Telemedicine Software Platforms Market Overview

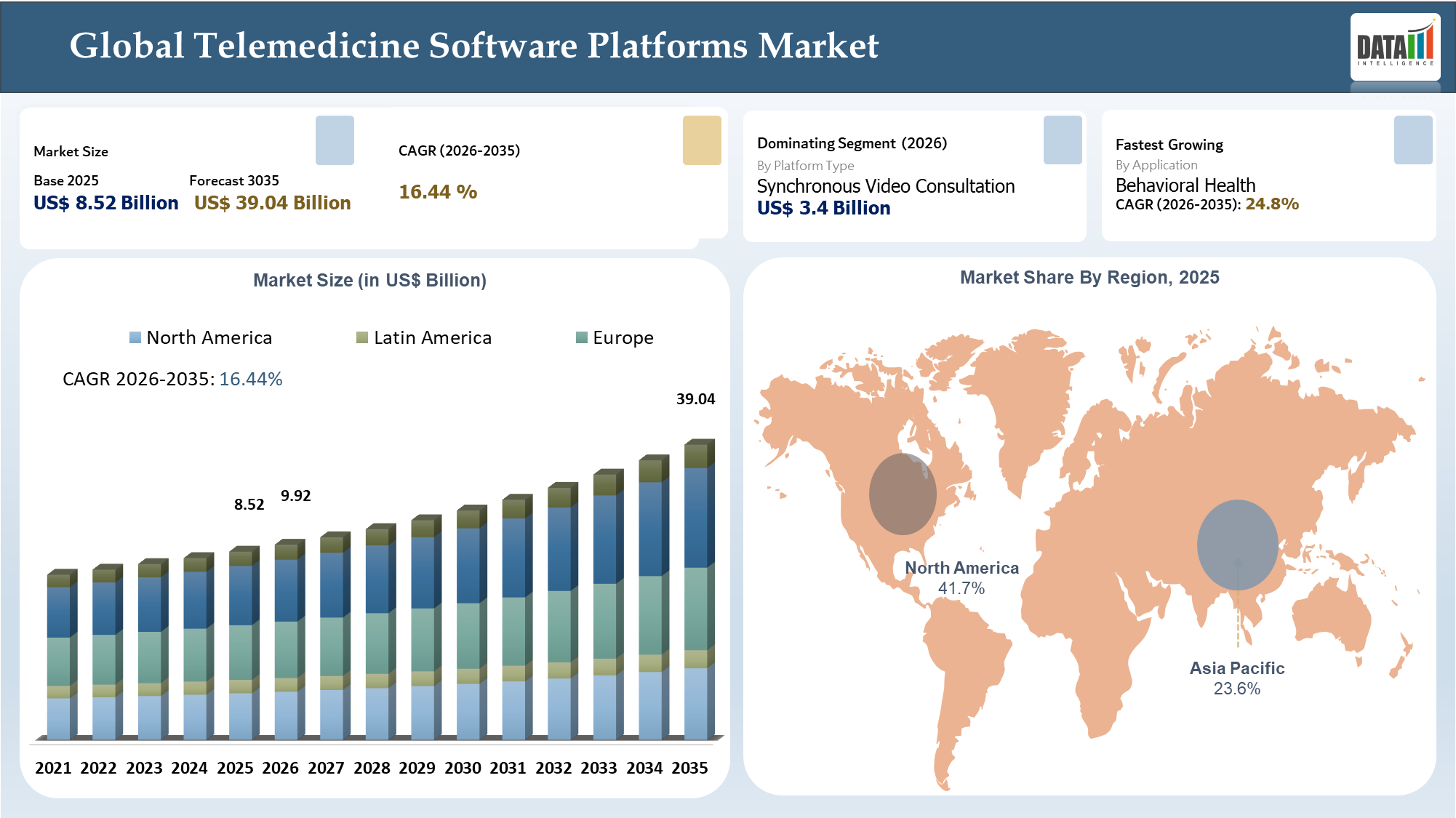

The global telemedicine software platforms market reached US$ 8.52 billion in 2025 and is expected to reach US$39.04 billion by 2035, growing with a CAGR of 16.44% during the forecast period 2026-2035. According to analysis from DataM, the telemedicine software platforms market is not characterized by general demand themes. Instead, there are certain operational realities in play: successful platforms will not be based simply on video capabilities but will have to show reimbursement workflow, EHR compatibility, scheduling functionality, and provider acceptance. Similarly, virtual visits are being used for chronic disease management, remote triage, and specialty access rather than simply as replacement visits. In doing so, these dynamics change the criteria on which suppliers base their value propositions, how potential customers evaluate their options, and the cases in which premium pricing can still be justified.

