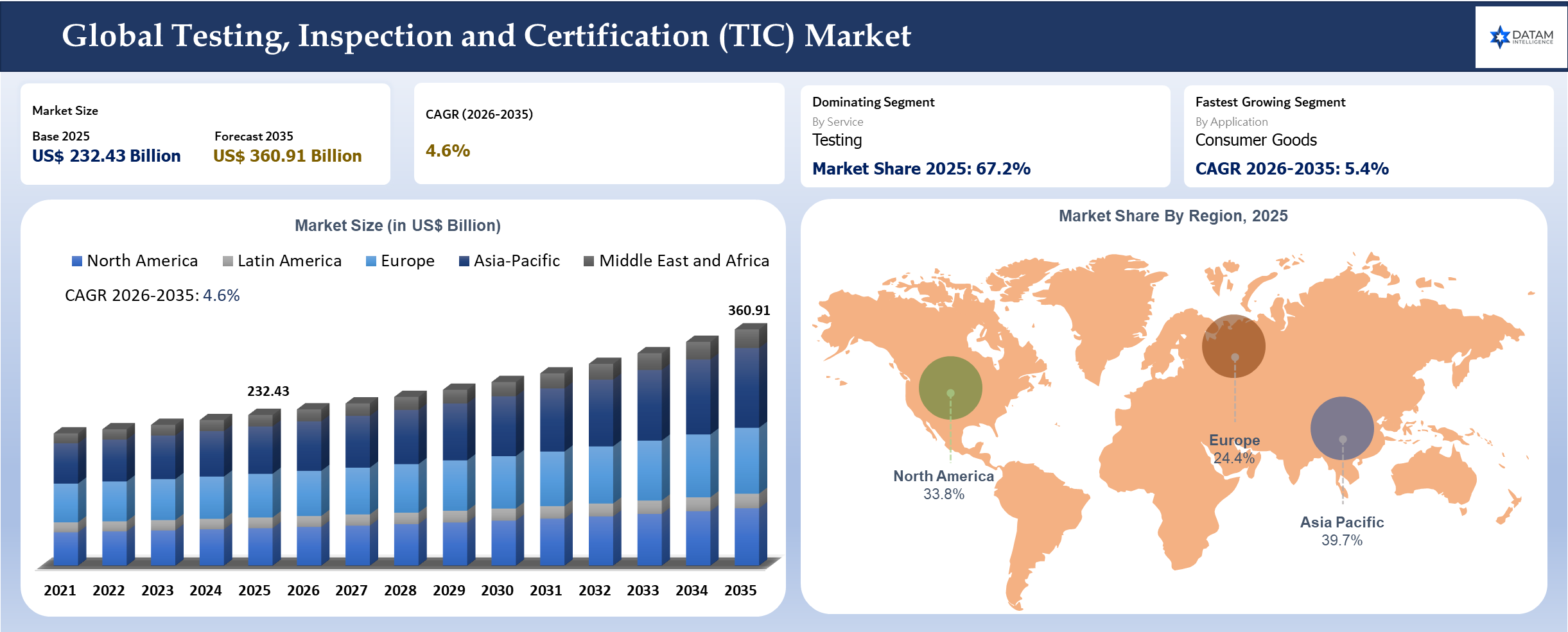

Testing, Inspection and Certification (TIC) Market Size & Forecast

The global TIC market size was reached US$ 232.43 billion in 2025 and is expected to reach US$ 360.91 billion by 2035, growing with a CAGR of 4.6% during the forecast period 2026-2035. The demand is increasing since compliance work is transitioning from being occasional to being continual, not just product compliance but assurance of all facilities, infrastructure, software-enabled assets and even extended supplier ecosystems.

Big manufacturing corporations and infrastructure owners depend on assurance from companies more often since they have become sector-specific. EV batteries need electrical safety testing, thermal abuse testing, charging interoperability and materials tracing testing; food producers need control testing, lab testing and supplier testing. Data centers need pre-tenant commissioning, quality control and energy efficiency testing prior to capacity being made available to hyperscalers.

There is a shift happening in procurement practices as well. Companies do not require a lab facility or issuing a certificate anymore. The company they choose needs to be able to offer multiple services such as laboratory capabilities, field inspections, cyber assurance services, sustainability verification, digital capabilities, and access to local certification programs. Scale continues to matter but specialization does too.

Testing, Inspection and Certification Industry Trends and Strategic Insights

- A major trend is the movement toward connected assurance workflows. Laboratory information management systems, remote inspection tools, computer vision, digital twins and automated evidence capture are reducing manual documentation burden. For regulated customers, faster turnaround has become a competitive advantage because delayed approval can hold inventory, delay construction completion or postpone product launch.

