Tapioca Starch and Derivatives Market Overview

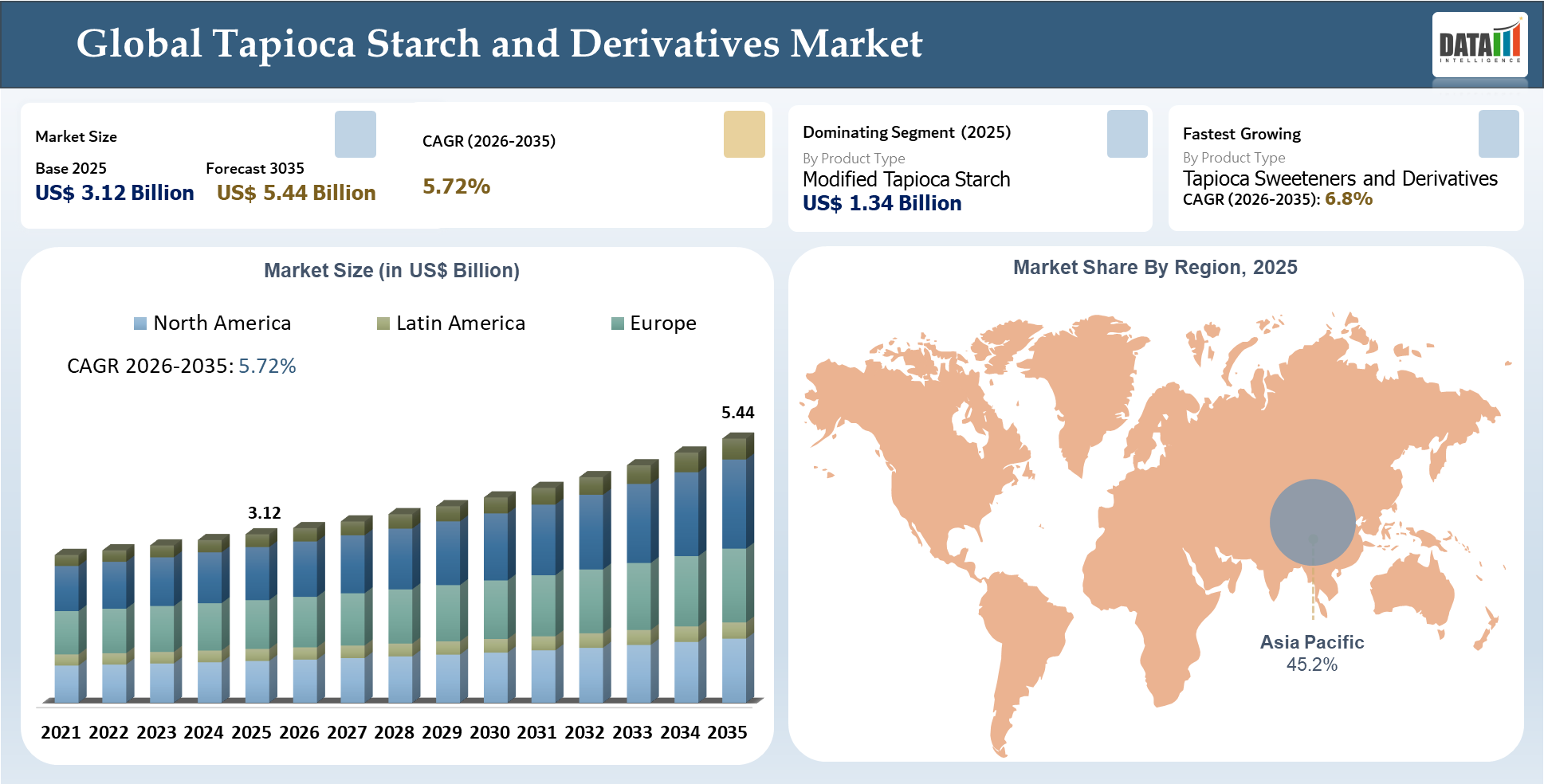

The global tapioca starch and derivatives market stood at US$ 3.12 billion in 2025 and is projected to reach US$ 5.44 billion by 2035, growing at a CAGR of 5.72% during the forecast period 2026-2035. There is vigorous growth in the market because of the shift from commodity applications of tapioca derivatives to industrial, functional, and clean-label applications. Tapioca starch obtained from cassava roots is increasingly sought after because of its flavor-neutral, gluten-free, highly viscous, and easily digestible nature that can be used in different industries.

