T-cell Engagers Market Overview

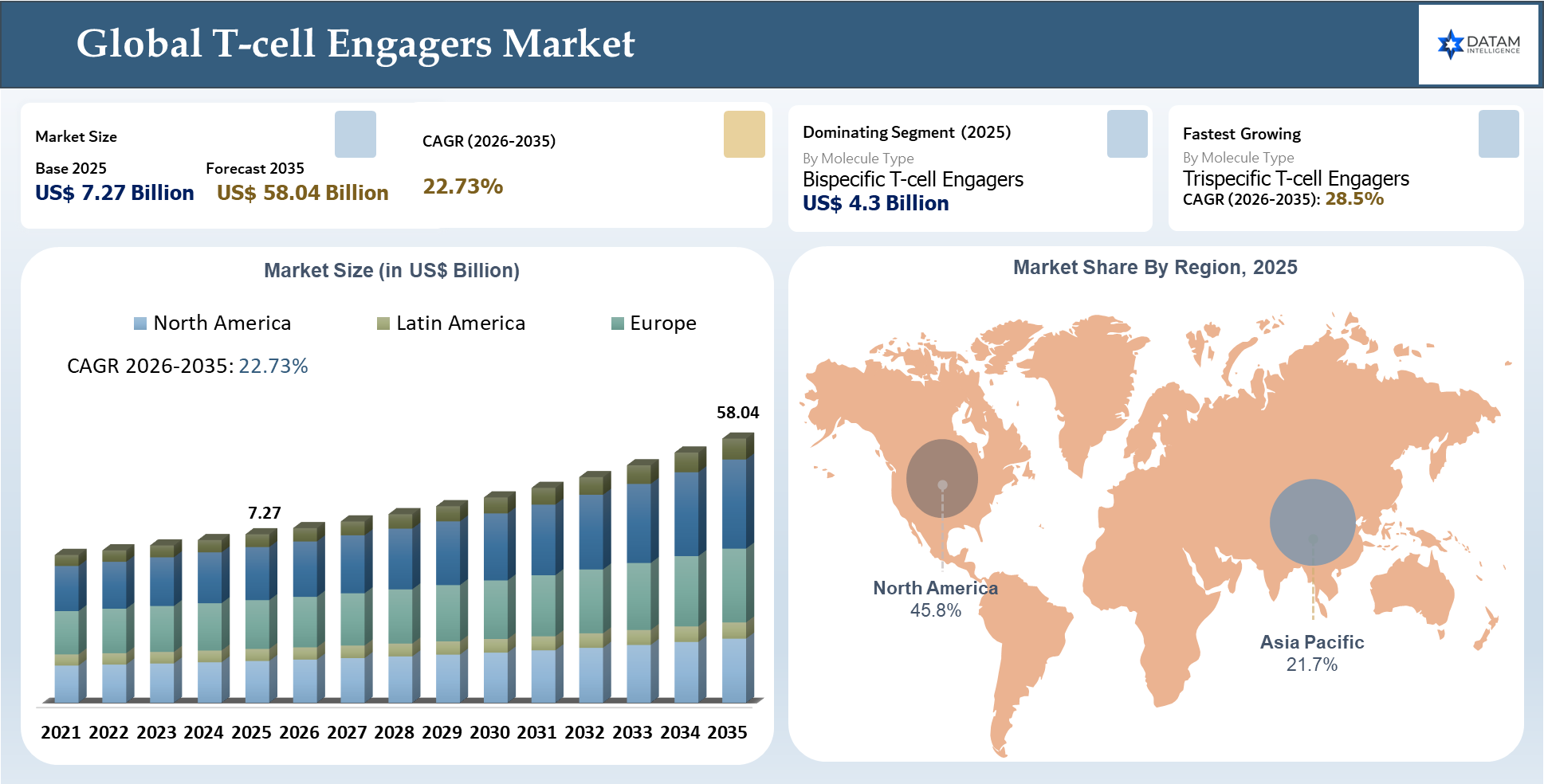

The Global T-cell Engagers Market stood at US$ 7.27 billion in 2025 and is projected to reach US$ 58.04 billion by 2035, growing at a CAGR of 22.73% during 2026-2035. Market growth is being propelled by the increasing incidence of cancer across the globe, growing utilization of targeted immuno-oncological treatments, and the rising need for efficacious treatments that can provide profound reactions in relapsed, refractory, and challenging cancers. T-cell engagers are becoming increasingly important strategically since they direct patients’ own T cells to the cancer cells, providing a highly targeted immune-based therapy as opposed to other treatment methods.

