Solid State Circuit Breaker Market Overview

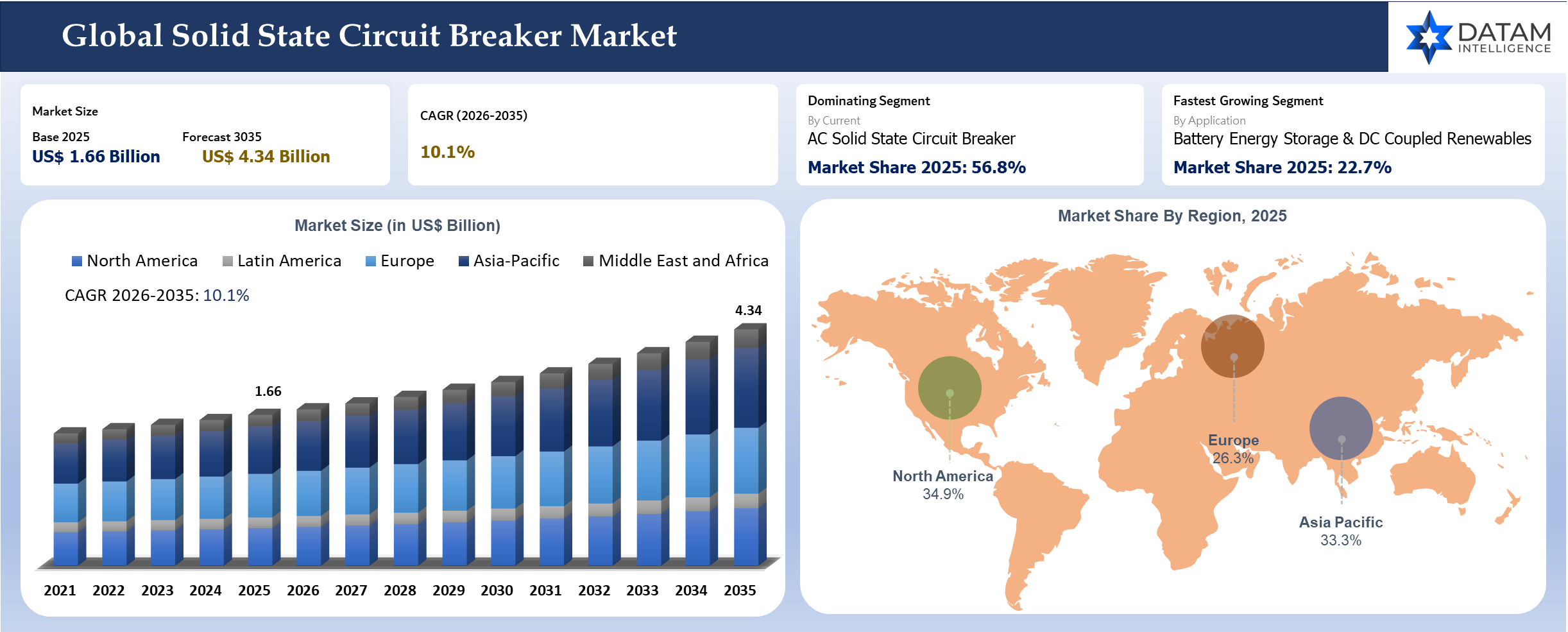

The global solid-state circuit breaker market reached US$ 1.66 billion in 2025 and is expected to reach US$ 4.34 billion by 2035, growing with a CAGR of 10.1% during the forecast period 2026-2035. The solid-state circuit breakers allow ultra-fast fault disconnection within microseconds, which are essential for securing infrastructures that have evolved using power electronics-based technologies, including data centers, EV charging stations and renewable energy plants. The invertor-based systems are dependent on sophisticated protection schemes due to low system inertia and two-way flow of energy, making the adoption of solid-state technology more prevalent.

The solid-state circuit breakers complement the current requirements in the sense that they facilitate real-time monitoring and predictive maintenance and can be seamlessly integrated with digital substations. Wide bandgap semiconductor technology, including silicon carbide (SiC) and Gallium Nitride (GaN) technology, is making solid-state breakers more viable due to higher efficiency and cooling capabilities.

Solid State Circuit Breaker Industry Trends and Strategic Insights

- SSCBs become increasingly relevant in scenarios where rapid fault detection and digital coordination outweigh the economic considerations typical of conventional breakers.

