Overview

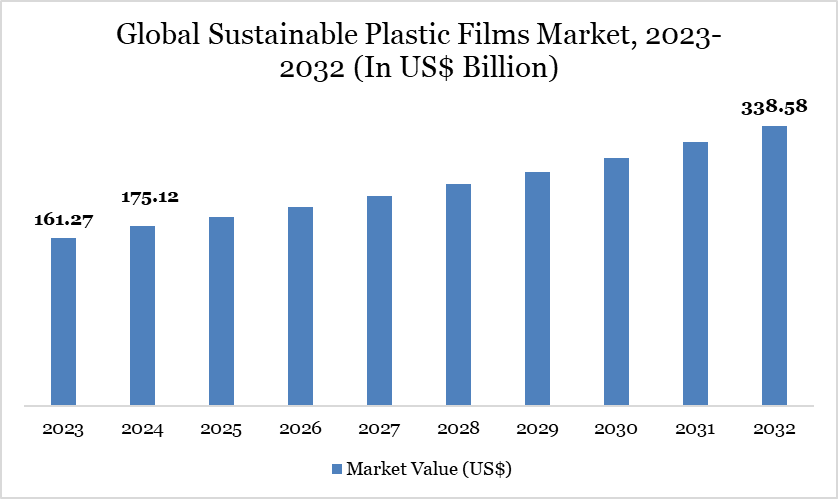

The global Sustainable Plastic Films market reached US$ 175.12 billion in 2024 and is expected to reach US$ 338.58 billion by 2032, growing at a CAGR of 8.59% during the forecast period 2025-2032.

The global market for sustainable plastic films is seeing a significant movement toward mono-material film structures, particularly those made of polypropylene or polyethylene, which are designed to simplify recycling while maintaining functionality. At Fachpack 2025, Innovia Films demonstrated a complete line of mono-material BOPP films that complies with the EU's Packaging and Packaging Waste Regulation (PPWR).

It includes Propafilm CHS and CHT, high-performance PP films with exceptional printability and thermal resistance for retort applications, as well as ultra-high barrier solutions designed to replace PET or foil layers in a totally recyclable mono-PP laminate structure. The developments represent a clear industry-wide effort to promote recyclability through mono-material design, offering high barrier qualities without the complexity of multilayer films and aligning with circular economy aims.

Sustainable Plastic Films Market Trend

The transition to mono-material films designed for easy recycling while maintaining barrier qualities is a key trend in the worldwide sustainable plastic film market. Historically, multilayer films blended many polymers to give durability and oxygen/moisture resistance, but they were practically hard to recycle. Companies are investing in all-PE or all-PP films with improved coatings and barrier technologies to ensure complete compatibility with existing recycling streams.

For example, Amcor, Mondi and Berry Global have all introduced recyclable mono-material films designed for food packaging applications, while retailers such as Tesco and Aldi have begun to replace mixed-plastic flexible packaging with mono-material alternatives. This trend is accelerating acceptance as both authorities and customers want packaging that is not just reduced in environmental footprint, but also practically recyclable at scale.

Market Scope

Metrics | Details |

By Material | Biodegradable Plastics, Recyclable Plastics, Others |

By Application | Packaging Films, Agricultural Films, Industrial Films, Others |

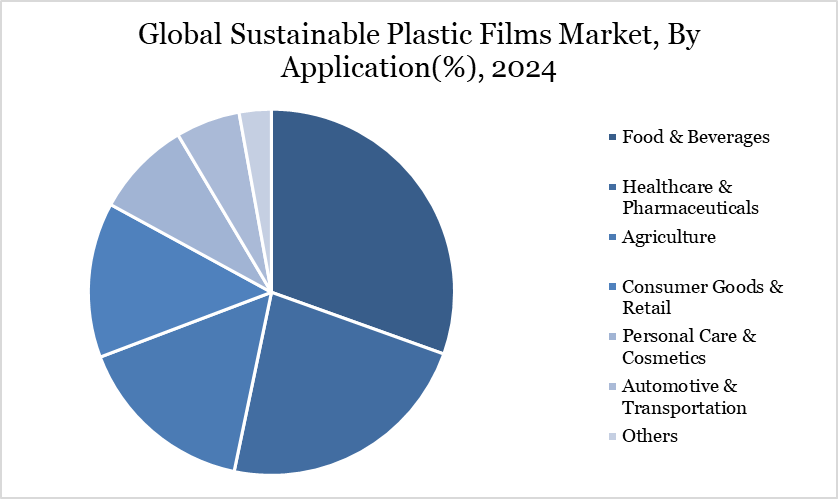

By End-User | Food & Beverages, Healthcare & Pharmaceuticals, Agriculture, Consumer Goods & Retail, Personal Care & Cosmetics, Automotive & Transportation, Others |

By Region | North America, South America, Europe, Asia-Pacific, Middle East and Africa |

Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth |

Market Dynamics

Regulatory Push and Corporate Commitments Toward Circular Packaging

The combined effect of regulatory mandates and voluntary company initiatives to reduce plastic waste is a significant driver of the worldwide sustainable plastic films industry. The European Union mandates that all packaging be recyclable or reusable by 2030, while the United States, Canada and parts of Asia-Pacific are tightening single-use plastic prohibitions and encouraging extended producer responsibility (EPR).

At the same time, more than 500 companies have vowed to improve their usage of recyclable, compostable or bio-based packaging under the Ellen MacArthur Foundation's Global Commitment program. This combination push from regulators and brands is accelerating demand for recyclable mono-material films, compostable alternatives and films that incorporate post-consumer recycled (PCR) content, driving innovation and acceptance worldwide.