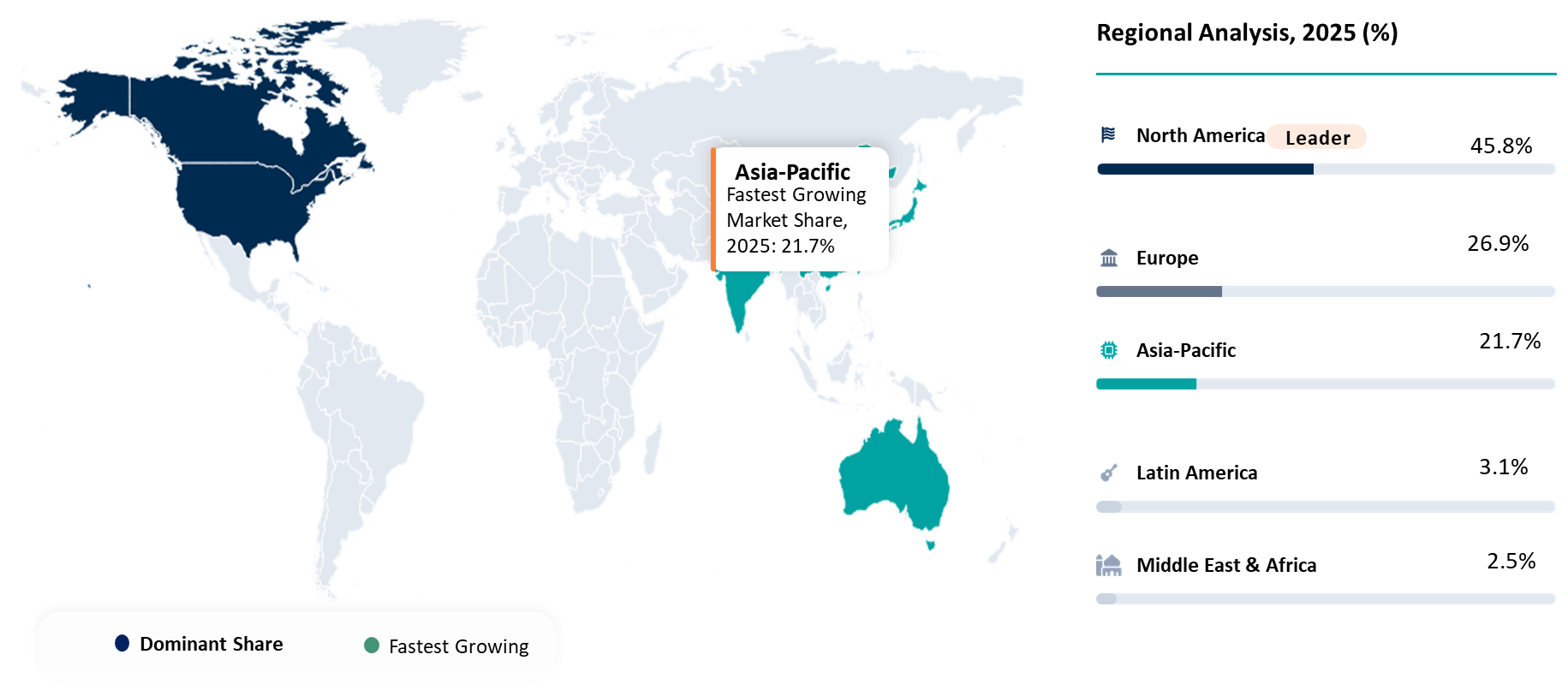

Clinical research activities, increasing investments by the pharmaceutical industry, and physician confidence in therapeutic antibodies to redirect T-cells are influencing the market. The demand is also being bolstered by regulatory reforms, increasing availability of specialized centers for oncology, and increased use of biomarker-driven patient selection techniques. North America holds the highest market share with 45.8% in 2025, attributed to robust R&D in oncology, early approval of regulatory agencies, advanced cancer treatment infrastructure, and higher adoption of innovative therapies. Moreover, the Global T-cell Engagers Market is anticipated to grow at a fast pace in the coming years as firms will focus on developing safer dosage regimens, effective side effects management, outpatient administration capabilities, broader indication scope, and solid tumors application.

AI Impact Analysis

Artificial intelligence has been playing an important role in the evolution of the Global T-cell Engagers Market through improved target identification, molecule engineering, clinical development, and commercialization efforts. AI based bioinformatics platforms can be employed in identifying novel tumor antigens, immune evasion mechanisms, and biomarkers that facilitate the development of the next generation of bispecific/multispecific engagers. AI is also employed in predicting antigenic binding affinity, safety profile, cytokine induction, and treatment efficacy for the purpose of minimizing the probability of failure during early development.

AI in clinical research facilitates patient stratification using genomics, proteomics, and biomarker data analysis, thus enabling patients who will be responsive to T cell engagers to participate in trials, resulting in efficient and successful clinical studies, shortened timelines for patient recruitment, and precision oncology solutions. The use of digital pathology and imaging through AI also improves tumor characterization and therapeutic monitoring.