The demand growth is fueled by the need for food manufacturers to alter their recipes to match consumer tastes for natural and allergy-friendly ingredients. The use of tapioca starch and derivatives is popular in sauces, soups, baked goods, snacks, dairy substitutes, noodles, frozen food products, and pre-cooked meals. Tapioca starch can improve consistency, shelf-life, water retention, and stability in these applications. There is robust business growth for modified tapioca starches owing to their process tolerance, freeze-thaw stability, acid stability, and rheology control advantages over native starches.

In addition to the food industry, other applications in the form of pharmaceuticals, adhesives, textiles, paper coatings, cosmetics, biodegradable packaging, and bioplastics have become the new focus for tapioca derivatives. In these sectors, tapioca derivatives find applications in binding, coating, disintegration, film formation, and materials substitution for sustainability purposes. The Asia Pacific region dominates both the supply and consumption of tapioca derivatives, owing to the high availability of cassava crops in Thailand, Vietnam, Indonesia, China, and India. The ability to modify tapioca derivatives, secure stable supplies of raw materials, export capabilities, regulatory compliance, and provision of application-specific customer support will be crucial for competitive advantage.

AI Impact Analysis

AI is slowly transforming the global tapioca starch and derivatives market by improving cassava procurement, starch manufacturing, quality control, and demand forecasting processes. At the beginning stage of production, AI can assist processors in managing cassava growth, yield expectations, disease occurrences, and harvesting periods to minimize uncertainties regarding the supply of raw materials. During manufacturing, AI technology can facilitate process optimization in relation to moisture content, viscosity, temperature, drying capacity, and modification factors in both native and modified forms of tapioca starch.

Furthermore, ingredient providers can utilize AI to assist clients in choosing the appropriate tapioca starch derivatives based on their required physical properties such as texture, stability, mouthfeel, and binding or clean label requirements. Predictive analytics can aid in optimizing pricing, inventory management, and export decisions by analyzing available crop information, logistics expenses, consumer demand, and trade flows within specific regions. AI technologies can play a significant role in quality assurance through batch variability reduction and compliance with traceability requirements.

The implementation of AI technology in the market is hindered by low digitization levels among tapioca starch manufacturers. Therefore, companies combining AI with processing expertise, farmer connections, and end-use support can better manage quality, cost, and custom formulation.

Tapioca Starch and Derivatives Market Key Takeaways

- Product Type remains the most commercially relevant framework for analysis, as it shows how demand is split across native tapioca starch, modified tapioca starch, tapioca sweeteners and derivatives, tapioca fiber, tapioca protein and others.

- Modified tapioca starch and other value-added tapioca derivatives have seen increased demand because of the tangible advantages they confer in terms of functionality, viscosity, freeze/thaw stability, binding properties, and processability.

- The Asia Pacific region dominates the market owing to favorable conditions such as large-scale cassava production, processing facilities, and export-oriented tapioca starch manufacturers in Thailand, Vietnam, Indonesia, China, and India.

- Successful players are characterized by their ability to procure raw cassava, modify tapioca starch, deliver quality, comply with food safety standards, and distribute globally.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 3.12 Billion | |

| 2035 Projected Market Size | US$ 5.44 Billion | |

| CAGR (2026-2035) | 5.72% | |

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Product Type | Native Tapioca Starch, Modified Tapioca Starch, Tapioca Sweeteners and Derivatives, Tapioca Fiber, Tapioca Protein and Others | |

| By Modification Type | Physical Modification, Chemical Modification, Enzymatic Modification and Dual Modified Starch | |

