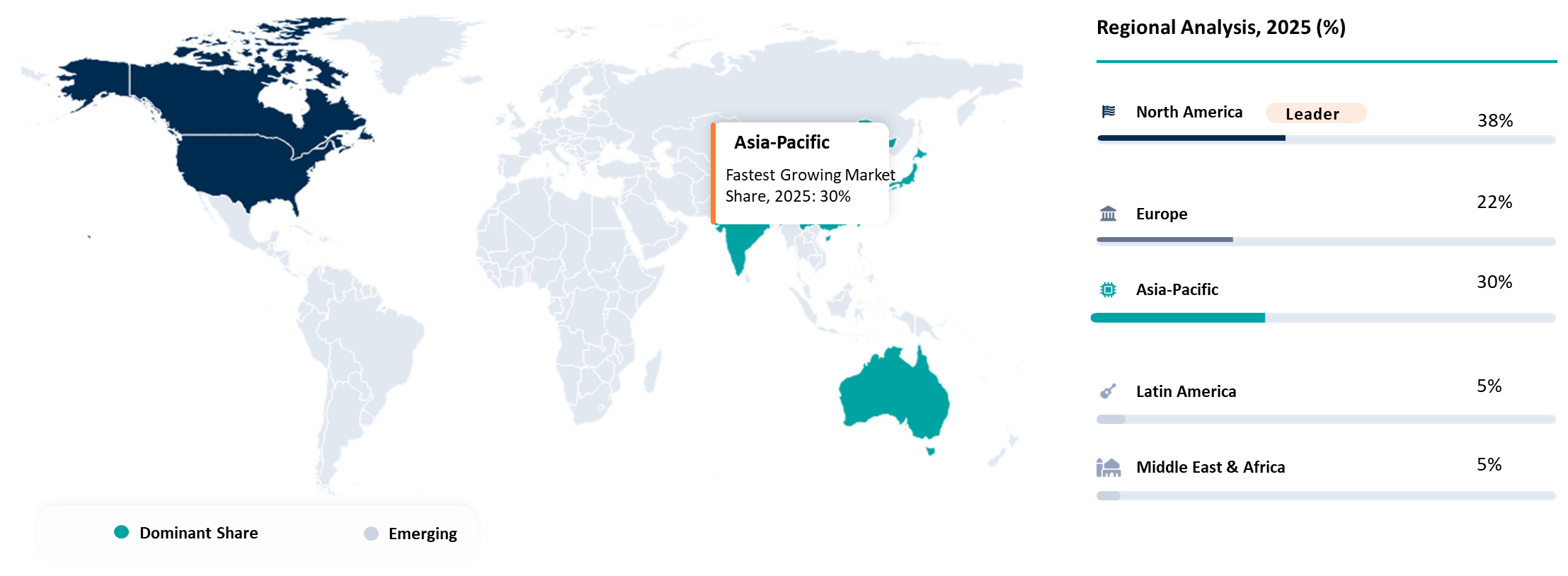

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Component | Hardware, Software, and Services | |

| By Deployment Mode | On Premises, Cloud-Based | |

| By Application | Agriculture, Healthcare, Manufacturing, Automotive, Industrial IoT, Consumer Electronics, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