- Battery energy storage, electric vehicle charging stations, marine applications, data center distribution networks and industrial DC systems provide clear demand drivers for the technology.

- The market is advancing as reliable product certification and application guidance facilitate the commercial assessment of solid-state protection solutions.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 1.66 Billion | |

| 2035 Projected Market Size | US$ 4.34 Billion | |

| CAGR (2026-2035) | 10.1% | |

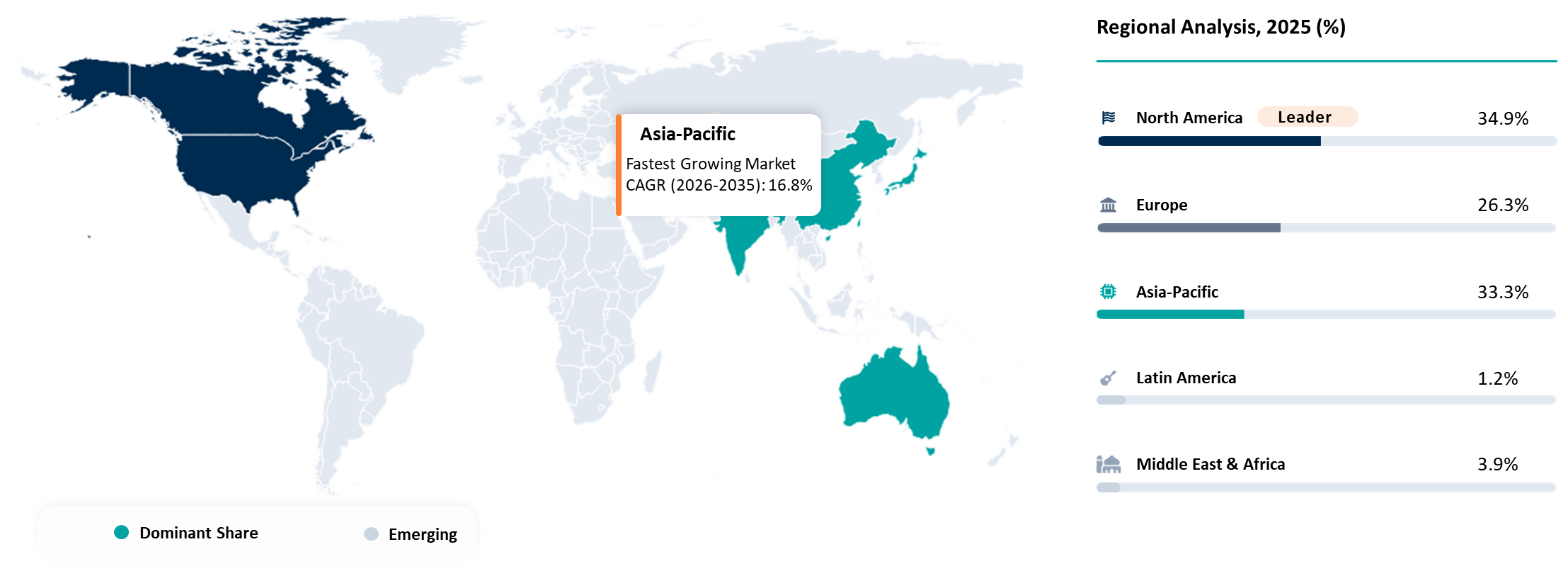

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Current | DC Solid State Circuit Breaker, AC Solid State Circuit Breaker, Hybrid Solid State Circuit Breaker | |

| By Voltage Range | Low Voltage, Medium Voltage, High Voltage Direct Current | |

| By Device Topology | MOSFET Based, IGBT Based, Wide Bandgap Semiconductor Based, Hybrid Mechanical and Solid-State Topology | |

| By Application | Battery Energy Storage and DC Coupled Renewables, EV Fast Charging and Charging Hubs, Data Centers and AI Power Distribution, Marine and Shipboard Power, Industrial DC Microgrids, Rail and Traction Power | |

| By Protection Function | Ultra-Fast Fault Isolation, Selective Protection, Arc Flash Reduction, Remote and Intelligent Protection | |

| By Region | North America | USA, Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