- Another important shift is the rise of sustainability assurance. Carbon accounting, responsible sourcing, recycled content verification, product environmental claims and supply chain due diligence now sit closer to quality and risk functions. Providers with audit networks and recognized sector experts are turning sustainability from an advisory offering into repeatable verification revenue.

TIC Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 232.43 Billion | |

| 2035 Projected Market Size | US$ 360.91 Billion | |

| CAGR (2026-2035) | 4.6% | |

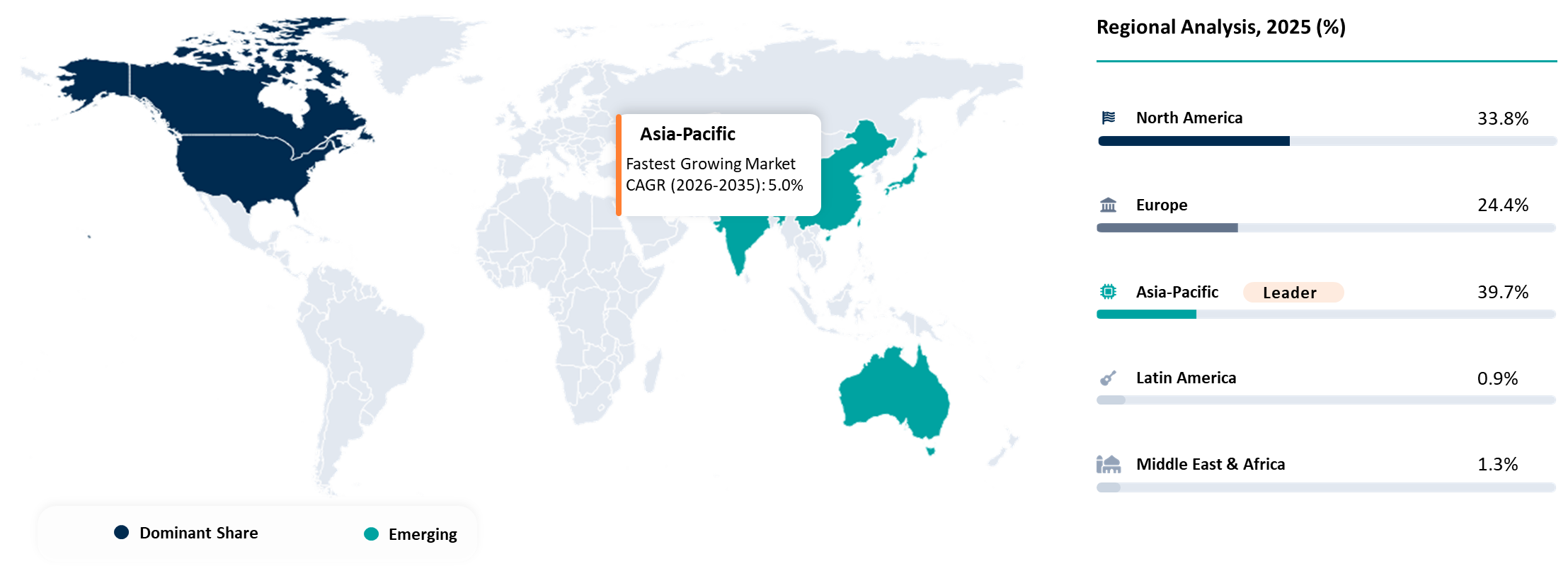

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Service | Testing, Inspection, Certification, Consultation and Training, Classification and Statutory Assurance | |

| By Sourcing | In-House Sourcing, Outsourcing | |

| By Application | Agriculture and Forestry, Consumer Goods, Healthcare, Financial Institutions, Building and Infrastructure, ICT and Telecommunications, Manufacturing, Mining, Oil and Gas, Power Utilities, Transportation and Logistics, Diversified Industrial and Public Services | |

