Secondary Battery Materials Market for Lithium-Ion Batteries Market Definition and Overview

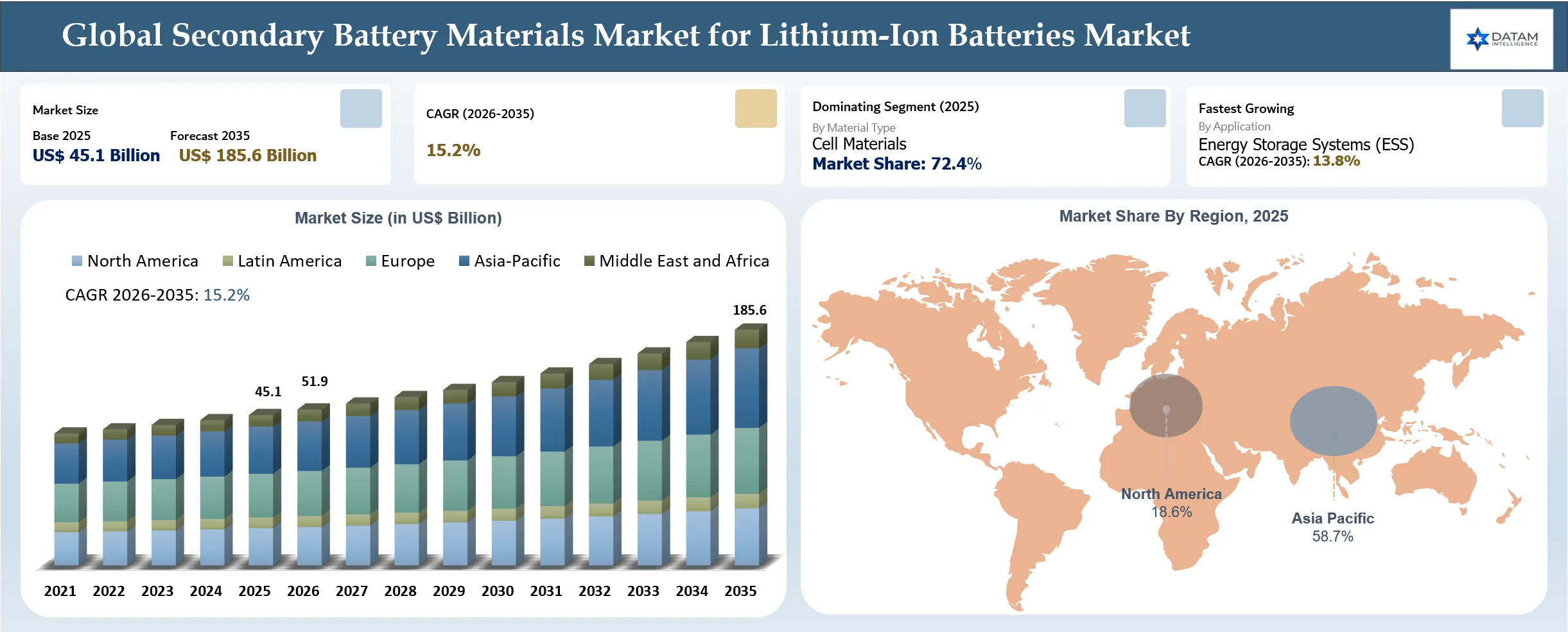

The global secondary battery materials market for lithium-ion batteries market reached USD 45.1 billion in 2025 and is expected to reach USD 185.6 billion by 2035, growing with a CAGR of 15.2% during the forecast period 2026-2035, due to rapid investment into battery gigafactories; accelerated production of electric vehicles, as well as increased stationary energy storage capacity, which is contributing to higher requirements for cathode materials, graphite anodes, electrolytes, separators, as well as current collectors. According to the International Energy Agency (IEA), the global lithium-ion battery market surpassed USD150 billion in 2025 with over a 20% increase since 2024 owing to significant momentum within the entire battery value chain.

The IEA also stated that the average price of battery packs was reduced by 8% in 2025, whereas Lithium Iron Phosphate (LFP) batteries became almost 15% cheaper. LFP batteries became over 40% cheaper than nickel manganese cobalt (NMC) batteries. At the same time, commercialization of silicon-rich anodes, electrolyte innovation, dry electrode manufacturing, as well as battery recycling technology, became an impetus for innovation within the battery materials value chain. Nevertheless, fluctuations in the prices of lithium, nickel, graphite, as well as cobalt are influencing the procurement process along with the concentration of critical minerals processing and battery-grade materials processing. A joint venture between N.A.N. GreenMet and Silox to establish an advanced lithium-ion battery recycling plant in the state of Andhra Pradesh. The initiative will take place in two stages and will aim for a capacity of 40,000 tons per year (TPA) of battery waste shredding and 20,000 TPA of hydrometallurgical refining to extract lithium, cobalt, nickel, and manganese from batteries. In addition, the plant will make battery-grade metal salts, pCAM, and CAM to contribute to the domestic supply chain of critical minerals in India.