Manufacturing optimization is an important aspect where AI improves biologics manufacturing processes such as yield, production, and process control. AI commercialization helps pharmaceutical companies assess market requirements, pricing, competition, and physician acceptance. Going forward, as T cell engager pipelines are diversified into solid tumors and autoimmune indications, AI is bound to play an increasingly important role in innovating faster and lowering drug development costs.

T-cell Engagers Market Key Takeaways

- The molecule type and target indication continue to represent the two most commercially relevant approaches to market analysis, showing which biopharma companies are prioritizing bispecific, trispecific, and future generation T-cell redirecting technologies in the hematological malignancy and new solid tumor indications space.

- Increasingly, demand is going to be driven by products that show high levels of clinical differentiation, such as high levels of response, durable remission potential, low-risk cytokine release syndrome profiles, decreased neurotoxicity, and broader patient suitability.

- North America is at the forefront of the Global T-Cell Engagers Market, due to its robust oncology R&D capabilities, advanced regulatory system, advanced specialist cancer treatment facilities, and the presence of leading companies developing CD3 bispecific antibodies.

- There is a shift away from late-line hematological cancers to earlier indications, more emphasis on subcutaneous delivery and outpatient care, and solid tumors are increasingly targeted by companies working in this space to increase their commercial success.

- Leading companies will have robust clinical data, differentiated targets, safe dosing, and reimbursement strategy, allowing for quicker adoption among physicians.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 7.27 Billion | |

| 2035 Projected Market Size | US$ 58.04 Billion | |

| CAGR (2026-2035) | 22.73% | |

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Molecule Type | Bispecific T-cell Engagers, Trispecific T-cell Engagers, Multispecific T-cell Engagers, T-cell Receptor Based Engagers, Antibody Fragment Based T-cell Engagers, and Full-Length Antibody Based T-cell Engagers | |

| By Target Antigen | CD19, CD20, CD22, CD33, BCMA, GPRC5D, HER2, EGFR, PSMA, DLL3, CEA, Claudin 18.2, Mesothelin, and Others | |

| By Therapy Type | Monotherapy and Combination Therapy | |

| By Indication | Cancer, Autoimmune Diseases, Infectious Diseases, Fibrotic Disorders, Immune Mediated Disorders, Transplant Rejection, Rare Diseases, and Others | |

| By Mechanism of Engagement | T-cell Redirecting Engagers, Tumor Specific T-cell Activation, Conditional Activation T-cell Engagers, Immune Synapse Enhancing Engagers, and Cytotoxic T-cell Recruitment Platforms | |

| By Administration Route | Intravenous, Subcutaneous, Intratumoral, and Continuous Infusion | |

| By Development Stage | Discovery Stage, Preclinical Stage, Phase I, Phase II, Phase III, and Commercialized Products | |

| By End User | Hospitals, Specialty Cancer Centers, Academic Research Institutes, Biotechnology Companies, Pharmaceutical Companies, Contract Research Organizations, and Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