Higher Costs and Infrastructure Gaps in Recycling

Despite increased pace, the worldwide market is constrained by higher costs and a lack of recycling infrastructure. Sustainable plastic films, particularly biodegradable and bio-based varieties, are frequently 20-50% more expensive than conventional plastics due to raw material constraints and manufacturing complexity. Furthermore, many locations still lack proper recycling and composting infrastructure, so even recyclable films may end up in landfills.

While Europe has well-developed collection systems, much of Asia, Africa and Latin America suffer from segregated garbage collection, hampering the efficiency of circular economy projects. Cost and infrastructure hurdles impede large-scale implementation, particularly in price-sensitive sectors and developing regions.

Segment Analysis

The global sustainable plastic films market is segmented based on material, application, end-user and region

Rising Shift Towards Eco-friendly Solutions in Food and Beverages

Food and beverages account for the bulk of the global market due to the growing trend for eco-friendly packaging solutions that balance product safety, shelf life extension and environmental responsibility. With global food packaging waste accounting for roughly 36% of total plastic waste (UNEP, 2023), regulators and consumers are encouraging firms to use recyclable, biodegradable or bio-based films instead of traditional plastics.

Leading food and beverage businesses, including Nestlé, PepsiCo and Unilever, have stated plans to make all of their packaging recyclable or reusable by 2025, generating direct demand for sustainable films. Furthermore, improvements in high-barrier bio-based films are extending the shelf life of perishable foods such as dairy, meat and fresh vegetables, reducing food waste while fulfilling sustainability targets. Recent introductions, such as Mondi's recyclable mono-material barrier film for meat packaging in Europe and Amcor's recyclable polyethylene films for snacks, demonstrate how innovation is being pushed by the food industry's requirement for both performance and compliance.

Geographical Penetration

Stringent Regulations in Food & Beverages Packaging Drives the Asia-Pacific Market

The continual strengthening of packaging regulations across Asia-Pacific is a significant driver for the sustainable plastic films market in the food and beverage sector. For example, India's Bureau of Indian Standards is amending its standards to enable recycled PET in food contact packaging beginning in 2025, while Indonesia is implementing a new standard for paper/cardboard food packaging, both of which promote recyclable materials.

As part of its Resource Sustainability Act, Singapore has enhanced regulation of food-contact materials and taken steps toward extended producer responsibility (EPR). Thailand plans to strictly regulate food contact paper and has just prohibited all plastic garbage imports. Regulatory changes are driving food and beverage businesses to employ recyclable or mono-material films that are EPR-compliant and safer for customers.

Sustainability Analysis

Growing demand for recyclable, biodegradable and bio-based packaging in areas such as food, drinks, agriculture and healthcare is shaping the market's sustainability. A crucial factor is growing pressure to minimize single-use plastic trash, which the UNEP estimates to be about 141 million tons per year. Major producers and converters are shifting to mono-material films, which allow for easier recycling and are introducing post-consumer recycled resins into their product lines.

For example, in late 2024, Amcor reported that it has expanded its line of 100% recyclable polyethylene-based films for European food packaging. The programs connect with the European Union's objective of making all packaging reusable or recyclable by 2030, directly affecting industry innovation and adoption.

Competitive Landscape

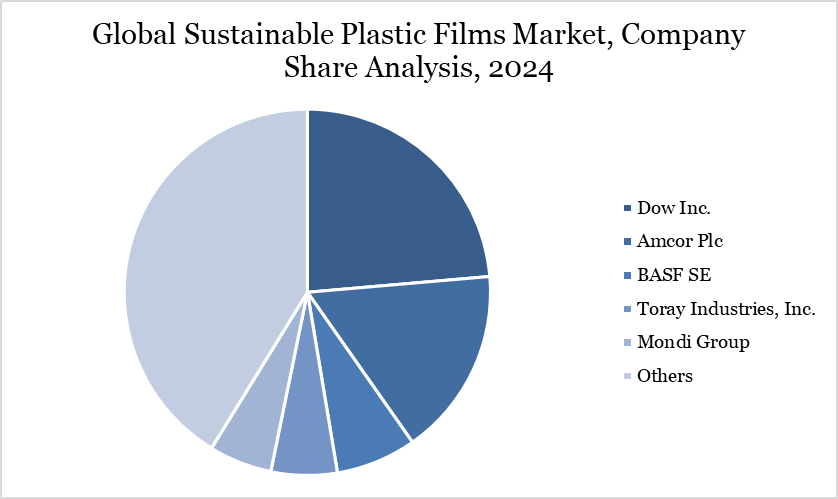

The major global players in the market include Dow Inc., Amcor Plc, BASF SE, Toray Industries, Inc., Mondi Group, Sealed Air Corporation, Uflex Ltd., SABIC, Novamont S.p.A. and Futamura Group.

Key Developments

In 2025, Amcor plc and Fedrigoni established a partnership to develop a recyclable flexible packaging solution that blends Amcor's AmPrima Plus flow wrap with Fedrigoni's semi-rigid labels. The entire box may be recycled in polyethylene streams across Europe, according to the companies. The idea is related to the EU's Packaging and Packaging Waste Regulation, which requires all packaging to be recyclable by 2030. The company stated the mono-material design has been validated as recyclable by RecyClass and cyclos-HTP.

In January 2024, CAMM Solutions has developed a biodegradable stretch film as a sustainable alternative to traditional plastic films used in logistics. This new solution is composed of a blend of natural materials and contemporary PVOH formulations, providing the same performance as typical stretch films while eliminating microplastic contamination.

Why Choose DataM?

Data-Driven Insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. This approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. This personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. These insights complement and go beyond what is typically available in generic databases.

Target Audience 2024

Manufacturers/ Buyers

Industry Investors/Investment Bankers

Research Professionals

Emerging Companies