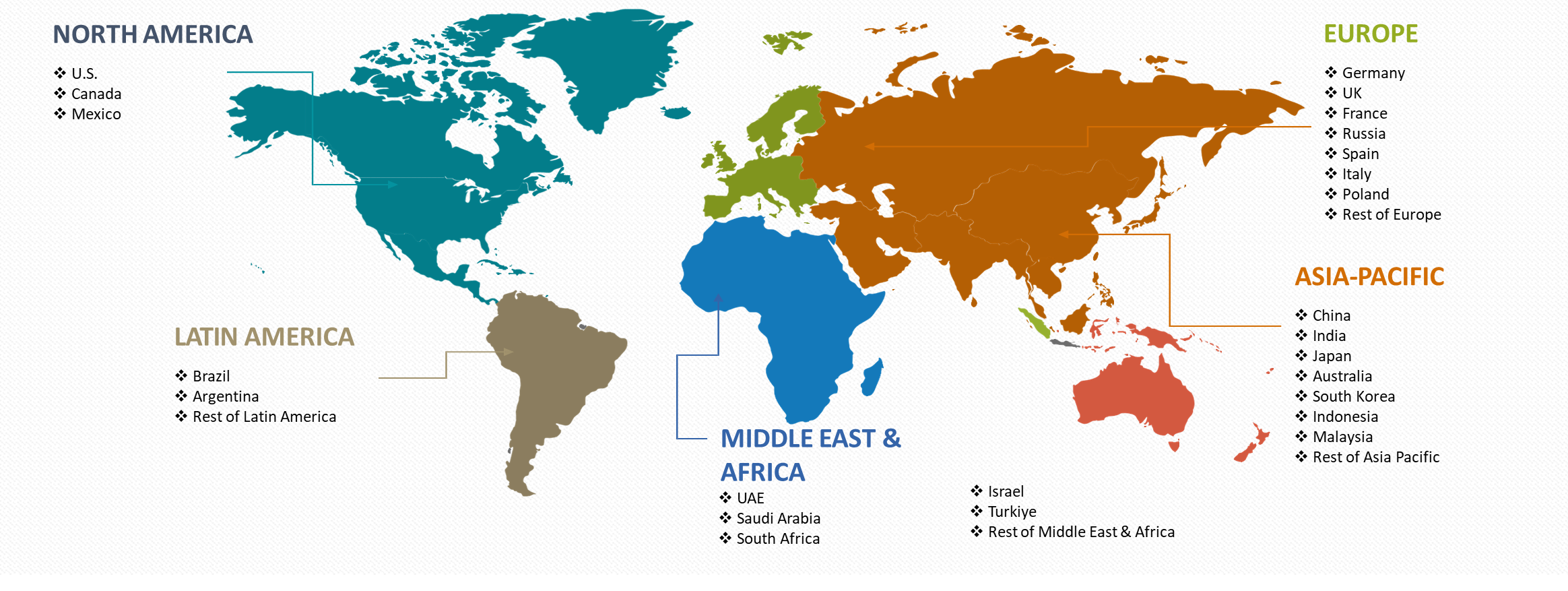

| By Region | North America | USA, Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Türkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Key Takeaways

- Service demand is becoming more recurring as companies move from one-time certification toward continuous supplier surveillance, product change control and digital evidence management.

- Testing remains the largest and most technically defensible service line because certification, inspection and market access decisions depend on accredited laboratory evidence.

- EV batteries, charging systems, heat pumps, grid storage and power electronics are creating higher value work that blends electrical, thermal, chemical, mechanical and software safety expertise.

- USA remains a priority geography because product liability exposure, FDA oversight, OSHA recognized testing routes and data center construction create durable assurance spending.

- Japan will attract investments owing to the increasing need for compliance-related services in the automotive, robotics, electronics, medical device and precision manufacturing industries.

- The testing of foods, nutraceuticals and pet foods will grow as there will be the need for contaminants screening, microbiology, allergens, suppliers' verification and labeling.

- Projects like data centers and semiconductor plants will lead to increased demand for commissioning, cleanroom validation, electrical inspection and construction QA services.

- Remote auditing, digital portals, sample tracking, and AI-enabled defect review will increase the efficiency in service delivery, hence setting a new level of expectation among clients.

- The acquisition of specialized laboratories will continue to be the most sought-after strategy of growth as qualifications and client relationships take time to develop.

- The verification of sustainability claims will move from general declarations to specific details such as emissions, chain of custody, recycled materials and product-level information.

- The lack of talent in testing areas, including batteries, cybersecurity, food chemistry and advanced material tests, will help retain premium pricing for top-notch firms.

- The existence of accreditation schemes in different countries and regional differences will keep creating challenges for exporters who require worldwide certification.

AI Impact

Digital Assurance and Laboratory Automation

AI is changing the operating model for assurance providers rather than replacing laboratory science. The strongest impact is visible in evidence processing, defect recognition, document review, scheduling, risk scoring and automated compliance mapping. In high-volume testing programs, AI can prioritize samples, flag abnormal results and reduce the time engineers spend on repetitive validation steps.

Computer vision is increasingly relevant for industrial inspection. Wind blades, pipelines, bridges, storage tanks, vehicle components and production lines create large image sets that are difficult to review manually. AI-based image analytics can identify corrosion, cracks, coating defects, weld irregularities and surface damage before an inspector prepares the final technical assessment.

Laboratories are also using AI to improve throughput. Automated sample tracking, predictive maintenance for instruments and anomaly detection in test outputs help reduce rework. In food and pharmaceutical testing, data integrity is critical, so AI tools must be deployed within controlled quality systems and supported by audit trails rather than informal analytics dashboards.