Key Takeaways

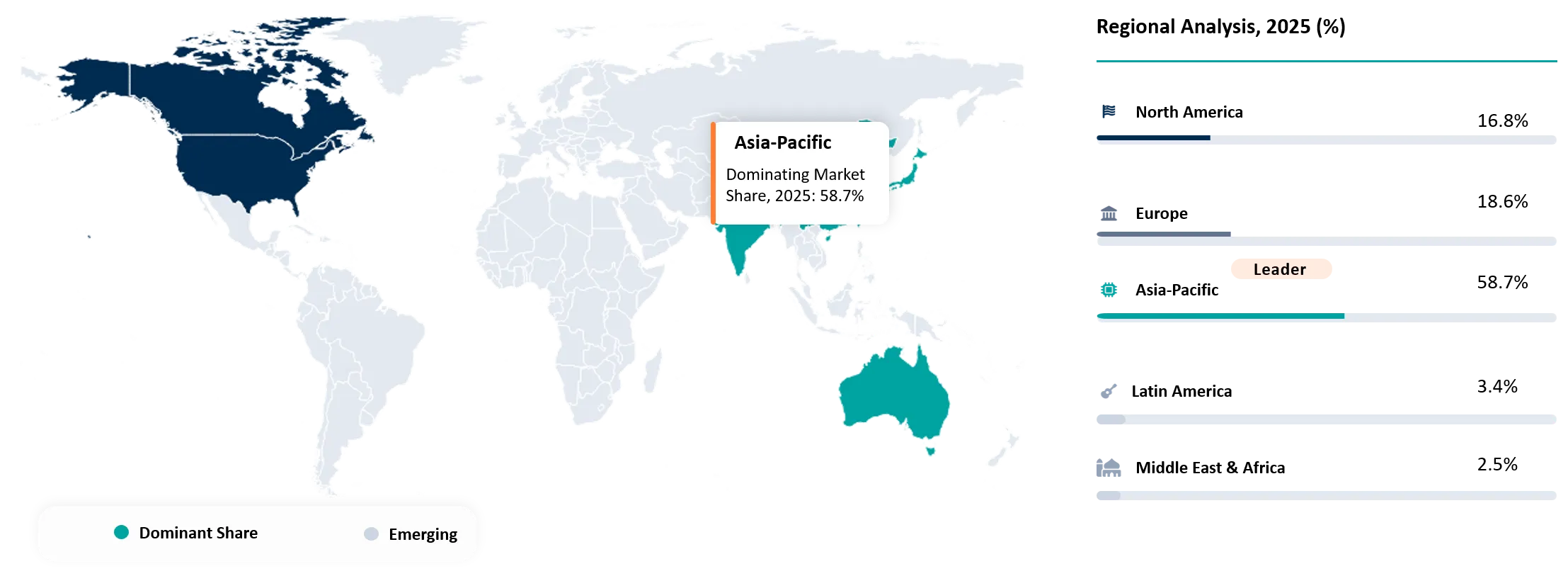

- Asia-Pacific dominates the global Secondary Battery Materials Market for Lithium-Ion Batteries, with a 58.7% market share in 2025. China was a major contributor to the market, representing over 75% of the total global lithium-ion battery production capacity.

- The Cell Materials sub-segment had the largest share in the global secondary battery market for Lithium-ion Batteries, with a market share of 72.4% in 2025. This is attributed to the rising total global production capacity of Lithium-ion batteries, which crossed 4 terawatt hours (TWh).

- The average price of battery packs fell by 8% in 2025, whereas LFP batteries fell to almost 15% below their previous prices. As a result of such changes in the price level, LFP batteries were about 40% less expensive than NMC batteries.

- In September 2024, the United States Department of Energy funded $3 billion in 25 factories for battery manufacturing and recycling. The private sector ventures will create 8,000 jobs during the construction phase and 4,000 permanent job positions in 14 states.

Secondary Battery Materials Market for Lithium-Ion Batteries Market Industry Trends and Strategic Insight

- Lithium Iron Phosphate (LFP) technology has been changing the dynamics of material consumption throughout the battery value chain.