| By Functionality | Thickening Agent, Stabilizer, Binder, Texturizer, Gelling Agent, Film Forming Agent, Moisture Retention Agent, Fat Replacer and Adhesive Agent | |

| By Application | Food and Beverages, Animal Feed, Paper and Packaging, Pharmaceuticals, Cosmetics and Personal Care, Textiles, Adhesives, Bioplastics and Others | |

| By Grade | Food Grade, Feed Grade, Pharmaceutical Grade, Cosmetic Grade and Industrial Grade | |

| By Form | Powder, Liquid, Granules, Paste, Pellets and Flakes | |

By Distribution Channel

| Direct Sales, Distributors, Ingredient Suppliers, Online B2B Platforms and Specialty Chemical Suppliers | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Disruption Analysis

Transition from Commodity Tapioca Starch to High Value Functional and Sustainable Derivatives

The disruptions in the global tapioca starch and derivatives market can be attributed to the trend in which food industry producers are now looking for high-performing, application-specific ingredients instead of commodity starch sources. Food manufacturers now prefer plant based, clean-label, and allergen-friendly tapioca starch alternatives over their synthetic and gluten counterparts in order to formulate products.

Sustainability-driven industrial uses are also expected to be disruptive forces in the future. Tapioca starch is emerging as an important alternative to petroleum-sourced components due to its use in making biodegradable packaging, bio-based adhesives, coatings for paper products, and compostable goods. This will be driven further by supply chain risks, such as cassava volatility, climatic risks, crop diseases, and dependency on exports.

Technological innovations and capabilities can also disrupt competition within the industry. Tapioca starch producers with higher quality modification technologies, formulation expertise, and better quality management systems will beat low cost commodity producers because of rising customer requirements for consistency and regulatory compliance, especially when it comes to viscosity, texture, shelf life, and safety.