According to DataM, the competitive dynamic is shifting from product availability to execution. Indeed, in this marketplace, payers and providers are increasingly likely to choose solutions based on their ability to cut no-shows, route traffic effectively, and retain customers in their programs. Such a dynamic results in a selective environment that favors vendors who are able to demonstrate implementation excellence, channel strength, or applicability relative to other vendors who focus exclusively on general market awareness. Demand may be strong, but share movement will depend increasingly on credibility.

AI Impact Analysis

In the telemedicine software platforms market, AI is beginning to have an impact on the commercial landscape through other channels, including design optimization, process control, predictive maintenance, quality analytics, and demand sensing. This will affect the development, production, and post-sales support of products, resulting in improved performance rather than a new product category.

The buyer benefit will occur when the AI solution leads to savings on cost, improvement on time, increased accuracy in diagnosis, or reduced error in operations. Providers of telemedicine software platforms that offer solutions in which intelligence is built into the product and complemented by service information are creating defensible business relationships beyond product specification competition.

Commercialization is another aspect impacted by AI in the telemedicine software platforms market. Sales departments can now offer simulation, configuration, and usage analysis services to clients, whereas post-sales departments rely on performance analytics to enhance their strategies for renewals, parts, and services.

Telemedicine Software Platforms Industry Trends and Strategic Insights

- Applications is by far the most commercially relevant perspective as it helps understand how buyers prioritize their spending, compare vendors, and view trade-offs when it comes to telemedicine software platforms.

- The focus is gradually moving away from platforms that can generate evidence of success through Behavioral Health and Chronic Care Management applications.

- The North American region is leading the way competitively with USA and Canada dictating the design, procurement, and go-to-market strategy of product offerings.

- The most successful players are leveraging product strength, application experience, and ecosystem connections to maintain pricing leverage and accelerate buyer decision processes.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 8.52 Billion | |