- Utility-scale battery installations are increasing the purchase of cathode, anode, electrolyte, separator, and copper foil materials, thus diversifying the demand pattern of the industry by lowering its dependency on automobiles.

- Silicon-based anode technology is moving towards commercial by the cell manufacturers have started to incorporate anode technology that uses graphite combined with silicon to increase energy density and fast charging capacity.

- Dry electrode fabrication is transforming the economic viability of battery material processing, it led to decreased energy use, increased process simplicity, and less need for capital-intensive drying processes while requiring more materials tailored to dry processing.

- The location of refining facilities for precursors and batteries is receiving significant investments. Governments are promoting local production of cathode precursors, lithium chemicals, graphite processing, and electrolytes using inducements intended to build national battery value chains.

Secondary Battery Materials Market for Lithium-Ion Batteries Market Scope

| Metrics | Details | |

| 2025 Market Size | USD 45.1 Billion | |

| 2035 Projected Market Size | USD 185.6 Billion | |

| CAGR (2026-2035) | 15.2% | |

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | North America | |

| By Material Type | Cell Materials, Module Materials, Pack Housing Materials | |

| By Battery Chemistry | Lithium Iron Phosphate (LFP), Nickel Manganese Cobalt (NMC), Nickel Cobalt Aluminium (NCA), Lithium Cobalt Oxide (LCO), Lithium Manganese Oxide (LMO), Others | |

| By Battery Form Factor | Cylindrical Batteries, Prismatic Batteries, Pouch Batteries | |

| By Application | Electric Vehicles (EVs), Energy Storage Systems (ESS), Consumer Electronics, Power Tools, Industrial Equipment, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Türkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Secondary Battery Materials Market for Lithium-Ion Batteries Market Disruption Analysis

Rapid Commercialization of Sodium-Ion Batteries Reshaping the Secondary Battery Materials Supply Chain

The Secondary Battery Materials for Lithium-Ion Batteries Market faces a disruption due to the commercialization of sodium-ion batteries, especially for stationary ESS, electric two-wheelers, and entry-level electric vehicles. Contrary to lithium-ion batteries, sodium-ion batteries do not require any lithium, nickel, cobalt, or, in certain cases, high-purity graphite, thus posing an uncertain future ahead for suppliers of traditional secondary battery materials. Despite the expected dominance of lithium-ion batteries in the market for their high energy density for the forecast period, sodium-ion batteries are gradually becoming an economically viable alternative. However, in 2025-2026, the process of commercialization gained much momentum; for example, CATL started manufacturing its second generation of sodium-ion batteries with a capacity of more than 200 Wh/kg, and BYD and other Chinese battery makers announced sodium-ion battery use for compact electric vehicles and stationary energy storage projects.

According to the International Energy Agency (IEA), the world battery demand exceeded 1 TWh in 2025, with continued rapid growth of stationary energy storage systems being installed, which creates favorable conditions for cheaper batteries. On the other hand, according to BloombergNEF (BNEF) forecast, sodium-ion batteries will take a greater share of stationary storage and low-cost mobility markets in the following decade, which means that there is a need for battery material suppliers to diversify their portfolios from solely lithium-based to other battery materials.

