SCD Diamond Cutting Tools Relapping Market Overview

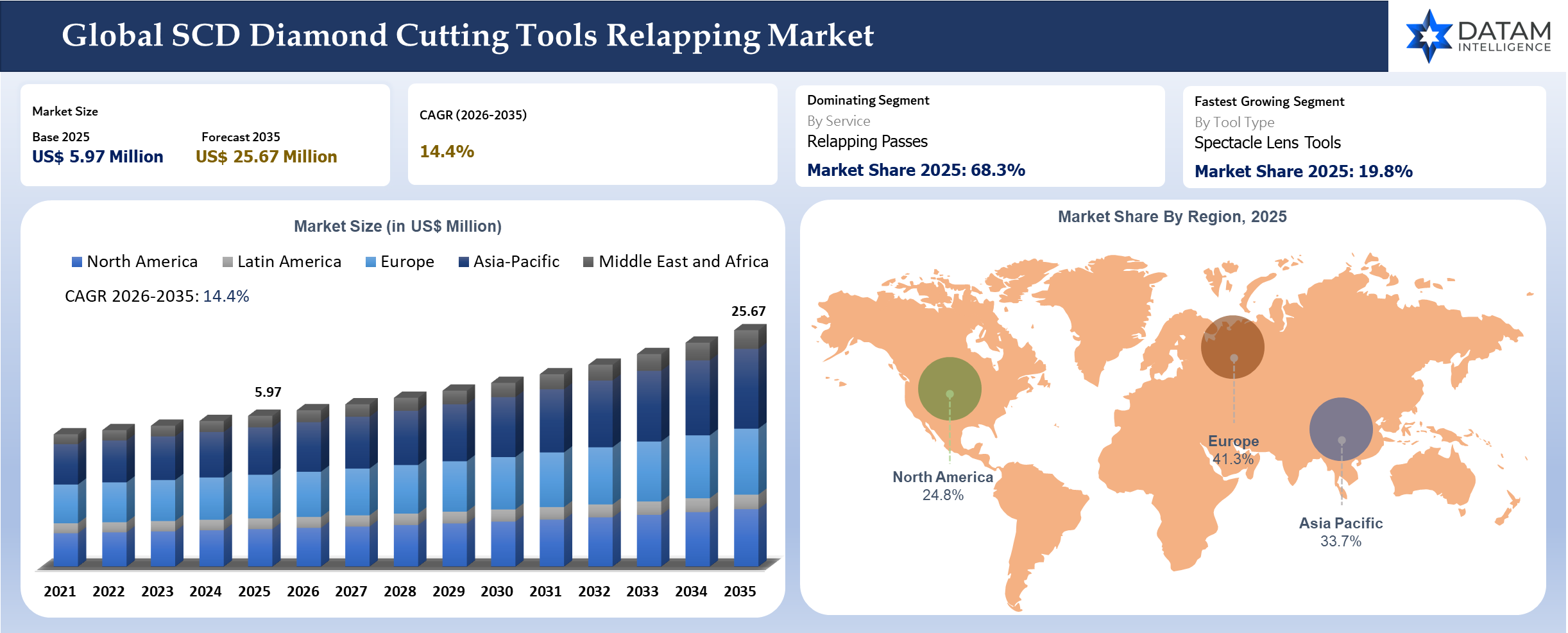

The global SCD diamond cutting tools relapping market reached US$ 5.97 million in 2025 and is expected to reach US$ 25.67 million by 2035, growing with a CAGR of 14.4% during the forecast period 2026-2035. Specialist diamond tool servicing has become a specialist aftermarket market because ultra-precision workshops increasingly prefer controlled tool recovery over immediate replacement. A new diamond turning tool can hold value through several service cycles when the diamond edge only has micro chipping, rake face wear, radius drift or front clearance deterioration. Contour Fine Tooling states that its repair process laps the top rake surface to create an edge equal to a new tool and can add reradiussing or brazing when needed. K and Y Diamond also states that trained staff can relap a diamond tool up to 30 times by removing only the damaged area. Such evidence shows why recurring service revenue has become an important cost control lever for optics, ophthalmic, aerospace, electronics and precision mold makers.

Market demand sits inside a narrow but high-value machining ecosystem. Diamond tools support single-point diamond turning and ultra-precision cutting, where surface finish often needs nanometer-level control rather than conventional machining tolerances. NIST describes diamond turning as the use of special machine tools with single-crystal diamond cutting tools to produce metal optics. Research published through the U.S. National Science Foundation notes that diamond turning and milling can achieve surface roughness of 1 to 10 nm, depending on process parameters and workpiece material. Tool recovery, therefore, protects a production capability that cannot be substituted easily by standard carbide or PCD tooling.