AI also creates new demand for the sector. Connected products, AI-enabled medical devices, autonomous vehicles, smart building systems and industrial software require assurance across cybersecurity, data governance, functional safety and model reliability. Assurance providers that combine physical testing with digital risk expertise will be better placed than providers focused only on legacy compliance checks.

Disruption Analysis

Software Defined Products and Sustainability Verification

Software defined products are reshaping the market because safety and compliance no longer end at the factory gate. A vehicle, medical device, industrial robot or connected appliance can change after launch through firmware updates. Assurance programs must therefore evaluate product architecture, update controls, cybersecurity exposure, data flows and ongoing performance monitoring.

Sustainability claims are creating a second disruption. Buyers, regulators and investors are challenging unsupported claims around recycled materials, emissions, responsible sourcing and product life cycle performance. Verification work is moving from broad ESG reports toward item-level evidence such as chain of custody, material content, factory energy data and supplier-level audit trails.

Provider economics are changing as well. Traditional field inspection remains important, yet higher margins are shifting toward specialized programs with data platforms, technical experts and repeatable certification frameworks. Providers that can turn fragmented compliance evidence into structured digital records will hold stronger pricing power.

White Space Opportunities

Multi-site assurance through digital platforms: Larger buyers desire to leverage one platform that will trace certificates, audit outcomes, lab test results, non-conformities, and any evidence offered by the supplier in a multi-country environment. A TIC provider with accredited services in combination with an efficient digital layer can create a shift from project-based engagements to a recurring compliance management model.

EV battery and energy storage safety programs: There is an unmet need in battery safety due to the breadth of services required to ensure safety, whether at the cell level, pack design, thermal runaway, charging behavior, transport, installation and fire safety risks. Service providers with their own unique chambers, chemistry analysis, and field inspections can secure premium opportunities in automotive, grid storage, and electrified buildings.

Data center commissioning and semiconductor facility assurance: Due to the hyperscale growth in data centers and the semiconductor manufacturing localisation trend, there is a growing need for inspection, cleanrooms, electrical assurance, and quality checks on critical facilities.

Cyber Physical Product Certification: Smart appliances, manufacturing plants, medical instruments, EV chargers, and industrial control systems require guarantees in terms of hardware safety, firmware upgrades, cybersecurity, and functionality. Testing companies can enhance their capabilities through developing cyber physical certification offerings. Product Claims Sustainability Verification: Purchasers are switching from generic ESG claims to concrete data about carbon emissions, recycled material, responsible sourcing, and chain of custody. Testing companies that have audit and lab capabilities can turn sustainability verification into recurring revenue.