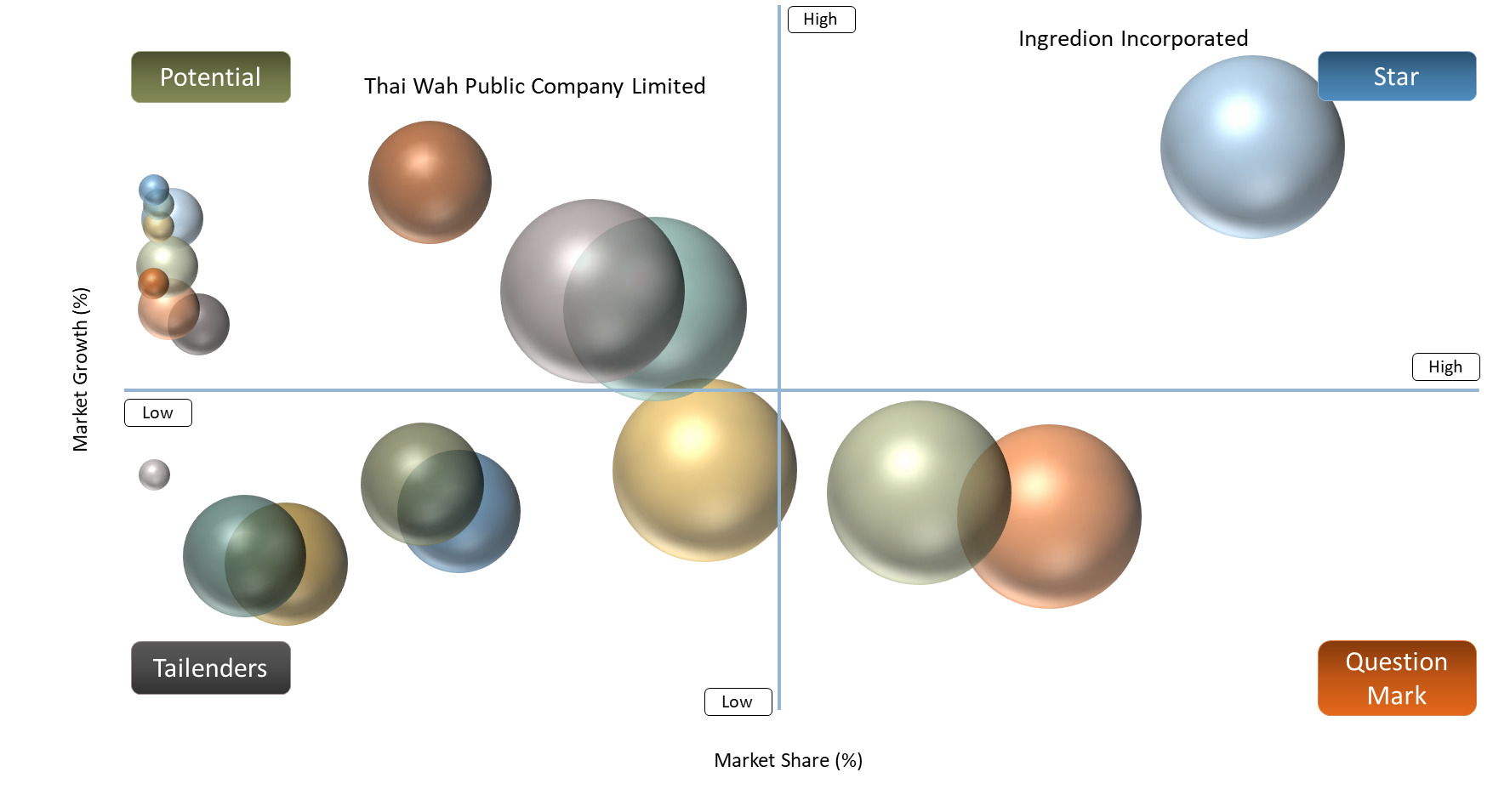

BCG Matrix: Company Evaluation

For the global tapioca starch and derivatives market, the Stars are exemplified by firms with significant international presence, a diversified portfolio of tapioca starches, sophisticated modification expertise, and high penetration levels in end-use markets including foods, pharmaceuticals, industry, and ingredients. These include companies like Ingredion Incorporated, Cargill, Incorporated, Roquette Frères, and Tate & Lyle because of their efficient processing technology, reputation for clean-label ingredients, robust R&D, and extensive customer connections. Such firms have an edge owing to economies of scale, formulation expertise, and global reach.

On the other hand, Cash Cows can be identified as companies that exhibit regional market dominance and efficient cassava supply chains, especially in Asia. Thai Wah Public Company Limited, SMS Corporation Company Limited, and General Starch Limited are dominant due to their ability to produce at large volumes, have exporting capabilities, and specialize in tapioca starch derivatives.

Question Mark companies are depicted by the likes of Starpro Starch (Thailand) Co., Ltd., Beneva Starch Co., Ltd., Shafi Gluco Chem Pvt Ltd, Bluecraft Agro Private Limited, Angel Starch, and Varun Industries. The aforementioned firms thrive within the niche of expanding derivatives of tapioca but need more geographical expansion, better product differentiation, and brand awareness.

Market Dynamics

Clean Label and Gluten Free Reformulation Driving Tapioca Starch Adoption in Food Applications

Tapioca starch is gaining more attention due to the clean label and gluten-free reformulation trend since food companies need components that are simple, functional, and palatable for conscious consumers. According to the U.S. FDA, gluten-free foods must contain less than 20 parts per million of gluten, thus providing food producers with a standard when creating gluten-free bakery products, snacks, sauces, and ready meals.

Moreover, scientific research states that the prevalence of celiac disease accounts for nearly 1% of the world's population, resulting in steady demand for gluten-free food products. Thus, the product under consideration can be used as an effective reformulation component due to its inherent absence of gluten, neutral flavor, and texture-improving properties. In particular, tapioca starch is suitable for thickening sauces, softening bakery items, binding snacks, and improving the mouthfeel of dairy substitutes.

Furthermore, scientific research into cassava-based gluten-free bread demonstrates that cassava starch improves bread softness upon storage and enhances crumbs' cohesion and moisture content. This makes tapioca starch a practical reformulation ingredient across clean label and gluten free food categories.