Cost, lead time and repeatability shape purchasing behavior in this market. Micro LAM highlights repair turnaround with a maximum of 3 days for tool relaps. K and Y documentation mentions one day turnaround for serviced tools and one to two weeks for recone work. Gold Technic in Singapore states that restored diamond tools can return to their original condition within 5 to 7 days. Service providers that combine fast turnaround, edge geometry expertise, inspection reports and tool history data gain stronger customer retention because a delayed diamond tool can stop an entire optical lens, infrared lens, hard disk substrate or contact lens mold line.

Industrial diamond supply conditions also support servicing economics. USGS Mineral Commodity Summaries 2026 states that synthetic diamond accounted for more than 99% of global industrial diamond production and that China, the U.S. and Russia produced about 99% of synthetic industrial diamond by quantity in 2025. Even with strong synthetic diamond availability, high-grade single-crystal used in ultra-precision tools requires careful orientation, polishing skill and metrology. Tool recovery helps customers stretch the economic life of qualified tools while reducing scrap risk and repeat qualification effort.

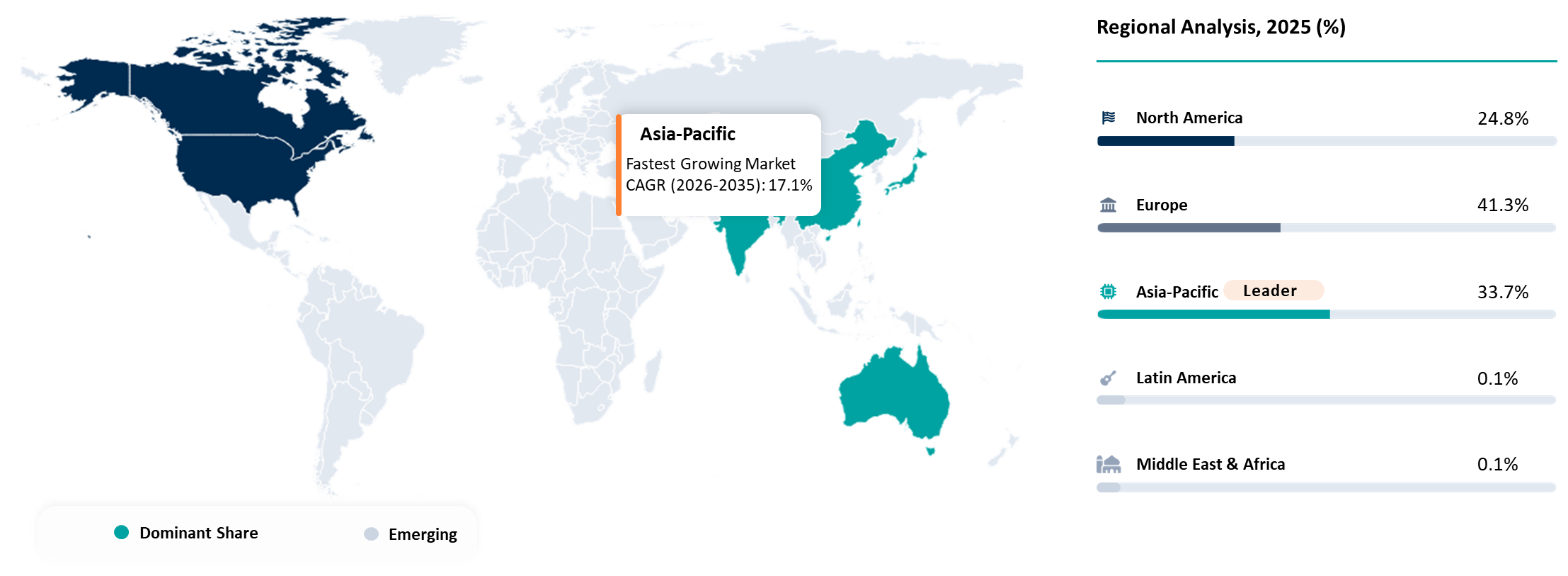

Asia-Pacific carries a strong growth position due to large optical, electronics, watch, jewelry, automotive precision, semiconductor equipment and ophthalmic manufacturing clusters. India is moving from a purely abrasive tool-based to specialist ultra-precision providers. Reliance Diamond Tools, Solar Diamond Tools and Kamala Engineering add broader Indian diamond tooling capacity, which strengthens local sourcing options even when some providers sit closer to adjacent PCD, CBN, dressing and natural diamond tooling than pure single-crystal relap work. Hardten Precision Technologies is the only SCD tool manufacturer and relap service provider in India, based in Surat, that publicly offers tool relapping service and single-crystal tooling for ophthalmic, electro optics, roto gravure, automotive, space and defense and watch and jewelry work.

SCD Diamond Cutting Tools Relapping Industry Trends and Strategic Insights

- Optics shops are asking for tool history, waviness certificates and inspection proof instead of a simple sharpened edge.