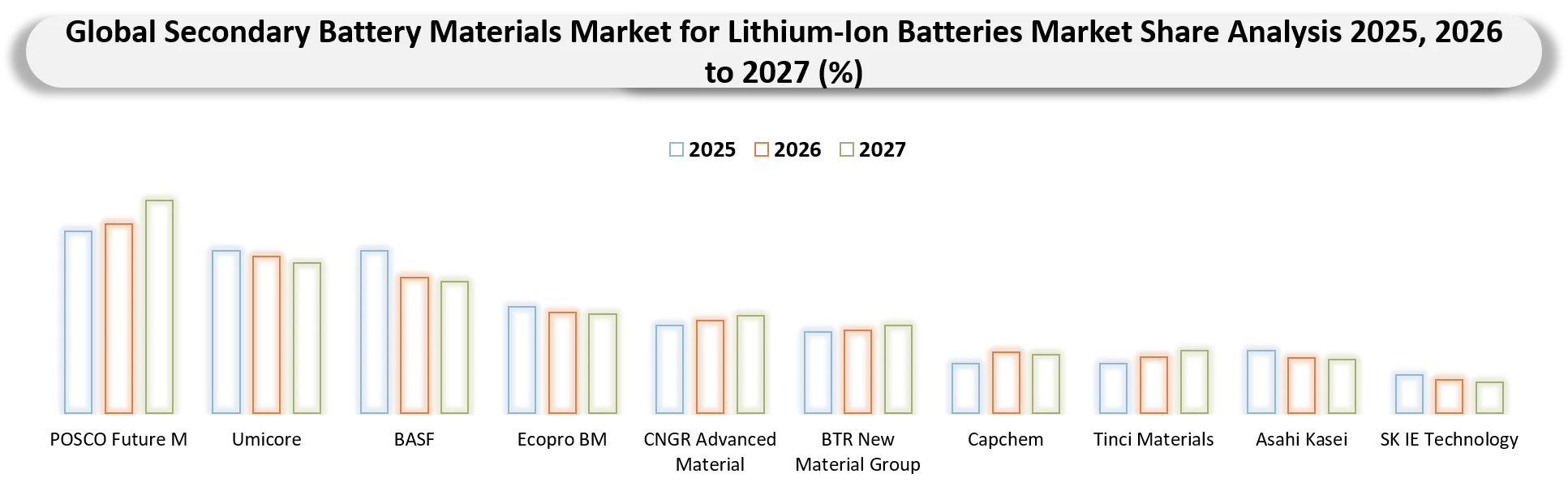

Secondary Battery Materials Market for Lithium-Ion Batteries Market BCG Matrix: Company Evaluation

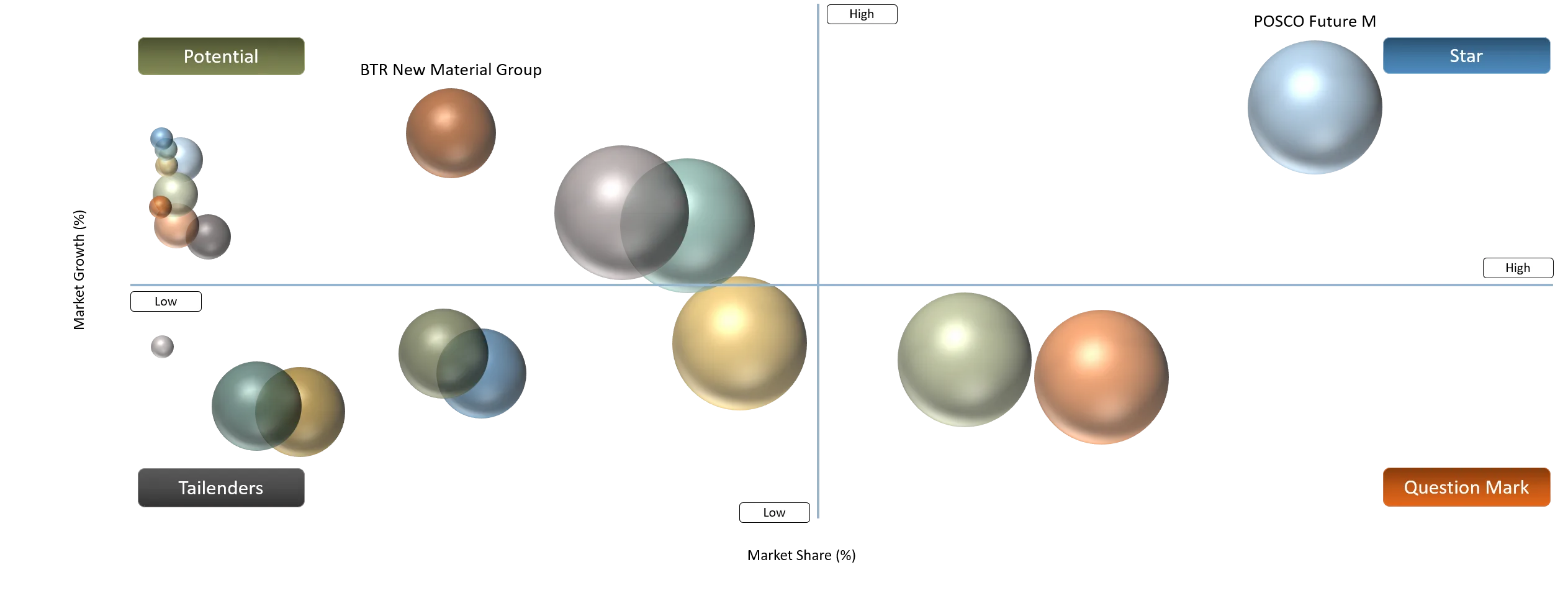

Star companies are POSCO Future M and Umicore because of the dominant position held by these two firms within the value chain of battery materials globally, thanks to their huge inventory of cathode active materials, supply contracts with battery makers, and constant investment in future battery materials. This is possible due to their strong position within fast-growing electric vehicle and energy storage segments, together with capacity expansions within North America, Europe, and Asia. Question marks include BASF, Ecopro BM, and CNGR Advanced Materials because they are scaling up their production of cathode active materials and precursor technologies due to increasing demand for lithium-ion batteries.