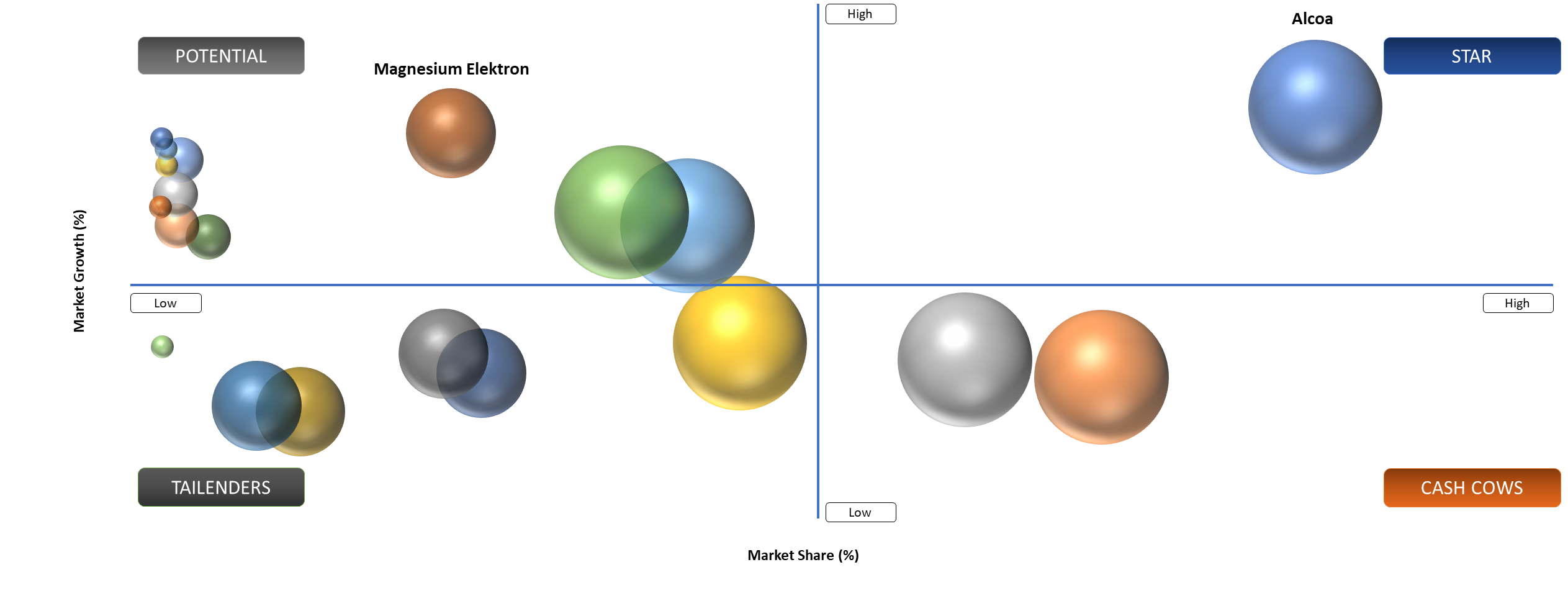

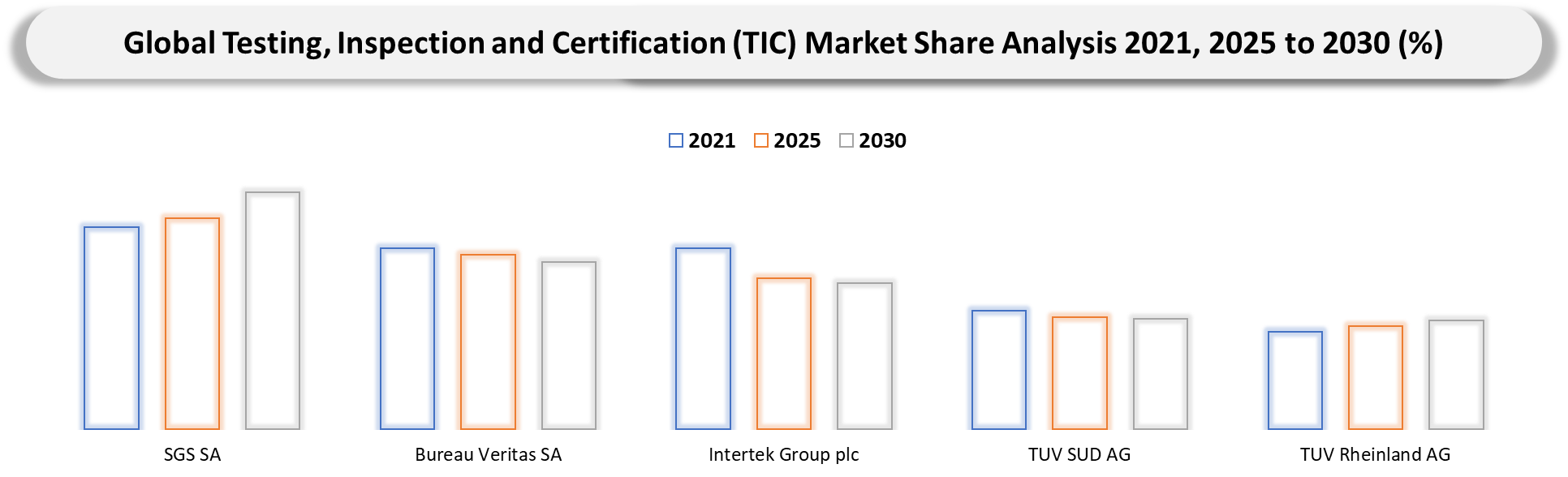

BCG Matrix: Company Evaluation

Stars include SGS, Bureau Veritas, Intertek, TUV Rheinland, DEKRA and UL Solutions because they combine global laboratory networks, recognized marks, diverse sector coverage and strong acquisition capacity. They are well placed in growth pockets such as EV batteries, electrical safety, cybersecurity, food testing, data center commissioning and sustainability verification. Strong brand trust helps them win multi-country contracts where buyers need harmonized assurance across factories and sales markets.

Potential companies include focused providers in EV battery testing, semiconductor cleanroom assurance, cyber physical security, advanced materials testing, food laboratory networks and digital inspection platforms. Many have smaller revenue bases than the global leaders, yet their technical concentration makes them attractive acquisition targets. Growth will depend on accreditation breadth, customer concentration risk and the ability to scale technical labor without diluting quality.