- Service decisions are shifting from reactive repair to planned service cycles based on surface finish drift and tool edge inspection.

- Local service capacity in India, Singapore, South Korea and China is reducing dependence on European or North American turnaround for standard geometries.

- Controlled edge recovery is gaining value as freeform optics, infrared lenses and high precision molds require consistent radius and rake geometry.

- Independent service providers are becoming credible alternatives where customers use mixed fleets of Contour, K and Y, Micro LAM, Diatec, Apex or locally sourced tools.

- AI-enabled inspection and tool life logs are beginning to influence service scheduling, even though the market still depends heavily on master craft skill.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 5.97 Million | |

| 2035 Projected Market Size | US$ 25.67 Million | |

| CAGR (2026-2035) | 14.4% | |

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Service | Relapping Passes, Regrinding, Re Radiusing, Recone, Resetting, Rebrazing, Retipping, Full Refurbishment, Inspection And Certification, Process Support | |

| By Tool Type | Single Point Turning Tools, Ophthalmic Tools, Optics Tools, Fly Cutting Tools, Form Tools, Grooving Tools, Boring Tools, Milling Tools, HDD Component Tools, Display And LED Mold Tools, Semiconductor And Electronics Tools, Aerospace And Defense Precision Tools, Medical Precision Tools, Jewelry And Watchmaking Tools, Others | |

| By Tool Condition | Routine Wear, Chipped Edge, Radius Drift, Geometry Deviation, Diamond Dislodged, Severe Damage | |

| By Service Provider | Tool OEM Relapping Centers, Independent Relapping Specialists, Regional Distributor Service Partners, Machine OEM Service Networks, In House Captive Tool Rooms | |

| By Turnaround Time | Same Day, 1 To 3 Days, 4 To 7 Days, More Than 7 Days | |

| By Contract Model | Per Tool Pricing, Batch Pricing, Annual Service Agreement, Tool Management Portal | |

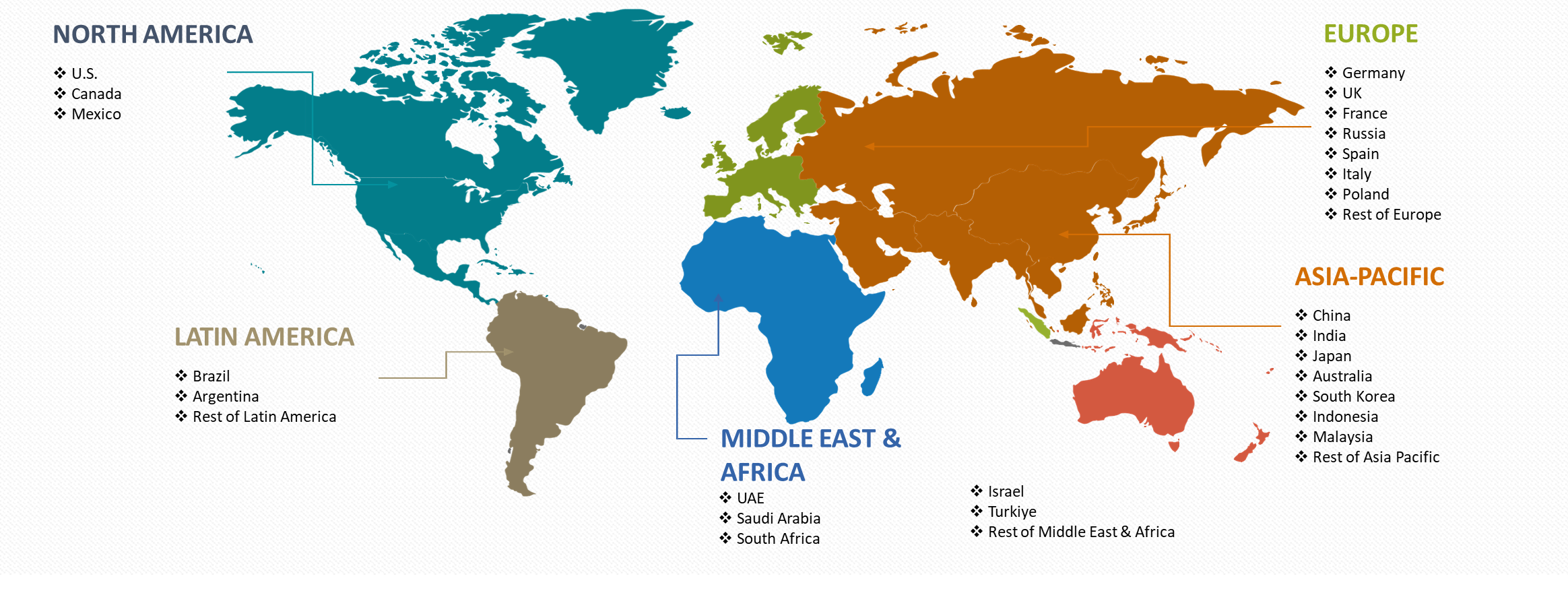

By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Strategic Indicators For SCD Diamond Tool Relapping