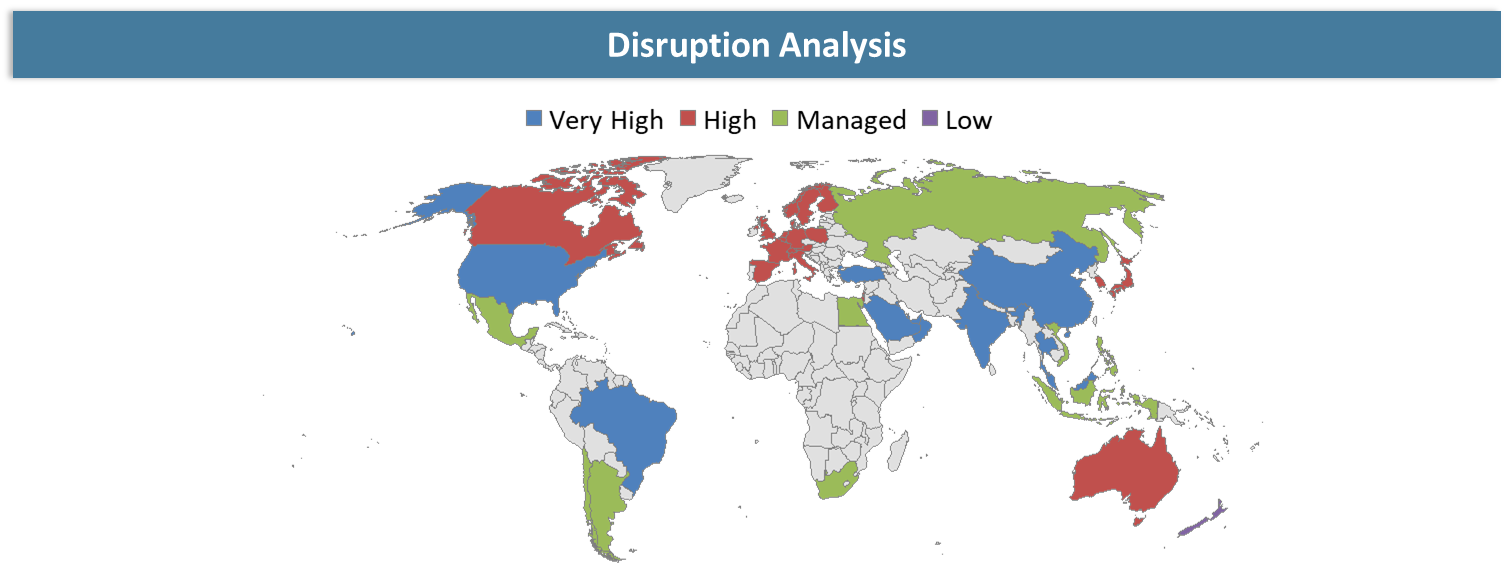

Disruption Analysis

Shift from Cloud-Dependent AI Models to Ultra-Low-Power Edge Intelligence Redefining Compute Paradigms

The TinyML industry is moving from central cloud-based systems to extremely low-power edge devices, which can perform real-time inference. It is transforming the way data is processed by reducing latency, eliminating the need for bandwidth, and lowering costs while supporting autonomous decision-making capabilities on-device. Cloud-first AI players and IoT firms are being disrupted as organizations favor local processing and secure computations.

At the same time, improvements in microcontroller efficiency, model compression approaches, and AI frameworks for embedded devices are boosting the adoption of AI technology in limited resource environments. This trend will drive the adoption of cost-effective AI in industries like industrial automation, healthcare applications, and consumer electronics. Those market players that do not adapt their strategy to the new reality by embracing efficient edge-based AI solutions could become less competitive in the future.