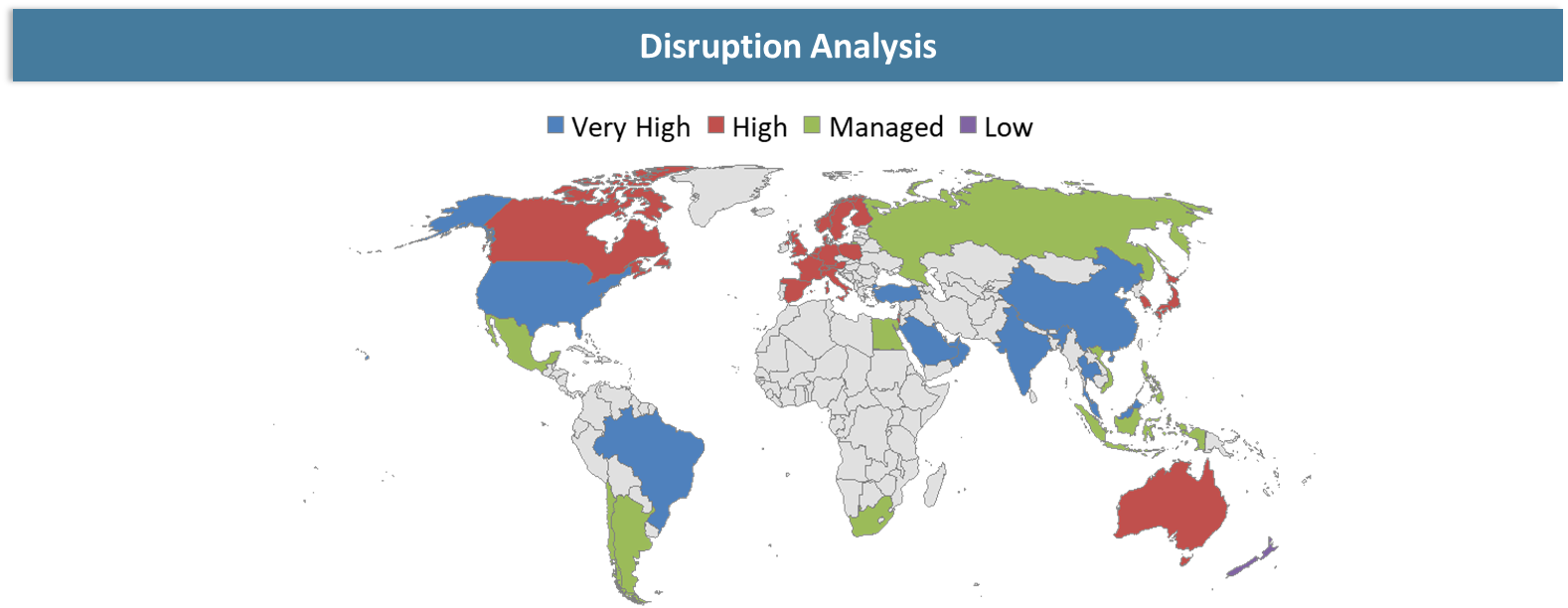

Disruption Analysis

The largest disruption is the transition from a system that considers breaker performance predominantly based on capacity and durability to one that bases it on speed, intelligence and compatibility with DC system architectures. Conventional electrical expertise may be required, but semiconductor and power electronics knowledge has become increasingly important in protection-system design. Another disruptive trend is the adoption of DC power distribution in contexts where previously only AC was expected.

Battery block storage, electric vehicle charging stations, photovoltaics with DC power distribution and data centers designed around DC all represent contexts in which conventional assumptions about protection systems do not sit comfortably. It creates clear possibilities for the adoption of SSCBs. When products are developed beyond conceptual demonstration and enter a standards-based offering phase, buyers gain greater comfort. It removes one of the most significant barriers to adoption seen historically within critical infrastructure contexts. As power systems incorporate higher-value electronics, selective fast-breaking protection is easier to justify.