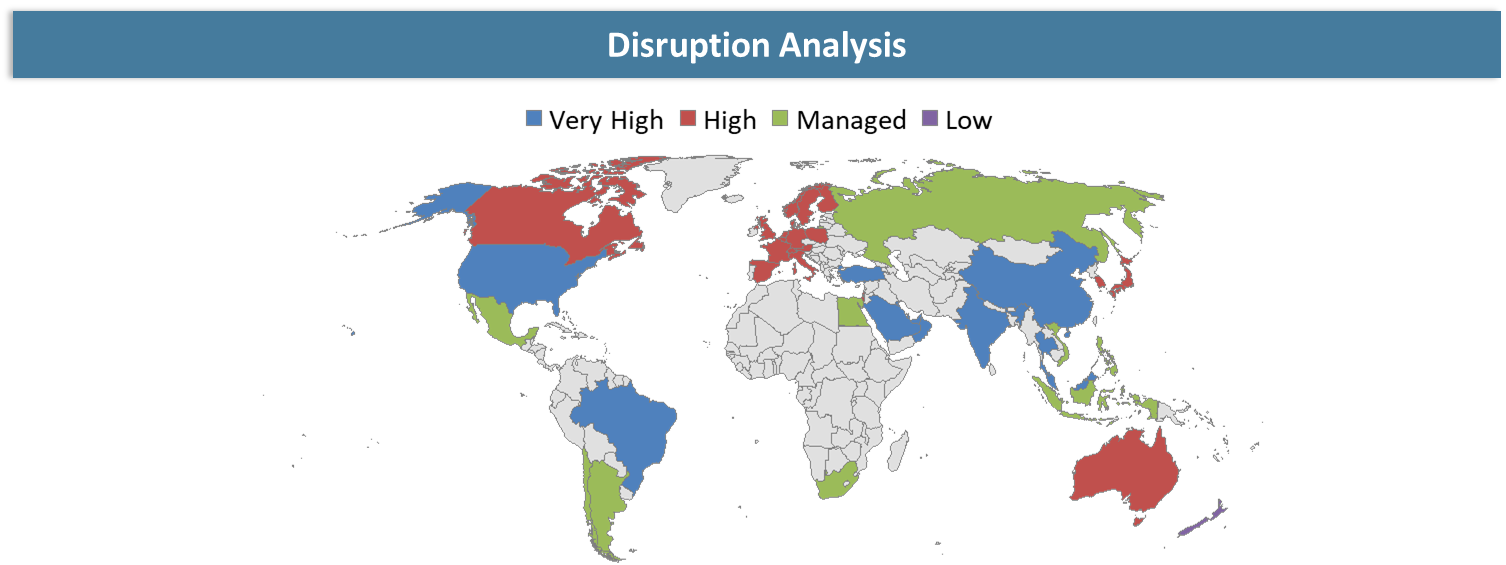

Disruption Analysis

Next Generation Immunotherapy Platforms and Expanding Clinical Applications Are Reshaping Competitive Dynamics in the T-cell Engagers Market

The Global T-Cell Engagers Market is experiencing disruption fueled by innovation in immunotherapy platforms, changes in biology targets, and new competitors entering the market with competing therapies. Classic cancer treatments like chemotherapies and monoclonal antibodies have been challenged in the light of innovations in T-cell engagers that can effectively activate immune cells and treat cancers.

One of the main sources of disruptions is diversification in the application of the T-cell engager platform that will go beyond blood cancers to include the treatment of solid tumors. Moreover, increased competition from CAR T-cell therapies, antibody-drug conjugates, and immune checkpoint inhibitors will push companies to innovate further.

Developments in manufacturing, such as antibody engineering that can be scaled up and off-the-shelf therapy creation, will make things less complicated than in personalized cell-based treatments. Collaborations of biotech companies and big pharma are speeding up platform commercialization and product development. Moreover, increased focus on autoimmune diseases might disrupt market boundaries as far as T-cell engagers will be seen as an immunomodulatory treatment modality.