| 2035 Projected Market Size | US$ 39.04Billion | |

| CAGR (2026-2035) | 16.44% | |

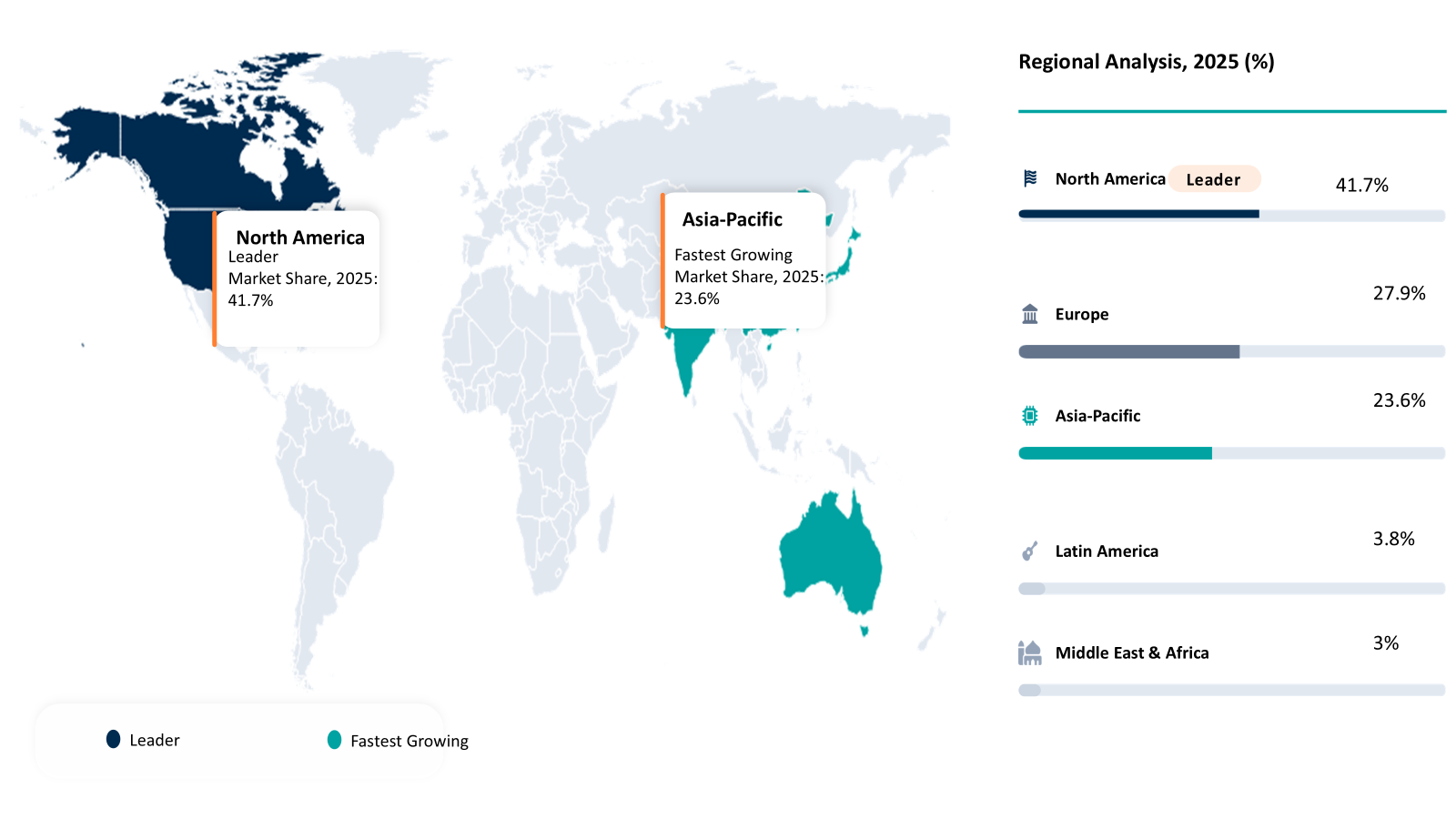

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Platform Type | Synchronous Video Consultation, Asynchronous Virtual Care, Remote Monitoring Integrated Platforms, Specialty Telemedicine Platforms | |

| By Deployment Model | Cloud, On Premises, Hybrid | |

| By Application | Primary Care, Behavioral Health, Chronic Care Management, Post Acute Follow Up, Dermatology and Specialty Care | |

| By End User | Hospitals, Clinics, Payers, Employers, Digital Health Providers | |

| By Business Model | Subscription, Per Encounter, Enterprise License, Payer Contract | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Disruption Analysis

Shift from Feature-Based Selling to Outcome-Driven, Ecosystem-Led Telemedicine Platforms

The primary disruption in telemedicine software platforms lies not in any particular product release, but in the shift of the market from feature specification to measurable operational performance. The salespeople can no longer afford to speak in terms of spec sheets or high-level innovation buzzwords when their clients are concerned with how quickly and effectively the software integrates with current infrastructure, performs at scale, and delivers return on investment.

The next disruption in this market is commercial. Partnership models, integration strategies, and bundled offerings are altering the customer criteria for narrowing down supplier options. In many instances, the vendor with control over the supporting ecosystem can win the deal, despite similar core software functionality of its competitor.

The telemedicine software platforms market is experiencing a disruption of increasing scrutiny of resilience and accountability. Clients are becoming more interested in knowing where the product is manufactured, who provides local support, how the supplier reacts during shortages, and how results are assessed post-installation.