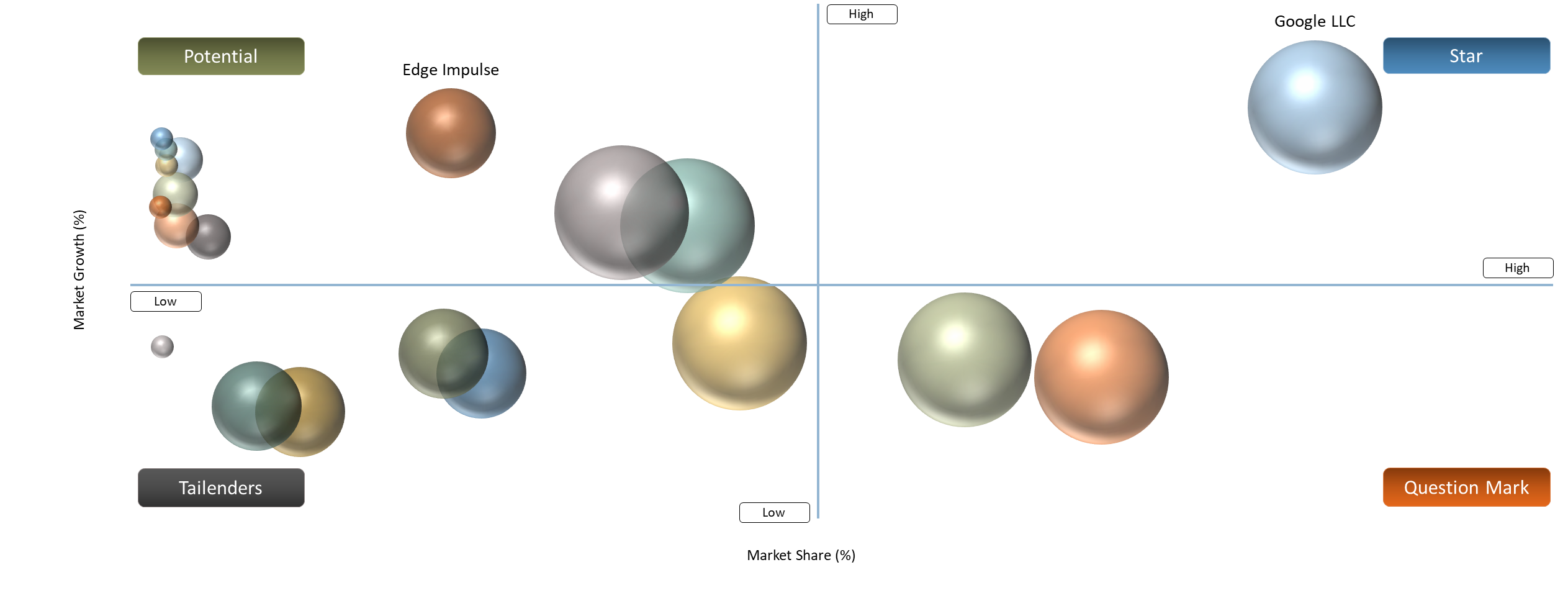

BCG Matrix: Company Evaluation

The Hyperscalers like Google and Microsoft can be considered Stars since they possess strong ecosystems for AI, scalability at the edge, and TinyML integration into the architecture of IoT and cloud solutions. Other companies that can be placed in this category include semiconductor giants like STMicroelectronics and NXP Semiconductors. The latter benefit from their extensive product line of microcontrollers as well as embedded AI. On the other hand, Arm Limited and Nordic Semiconductor can be positioned as Question Marks since their technological capability is very promising, while their value creation is not as direct in the TinyML environment. The future placement of these organizations will hinge upon the degree of integration within the ecosystem and monetization of edge AI solutions.

Edge Impulse, SensiML Corporation, and Imagimob are Potential players owing to their innovative approach and increasing use of development platforms to facilitate the implementation of TinyML solutions. They represent strong growth opportunities but have relatively small shares in comparison with leading companies in the industry. Syntiant belongs to Tailenders due to its narrow product focus and constrained scale of operations.

Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

| Rise of Edge AI and IoT Proliferation | 2.6% | Highly concentrated in Asia-Pacific and North America with large-scale IoT deployments | Smart sensors, industrial IoT, connected devices | Drives large-scale deployment of on-device intelligence, reducing dependence on cloud infrastructure |

| Demand for Real-Time, Low-Latency Processing | 2.2% | Strong across automotive, healthcare, and industrial automation sectors globally | Wearables, driver monitoring systems, predictive maintenance | Positions TinyML as critical for latency-sensitive applications requiring instant decision-making |

| Ultra-Low Power AI Requirements | 2.0% | Concentrated in battery-operated device ecosystems such as consumer electronics and remote IoT | Wearables, smart home devices, remote monitoring systems | Enables long-duration operation and expands AI adoption in energy-constrained environments |

| Advancements in Microcontrollers and Edge AI Hardware | 1.8% | Centered in semiconductor innovation hubs such as the United States, Europe, and East Asia | Embedded AI chips, microcontroller-based ML devices | Strengthens hardware-software co-optimization and accelerates commercialization of TinyML solutions |

Rise of Edge AI and IoT Proliferation Accelerating TinyML Adoption Across Distributed Environments

The rapid growth witnessed by IoT and Edge Computing technologies is one of the significant reasons behind the rising interest in TinyML technology, backed by reliable quantitative evidence from both enterprise environments and device infrastructures. The number of connected IoT devices is expected to grow 14% year-over-year to 21.1 billion by the end of 2025, along with rapid enterprise adoption with 64% firms adopting IoT and another 23% in the process of implementing it. On the other hand, 97% of CIOs include edge AI in their roadmaps, with nearly 52% of them being deployed or operational.

However, there is an operational aspect of the transition to TinyML that is quite crucial and important for organizations as well. Approximately 82% of businesses have already started using real-time IoT analytics or are considering doing so. Similarly, more than 75% of companies have started using AI/ML in IoT solutions so that they can predict certain scenarios and automate their operations. The use of Edge AI helps in reducing the latency by up to 90%, as well as bandwidth usage by 75%, in addition to enabling 65% of IoT data to be analyzed at the edge. Moreover, industrial applications show some benefits, such as ~40% reduction in downtime, making the ROI of integrating edge intelligence tangible and clear.