Market Dynamics

Regulatory Complexity and Product Electrification Expanding Outsourced Assurance

Regulation has become more detailed across product categories and geographies. USA workplace safety rules recognize private sector laboratories under the NRTL program for specific product safety standards. FDA food safety policy has moved toward prevention and accredited testing in selected situations. Japan uses JIS, PSE and product certification frameworks that require technical evidence and supplier discipline. Cross-border sellers need providers that can translate such requirements into practical test plans.

Electrification is a major growth layer. EVs, chargers, grid assets, battery storage systems, heat pumps and industrial power electronics require electrical, thermal, mechanical, chemical and software-related checks. Failure can trigger recalls, fires, insurance disputes or delayed infrastructure commissioning. Outsourced assurance helps companies manage technical risk while internal engineering teams focus on product development and production scale-up.

Fragmented Standards and Talent Scarcity Pressure Service Delivery

The market faces execution pressure from fragmented standards, country-level approval routes and shortages of experienced engineers. Similar products often require different documentation and test paths depending on destination market. Complex approval workflows can reduce speed even when testing capacity exists.

Talent scarcity is equally important. Battery safety, semiconductor facilities, medical device compliance, cyber physical security and advanced materials testing need specialized people who understand both standards and real operating conditions. Hiring and training cycles are long, so providers must balance growth ambition with quality discipline.

Segmentation Analysis

By Service

Testing Services Become the Core Growth Engine as Products Turn Digital and Safety Critical

Testing services represent the most prominent revenue pool because every certification, inspection program and market access route starts with reliable evidence. The segment covers mechanical, chemical, electrical, environmental, microbiological, performance, software and failure analysis testing. It is quantifiable because laboratories bill by sample, project, product family, approval scheme, method complexity and turnaround time.

Product complexity is lifting the value of testing. A modern vehicle component may involve lightweight materials, embedded software, sensors, electronics and thermal exposure. A food product may need microbiology, allergen checks, contaminant screening, shelf life validation and label compliance. A data center or semiconductor facility may require materials testing, cleanroom validation, electrical inspection and commissioning support.

Testing has also become more linked to launch timing. Delays in a certificate or failed sample can postpone retail listings, infrastructure handover, export clearance or medical device approval. Customers therefore prefer providers with recognized methods, broad accreditation and capacity redundancy across regions.

Digital laboratory operations are improving the segment. Automated sample registration, chain of custody systems, instrument integration and client portals reduce communication delays. Greater transparency also helps global quality teams compare results across factories and suppliers.

By Application

Electrical Safety and EV Battery Testing

Electrical safety and EV battery testing is one of the strongest sub-segments because electrified products combine high energy density, software controls and consumer safety risk. Services include abuse testing, thermal propagation checks, charging interface evaluation, insulation testing, electromagnetic compatibility, environmental exposure and pack level performance validation.

Demand comes from vehicle OEMs, battery cell producers, charger manufacturers, grid storage developers and component suppliers. Technical requirements are rising because batteries are being deployed in mobility, homes, commercial buildings and utility projects. Insurers and regulators now ask for clearer evidence around fire behavior, traceability and installation quality.

Laboratory investment is likely to remain high because battery tests require specialized chambers, safety systems and trained staff. Providers with integrated electrical, chemical and mechanical testing capabilities can handle more of the validation workflow internally, which improves customer retention and turnaround control.

Food Safety and Consumer Product Testing

Food safety and consumer product testing remain a steady sub-segment because regulatory pressure and brand protection needs do not weaken during economic cycles. Work includes microbiology, contaminants, nutrition labeling, allergens, packaging migration, toy safety, restricted substances, textile chemicals and household product performance.

USA food safety oversight continues to emphasize prevention rather than response. Importers and manufacturers increasingly need supplier verification and accredited laboratory evidence. Global retailers also impose private standards that may exceed local regulation, making third-party testing part of commercial access rather than optional quality control. Consumer product testing is shifting from single batch checks toward ongoing supplier surveillance. Online marketplaces, private label growth and fragmented sourcing make traceability difficult. Providers that combine lab testing, factory audits and digital product files can reduce recall risk and support faster market entry.

Geographical Penetration

North America Testing, Inspection and Certification Market Trends

North America leads due to its strict product liability environment, large industrial base, strong private standards ecosystem and high concentration of regulated sectors. The region combines advanced manufacturing, energy infrastructure, aerospace, healthcare, food processing and consumer product imports, all of which need formal assurance evidence.

Infrastructure renewal is creating project inspection demand across bridges, power networks, water assets, data centers and renewable installations. Buyers increasingly ask providers to support design review, commissioning, construction quality checks and operational inspection rather than one-off compliance certificates.

Technology customers are also raising demand. Data centers, semiconductor facilities, cloud infrastructure and connected device companies need assurance around construction quality, electrical systems, cyber risk, environmental performance and equipment safety. The LotusWorks transaction shows how mission-critical commissioning is becoming a TIC growth platform.