Potential companies include BTR New Material Group, Capchem, and Tinci Materials, who are profiting from rising demand in advanced graphite anode materials, battery electrolyte solutions, lithium salt materials, and electrolyte additives. These companies have high technology capabilities and increasing production capacity, especially in China, as well as growing foreign investments aimed at producing batteries elsewhere in the world. Tailenders consist of Asahi Kasei and SK IE Technology, which are well-established manufacturers of lithium-ion battery separators, but have a more limited range of products than diversified battery materials manufacturers.

Secondary Battery Materials Market for Lithium-Ion Batteries Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

The Rapid Growth of the Lithium-Ion Battery Manufacturing Capabilities Globally

| 40% | Very High |

EV battery cells, Energy Storage Systems (ESS), Consumer electronics, Industrial batteries

| Accelerates investments in cathode, anode, electrolyte, separator, and current collector production while driving global battery material capacity expansion. |

Increasing Deployment of Energy Storage Systems (ESS) on a Grid Scale

| 25% | High | Utility-scale ESS, Commercial & Industrial ESS, Renewable energy integration | Diversifies battery material demand beyond automotive applications and increases long-term consumption of LFP cathodes, graphite anodes, and electrolytes. |

Investments in Battery Recycling and Circularity of Materials Recovery

| 16% | Medium-High | End-of-life EV batteries, Manufacturing scrap recycling, Closed-loop supply chains | Expands secondary sourcing of lithium, nickel, cobalt, graphite, copper, and aluminum while improving raw material security and sustainability. |

Increasing Need for Battery-Grade High Purity Lithium Chemicals

| 20% | High | Cathode production, Electrolyte manufacturing, Lithium refining | Encourages investments in lithium refining capacity, high-purity lithium compounds, and localized chemical processing to support battery-grade material demand. |

Growing Demand for High Performance Electrolytes and Advanced Separators

| 14% | Medium | Fast-charging EV batteries, Premium EVs, Solid-state battery development, ESS | Promotes commercialization of advanced electrolyte formulations, ceramic-coated separators, and high-voltage battery materials that improve battery safety and performance. |

The Rapid Growth of the Lithium-Ion Battery Manufacturing Capabilities Globally

The rapid expansion of global manufacturing capacity for lithium-ion batteries is one of the primary drivers of exponential growth in the demand for secondary battery materials, including cathode materials, graphite anodes, electrolytes, separators, copper foil, and aluminum foil. According to the International Energy Agency (IEA), the entire global lithium-ion battery market exceeded $150 billion in 2025 and has grown each year by over 20% since 2024, as a result of a tremendous amount of investment throughout the supply chain related to batteries. The IEA also estimated that global battery manufacturing capacity exceeded 3 terawatt-hours annually in 2025, made possible by the commissioning of numerous gigafactories located throughout China, North America and Europe, as well as India and Southeast Asia. In parallel, the battery sector is becoming more cost-effective, accelerating large-scale material consumption.

For instance, in September 2024, the U.S. Department of Energy (DOE) released more than USD 3 billion in investments in 25 battery manufacturing and recycling facilities in 14 states in the USA. These facilities are projected to generate over 8,000 construction jobs and more than 4,000 full-time operational jobs, and help expand the domestic capacity for critical minerals processing for batteries, battery components manufacturing, battery cells manufacturing, and battery recycling.

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

Frequent fluctuations in lithium, nickel, cobalt, and graphite affect cost, strategy, and profits for battery material producers.

| 22% | Raw material procurement and production cost | Cathode materials, anode materials, electrolyte production, battery chemical manufacturing | Increases procurement uncertainty, compresses manufacturer margins, and accelerates long-term sourcing contracts, recycling investments, and upstream integration strategies. |

Growing demand for lithium carbonate, lithium hydroxide, artificial graphite, nickel sulfate, and cobalt sulfate is putting pressure on the upstream supply chains.

| 18% | Critical mineral availability | Battery-grade lithium refining, cathode precursor production, graphite processing | Intensifies competition for battery-grade raw materials, extends procurement lead times, and encourages capacity expansion in mining and refining. |

Supply Chain Disruptions and Geopolitical Risk are factors that affect the availability of raw materials for batteries.

| 19% | Global supply chain resilience | International sourcing, battery manufacturing, regional material supply | Drives localization of refining and material production, supplier diversification, and strategic stockpiling to reduce dependence on concentrated supply regions. |