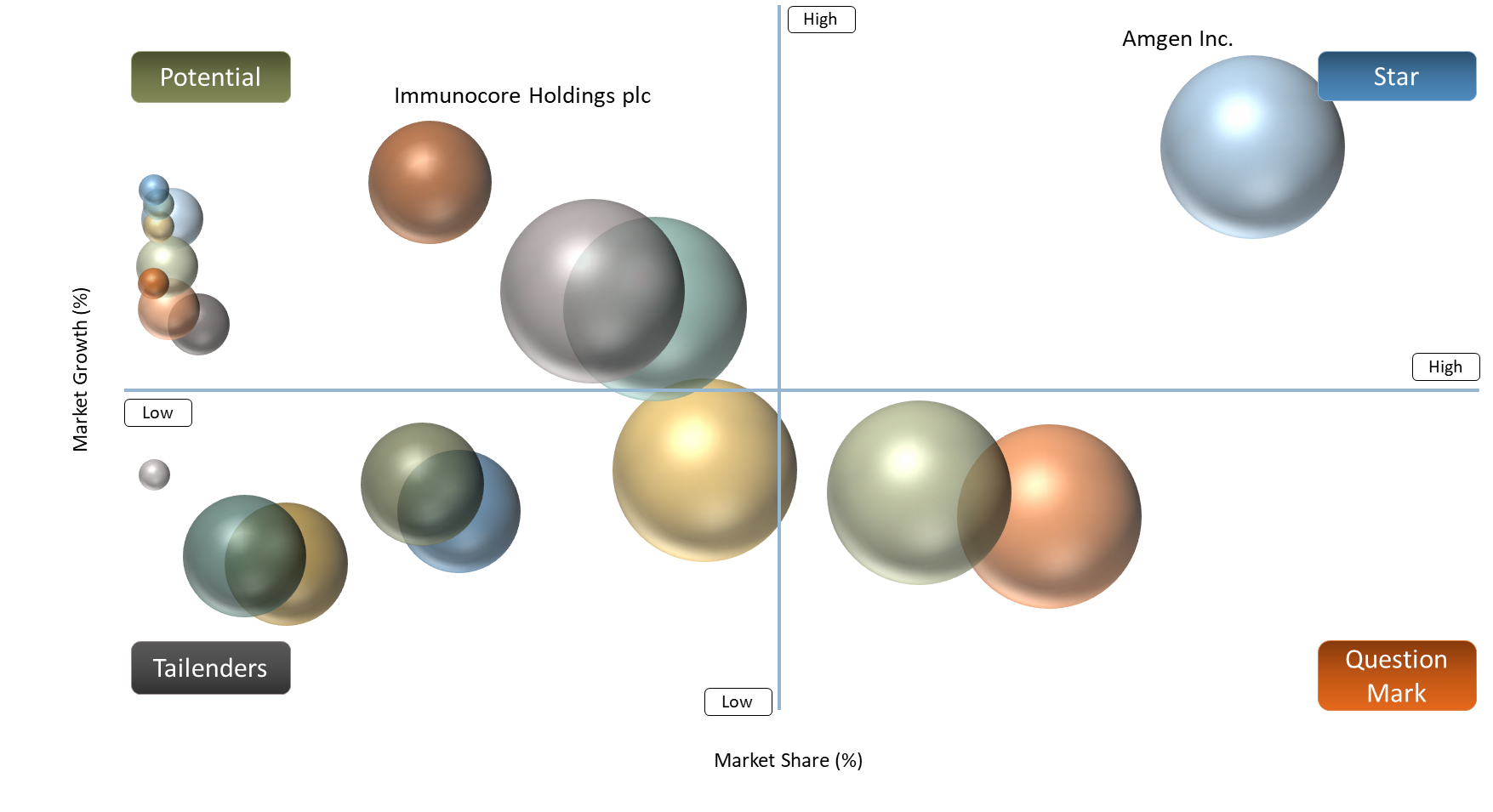

BCG Matrix: Company Evaluation

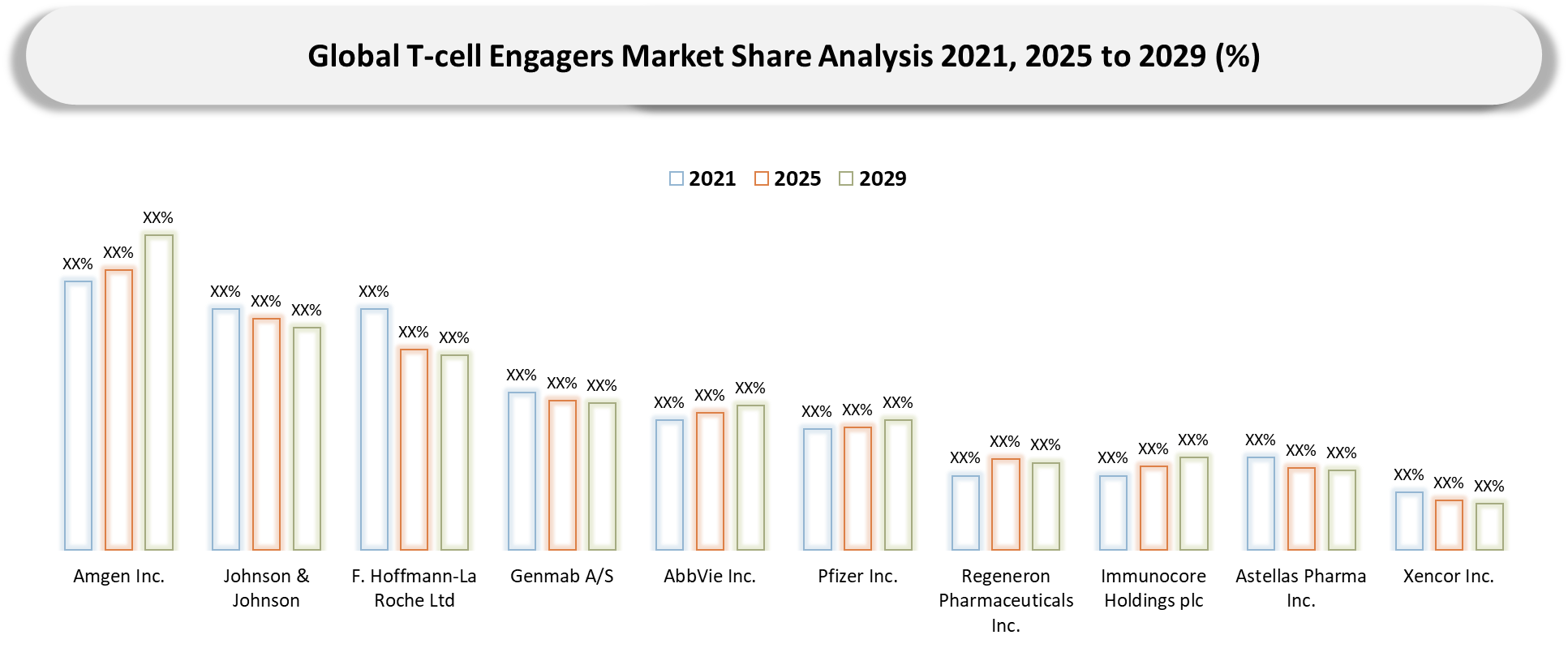

In relation to the BCG Matrix, Stars will consist of those companies that have an outstanding portfolio of commercialized T-cell engager products, with already approved products and an excellent oncology presence and ongoing growth. Examples of these include Amgen Inc., Johnson & Johnson, F. Hoffmann-La Roche Ltd, Genmab A/S, AbbVie Inc., Pfizer Inc. and Regeneron Pharmaceuticals Inc. These companies have the benefit of already having some CD3 based bispecific product, or even being in clinical trials for such products, as well as having a wide presence in oncology and growing in hematological malignancies and solid tumors.