High Regulation Impact

Export Controls and Dual-Use Optics Are Creating More Documentation Pressure

SCD relapping demand is closely linked to precision optics, IR optics, electro optics, aerospace optics and defense-related diamond turning. In these areas, service providers are increasingly expected to maintain tool history, geometry reports, customer traceability and repair records because the serviced tool may support controlled optical components or defense-grade precision parts. Regulation does not directly control “relapping” as a standalone activity but it affects the customer’s documentation expectations.

Critical Material Rules Are Pushing Tool Life Extension

Europe’s Critical Raw Materials Act is focused on reducing supply dependence and improving circularity across critical material value chains. Tungsten, cobalt and several advanced manufacturing inputs remain under closer policy attention. For SCD relapping providers, this indirectly supports a stronger business case for repair, relap, regrind and retip services because customers want to extend usable tool life rather than rely only on new tool procurement.

Medical And Ophthalmic Manufacturing Require Higher Process Control

Contact lens, IOL, spectacle lens mold and medical precision component production need consistent surface quality and repeatable dimensional performance. Relapping providers serving these customers face higher inspection expectations around radius, waviness, rake face, clearance face and edge condition. The regulatory effect is therefore seen in quality assurance and certification needs rather than in a direct relapping license

requirement.

High Investment Activity

OSG’s Move Into Contour Shows Institutional Interest In Ultra Precision Diamond Tooling

The strongest investment signal is OSG Europe’s acquisition of Precision Tools Holding B.V., the parent company of Contour Fine Tooling and Technodiamant, in July 2024. Contour is positioned around ultra-precision diamond point cutting tools and its acquisition shows that global tool groups are willing to invest in niche diamond tooling platforms where tool grinding, relapping and micro-precision customer access matter.

Diamond Tooling Investment Is Moving Toward Micro Precision Rather Than Commodity Cutting Tools

OSG later highlighted that the Precision Tools Holding acquisition expanded its presence in micro-precision machining and added diamond tool grinding technology, SCD inserts, SCD bites, SCD fly-cutting inserts and SCD ball end mills. For relapping, this matters because the aftermarket value is highest where tools are expensive, geometry-sensitive and repeatedly restored rather than discarded after one cycle.

Japan’s Tooling Policy Is Supporting Digital And High Value Manufacturing Upgrades

METI’s FY2025 vision for machine parts and tooling industries focuses on digital technologies and managerial resources to strengthen Japan’s manufacturing foundation. SCD relapping service providers may benefit from this direction because Japanese manufacturers increasingly require precision maintenance, tool traceability, service quality records and digitalized tooling workflows.

Recent M&A Or Funding

- July 2024: OSG Europe S.A., a subsidiary of OSG Corporation, acquired Precision Tools Holding B.V., the parent company of Contour Fine Tooling and Technodiamant. The transaction strengthened OSG in ultra precision diamond point cutting tools and expanded its access to optical application customers.

- August 2024: Nissin Diamond Co., Ltd., an OSG Group company, announced the acquisition of Micro Diamond Corporation business. The deal strengthened OSG Group exposure to ultra small diameter monocrystalline diamond ball end mills and micro machining tool capability.

New Product Launches

- October 2025: Precitech and TRIOPTICS announced integration of TRIOPTICS OptiCentric measurement system and ATS software processes with Precitech SPDT machines. The launch is relevant because tighter lens centering and metrology integration raise the need for consistent SCD tool condition, geometry control and relapping documentation.

- December 2025: TRIOPTICS introduced SurfInspect for objective and economical inspection of optical surfaces in compliance with ISO 10110-7. The launch supports the broader precision optics quality ecosystem where surface finish, tool condition and repeatable diamond turning performance are closely linked.

Supply Chain Disruption

Disruption in this market is often caused by service distance rather than raw material shortage. A damaged SCD tool may need to be shipped to Europe, North America, Singapore, Japan or South Korea when local relapping capability is not qualified. Customs delays, courier risk, tool insurance issues and limited technician availability can turn a small edge repair into a production stoppage for contact lens, IOL, IR optics or precision mold customers.

Pricing Volatility

New SCD Tool Prices Make Relapping A Cost Avoidance Decision

Relapping becomes more attractive when replacement SCD tools are expensive, imported or application-specific. In optical turning, contact lens tooling, IOL molds, prism molds and mirror finishing, a customer is not only paying for the diamond tip but also for geometry, edge preparation, waviness control, inspection and delivery time. A properly executed relap can protect production continuity at a lower cost than full tool replacement.