Increasing environmental compliance issues and refining regulations affect operations and increase costs.

| 13% | Refining operations and regulatory compliance | Lithium refining, graphite purification, chemical processing facilities | Raises operating and compliance costs, increases capital expenditure for environmental upgrades, and delays new refining and processing projects. |

Frequent fluctuations in lithium, nickel, cobalt, and graphite affect cost, strategy, and profits for battery material producers

One of the key constraints that impacts the Secondary Battery Materials Market for Lithium-Ion Batteries is the volatility associated with the pricing of battery mineral raw materials, such as lithium, nickel, cobalt, and graphite. Manufacturers of battery materials depend on these raw materials to manufacture cathodes, anodes, electrolyte, and precursors, which makes them highly dependent on the pricing of commodities. Though the correction in lithium prices from the peak period of 2022–2023, there have been some price swings in the year 2025–2026 due to various reasons like changes in the demand for EVs, inventory management, and new mining operations, in addition to changes in global trade dynamics. On the other hand, USGS has reported the global mine production of lithium to be around 240,000 metric tons during 2025.

For instance, in February 2026, the U.S. Geological Survey (USGS) reported that the world mineral market witnessed considerable price instability in 2025, with lithium prices dropping 24% and nickel prices reducing 11%. Despite the reduction in lithium prices, there was an increase of 50% in U.S. cobalt production and 34% in nickel production, while the value of cobalt and nickel increased 80% and 19%, respectively, from 2024.

Secondary Battery Materials Market for Lithium-Ion Batteries Market Segment Analysis

The global secondary battery materials market for lithium-ion batteries is segmented based on material type, battery chemistry, battery form factor, application, and region.

Cell Materials Dominate the Secondary Battery Materials Market Due to Their Fundamental Role in Lithium-Ion Cell Manufacturing

The Cell Materials category holds the largest segment of the Global Secondary Battery Market for Lithium-Ion Battery, with a market share of 72.4% in 2025, because it contains all the main electrical components (cathodes, anodes, electrolytes, separators, current collectors, cell casing) which allow the battery's performance characteristics such as power and energy capacity, cycle life, charging performance, and safety to be understood. The increased demand for these components was driven by the surge in global lithium-ion battery production that occurred in 2025 and 2026. Benchmark Mineral Intelligence (BMI) estimates that the total global manufacturing capacity of lithium-ion batteries surpassed 4 terawatt hours (TWh) in 2025, with additional manufacturing capacity estimated at more than 1.5 TWh and continuing to create record amounts of demand for cathode and anode materials specifically made for batteries. As per BloombergNEF (BNEF), there was a substantial increase in the total value of the world’s lithium-ion battery market in 2025 as it reached over USD150 billion, along with significant reductions in battery-packed prices below USD100 per kilowatt-hour (kWh), which has resulted in accelerating production of batteries and driving increased demand for battery materials throughout the supply chain.

Simultaneously, investments in gigafactories on a massive scale in China, the USA, Europe, South Korea, and Southeast Asia have enhanced the purchase of high-purity cell materials as manufacturers bring production closer to home and source raw materials for the long term. Cell Materials continue to be the most significant money-making division, having the highest share of material demands.

Secondary Battery Materials Market for Lithium-Ion Batteries Market Geographical Penetration

Rapid Expansion of Battery Material Manufacturing and Integrated Supply Chains Strengthens Asia-Pacific's Market Leadership

The Asia Pacific region is dominating the Secondary Battery Materials Market for Lithium-Ion Batteries Market, with a market share of 58.7% in 2025, due to an extremely integrated ecosystem for battery materials, robust refining facilities, and manufacturing capacity for battery cells in countries like China, Japan, South Korea, and Southeast Asian nations. This region is leading in producing cathode active materials, artificial graphite, lithium chemicals, electrolyte, separators, and copper foil, providing the majority of the world’s lithium-ion battery producers. Continued leadership in the region has been demonstrated by massive investments in battery material manufacturing and local supply chains. In the period from 2025 to 2026, businesses such as POSCO Future M, Ecopro BM, CNGR Advanced Material, BTR New Material Group, Tinci Materials, and Capchem have made announcements about their expansion capacities of cathode material manufacturing, graphite anodes, electrolytes, and lithium chemicals to cope with demand from the EV and ESS manufacturing industries.