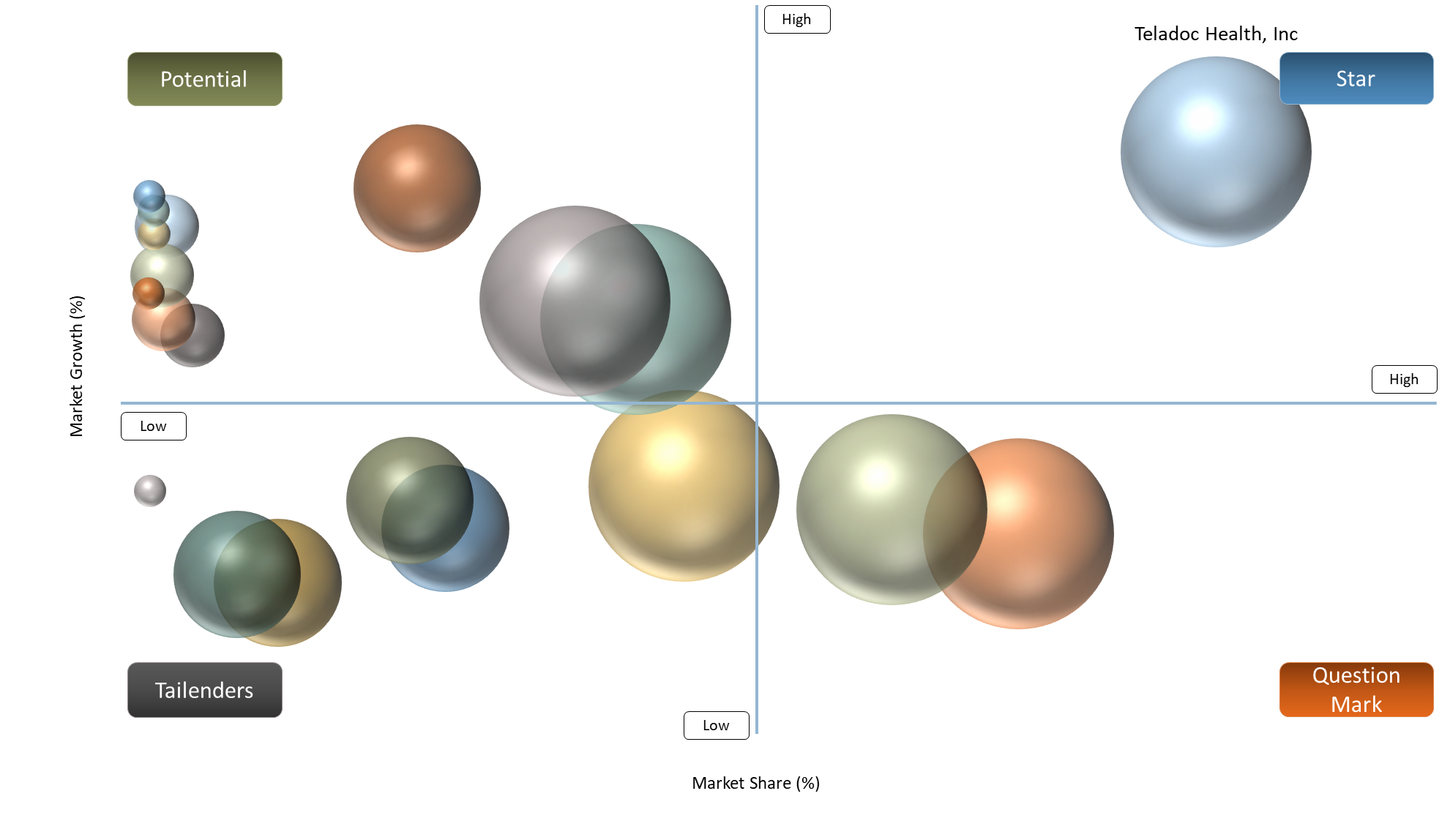

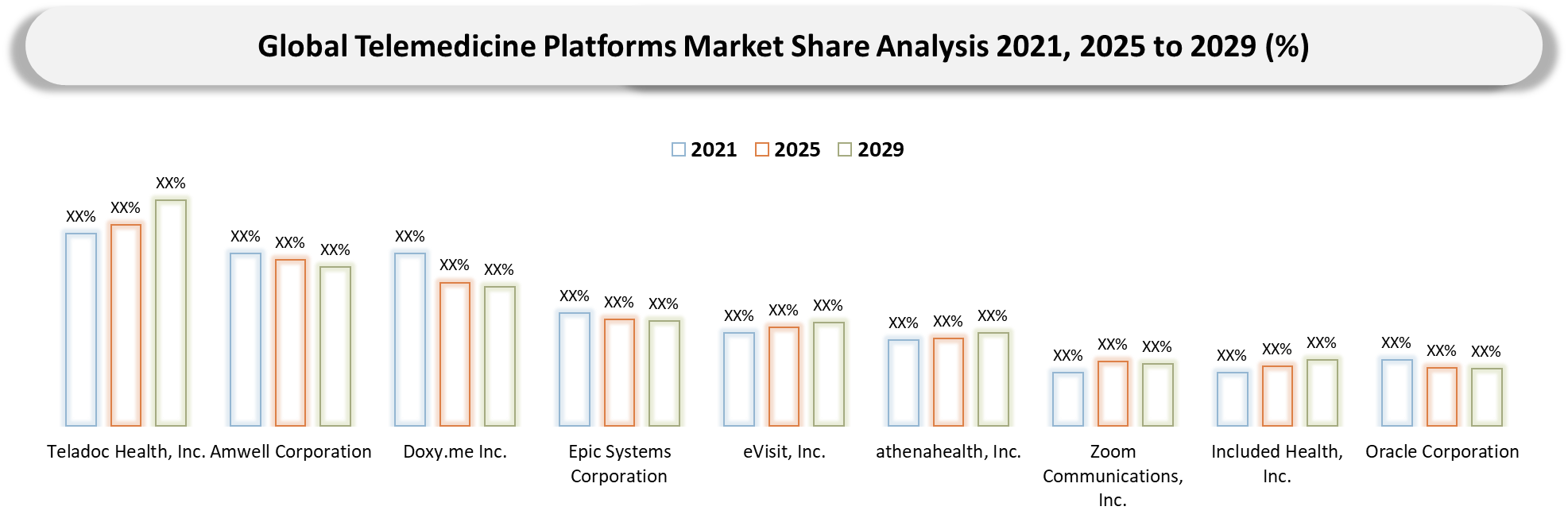

BCG Matrix: Company Evaluation

Stars under BCG terminology are the companies that have high demand momentum along with ecosystem strength in the telemedicine software platforms industry. This category includes Teladoc Health, Inc., Amwell Corporation, Doxy.me Inc., Epic Systems Corporation, and Doctolib SAS, owing to their broad platform footprint, platform integration, and account expansion capability.

Cash cows refer to those scale-enabled players that leverage their installed base, contractual durability, and operational stickiness despite the fact that their growth rates are not comparable to other categories. Examples of these types of organizations include Oracle Corporation, athenahealth, Inc., Zoom Communications, Inc., Koninklijke Philips N.V., and Medtronic plc.

Question marks are companies with niche differentiation but lack ecosystem reach and enterprise penetration. This category includes eVisit, Inc., Included Health, Inc., Wheel Health, Inc., Carenet Health, Inc., Mend Technology, Inc., Ada Health GmbH, and Twilio Inc.

Market Dynamics

Shift toward measurable operating value and application specific buying criteria

Another key source of growth in the telemedicine software platforms market involves the transition from generic interest in a product category to targeted purchases that will produce concrete improvements. In today’s world, customers are searching for technology that can help increase throughput, improve quality, reduce turnaround times, ease labor demands, or enable a new service approach.

However, an even deeper level of demand comes from the process of evaluating vendors, where technical capabilities are not the only criterion used to winnow the list. Instead, procurement officers consider deployment challenges, support, regulatory readiness, complexity of integrations, and evidence about cost reductions or efficiencies that may have been offered. The resulting tendency is for budgets to become concentrated in segments that have better proof points, such as Behavioral Health and Chronic Care Management.

The growing maturity of the overall ecosystem represents another reason why the market can grow. As more organizations find ways to procure the supporting elements needed to take advantage of technology – including surrounding applications, integrators, connections, and manufacturing resources – they will be willing to make the purchase.

Finally, end users have grown increasingly intolerant to solutions that leave them with additional tasks after deployment. They need products that will be compatible with current infrastructure and scalable without further redesigning. This has been driving the need for better-quality service providers.