Synthetic Industrial Diamond Supply Is Concentrated, Creating Input Risk

USGS reported that synthetic diamond represented more than 99% of global industrial diamond production in 2025 and China, the U.S. and Russia produced about 99% of synthetic industrial diamond by quantity. Concentration at this level can affect replacement tool economics, especially when customers depend on specific diamond quality, tool blank availability or imported precision tooling.

Turnaround Premiums Are Becoming A Real Price Variable

Pricing is not only based on relap type. Same day, 1 to 3 day and emergency relap services can command a premium because the customer is avoiding idle diamond turning machines, delayed lens mold production or missed delivery schedules. Complex services such as geometry correction, controlled waviness restoration, retipping and rebrazing can also increase pricing because they require senior technicians, specialized inspection and higher rework risk.

Procurement Pressure

Procurement teams are pushing production managers to extend tool life before approving new SCD tool purchases. Approved relapping suppliers help customers reduce replacement spend, avoid emergency purchases and maintain tool level documentation. The pressure is strongest where tools are tied to qualified parts such as contact lens tools, IOL tools, aspheric optics, metal mirrors and precision optical molds.

New Technology Adoption

Adoption is moving toward more measurable service workflows. Microscopy, interferometry, tool geometry reports, waviness certificates, digital tool history and customer portals are becoming more important because buyers need proof that restored tools can return to production without trial and error. AI assisted inspection can support this workflow by flagging wear patterns or edge damage but expert technician judgment remains essential.

Regional Expansion Opportunity

Regional service expansion is most attractive in Japan, Singapore, South Korea, Europe and North America because these locations have stronger installed bases in precision optics, ophthalmic tooling, IR optics and ultra precision machining. India should be positioned as an emerging service opportunity rather than a leading demand center because the current market is smaller and concentrated among a limited number of specialist providers.

Government Policy Support

Japan’s Industrial Tooling Policy Supports Precision Service Ecosystems

METI’s FY2025 vision specifically aims to strengthen machine parts and tooling industries through digital technologies and better use of human resources. This is relevant for SCD relapping because Japan has a strong base in optics, precision molds, machine tools, semiconductors and high-end manufacturing where tool life management and service quality are critical.

EU Critical Raw Material Policy Supports Repair And Circularity

The European Critical Raw Materials Act is designed to strengthen raw material value chains, improve resilience and support circularity. While it does not mention SCD relapping directly, the policy direction favors longer tool life, recycling, repair-based service models and lower dependence on new material inputs. This gives relapping providers a stronger sustainability and procurement argument in Europe.

Regional Manufacturing Security Programs Are Creating Indirect Demand

Government support for semiconductors, defense optics, advanced manufacturing, medical devices and localized industrial production increases the installed base of precision machining and optics manufacturing. SCD relapping benefits from this because every high-value diamond turning cell creates recurring tool maintenance demand after initial tooling deployment.

Import Export And Pricing Intelligence

Direct import export tracking is not the best primary method for SCD tool relapping because relapping is a service and returned tools may move under repair, warranty or temporary movement records. UN Comtrade based trade data can still be used as a supporting proxy through HS 820790 for interchangeable tools. A more precise trade proxy is HS 82079010 in customs systems that separate tools with working parts of diamond or agglomerated diamond. The proxy should be used carefully because it captures new tools and other interchangeable tools rather than relapping service revenue.

| Proxy Code | Reporter | Trade Flow | 2024 Trade Value | Interpretation |

| HS 820790 | European Union | Exports To World | US$ 691.6 Million | Large precision tool export base but not relapping specific |

| HS 820790 | Germany | Exports To World | US$ 635.5 Million | Strong tool export signal for Europe based sourcing |

| HS 820790 | China | Exports To World | US$ 489.6 Million | High volume tool export base with broad product mix |

| HS 820790 | U.S. | Exports To World | US$ 202.5 Million | Relevant proxy for advanced tool exports from North America |

| HS 820790 | Italy | Exports To World | US$ 168.3 Million | European industrial tool export signal |

Pricing intelligence should therefore sit beside trade intelligence. The report should benchmark standard relap, express relap, re radiusing, recone, retipping, inspection certificate and tool management program pricing by region and provider type. The strongest commercial output is not only import export movement but a buyer ready view of service price, lead time, acceptance criteria and documentation level.

Company Coverage Preview

OSG Corporation is the largest strategic player to cover because its diamond tooling platform now includes Contour Fine Tooling through the acquisition of Precision Tools Holding B.V. Contour gives OSG a highly specialized position in ultra precision diamond point cutting tools for optical applications such as spectacles, contact lenses, IOLs and electro optics. The acquisition moved OSG beyond a conventional cutting tool portfolio and strengthened its presence in a premium micro precision niche where relapping, tool history and geometry control are commercially important.