Cash Cows will be companies with solid biologics development infrastructure, oncology expertise and good immune-engager assets that provide the company with long-lasting stability. Bristol Myers Squibb Company, GSK plc and Gilead Sciences Inc. fit the description because of their oncology capability, partnership, clinical development and capability for scaling up promising immune-engager programs through more commercial channels.

Question Marks will be companies with outstanding platforms, good clinical assets, and T-cell engager products but not as commercialized and scaled as large pharmaceutical companies. In this category we find companies like Immunocore Holdings plc, Astellas Pharma Inc., Xencor Inc. and Merus N.V..

Market Dynamics

Approved T-cell Engagers Are Reshaping Blood Cancer Treatment Through Deeper Responses in Relapsed and Refractory Patients

T-cell engagers that have received approval are revolutionizing the treatment of hematological cancers through the provision of an answer to the major drawback faced by relapsed and refractory patients in which traditional treatments yield less value. The novel drugs target endogenous T-cells through the creation of a bridge between CD3 receptors and tumor-related antigens such as BCMA, CD19, and CD20 and, therefore, produce highly targeted toxicity without necessitating cell engineering processes required for autologous therapies. Such drugs are highly clinically relevant especially in later lines of treatment where patients face resistance, increased risk of relapse, and few enduring options.

The clinical adoption of these products is being rapidly driven by the efficacy results obtained in clinical trials. For instance, the BCMA-based agent, teclistamab, registered an impressive response rate of over 61.8% in heavily pretreated patients suffering from multiple myeloma. Similarly, epcoritamab showed promising response rates exceeding 80% among patients with relapsed follicular lymphoma. The results have played a significant role in transforming treatment protocols and building confidence among physicians with respect to the use of dual specificities in immune engagement therapy.

From a commercial standpoint, the approved drugs help validate the technology platform, mitigate risks and spur investments in the development of additional molecules.

Neurotoxicity and infection risks increase monitoring burden and restrict use beyond specialist cancer centers

The T-cell engagers are bound to experience barriers when it comes to adoption since their effectiveness depends heavily on rigorous safety surveillance and specialized treatment. Safety issues including cytokine release syndrome, neurotoxicity, ICANS, infections, cytopenias, and pneumonia can arise during administration of the medication, especially during the up-dosing process or the first few cycles. It is therefore difficult for a community oncology practice to adopt the T-cell engaging treatments owing to lack of inpatient capacity, immunotherapy-trained staff, and proper protocol for addressing potential toxicities.

In this regard, the FDA noted that cytokine release syndrome (CRS) occurred in 72%, neurologic toxicity in 57%, and immune effector cell-associated neurotoxicity (ICANS) in 6% of those taking Tecvayli. Similarly, 28% of Epkinly patients had infections, 24% experienced CRS and 0.8% experienced ICANS. Such safety considerations result in higher costs, restricted decentralization of care and increased dependence on specialist cancer centers.

Segmentation Analysis

The Global T-cell Engagers Market is segmented based on molecule type, target antigen, therapy type, indication, mechanism of engagement, administration route, development stage, end-user, and region.

Bispecific T-cell Engagers Lead Market Expansion Through Regulatory Validation and Broad Clinical Adoption

Bispecific T-cell engagers account for the most developed molecule type in the Global T-cell Engagers Market, driven by strong regulatory validation, medical practitioner awareness, and clinical pipeline development. Contrary to trispecific and higher-order types, bispecific products have progressed beyond proof-of-concept and into commercialization and wide-scale clinical development in leukemia, lymphoma, multiple myeloma, and certain solid tumors.

Approval rate is one of the critical markers for evaluating the market. By 2025, the FDA had approved 14 bispecific antibodies for use in cancer patients, with several bispecific off-the-shelf T-cell engagers among the approved molecules. This trend confirms the growing regulatory confidence in bispecific immune engagement mechanisms and highlights the increased relevance of these drugs in oncology.

Strategically, bispecific T-cell engagers are the leading profit generation segment. The combination of scalable manufacturing, regulatory guidance, and physician acceptance provides an advantage for these molecules over personalized therapies. As the product pipeline expands into first-line therapy and solid tumors, bispecific T cell antibodies formats will likely maintain their market dominance among molecule types..

Geographical Penetration

North America Leading T-cell Engagers Advancement Through Innovation Density and Commercial Execution Leadership

North America is the dominant player in the T-cell Engagers Market, backed by high oncology research and development intensity, early adoption of immunotherapy treatments, and presence of prominent biopharmaceutical companies developing bispecific and multispecific antibody technology platforms.

A mature clinical trial infrastructure, cancer specialty centers, quick approval process, and better treatment accessibility relative to developing nations are some of the additional strengths. The growing prevalence of hematologic cancers, wider application of CD3-based T-cell engagement products, and higher spending on off-the-shelf therapies for difficult-to-treat cancers will fuel market growth. The commercialization process is also gaining traction, as manufacturers explore opportunities outside of hematological cancers and enter solid tumors, which currently lack a treatment option.