Integration burden, compliance friction, and longer enterprise decision cycle

The key limitation within the telemedicine software platforms industry is the disconnect between customer demand and rapid implementation. Numerous organizations encounter difficulties such as integration challenges, validation requirements, limitations in data or process flow, and procurement procedures that may prolong the process despite an appealing business proposition.

This issue becomes apparent in situations where the offering interacts with regulated processes, capital expenditure, existing technology infrastructure, or requires approvals from multiple parties. Companies that fail to recognize this aspect tend to overestimate the conversion rate of pilot projects into actual sales.

Segmentation Analysis

The global Telemedicine software platforms market is segmented based on the platform type, deployment model, application, end user, business model, and region/countries.

Application-Led Differentiation Is Reshaping Telemedicine Platform Economics

Application remains the best framework for making sense of the telemedicine software platforms market because it reflects actual buyer decision making about trade-offs versus a vendor’s marketing of its entire suite of products. Market size calculations aside, budgeting, price leverage, supplier differentiation, and implementation risks are all much more apparent in terms of this segment. It is also, among others, the easiest segment to analyze because actual purchase behavior, product offering and applicability is far easier to discern than the abstraction that goes on in strategic discussions.

Two particular subsegments within this larger telemedicine software platforms market deserve special consideration based on their commercial relevance and the reason why they get the advantage over one another. The first always derives from economies of scale, experience or integration, while the other from greater control, performance or fit within the particular use case scenario. This difference is precisely the reason why these two particular subsegments are meaningful in market research and consulting contexts.

Behavioral Health is still relevant in situations where the customer does not need to change the whole operation system to integrate it into its workflow. In other words, there is no need for additional expenses or changes in partners, which is another reason why the buying process does not get complicated. As practice shows, the early market development stage favors this sub-segment because everything is easier to implement.

Commercially speaking, it is always better if suppliers are able to combine Behavioral Health with some additional services that would make it easier for customers to use and close deals. This solution will prove to be extremely attractive in situations when the customer wants to see results quickly despite understanding that there may be other products in the future.

As mentioned above, there are certain situations when customers are more concerned about controlling the work and functionality of the solution. In such cases, Behavioral Health loses its competitive edge if the vendor cannot demonstrate better workflow fit and post-deployment support. That is why industry leaders continue developing it with additional services in mind.

Whereas Chronic Care Management generally receives consideration when traditional solutions fail to meet the mark in terms of visible deficiencies. Consumers gravitate towards this solution when control, efficiency, and compatibility with their processes and specialized products are at stake. Revenue may take longer to develop, but the account will be worth more as the customer is tackling a greater issue and won’t necessarily be purchasing on price.

The first key advantage offered by Chronic Care Management is that it offers the opportunity for competitive repositioning. The reason is that suppliers who succeed in this realm end up not being vendors, but partners who can play a role in determining design, process, and future direction. This shifts the discussion from product similarity to ownership of results, which is critical for premium market positioning.

The most helpful perspective from a consulting standpoint would be the one where neither of the two segments replaces each other. Rather, what typically happens is that both segments exist together, but their ratio changes over time. In Behavioral Health, there tends to be greater volume and quicker onboarding, whereas Chronic Care Management caters to the high-end market.

Geographical Penetration

North America Is Setting the Competitive Tempo for the telemedicine software platforms markets

A case could be made for North America, as a top priority region in the telemedicine software platforms market, in that it is seeing shifts that go beyond the hype and into actual operation. Changes in procurement, financing, compliance requirements, and distribution dynamics indicate that this market is not only ripe with opportunities but can also serve as a bellwether of revenue concentration and competition down the road. There seems to be a shift from emergency-induced uptake of virtual care solutions to a selectivity phase driven by alignment with provider workflows, chronic disease care requirements, orchestration of care delivery, and asynchronous engagements beyond simply video consultations.

The United States should get special attention because, at least from an innovation category standpoint, it typically drives category directions owing to sheer size and challenging buyer conditions. In other words, buyers have become quite selective as to whether a product aligns with local costs, implementation possibilities, service expectations, and quantifiable return on investments. As such, commercial success will likely depend on coordination within the ecosystem of solution implementation and complementary health technologies, as well as reducing patient leakage, improving access to behavioral health services, and boosting physician productivity.