The company reached a stronger position by combining scale, application access and specialist tool know how. Contour brings deep relationships in ophthalmic and optics manufacturing while OSG brings global manufacturing discipline, brand reach and customer access across industrial tooling. The strategic advantage is not only tool supply. It is the ability to support the full lifecycle of high value SCD tools through manufacturing, repair, relap capability, quality documentation and customer specific service models.

The main USP is the combination of global reach and niche technical credibility. Contour is closely associated with relaps, repair facilities, waviness certificates and tool resource management. Such capabilities matter because SCD tool users are not only buying a sharp edge. They are buying predictable optical performance, reduced machine idle time and confidence that restored tools will meet qualified production requirements.

AI Impact Analysis on Tool Inspection, Service Scheduling and Traceability

AI impact in this market is practical rather than promotional. The strongest use case is image-based edge inspection, where high-magnification photos can be compared with past tool conditions and known failure modes. AI can help classify micro chipping, crater wear, waviness drift and polishing marks before a tool enters production. Human experts still make final decisions because diamond orientation, tool history and customer application context remain critical.

Predictive service scheduling is the second meaningful use cas\. A customer can link tool use hours, machined material, surface finish readings and last relap date to anticipate when a tool should return for service. Such scheduling reduces emergency shipments and machine idle time. Providers with customer portals and tool history records are better placed to adopt this model because data continuity matters more than algorithm sophistication.

AI can also improve quotation discipline. Service providers can use historical repair tickets to estimate whether a tool needs standard relap, reradiussing, recone or replacement. A consistent quote matrix reduces subjective pricing and helps sales teams defend premium fees for controlled geometry work. Small shops may lag because data capture is often informal. Larger specialists can use AI to convert craft knowledge into repeatable commercial workflows.

Disruption Analysis

Traditional diamond tool servicing relied on craftsman judgment, customer phone calls and manual inspection notes. The disruptive layer now comes from traceable service histories and metrology-based decisions. Contour highlights its My Contour portal with tool history, technical documents and waviness certificates. Such digital traceability matters because optics and ophthalmic customers often need to prove tool condition when a lens mold, IR optic or freeform part moves from prototype into repeat production. Service providers that treat relapping as a documented precision process can charge for confidence rather than only labor time.

Another disruption comes from customers sending mixed brand tools to third-party providers. K and Y documentation states that it repairs tools from any manufacturer. SINJIN also presents repair through regrinding, relapping and resharpening. Independent shops can therefore capture wallet share from customers who use multiple tool brands or who need faster local turnaround. OEM toolmakers still hold an advantage in geometry data and original tool design knowledge, yet regional repair houses can win standard repairs where customer priority is speed, cost and proximity.

Precision optics and defense supply chains are also reshaping demand. NASA lesson material describes diamond turning as a precision machining capability for aerospace optical systems. Teledyne FLIR Defense highlights precision optics for defense, industrial and commercial markets. Higher interest in IR imaging, space optics, sensors, high-energy lasers and advanced metrology creates more tool wear in niche machining lines. Relapping becomes a continuous service because customers cannot stop a qualified production cell while they wait for new tool procurement and incoming validation.

India and Southeast Asia introduce a different form of disruption. Local providers such as Hardten, Reliance Diamond Tools, Solar Diamond Tools, Kamala Engineering and Gold Technic increase regional availability for repair, polishing, natural diamond, PCD, CBN and single-crystal adjacent tooling. Lower service costs and shorter logistics routes can shift routine work away from established Western suppliers. High-end controlled waviness or ultra-tight freeform geometries may still flow to global specialists, yet routine edge recovery can localize faster as customer confidence improves.