The hospital administration system, the need for toxic monitoring, and the management of cytokine release syndrome are fueling the need for more experienced oncology centers, which will give North America an edge structurally. Furthermore, the acceptability of payers, adoption of companion diagnostics, and incorporation in clinical guidelines will help speed up market penetration. All these factors have led to the belief that North America will continue its dominance, but in a different way.

U.S. T-cell Engagers Market Trends

The US T-cell Engagers Market is progressing from a specialized hematologic oncology market to an expanded immuno-oncology growth platform. Its adoption is currently driven by the relapsed/refractory multiple myeloma, lymphoma, and leukemia indications wherein T-cell redirection therapies are widely applied after primary therapy failure. According to the American Cancer Society, around 2.04 million newly diagnosed cancer cases and 618,120 deaths from cancer occurred in the US in 2025.

One major market trend observed is the transition from inpatient-focused administration toward more manageable treatment paradigms. Players are focusing on step-up dosing, subcutaneous administration, enhanced cytokine release syndrome management, and outpatient administration feasibility to mitigate patient monitoring requirements and enhance treatment scalability. Other critical trends in the industry include expanding the pipeline from hematologic cancers to solid tumors via bispecific, trispecific, and advanced antibody technologies.

Market growth is also fueled by the robust US clinical trial framework, fast FDA review timelines, payers' willingness to reimburse innovative oncology therapies, and early clinical guideline incorporation. In summary, market growth will be propelled by expanded labeling, front-line positioning, and enhanced safety and convenience of dosing formulations.

Canada T-cell Engagers Market Outlook

The Canadian T-cell Engagers Market will see sustained growth over the forecast period due to increased cancer patient pool, greater use of precise immunotherapy, and wider availability of bispecific antibodies via specialized oncology centers. According to Canadian Cancer Statistics, Canada had an estimated 254,800 newly diagnosed cases of cancer and 87,400 cancer deaths in 2025. This demonstrates the rise in cancer burden, leading to a higher requirement for targeted therapies.

The primary driver behind market growth will be the growing incidence of relapsed or refractory blood cancers such as multiple myeloma, lymphoma, and leukemia. These patients will receive T-cell redirecting therapies when conventional treatment approaches prove ineffective. Nonetheless, the uptake in Canada will significantly rely on health technology assessment, reimbursement at a provincial level, therapy cost, and hospital preparedness to handle cytokine release syndrome and neurotoxicity.

An important development in Canada will be the trend towards less toxic and more manageable routes of therapy administration. These include dose escalation, subcutaneous formulation, and outpatient management strategies. Clinical evidence will lead to further adoption of T-cell engagers in Canada as an earlier line of therapy and selected indications for solid tumors.

Competitive Landscape

- In terms of competition, the Global T-cell Engagers Market is somewhat consolidated, with rivalry among big oncology-oriented pharmaceutical players as well as small biotech firms engaged in bispecific, trispecific, and multispecific immune engager platforms. Key market leaders including Amgen Inc., Johnson & Johnson, F. Hoffmann-La Roche Ltd, Genmab A/S, AbbVie Inc., Pfizer Inc., and Regeneron Pharmaceuticals Inc. are increasing their competitive edge through approved drugs, strong pipelines, widening indications, and globalization.

- Other important players include innovator firms such as Immunocore Holdings plc, Astellas Pharma Inc., Xencor Inc., and Merus N.V., whose strategies revolve around unique T-cell redirection mechanisms, innovative drug targets, and advanced drug formulations. Other leading companies like Bristol Myers Squibb Company, GSK plc, and Gilead Sciences Inc. are improving their competitive position through oncology-oriented drug pipelines, partnerships, and immunotherapy research & development efforts. Generally, competition is characterized by unique target identification, safety profiles, convenient dosing regimens, solid tumor success rate, and market penetration ability.

Key Developments

- April 2026: Astellas Pharma and Vir Biotechnology entered a global collaboration to develop VIR-5500, a PSMA-targeting dual-masked T-cell engager for prostate cancer.

- March 2026: Antengene licensed ATG-201, a CD19 CD3 bispecific T-cell engager for autoimmune diseases, to UCB for global development.

- February 2026: Boehringer Ingelheim and Zai Lab announced collaboration for a DLL3-targeting T-cell engager combined with antibody drug conjugate therapy.

- January 2026: Johnson & Johnson expanded Tecvayli clinical development into earlier-line multiple myeloma treatment settings through additional Phase III studies.

- September 2025: Regeneron Pharmaceuticals received FDA approval for linvoseltamab, a BCMA CD3 T-cell engager for relapsed multiple myeloma.