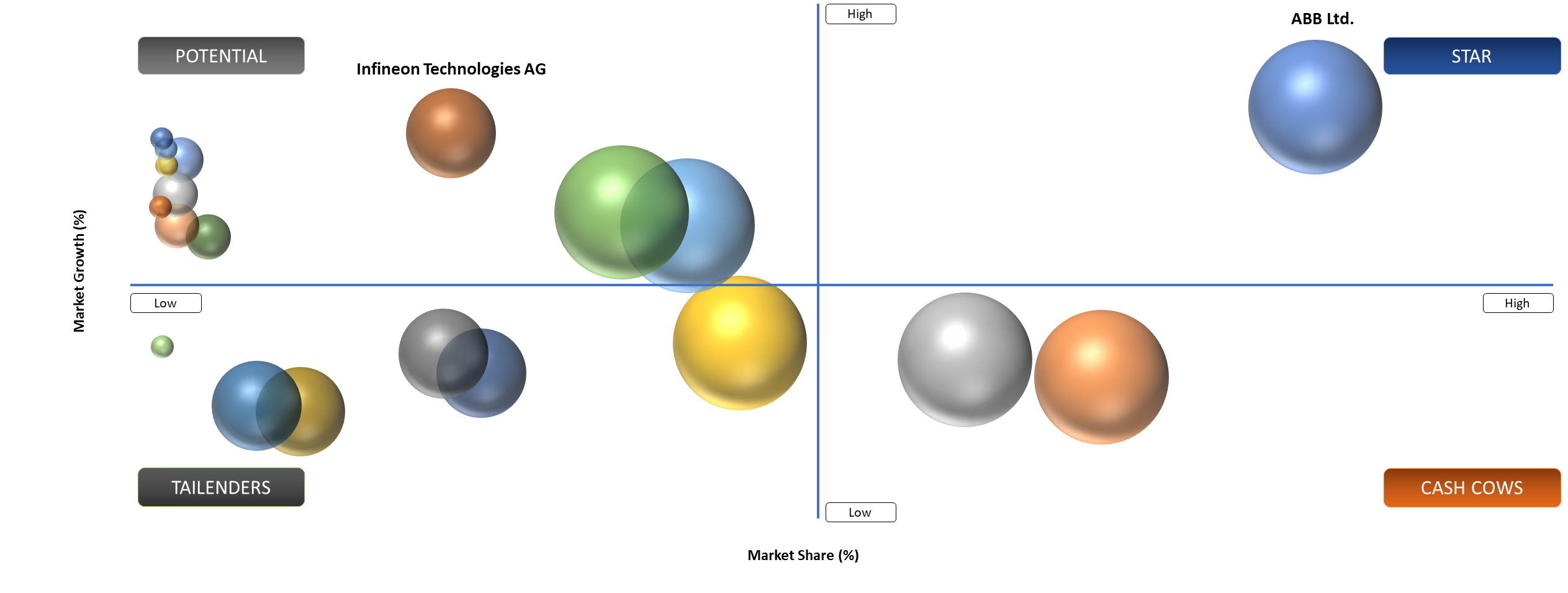

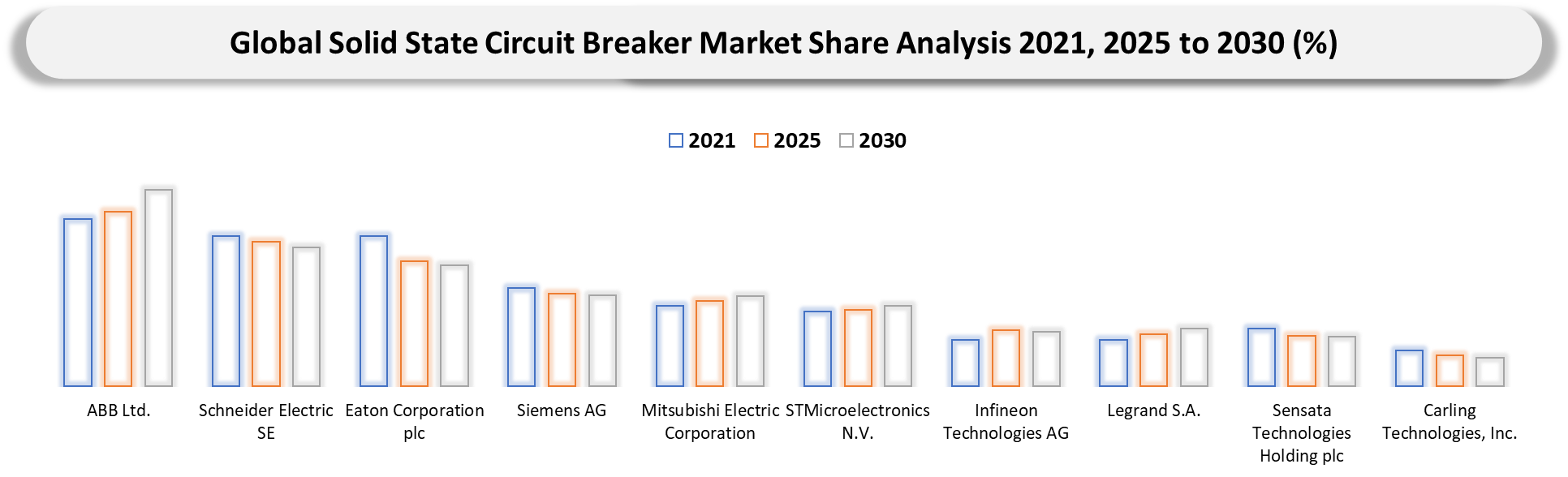

BCG Matrix: Company Evaluation

ABB Ltd., Schneider Electric SE and Eaton Corporation plc have been chosen for the stars category because of their credentials in electrical distribution, coupled with the capability to apply innovative protection technologies within practical settings. The star category's prominence is further demonstrated by the inclusion of ABB, which stands out because of the position created by Infinitus through solid-state DC protection certified by IEC. Companies that fall under the potential category have great advantages based on channel strengths, base-of-installation strength and the breadth of the electrical distribution range, even if their SSCB products lag those of breakers.

Market Dynamics

High-value DC and power-electronics systems need much faster fault isolation than conventional protection

In terms of energy storage, electric vehicle charging stations, shipboard DC systems and high-density computing infrastructure, a fault condition can rapidly spiral out of control and threaten the expensive equipment that follows. As such, end users are increasingly recognizing the economic benefits of extremely rapid interruption and selective fault isolation.

In situations where a slower or poorly timed interruption sequence occurs within a battery string, charging station or highly concentrated power rack design, the stress induced on equipment can be far greater than the cost of the circuit breaker itself would imply. It makes solid-state technology more economical within certain specific application areas. However, a greater tolerance for digital control of power systems is contributing to the rising demand.

High cost and thermal-design complexity still limit adoption outside premium use cases

SSCBs are faster and more intelligent as well, but at the same time, they are more expensive in terms of hardware and power loss compensation as compared to conventional breakers. It makes users hesitant when it comes to their adoption of situations that do not justify their monetary benefit. It leads to a situation in the market where such devices must be marketed based on suitability of application and not by replacing conventional breakers.

Segmentation Analysis

The global solid-state circuit breaker market is segmented based on the current, voltage range, device topology, application, protection function and region.