BCG Matrix: Company Evaluation

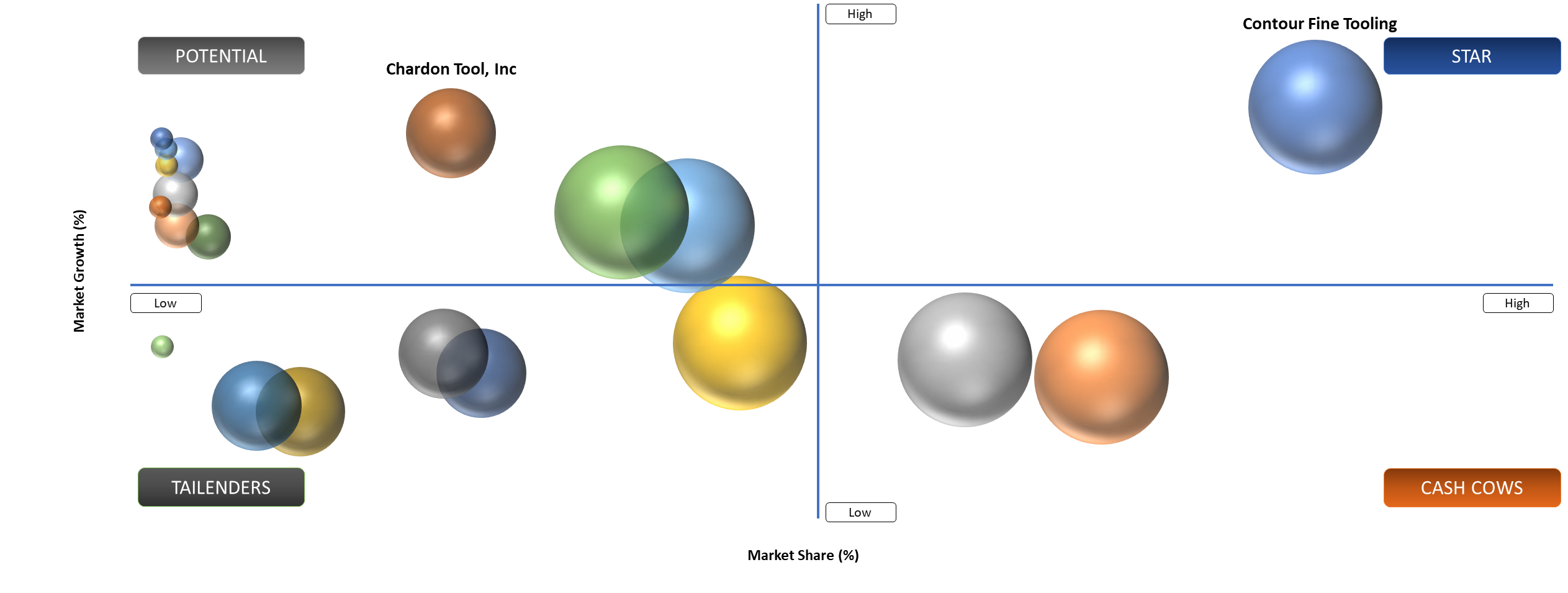

Stars

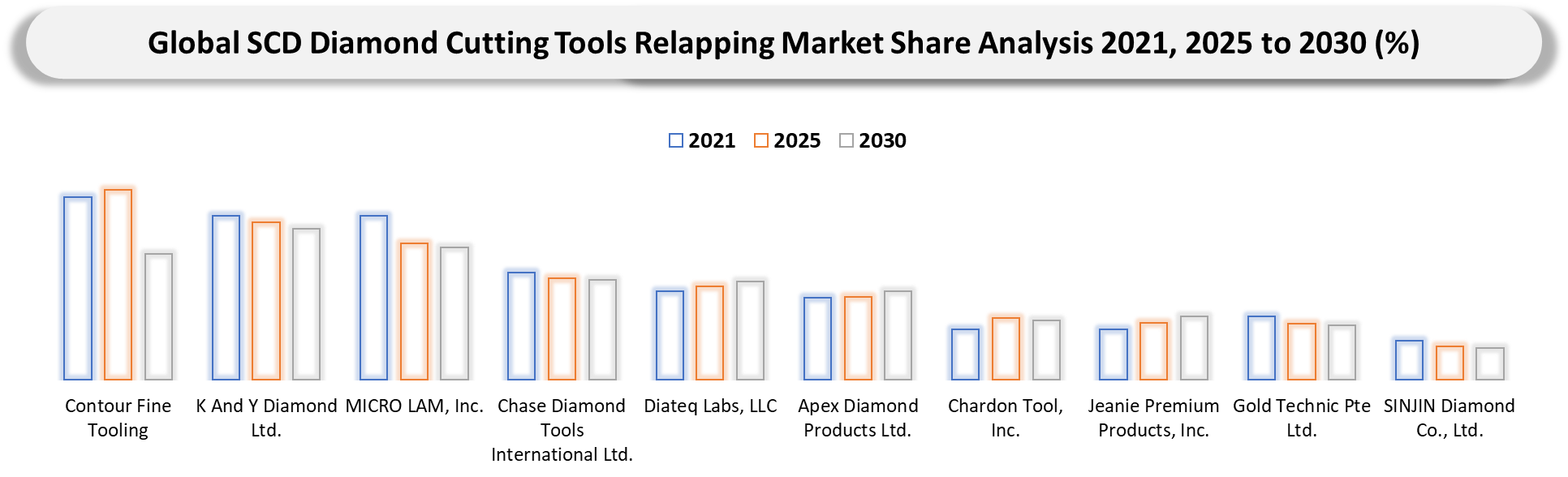

Stars in this market are providers that combine diamond tool design, relapping expertise, metrology proof, customer portal capability and global or regional turnaround strength. Diatec, K and Y Diamond and Micro LAM fit strongly because each links tool supply with repair support and technical assistance. Diatec brings multiple manufacturing and repair facilities, while its repair page describes top rake lapping, reradiussing and brazing support. K and Y add strong relap economics with a claim that a tool can be serviced up to 30 times when damage allows. Micro LAM strengthens its position through diamond tool supply, laser-assisted machining know-how, process development support and fast repairs. Star companies win when customers consider tool performance, tool life records and production continuity as one purchasing decision. Contour was once a Star, but after its acquisition by Technodiamant, it lost most of its revenue.