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

| Limited Memory and Computational Capacity | 1.9% | Microcontroller architecture and on-device processing limits | Complex vision models, multi-sensor AI applications | Constrains model sophistication, limiting TinyML adoption in high-accuracy and compute-intensive scenarios |

| High Development and Model Optimization Complexity | 1.7% | Model compression, quantization, and deployment workflows | Custom TinyML applications and edge AI integration | Increases development time and cost, creating barriers for large-scale and rapid deployment |

| Fragmented Ecosystem and Lack of Standardization | 1.5% | Cross-platform hardware and software interoperability | Multi-device IoT ecosystems and scalable deployments | Slows ecosystem maturity and complicates integration across diverse platforms |

| Power vs Performance Trade-offs in Edge Devices | 1.3% | Energy management in battery-powered systems | Always-on monitoring, voice detection, remote sensing | Limits sustained performance and reduces efficiency in continuous, real-time applications |

Limited Memory and Computational Capacity

Deployments involving TinyML are always subject to constraints in terms of the available memory, storage, and computing power of the underlying edge devices. These constraints are more acute than those that affect other types of computing infrastructure because edge devices have stricter limits as far as their capacity is concerned. As such, the machine learning models that can be deployed under the circumstances are often less sophisticated.

This issue means that organizations have to engage in significant efforts in terms of model optimization before being able to deploy machine learning models on the edge. The current approach involves several methods of optimization including pruning and quantization as well as redesigning of machine learning architectures. While the above-mentioned approaches have been proven effective in optimizing machine learning models, they add another layer of complexity to the task at hand.

Segmentation Analysis

The global TinyML market is segmented based on component, deployment mode, application and region.

Embedded AI Integration and Advancements in Edge-Optimized Chip Architectures Driving Market Leadership

The hardware segment leads the TinyML market due to the wide-scale usage of microcontrollers, sensors, and low-power processors used for data processing purposes in different end-user sectors. The growing tendency towards embedding AI features directly into semiconductor chips allows for immediate processing at the endpoint without any need for additional infrastructure and centralized computing facilities. These trends can be observed in several end-use segments, such as consumer goods, industrial machinery, or medical devices.

Advancements in chip design, including energy-efficient architectures and dedicated AI accelerators, are further strengthening the value proposition of hardware in TinyML deployments. For instance, in 2025, Qualcomm, a U.S.-based semiconductor and edge AI technology company, acquired Arduino, an Italy-based microcontroller hardware platform provider, and introduced the Arduino UNO Q, an AI-enabled development board integrating a high-performance processor with a real-time microcontroller to enable on-device edge AI and TinyML applications.The growing popularity of edge computing ecosystems contributes to the strong market position of the hardware segment.

Geographical Penetration

Strong AI Ecosystem and Early Edge Adoption Driving Regional Leadership

North America holds the position as the market leader owing to the presence of an established AI ecosystem, high adoption of IoT technologies, and robust edge computing infrastructure development. In this region, early adoption of technology across sectors like health care, industrial automation, and consumer electronics helps in quick adoption of on-device intelligence. Focus on real-time data processing and privacy-oriented solutions is boosting the regional market position.

The development of advanced semiconductors and AI platforms is expected to drive the market. For instance, in 2026, Google, a U.S.-based technology company, launched next-generation training and inference TPUs to enhance AI processing efficiency and scalability. Such technological advancements indicate that the region focuses on developing its AI capabilities, which indirectly promotes edge AI capabilities and TinyML solutions.

U.S TinyML Market Trends

The U.S emerges as the major contributor to growth in North America owing to its advanced technology infrastructure and high adoption rates among enterprises of AI-based solutions. The nation enjoys the advantages of prominent semiconductor companies, providers of AI platforms, and a developed startup culture, which facilitates the swift development and implementation of TinyML applications in diverse sectors like healthcare, automotive, and manufacturing. Moreover, the US is investing heavily in R&D efforts, reinforcing its dominant role in developing edge intelligence technologies.

The growing need for timely analysis, secure handling of sensitive information, and minimal latency encourages enterprises to adopt on-device AI solutions. They are incorporating TinyML technologies in their IoT networks to enhance efficiency and minimize reliance on cloud computing.

Canada TinyML Market Outlook

Canada has gradually been increasing its footprint in the TinyML market due to high-quality academic research, government initiatives, and efforts aimed at developing business cases for AI. Ethical approaches to AI development and data protection in Canada make it an excellent fit for the main benefits associated with TinyML solutions that are used for the processing of locally generated data. The rising popularity of IoT systems in various industries also contributes to the market expansion.

In addition, Canadian startup culture and partnerships between research organizations and companies have led to the development of innovative edge AI solutions. Although the current market size in Canada is smaller than in the US, consistent market growth has been recorded because of AI research progress and increased enterprise awareness.