Another sign is that of Canada. Geographical factors still strongly influence telehealth initiatives, whereas procurement leans towards interoperability and the ability of the telehealth system to be in sync with the overall public health system.

U.S. Telemedicine software platforms market Trends

This market deserves close examination since it is currently being driven by true changes in operations rather than just by rising demand. The procurement process has become more systematic, with buyers assessing platforms not only according to their integrability with current health IT infrastructure, alignment with reimbursement approaches, and readiness to implement extensive clinical workflows but also based on other key criteria.

U.S. buyers have become increasingly demanding and results-oriented in recent years. They look for telemedicine platforms capable of quick implementation, proven track record of successful operation in the field, and positive ROI. Generic offerings characterized by a wide range of features are rapidly losing their appeal due to the need for solutions that fit into local economic realities, regulatory frameworks, and technical standards.

Success of any commercial endeavor in the US now depends very much on the strength of the ecosystem. Companies which are able to combine their implementation strategies, compliance, and service delivery with collaboration between the vendors, insurers, healthcare providers, and technology partners are gaining an edge. Requirements are focused on those places where telemedicine will allow for reduced leakage, increased access to behavioral health services, and increased physician efficiency.

Canada Telemedicine software platforms market Outlook

In Canada, there is a unique and strategically relevant growth path for the telemedicine software platform market that depends on the country’s geography, healthcare organization, and policies that govern its implementation. The market in Canada is very much determined by the need to increase access to healthcare services among remote and underserved territories, thus rendering telemedicine as an integral part of the overall healthcare system. Procurement in Canada is different from that of the US, in that it relies less on the private sector and, consequently, on innovations, and is more concerned about data security and compliance.

For buyers in Canada, the key criteria are seamless integration with the current infrastructure and proven improvements in access and results. There is little interest in further developing features; instead, vendors must prove the stability and effectiveness of their technology. Also, there will be provincial requirements that must be adhered to.

Among promising areas for the Canadian market, one can mention chronic disease management, mental health services, and remote patient monitoring. In addition, the country shows promising signs of being an incubator for innovative premium solutions..

Competitive Landscape

- The competitive dynamics of the telemedicine software platforms market have shifted towards a dichotomy of scale between platform providers on one hand, and specialists, on the other. Leading companies like Teladoc Health, Inc., Amwell Corporation, Doxy.me Inc., Epic Systems Corporation, Oracle Corporation, eVisit, Inc., athenahealth, Inc., Zoom Communications, Inc., Included Health, Inc., and Doctolib SAS create market standards based on their wide-ranging platforms, enterprise-wide coverage, integrations, and access. On the other hand, smaller players and specialists compete on their quick time-to-deployment, suitability for specific workflows, deep use-case expertise, and delivery models. With increasing maturity, competitive differentiators have moved away from mere availability of telemedicine services, and towards implementation capability, interoperability, service support, and tangible value delivery.

- Given the competition among vendors to enhance the user experience throughout the healthcare process, positioning in the market is not just about having a good product, but it also involves the speed of onboarding, integration, data management, workflow facilitation, clinical usability, and platform management. Firms that have a strong position in high-demand products like behavioral health, chronic care management, follow-up care, and care coordination can better maintain their price structure and grow their market share.

Key Developments

- January 2025: Teladoc Health, Inc. expanded its enterprise care ecosystem through a collaboration with Amazon’s Health Benefits Connector, strengthening access to chronic condition programs and reinforcing higher-value platform partnerships.

- January 2025: Amwell Corporation sharpened its clinical programs portfolio by adding Vida, strengthening its chronic care and healthy living positioning for payer and provider customers.

- March 2025: Teladoc Health, Inc. expanded connected care partnerships across specialty care, digestive health, fertility, and family building, highlighting the market shift toward ecosystem-led virtual care models.

- April 2025: Teladoc acquired UpLift, expanding covered mental health access and signaling stronger investment in behavioral health-oriented offerings.

- July 2025: Teladoc launched Wellbound EAP, reflecting stronger commercialization around workforce mental health and higher-value employer demand.

- February 2025: Market leaders placed greater emphasis on hybrid care, chronic care management, and platform breadth rather than standalone virtual visit functionality.