Cassava Price Volatility and Seasonal Crop Dependency Affect Raw Material Availability and Production Margins

The volatility in the cost of cassava and seasonal dependence on the crop are the main limitations in the global tapioca starch and derivatives market, as cassava is the source material for tapioca starch. The manufacturers of tapioca starch have a high reliance on agriculture, meaning that climate, disease, seasons of planting and harvesting crops, and logistics are significant factors influencing the market. The production of cassava takes place mainly in Thailand, Indonesia, Vietnam, Nigeria, and Brazil, implying that any issues in harvests would be a supply risk.

However, according to the Food and Agriculture Organization (FAO), the global production of cassava exceeds 330 million metric tons each year. Yet, the variability of the harvest depends on rains, droughts, pest infestations, and agricultural practices. Therefore, there are some periods when farmers harvest their crops seasonally, which implies that the supply of the raw material may become unsteady, causing fluctuations in the cost of extraction and operation of factories. High prices of cassava roots affect the margin of profits as raw materials constitute an essential part of production costs.

Segment Analysis

The global Tapioca Starch and Derivatives market is segmented based on product type, modification type, functionality, application, grade, form, distribution channel, and region.

Modified Tapioca Starch Emerging as a High Value Functional Ingredient Across Food and Industrial Applications

It is anticipated that modified tapioca starch would continue to be the most lucrative type of product in the Global Tapioca Starch and Derivatives Market because of its better functional properties than the native version of tapioca starch. Food producers are turning to the use of modified tapioca starch to enhance the attributes of their sauces, soups, baked goods, snack foods, noodles, plant-based milk products, frozen food items, and prepared meal products. The tasteless and non-gluten characteristics of modified tapioca starch make it an excellent choice.

Beyond its applications in food products, modified tapioca starch has found uses in the production of paper, textile, adhesive, pharmaceutical, cosmetic, and bioplastic industries as a binder, coating agent, film former, disintegrant, and material strength enhancer. There are various types of modified tapioca starch such as crosslinked, acetylated, hydroxypropylated, oxidized, cationic, and pregelatinized tapioca starch which are chosen depending on their unique characteristics to meet end-user performance needs. The use of modified tapioca starch is scientifically proven by the work of Sasikunya Tuankriangkrai et al., where they showed that even using 1% of modified tapioca starch improves freeze-thaw stability and reduces expressible moisture in frozen fish gels. Suppliers who have modification technology, high-quality standards, technical expertise, and export facilities are expected to reap more profit margins in this industry.