Competitive Landscape

- The TinyML market is highly competitive, led by platform providers such as Google and Microsoft, which drive ecosystem adoption through scalable AI frameworks and edge integration capabilities. Semiconductor leaders including STMicroelectronics and NXP Semiconductors play a critical role by enabling on-device intelligence through advanced microcontrollers and low-power AI hardware. Arm Limited strengthens the market through its widely adopted architectures that support edge AI deployment at scale. Additionally, specialized players such as Edge Impulse are gaining traction by offering developer-centric platforms that simplify TinyML implementation across industries.

- Key players include Google LLC, STMicroelectronics, Arm Limited, Microsoft, Edge Impulse, NXP Semiconductors, Imagimob A.B, SensiML Corporation, Nordic Semiconductor, Syntiant Corp

Key Developments

- February 2025: NXP Semiconductors, a Netherlands-based semiconductor company, announced the acquisition of Kinara, an edge AI chipset company, to strengthen its neural processing and edge AI capabilities for intelligent systems.

- June 2025: Nordic Semiconductor, a Norway-based semiconductor company, showcased ultra-tiny ML models through its Neuton framework designed to run on wireless SoCs with significantly reduced memory footprint and improved inference efficiency.

- April 2026: Google, a U.S.-based technology company, launched next-generation training and inference TPUs to enhance AI processing performance and compete in advanced AI hardware.

- October 2025: Qualcomm, a U.S.-based semiconductor and edge AI technology company, acquired Arduino, an Italy-based microcontroller platform provider, and introduced the Arduino UNO Q, an AI-enabled development board for on-device edge AI applications.

- September 2025: Arm Limited, a U.K.-based semiconductor design company, launched next-generation mobile chip architectures optimized for AI-driven workloads and on-device intelligence.

Why Choose DataM?

- Technological Innovations: Explores advancements in ultra-low-power AI design, including optimized microcontroller architectures, on-device inference engines, model compression techniques, and integration with edge computing frameworks that enable real-time analytics with minimal energy consumption across IoT applications.

- Product Performance & Market Positioning: Evaluates how different players perform across industrial IoT, healthcare wearables, consumer electronics, and automotive applications, comparing parameters such as power efficiency, inference speed, memory utilization, latency, and scalability, highlighting how leading companies differentiate through hardware-software integration.

- Real-World Evidence: Highlights practical use cases of TinyML across predictive maintenance, remote patient monitoring, smart agriculture, and intelligent consumer devices, demonstrating measurable improvements in operational efficiency, reduced cloud dependency, faster decision-making, and enhanced data privacy.

- Market Updates & Industry Changes: Tracks key developments such as new AI-enabled microcontroller launches, expansion of edge AI platforms, advancements in semiconductor design, and increasing adoption of decentralized AI architectures across major regions including North America, Asia Pacific, and Europe.

- Competitive Strategies: Analyzes how leading companies expand their presence through ecosystem development, platform integration, developer tool enhancement, and strategic partnerships, along with differentiation through energy-efficient AI solutions and end-to-end TinyML deployment capabilities.

- Pricing & Market Access: Explains pricing dynamics across hardware components, development platforms, and integrated solutions, including cost advantages of on-device processing over cloud-based models, along with accessibility through open-source frameworks and developer ecosystems.

- Market Entry & Expansion: Identifies growth opportunities in emerging markets driven by IoT expansion, increasing demand for real-time analytics, and rising adoption of low-power AI solutions, while outlining strategies such as localized manufacturing, ecosystem partnerships, and application-specific innovation.

Target Audience 2026

- Technology & IoT Companies: Firms developing connected devices, smart sensors, and embedded systems integrating TinyML for real-time intelligence.

- Semiconductor & Hardware Manufacturers: Companies designing microcontrollers, edge AI chips, and low-power processors targeting on-device machine learning applications.

- Healthcare & Wearable Device Companies: Organizations leveraging TinyML for remote monitoring, diagnostics, and personalized healthcare solutions.

- Industrial & Manufacturing Enterprises: Companies adopting TinyML for predictive maintenance, automation, and operational optimization.

- Automotive & Mobility Providers: OEMs and technology firms integrating edge AI for driver monitoring, safety systems, and autonomous features.

- Investors & Venture Capital Firms: Stakeholders tracking growth in edge AI, semiconductor innovation, and next-generation IoT technologies.

- Developers & AI Platform Providers: Software developers and platform companies focused on building, optimizing, and deploying TinyML models across industries.