- July 2025: Genmab and AbbVie expanded Epkinly development through combination trials targeting diffuse large B-cell lymphoma and follicular lymphoma.

- May 2025: Pfizer advanced Elrexfio into broader global commercialization following expanded regulatory approvals across additional oncology markets.

- May 2024: Amgen received FDA approval for Imdelltra, a DLL3 targeted T-cell engager for extensive-stage small cell lung cancer.

- June 2024: Roche expanded Columvi clinical adoption through additional studies evaluating earlier-line use in diffuse large B-cell lymphoma.

- March 2024: Merus advanced multiple trispecific immune engager candidates targeting solid tumors through early-stage oncology clinical trials.

- January 2024: Xencor advanced XmAb bispecific T-cell engager candidates targeting hematologic malignancies and solid tumor oncology applications.

White Space Opportunities

White spaces are present in the Global T-cell Engagers Market, including unmet needs in solid tumors, autoimmune conditions, and novel immune targeting. The current commercialization is largely centered on hematological cancers, but there are untapped opportunities in solid tumors as a result of difficulties associated with tumor microenvironment inhibition, antigen diversity, and off-tumor toxicity. Businesses that can build safer, tumor-selective technology platforms with enhanced tissue penetration will be able to create enormous business opportunities.

There is also an opening for autoimmune and immune-mediated diseases in which selective elimination of pathogenic immune cells can provide a unique solution compared to non-selective immunosuppressive drugs. Clinical trials for indications like lupus and myasthenia gravis show that this segment holds future growth opportunities outside oncology.

From a geographical perspective, emerging economies are underdeveloped in terms of lack of biological drug availability, financial barriers, and oncology facilities. There are possibilities to create regional marketing models. Moreover, platform differentiation via subcutaneous injection, low chances of cytokine release syndrome, and extended drug action duration are other gaps in the competitive landscape. Firms tackling manufacturing scale-up, outpatient treatment, and increased safety can achieve premium positioning in the market.

DMI Opinion

According to DataM, the biggest problem facing the Global T-cell Engagers Market is not about generating demand, but whether firms can successfully leverage their clinical advantages into viable commercial strategies. Although T-cell engagers have proven effective against hematological malignancies, sustained success involves striking a balance between efficacy, safety, ease of administration, and healthcare system readiness.

In practice, clinical differentiation now goes beyond simple response rates. Issues like cytokine release syndrome management, outpatient applicability, ease of administration, manufacturing scalability, and insurance coverage now play a key role in adoption decisions. Healthcare institutions seek products that fit easily into existing treatment regimens without imposing burdensome monitoring needs or infrastructure demands.

Despite this, many firms focus their marketing efforts on novel targets and pipeline sizes, neglecting potential adoption problems. Going forward, competitive success hinges on platforms that minimize toxicities, facilitate administration, enhance accessibility, and provide superior treatment results. Firms that can turn scientific advancements into clinical and healthcare adoption success are poised to dominate the future market for T-cell engagers.

Why Choose DataM?

- T-cell Engager Platforms Innovation: Focuses on developments within bispecific, trispecific, multispecific, Fc-engineered, and long-acting T-cell engagers platforms in oncology and immunological indications.

- Position and Clinical Performance of Companies: Considers competitive edge of major players with regard to target specificity, efficacy, safety, method of delivery, manufacture capacity, and pipeline stage.

- Clinical Adoption of T-cell Engagers: Highlights real-world application of T-cell engagers in hematological cancers, solid tumors, and autoimmune disease settings.

- Industry Trends and Market Intelligence: Covers approval trends, clinical trials, licensing deals, business development activities, manufacturing capacities, regulatory advancements, and investments in key geographical areas.

- Business Strategy and Competitive Benchmarking: Offers detailed analysis of strategic alliances, co-development arrangements, commercialization approaches, product pipeline growth, and competitive benchmarking of immunotherapy leaders.

- Pricing, Reimbursement, and Market Access Strategies: Reveals information about treatment costs, reimbursement trends, access in specialty oncology centers, adoption by hospitals, and commercialization in different regions.

- Market Penetration and Expansion Potential: Identifies unexplored treatment areas, advanced targeting technologies, emerging markets, and market penetration strategies for the global uptake of T-cell engagers.

Target Audience 2026

- Pharmaceutical and Biotechnology Companies

- Oncology Drug Development Teams

- Immunotherapy Research and Innovation Teams

- Clinical Trial and Translational Research Organizations

- Hospital Oncology Centers and Cancer Institutes

- Contract Research Organizations and CDMOs

- Corporate Strategy and Market Intelligence Teams

- Business Development and Licensing Teams

- Investors and Private Equity Firms

- Healthcare Providers and Specialty Clinics

- Regulatory and Compliance Teams

- Consulting and Life Sciences Advisory Firms

- Biologics Manufacturing and Supply Chain Teams

- Precision Medicine and Companion Diagnostics Developers

- Academic Research Institutes and Universities