Geographical Penetration

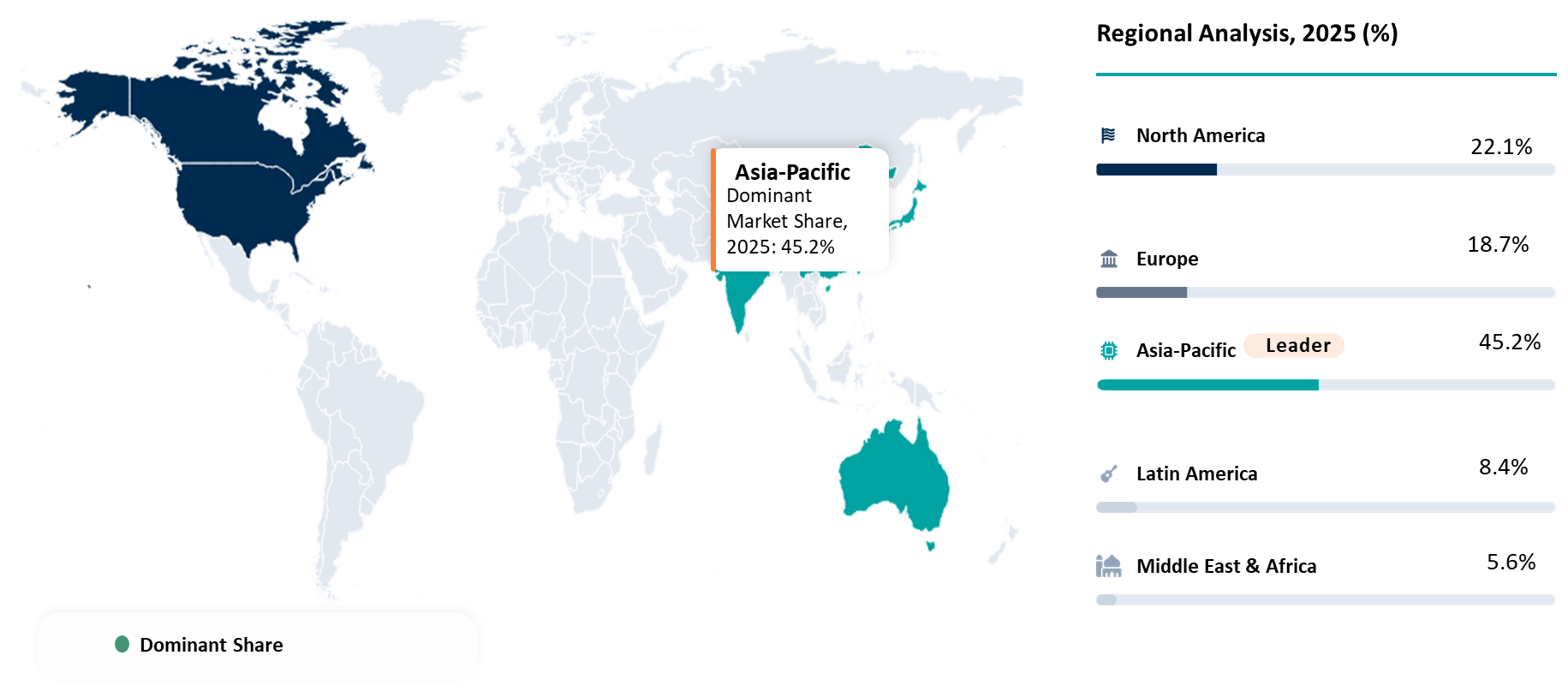

Asia Pacific Leading Tapioca Starch and Derivatives Market Through Strong Cassava Supply and Processing Scale

The Asia Pacific region leads the global tapioca starch and derivatives market, contributing 45.2% to the market in 2025. Factors driving the dominance of the region include robust cassava cultivation, extensive tapioca starch production facilities, and export centers in Thailand, Vietnam, Indonesia, China, and India. Thailand continues to be an important source of supply, with the Thai Tapioca Starch Association estimating cassava production at 24.98 million tons in 2024/2025 compared to 21.82 million tons in 2023/2024, indicating higher raw material supply for starch and derivative production.

There is growing demand for tapioca starch from food and beverage producers for its use in noodles, bakery products, sauces, snack products, non-dairy beverages, frozen foods, and processed foods. In addition, there is growing demand for tapioca derivatives from paper manufacturers, textile industries, adhesive industries, pharmaceutical companies, cosmetic industries, and biodegradable product manufacturers. With increased demand for clean label, gluten-free, plant-based, and sustainable ingredients from consumers, the Asia Pacific region will continue to be the leading producer, innovator, and supplier of tapioca starch and derivatives.

Thailand Tapioca Starch and Derivatives Market Trends

The Thailand tapioca starch and derivatives market shifts from bulk supply of native tapioca starch into advanced value-added modified starch, special food ingredients, pharmaceutical excipients, and sustainable tapioca materials. The country has advantages in terms of the presence of established cassava industry and engagement of firms like Thai Wah, SMS Corporation, General Starch, Starpro Starch, and Beneva Starch. An emerging trend in Thailand is the increasing attention paid to modified tapioca starch in applications like noodles, sauces, bakery goods, frozen food, paper, textile, glue, and pharmaceuticals.

According to Thai Tapioca Starch Association, exports of native tapioca starch by Thailand were 3.20 million tons while modified tapioca starch exports were 1.06 million tons in 2024. This demonstrates the strong presence of Thailand in both raw and processed tapioca products. Prices for export also indicate the level of international business activities since FOB Bangkok prices for tapioca starch were recorded at USD 555 per metric ton as of April 21, 2026. Sustainability, traceable cassava sourcing, farmer partnerships, and tapioca-based bioplastics are further strengthening Thailand’s position as a strategic global supplier.