USA Testing, Inspection and Certification Market Landscape

USA is a priority market because compliance is deeply embedded in commercial risk management. OSHA recognizes NRTLs to test and certify specific products for workplace safety standards. FDA food safety policy has shifted toward prevention through FSMA, which increases demand for supplier verification, laboratory testing and documented control systems.

Large domestic markets for EVs, aerospace, medical devices, industrial equipment, data centers and food production make USA attractive for both global TIC leaders and specialist laboratories. Acquisition activity is especially active because buying accredited labs and experienced engineers can be faster than building a national network from scratch.

Another USA specific trend is the convergence of assurance with litigation risk and insurance requirements. Product recalls, battery fires, food contamination events and construction defects can create high financial exposure. Independent evidence from recognized providers helps manufacturers defend quality decisions and satisfy buyers who require formal compliance records.

Asia-Pacific Testing, Inspection and Certification Market Trends

Asia-Pacific is the fastest developing region because manufacturing scale and export exposure create constant demand for conformity assessment. China, India, Japan, South Korea and Southeast Asia supply automotive parts, electronics, chemicals, machinery, food products and consumer goods to global markets. Each export route brings specific testing and documentation needs.

Regional demand is moving beyond basic product checks. EV batteries, solar equipment, semiconductor supply chains, robotics, medical devices and smart infrastructure need advanced technical validation. Governments are also strengthening domestic standards and laboratory ecosystems to support industrial upgrading. Service delivery is becoming more localized. Customers prefer providers that can test near production sites, issue reports accepted by destination markets and support corrective actions before shipments move. Local capacity reduces delay and avoids costly retesting after goods arrive in final markets.

Japan Testing, Inspection and Certification Market Outlook

Japan is a high-potential market because precision manufacturing and safety culture make compliance a strategic requirement. The country has strong automotive, electronics, robotics, medical device, chemical and industrial machinery sectors. Products are often built for both domestic reliability expectations and export acceptance.

Japan Industrial Standards define criteria for product quality, performance, safety and test methods across many categories. PSE requirements for electrical appliances and materials place responsibility on suppliers and importers to meet technical requirements and maintain inspection records. Such frameworks create consistent demand for certification bodies, laboratories and technical advisors.

Japan also offers growth in advanced mobility and factory automation. Automotive OEMs and tier suppliers need validation for EV systems, automated driving components, lightweight materials and battery packs. Robotics and industrial equipment companies need functional safety, electrical safety, EMC and software-related assessment as products become connected.

Competitive Landscape

- The competitive landscape is led by global assurance groups with accredited laboratories, recognized certification marks, sector specialists and local inspection networks. Scale matters because customers increasingly want one provider to handle product testing, supplier audits, certification, sustainability verification, calibration and market access support across several countries. Specialist firms still hold strong positions in high complexity niches such as battery safety, forensic engineering, food chemistry, cybersecurity, semiconductor facility quality and mission-critical commissioning.

- Competition is becoming more capability-led. Providers are investing in digital reporting portals, automated laboratory workflows, remote inspection tools, AI-assisted defect review and sector-specific advisory services. Mergers and acquisitions remain active because accreditations, expert assessors, client trust and laboratory infrastructure are difficult to replicate quickly.

Key Developments

- April 2026: Bureau Veritas signed an agreement to acquire LotusWorks, strengthening its position in data center commissioning, semiconductor facility support and mission-critical quality assurance.

- April 2026: TUV Rheinland opened an Automotive Component Testing Laboratory in Manesar, expanding precision testing and international compliance support for next-generation mobility programs.

- March 2026: SGS acquired Murray-Brown Laboratories in Denver, expanding food, pet food and nutraceutical testing capacity in North America.

- February 2026: Intertek ETL agreed to acquire QTEST in Colombia, adding electrical product testing, medium and high voltage testing and certification services for Latin American customers.

- January 2026: SGS completed the acquisition of Applied Technical Services, adding specialized testing, inspection, calibration and forensic engineering depth in the USA.

- November 2025: Intertek acquired Professional Testing Laboratory in the USA, improving its flooring and construction product testing capability for North American customers.

- September 2025: Merieux NutriSciences completed the global acquisition of Bureau Veritas food testing activities, expanding its laboratory network and food safety service reach.

- July 2025: SGS signed a definitive agreement to acquire Applied Technical Services, showing how USA technical assurance assets remain central to consolidation strategy.

- May 2025: TIC Council held its annual summit in Brussels, with digitalization, trust in quality infrastructure and industry collaboration as central themes.

- February 2025: Merieux NutriSciences completed the acquisition of Bureau Veritas food testing activities in Japan, Morocco, Southeast Asia and South Africa.