SiC-Driven Solid-State Circuit Breakers Accelerate Protection in Battery Storage and EV Charging Ecosystems

Battery energy storage is ideally suited to the application due to the DC bias of battery installations, their dense connectivity and sensitivity to fault propagation. The benefit of fast isolation becomes obvious and operators seek to minimize downtime, safeguard converters and strings of batteries while minimizing potential collateral damage to the entire system. As more storage installations come online, developers and integrators have a greater impetus to make installations safe, reliable and maintainable.

The SIC-based switches will enable selective protection that cannot be accomplished using existing products in certain architectures. Charging hubs, on the other hand, involve large power electronics, customer satisfaction considerations and expanding DC systems in one place. When faults affect a charging installation, they could cause losses directly by reducing service time, increasing repair costs and damaging customer satisfaction. Fast chargers, energy storage systems, photovoltaic systems and backend systems are currently designed as units. In such applications, digital-aware protection solutions are preferable to purely passive fault isolation.

Geographical Penetration

Asia Pacific Emerges as High-Growth Hub for Solid-State Circuit Breakers Amid Grid Modernization and Electrification Surge

The Asia-Pacific is currently the fastest developing market for solid-state circuit breakers (SSCBs) due to the growing electrification of the area, expanding renewable energy and major grid upgrade programs. In Southeast Asia and South Asia, there are ongoing investments from the Asian Development Bank worth millions of dollars towards various energy transitions and smart grids.

The fast-growing developments being made within the data center industry and in the use of electric mobility solutions, with the Asia-Pacific being home to some of the world’s fastest-growing data centers, according to the International Energy Agency. Moreover, the use of HVDC systems and microgrids in India, China, South Korea and Australia, among other countries, has led to higher usage of SSCBs, as regular mechanical circuit breakers are unable to keep up with the demands of DC and bidirectional power applications.