Vietnam Tapioca Starch and Derivatives Market Outlook

The significance of Vietnam within the Global Tapioca Starch and Derivatives Market is underscored by its robust base of cassava cultivation and export-oriented tapioca starch processing. The country has emerged as a key player in tapioca starch and derivative exports within the Asian market landscape. Vietnam benefits from favorable agricultural conditions, cost-effective production processes, and developing processing capabilities. Products such as tapioca starch are used extensively in food processing, noodle production, snacks, beverages, paper products, adhesives, textile manufacturing, and other industrial sectors.

Based on data from Vietnam Customs, Vietnam's exports of cassava and cassava products stood at 2.62 million metric tons in 2024, with revenue estimated at around USD 1.15 billion. This information illustrates Vietnam's prominent standing within regional starch export markets. The country is the primary trading partner for China within the tapioca starch market, making China a significant trading partner within the tapioca starch market. With rising demands for clean label, gluten-free, and natural products, Vietnam is poised to further its leadership position through the development of high-value starch derivatives.

Competitive Landscape

- The Global Tapioca Starch and Derivatives Market can be considered slightly fragmented, as competition occurs based on the ability to process tapioca starch, starch modification, exports, and the formulation knowledge for application requirements. Multinational ingredient players like Ingredion Incorporated, Cargill, Incorporated, Tate & Lyle, and Roquette Frères are competitive market participants because of their diverse range of starches, widespread geographic presence, and innovation in food, pharmaceutical, and industrial starches. The current trend among these participants is to produce clean label tapioca starch, optimize the textures, and formulate specialty tapioca derivatives for niche applications.

- Local players include Thai Wah Public Company Limited, SMS Corporation Company Limited, and General Starch Limited due to their proximity to cassava raw material supply, manufacturing capacity, and exports in Southeast Asia. The competitive strength of these companies is in the form of tapioca starch, sweeteners, and tapioca derivatives for various food and industrial applications.

- The small to medium-sized enterprises, such as Starpro Starch (Thailand) Co., Ltd., Beneva Starch Co., Ltd., Shafi Gluco Chem Pvt Ltd, Bluecraft Agro Private Limited, Angel Starch, and Varun Industries, engage in stiff competition based on their region-specificity, formulation flexibility, and low-cost manufacturing process. The industry is still application-oriented, and differentiation among the competing suppliers is largely dependent on the service offered to each customer and functionality of the product rather than the price.

Key Developments

- In March 2025, Thai Wah Public Company Limited and Fuji Nihon Corporation jointly developed high-quality tapioca starch products with new functionalities to strengthen food industry applications.

- In March 2026, SMS Corporation Company Limited showcased waxy tapioca starch and modified tapioca starch solutions at Food Ingredients China 2026, targeting bakery, dairy, snacks, sauces, frozen foods and noodles.

- In April 2026, Thai Wah Public Company Limited continued positioning ROSECO series, a thermoplastic starch resin derived from tapioca starch, for packaging, consumer goods and agricultural applications.

- In February 2026, SMS Corporation Company Limited and YES BIO presented DAVAMED and TAPIOPARM modified tapioca starch solutions for pharmaceutical and nutraceutical applications at PACCON 2026.

- In November 2025, SMS Corporation Company Limited showcased I-MEATEX SKV, a modified tapioca starch for plant-based food texture, strengthening its position in clean-label alternative protein applications.

- In December 2025, SMS became Thailand’s first EXCiPACT-certified tapioca starch manufacturer, strengthening its pharmaceutical-grade tapioca starch excipient positioning.

- In August 2024, Roquette Frères expanded its tapioca texturizing portfolio with four CLEARAM TR hydroxypropylated tapioca starch grades for food applications.

- In November 2024, Thai Wah Public Company Limited partnered with Fuji Nihon Corporation to establish a joint venture focused on producing and distributing tapioca starch and related products, strengthening innovation and regional market expansion.