Meanwhile, governments in China, South Korea, Japan, and India have made huge investments in battery industry clusters, critical minerals processing, and gigafactory ecosystem development. For instance, in March 2026, Fino, a South Korean-based company that produces materials for secondary batteries, received an investment of USD 48 million (KRW 70 billion) from Samsung SDI and an international financial institution based in Singapore. This investment will help create domestic manufacturing plants through Fino's joint venture with POSCO Future M to produce NCM and LFP battery materials.

China Secondary Battery Materials Market for Lithium-Ion Batteries Market Trends

China holds the dominant position in the Asia-Pacific Secondary Battery Materials Market for Lithium-Ion Batteries owing to an integrated battery materials supply chain, refinery facilities, and dominance in the manufacture of cathodes, synthetic graphite, lithium chemicals, electrolytes, separators, and copper foil. With a vertically integrated ecosystem, China allows cooperation between mining companies, refiners, battery materials producers, cell makers, and EV OEMs, which fast-tracks the deployment of next-generation batteries in a cost-effective manner. As per Benchmark Mineral Intelligence (2025), China held more than 75% of the world’s lithium-ion battery manufacturing capacity, while according to USGS 2026, China retained its dominance in the processing of battery-grade graphite and lithium chemicals.

For instance, in June 2026, Semcorp (Yunnan Energy New Material), a Chinese producer of lithium-ion battery separators, made a deal to acquire a 100% stake in SK Battery Materials Technology from SK IE Technology in its entirety for RMB 400 million (USD 60 million). This transaction will bring a lithium-ion battery separator plant based in Jiangsu, China, with an annual production capacity of about 940 million m², into Semcorp's possession, thus allowing Semcorp to rapidly increase its separation material production capacity, capacity utilization rate, and the supply of battery materials.

India Secondary Battery Materials Market for Lithium-Ion Batteries Market Outlook

India is emerging as the fastest-growing country in the Asia-Pacific Secondary Battery Materials Market for Lithium-Ion Batteries due to heavy government backing of local battery manufacturing, investment in battery material processing, and rapid localization of the lithium-ion battery value chain. With the introduction of the Advanced Chemistry Cell (ACC) Production Linked Incentive (PLI) Scheme and the National Programme on Advanced Chemistry Cell Battery Storage, investments in cathode materials, electrolyte production, graphite processing, battery recycling, and cells have been catalyzed. The Indian electric vehicle industry, according to India Brand Equity Foundation (IBEF), will see significant growth in battery manufacturing, as India rapidly builds out its local manufacturing capability to become less dependent on foreign battery materials.

For instance, in December 2025, GFCL EV Products Ltd, which is a subsidiary of Gujarat Fluorochemicals Limited (GFL), secured an approximate USD 50 million investment in equity from the International Finance Corporation (IFC). This will allow for the setting up of India's first integrated battery material manufacturing plant in Jolva, Gujarat. It will be producing various components of lithium-ion batteries such as the LiPF₆ electrolyte salts, electrolyte solutions and additives, LFP cathode active materials, and PVDF/PTFE binders.

Secondary Battery Materials Market for Lithium-Ion Batteries Market Competitive Landscape

- The Secondary Battery Materials Market for Lithium-Ion Batteries consists of three broad categories of participants: battery material manufacturers with integrated operations, cathode and anode material specialists, and electrolyte and separator specialists. POSCO Future M, Umicore, BASF, Ecopro BM, CNGR Advanced Material, and BTR New Material Group are the leading players in this market due to their large-scale manufacturing of cathode active materials, graphite anodes, and precursors to batteries, who serve battery manufacturers such as CATL, LG Energy Solution, Samsung SDI, SK On, Panasonic Energy, and BYD. Capchem and Tinci Materials are market leaders in electrolyte materials due to large-scale production of lithium salts and electrolytes, while Asahi Kasei and SK IE Technology hold strong market positions in lithium-ion battery separators. Competition in this market is growing in terms of vertical integration, localization of battery materials supply chain, raw material offtake agreements, and investments into next-generation materials such as silicon-anodes, LFP cathodes, and solid-state battery materials.

- Key players are POSCO Future M, Umicore, BASF, Ecopro BM, CNGR Advanced Material, BTR New Material Group, Capchem, Tinci Materials, Asahi Kasei, and SK IE Technology.

Key Developments

- December 2025: Neogen Ionics, which is owned by Neogen Chemicals, entered into a joint venture partnership with Morita Investment of Japan to form Neogen Morita New Materials, an organization that will produce and sell solid lithium hexafluorophosphate (LiPF₆), an electrolyte salt used in lithium-ion batteries.

- November 2025: NEO Battery Materials collaborated with Nascent Materials Inc. under a Joint Product Development Agreement to develop superior lithium-ion batteries using silicon-anode material and LFP/LMFP cathode materials.