- December 2024: Global assurance providers increased investment in battery, EV charger and energy storage testing capacity as electrification programs shifted toward commercial launches.

- October 2024: TIC companies expanded cybersecurity, software assurance and connected device compliance services as regulators increased attention on digital product risk.

- June 2024: Food, nutraceutical and pet food brands expanded accredited laboratory testing and supplier verification programs due to tighter retail and consumer scrutiny.

- April 2024: Infrastructure owners and contractors increased reliance on third-party inspection for data centers, renewable projects and high-voltage electrical systems.

DMI Opinion

According to DataM, the TIC market is entering a more strategic phase where independent assurance is no longer treated as a final approval step. Buyers want evidence that protects revenue, improves supply chain resilience and supports faster entry into regulated markets. Strong providers are moving closer to customer design, procurement and production teams because compliance decisions now affect launch timing, vendor selection and brand risk.

The most attractive growth pockets are tied to technical complexity. EV batteries, charging systems, grid storage, data centers, semiconductor facilities, medical devices, food safety and connected products require testing that blends standards knowledge with laboratory depth. Providers with multidisciplinary teams can capture higher value work because customers prefer one accountable partner across electrical, chemical, mechanical, software and documentation requirements.

USA remains a priority country because litigation exposure, federal agency oversight, high consumer product volumes, food safety enforcement and accelerated data center construction create durable demand for accredited services. Japan also deserves stronger attention because exporters need credible evidence for automotive, electronics, robotics, healthcare and precision manufacturing supply chains. Both countries reward providers that combine local accreditation with global market access support.

Digital tools will improve delivery speed but will not remove the need for recognized expert judgment. AI-assisted image review, automated laboratory scheduling, remote audits and client portals can reduce cycle time. Final purchasing trust still depends on accreditation, traceable methods, inspector competence and defensible documentation. Leading companies will use digitalization to strengthen evidence quality rather than replace technical review.

Consolidation should continue because acquisitions give immediate access to accreditations, scientists, inspectors, regional customers and specialized laboratories. Smaller laboratories with strong niches in food chemistry, battery abuse testing, cybersecurity, materials testing and forensic engineering may attract interest from larger groups seeking faster capability expansion.

Pricing power will remain strongest in services where failure cost is high. Battery safety, medical device testing, data center commissioning, high voltage testing, food contaminant screening and sustainability verification carry greater commercial consequences than routine checks. Providers that can document technical reliability and shorten approval timelines should defend margins better than commodity inspection firms.

Talent availability is becoming a structural constraint. Growth in advanced testing categories depends on engineers, chemists, auditors, cybersecurity assessors and sector experts who understand both regulations and customer operations. Companies that invest in training, knowledge management and standardized delivery models will be better placed to scale without compromising audit quality.

Over the forecast period, the winners will likely be providers that combine global reach with sharper specialization. A broad footprint helps multinational customers reduce vendor complexity. Sector depth helps solve high-value problems. Market leadership will depend on the ability to offer trusted evidence, fast turnaround, consistent quality and credible advisory support across both mature and fast-changing compliance categories.

Why Choose DataM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

Target Audience

- Certification Bodies and Accredited Laboratories: Global and regional TIC providers looking to benchmark service portfolios, accreditation coverage, sector specialization and expansion opportunities across testing, inspection, certification, auditing and calibration services.

- Manufacturers and Exporters: Automotive, EV, electronics, consumer goods, food, medical device, industrial equipment and chemical companies that need market access support, supplier verification and product safety validation across multiple countries.

- Infrastructure and Construction Companies: EPC contractors, data center developers, power project owners, utilities, bridge operators, tunnel developers and public works agencies using inspection, commissioning and quality assurance to reduce project delay and operational risk.

- Food, Agriculture and Retail Companies: Food processors, ingredient suppliers, private label owners, retailers and importers seeking microbiology testing, allergen checks, contaminant screening, packaging migration support and supplier audit programs.

- Energy, Utilities and EV Ecosystem Players: Battery makers, charging equipment suppliers, renewable energy developers, grid operators and storage system integrators needing electrical safety, field inspection, asset integrity and performance verification.

- Healthcare and Life Sciences Companies: Medical device manufacturers, pharmaceutical suppliers, diagnostic companies and healthcare product exporters requiring quality system support, laboratory testing and regulatory documentation.

- Investors and Private Equity Firms: Investment teams tracking laboratory rollups, accredited testing capacity, data center commissioning platforms, sustainability verification providers and specialist TIC acquisition targets.

- Government Agencies and Regulators: Public authorities, customs bodies, product safety agencies, infrastructure departments and standards organizations evaluating third party assurance capacity and compliance readiness.