White Space Opportunities

The global tapioca starch and derivatives market have several white spaces based on evolving food trends, industry diversification, and environmental considerations. One of the biggest untapped white spaces in this market is that of clean label and gluten-free food products in which tapioca starch can be used as an alternative to artificial thickening agents and other wheat-derived ingredients in bakery items, non-dairy products, snack foods, and ready-to-eat foods.

The industrial sector provides another great white space for growth. There has been limited penetration of tapioca derivatives in bioplastics, biodegradable packaging, paper coating, textile finishing, and eco-friendly adhesives as companies look for more sustainable sources of raw materials. Another white space lies in the emerging regions of Asia, Africa, and Latin America where cassava processing and tapioca derivatives production for exports can occur.

Premium products such as resistant starch, pregelatinized starch, and pharmaceutical-grade tapioca excipients are high-margin products with few competitors. Manufacturers that develop specialty starches with functionalities like viscosity modification, water binding, and increased shelf-life will be able to cater to specialized market demands. Besides, better logistics and tracking systems for cassava will open up possibilities with multi-national corporation’s keen on sustainable procurement practices.

DMI Opinion

According to DataM, the key obstacle to growth in the global tapioca starch and derivatives market is not creating demand, but meeting customer requirements for consistent quality, stable pricing, and performance characteristics for each application. The market favors suppliers that can not only offer commodity tapioca starch, but also help their clients achieve consistent functionality in the fields of food, pharmaceuticals, paper, textiles, adhesives, and bioplastics.

In practice, the availability of cassava raw materials, high purity, consistent viscosity, modifiability, food safety, and dependable logistics have become as crucial as low prices. Consumers are increasingly interested in tapioca-based products that are labeled naturally, gluten-free, non-GMO, and produced sustainably, without complicating formulations, sourcing, and compliance issues.

Many companies continue focusing on high volumes and low prices, but further expansion will hinge on specialized derivatives, technical assistance, traceability, and export capability. As a result, suppliers that can produce functional tapioca starch derivatives with predictable performance in end-user applications will probably prevail in the future market environment.

Why Choose DataM?

- Ingredient Intelligence: Offers an insight into native tapioca starch, modified tapioca starch, tapioca-based sweetener, maltodextrin, dextrins, fiber, protein, and specialty derivatives according to market requirements and application feasibility.

- End-Use Potential Analysis: Determines the applications where tapioca starch has maximum potential for use in foods and beverages, pharmaceuticals, paper and packaging, textiles, adhesives, animal feed, cosmetic and bioplastic industries.

- Supplier & Capability Comparison: Benchmarks different suppliers according to their product offerings, modification capabilities, production facilities, export capabilities, certifications, competitive pricing power, and application expertise.

- Cassava Supply Chain Analysis: Reviews cassava supply chain dynamics, cassava crop dynamics, cassava production hotspots, supply chain risks, logistics dependencies, and raw material pricing volatility.

- Price and Trade Flow Analysis: Monitors price movements in tapioca starch, trade flow trends, demand per country, supplier concentration analysis, and procurement trends of buyers.

- Clean Label and Sustainability Analysis: Assesses business potential for gluten-free food products, clean label food reformulations, non-GMO foods, plant-based foods, eco-friendly packaging materials, and bio-based products.

- Growth Strategy Development: Assists companies in defining focus applications, target end users, entry points to new regions, partnerships, distribution channels, and value-added product development.

Target Audience

- Food and beverage ingredient manufacturers

- Starch and derivative producers

- Modified starch manufacturers

- Cassava processors and exporters

- Bakery, confectionery and snack manufacturers

- Sauce, dressing and convenience food producers

- Pharmaceutical excipient manufacturers

- Paper, textile and adhesive manufacturers

- Bioplastics and sustainable packaging companies

- Animal feed and nutrition companies

- Procurement and sourcing teams

- Corporate strategy and market intelligence teams

- Business development and sales leaders

- Distributors and ingredient suppliers

- Investors, private equity firms and consulting teams