- November 2025: POSCO announced investments of approximately USD 818 million in lithium projects in Australia and Argentina, ensuring adequate supply of battery-grade lithium, a vital raw material in lithium-ion battery manufacturing.

- November 2025: HS Hyosung Advanced Materials entered into a deal to acquire an 80% share in Extra Mile Materials (EMM), a battery materials company that was spun off from Umicore.

- May 2025: Indonesia and the Philippines launched a Nickel Corridor initiative to improve their nickel supply chain for battery manufacturing purposes. In doing so, they seek to combine the nickel resources of the Philippines and the processing capacity of Indonesia to improve the supply of battery-grade nickel, which is a key ingredient in the production of NMC batteries.

- March 2026: EcoGraf Limited partnered with Taiwan-based Long Time Technology Co., Ltd. for developing technology related to the purification of graphite and anode material used in lithium-ion batteries.

- June 2026: Himadri Speciality Chemical increased its shareholding in International Battery Company (IBC) to 20.47% by investing in a bid to speed up the process of developing advanced lithium-ion battery materials.

Key Procurement Priorities and Buyer Evaluation Criteria

- Organizations investing in the Secondary Battery Materials Market for Lithium-Ion Batteries are now opting for suppliers who can offer high purity and consistency in battery materials that are needed to meet rigorous electrochemical specifications. They prefer to have suppliers with skills in producing cathode active material, graphite anode, electrolyte, separator, and current collector with stable quality and production scale.

- Procurement decisions are being made more frequently taking into consideration the fast growth in electric vehicle (EV) manufacturing, energy storage systems (ESS), and gigafactories. Companies that manufacture batteries and vehicles assess suppliers by how they ensure material availability, localized supply chain support, and cost-effective solutions despite the instability in lithium, nickel, cobalt, and graphite markets.

- Buyers will look at the purity of the material, size distribution, electrochemical behavior, energy density, cycle life enhancement, thermal stability, availability, and price competition when choosing a supplier of battery materials. In particular, suppliers of cathode and anode materials have to consider parameters like the consistency of nickel content, graphite quality, silicon incorporation capability, lithium recycling efficiency, etc.

Why Choose DataM?

- Technological Innovations: Highlights technological innovations in secondary battery materials in lithium-ion batteries such as high-performance cathode materials, anode materials, solid-state battery materials, silicon anodes, lithium recycling techniques, and innovative material compositions to facilitate higher energy density, fast charging, battery longevity, and increased safety in electric vehicle (EV), energy storage system (ESS), and consumer electronics applications.

- Product Performance & Market Positioning: Assesses competition among various material suppliers through energy density, electrochemical behavior, cycle life, thermal stability, cost efficiency, and sustainability, emphasizing how successful companies distinguish themselves through cathode chemistry, graphite substitutes, recycled materials, and vertically integrated battery material supply chains.

- Real-World Evidence: Highlights the use of state-of-the-art secondary battery materials in electric vehicles, energy storage in grids, consumer electronics, and industrial uses, which offer advantages like increased driving range, effective charging of batteries, decreased battery deterioration, safety, and better performance of the battery.

- Market Updates & Industry Changes: Monitors industry developments including growth in battery materials manufacturing, lithium-ion gigafactory investment, recycling activities, partnering, raw material procurement, and regional developments in Asia Pacific, North America, and Europe, enabling localization of the battery value chain.

- Competitive Strategies: Examines the ways top firms improve their competitive position in the marketplace via capacity increases, innovation in technology, partnerships, incorporation of recycling, and advanced battery chemistry investments to counter growing demands by manufacturers of electric vehicles, batteries, and energy storage firms.

- Pricing & Market Access: Elaborates on the pricing structure due to the availability of raw materials, fluctuating prices of lithium and nickel, quality of raw materials, technological processes, size of production, and supply chain linkages, alongside accessibility through battery producers, automakers' OEMs, suppliers of materials, and recycling facilities.

- Market Entry & Expansion: Growth opportunities based on electric vehicles, renewable energy storage, battery recycling, and high-performance battery demand are discussed, along with strategies including regional production facility development, sustainable sourcing, technology differentiation, and strategic alliances to position the company competitively in the global secondary battery materials market.

Target Audience

- Lithium-Ion Battery Manufacturers

- Electric Vehicle (EV) Manufacturers

- Battery Material Suppliers & Chemical Companies

- Battery Recycling Companies

- Energy Storage System (ESS) Providers

- Mining & Mineral Processing Companies

- Government Bodies & Regulatory Authorities