- August 2024: Competitive pressure intensified around performance, reliability, and business model discipline as vendors faced tougher scrutiny on sustainable value delivery.

- October 2024: Vendors accelerated focus on chronic care and virtual program ROI, especially in obesity and long-term care related use cases.

- December 2024: Partnerships across infrastructure, software, and service layers gained importance as vendors pursued faster deployment, smoother integration, and lower adoption friction.

DMI Opinion

As per DataM's findings, instead of questioning whether or not demand for telemedicine software platforms exists, it may be more relevant to consider which firms have managed to turn interest into sustainable revenue without making implementation any harder relative to their value propositions. In other words, the market seems to reward those players who are making virtual care work operationally. From our standpoint, healthcare systems, payers, and employer-based organizations will increasingly be considering workflows, compatibility, efficiency, patient retention, and results when picking telemedicine platforms.

According to DataM, many parties participating in this market continue to overrate product stories and underrate implementation considerations. In fact, telemedicine platform selection appears to be becoming more about interoperability, funding, data management, fast onboarding, and customer service. Firms betting on implementation and support-related aspects rather than visibility and scale alone are more likely to win.

From our standpoint, successful businesses will likely be the ones that have managed to align their products, commercial strategies, and partner ecosystems with specific buyer decision-making processes.

Why Choose DataM?

- Technological Advancements: Explains the latest technological innovations in the telemedicine software platforms market, which includes the evolution of telemedicine software platforms and their integration with EHRs and medical devices, along with other technologies such as artificial intelligence (AI), cloud computing, blockchain technology, and big data analytics.

- Market Positioning of the Key Companies: Determines the market positioning of leading vendors within the telemedicine software platforms market based on the analysis of crucial parameters such as platform scalability, integration capability, user-friendliness, compatibility with clinical workflows, customer profile, enterprise-level offerings, and adaptability to various care settings.

- Applications of Telemedicine Software Platforms: Demonstrates how telemedicine software platforms are employed in actual settings, including virtual visits for primary care, behavior health consultations, chronic disease management, follow-up visits, post-discharge care, and specialist visits. Examples highlight applications like seamless care coordination, reduced need for hospital visits, and increased access to healthcare services.

- Market Trends and Dynamics: Highlights some of the latest industry trends, such as the adoption of hybrid models of care, increasing preference for asynchronous care, growing remote monitoring services, collaboration between payers and providers, and rising demand in North America, Europe, Asia-Pacific, China, India, and Canada.

- Strategies of Competitive Players: Deals with the competitive strategies adopted by market players for increasing their market share with the help of platform expansion, ecosystems, interoperability, enterprise deal-making, workflow improvements, and special virtual care solutions.

- Pricing and Market Accessibility: Includes details on the modes of pricing in the market for telemedicine software platforms such as subscription-based pricing, pricing per provider, enterprise pricing, implementation costs, integration costs, and service support costs. It further includes regional aspects related to reimbursement access and regulatory compliance.

- Market Penetration and Growth: Identifies the areas where telemedicine software providers can explore for entering new markets. This section identifies the expansion strategies that help organizations grow their market presence and scale-up their operations in the future.

Target Audience 2026

- Corporate strategy & market intelligence teams: Teams analyzing growth opportunities, competitive dynamics, demand trends, and regional expansion prospects in the telemedicine software platforms market.

- Corporate development teams: Executives looking at new partnerships, target buyers, healthcare partner opportunities, and growth prospects within the virtual care ecosystem.

- Commercial teams: Salespeople focusing on buyer identification, account planning, channel strategy, customer acquisition, and market solution positioning.

- Venture capital & PE firms: Investment professionals considering the attractiveness of the market, scalability of solutions, revenue transparency, consolidation trends, and return potential.

- Procurement teams: Purchasing executives considering platform providers' integration capabilities, service quality, implementation preparedness, compliance standards, and lifecycle value.

- Technology and operations executives: Teams handling the implementation and integration process, performance and interoperability, workflow design, security, and health system integration.

- Strategy consulting & advisory services: Consultants helping organizations with strategies to enter the market, benchmark analysis, digital health strategy, partnership models, and growth plans.