China Solid State Circuit Breaker Market Trends

China is the primary contributor to the adoption of solid-state controllable circuit breakers in the Asia-Pacific region, driven by substantial investments in ultra-high voltage (UHV) transmission and power electronics. The state-owned power companies, including State Grid Corporation of China, are investing in solid-state and hybrid DC circuit breakers in their UHVDC applications, as rapid fault clearance is necessary for system reliability. Large amounts of research and development funding in billions are being made available each year for advanced wide bandgap semiconductors like SiC and GaN, which play an important role in the operation of SSCBs.

Japan Solid State Circuit Breaker Market Trends

Japan's market for solid-state circuit breakers is defined by innovation, robust research and development initiatives and a keen interest in developing resilient power grids and efficient energy utilization practices. Over the years, Japan has been making efforts to upgrade its power systems, which have seen renewables generating more than 20% of total electricity production in recent times, as stated by the Ministry of Economy, Trade and Industry. In addition, due to Japan's growing concern for disaster-proof infrastructure construction following catastrophes such as the Fukushima Daiichi nuclear disaster, there have been more investments in smart grid and microgrid systems that can operate autonomously and isolate faults quickly.

Competitive Landscape

- Competition exists between electrical legacy firms and semiconductor-based enablers. ABB Ltd., Schneider Electric SE, Eaton Corporation plc and Siemens AG are important due to their knowledge of channel requirements, certification considerations and system integration. Semiconductor firms, including STMicroelectronics N.V. and Infineon Technologies AG, are important due to device performance and control designs.

The key competitive advantage is going to belong to players who will be able to integrate these two areas. An excellent engineering solution for SSCBs without certification, thermal management and support will struggle. Similarly, a great distribution solution without solid-state breaker technology will struggle in premium DC markets.

Key Developments

- April 2026: STMicroelectronics N.V. released silicon carbide power devices optimized for solid-state breakers, enabling faster switching speeds and improved thermal efficiency in DC systems.

- March 2026: Schneider Electric SE expanded EcoStruxure power platform integrating solid-state protection, enabling real-time monitoring and predictive maintenance for data centers and smart grids.

- March 2026: Infineon Technologies AG expanded CoolSiC portfolio supporting solid-state breaker architectures, enhancing efficiency and reliability for EV charging and data center applications.

- March 2026: Delta Electronics, Inc. launched smart energy solutions integrating solid-state protection for EV charging infrastructure and high-efficiency data center power distribution.

- February 2026: Mitsubishi Electric Corporation enhanced power semiconductor-based protection systems supporting high-speed switching and arc-free interruption for renewable and industrial DC networks.

- February 2026: Toshiba Corporation advanced power semiconductor modules supporting solid-state circuit breakers, improving high-voltage DC protection efficiency and switching performance.

- February 2026: Texas Instruments incorporated released advanced gate drivers enabling precise control in solid-state breakers, improving switching speed and system-level reliability.

- January 2026: Siemens AG advanced digital switchgear portfolio integrating solid-state protection and IoT-enabled diagnostics for grid modernization and industrial automation deployments.

- January 2026: Littelfuse, Inc. expanded solid-state protection portfolio with fast-acting semiconductor-based breakers for industrial automation and battery energy storage applications.

December 2025: Fuji Electric Co., Ltd. introduced next-generation power electronics for solid-state breakers, enhancing reliability in industrial automation and renewable energy integration systems.

Why Choose DataM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

Target Audience

- Battery Energy Storage Developers and Integrators: Project teams seeking faster fault isolation and better protection coordination in DC-rich storage architectures.

- EV Charging Infrastructure Operators: Charging-network owners and site integrators evaluating premium DC protection for uptime, selective isolation and equipment safety.

- Data Center Power Architecture Teams: Operators, designers and electrical consultants building denser power-distribution environments for AI and mission-critical computing loads.

- Marine, Rail and Industrial DC System Designers: Engineering teams responsible for compact, high-reliability electrical systems where conventional protection may be too slow or bulky.

- Electrical Equipment OEMs and Panel Builders: Companies exploring how solid-state protection can be packaged into next-generation power-distribution platforms.

- Semiconductor and Power Electronics Companies: Device suppliers, control-IC vendors and module manufacturers enabling faster switching and protection intelligence.

- Utility and Microgrid Innovators: Stakeholders assessing premium protection in advanced DC feeders, resilient microgrids and digitally managed electrical systems.

- Investors and Strategic Technology Buyers: Capital providers tracking where intelligent protection can become a differentiated layer in modern electrification markets.