Potential

Potential companies are regional or application-focused providers that can capture demand from customers wanting lower cost, local service and shorter transit time. Gold Technic, SINJIN Diamond, Apex Diamond Products, Reliance Diamond Tools, Solar Diamond Tools and Kamala Engineering sit in this group. Gold Technic offers relapping and polishing from Singapore with a 5 to 7 day restoration cycle. Such companies can move closer to star status if they publish clearer single-crystal relap specifications, inspection tolerances, certification formats and case-based turnaround evidence.

Market Dynamics

Recurring Tool Life Extension Demand Is Driving Paid Relapping Cycles Across Ultra Precision Machining Lines

Ultra-precision manufacturers want lower tooling costs without compromising nanometer surface finish, which makes relapping a demand-side priority. Diamond tools usually fail through edge micro fracture, surface roughness drift, radius change or clearance face deterioration rather than full diamond loss. When a qualified tool can be restored through a controlled pass, customers avoid the cost of buying new tools and also reduce the qualification work attached to new geometry. K and Y explain that relapping removes only the damaged area and can return a tool to new condition within a short turnaround. Such economics directly support recurring service revenue.

Demand also grows because production cells have become more specialized. Ophthalmic molds, contact lens tools, IOL tooling, IR optics, diamond turned mirrors, disk substrates and non-ferrous precision parts often run on tightly controlled recipes. New tool insertion can require test cuts, measurement time and process tuning. Servicing the same known tool body can maintain customer confidence when service records preserve radius, clearance, rake and waviness expectations. Customers, therefore, view relapping as a production assurance service rather than a repair afterthought.

Volume data should be captured as number of diamond tools serviced or serviced per year. Service type is the best segment for volume reporting because each pass, repair or recone represents an actual service transaction. Service passes offer the strongest unit clarity because providers commonly describe relap turnaround and tool count. Revenue can then be modeled through average service price per pass by geometry, tool size and precision class. Tool type or application volumes are useful but harder to audit because one tool may serve multiple components across several production batches.

Limited Public Service Data and Craft Dependent Quality Slow Reliable Market Sizing

The main restraint is not a lack of need. The bigger challenge is limited visibility into service volumes, relap pricing, rejection rates, rework cycles and tool failure reasons. Many providers publish repair capability but do not disclose how many tools they process or how service price changes by radius, waviness, diamond size and inspection certificate requirement. Customers also treat tool service history as process sensitive information because edge conditions can affect product yield. Market sizing, therefore, needs triangulation from installed diamond turning machines, optics and ophthalmic production clusters, service turnaround claims and primary interviews with tool rooms.

Quality dependence also limits customer switching. A poor relap can alter radius size, rake condition or surface finish performance and can damage a production relationship quickly. K and Y note that radius size gets smaller as a tool is serviced. Such a geometry change must be understood by the customer before production resumes. Service providers without advanced lapping skill, inspection equipment and documentation can compete on price but may struggle in aerospace, defense optics, semiconductor equipment and high-end ophthalmic work where repeatability matters more than service cost.

Segment Analysis

The market is segmented by service type, tool type, tool geometry, diamond type, application area, customer type, service provider type and region. Service type gives the clearest basis for value and volume sizing because each relap, recone or refurbishment converts into a service ticket.

Service Passes Are the Most Bankable Service Segment Because Each Pass Converts Tool Wear Into Measurable Revenue

Service passes dominate the market because they are repeatable, countable and directly linked to tool life extension. Providers can record number of tools received, accepted, serviced, returned and rejected. Service passes create a clear bridge between customer maintenance behavior and market value.

Routine edge recovery also reflects the largest practical demand pool. Optical shops, ophthalmic mold producers and ultra-precision job shops often run the same tool geometry across repeated batches. Wear appears as declining surface quality or edge defect before full tool failure. A service provider can restore the rake surface, preserve the useful diamond body and return the tool with inspection notes. Customers value fast service because a single missing tool can delay an entire diamond turning schedule.

Commercial feasibility is high because relapping shows strong public validation. Contour complete repair and relaps services with 2 to 3 day in-house turnaround and same-day service on request. Micro LAM states that repairs can be completed within a maximum of 3 days for tool relaps. Gold Technic advertises diamond tool relapping and polishing with 5 to 7 day restoration. Multiple providers across different regions use the same service language, which makes the segment suitable for market modeling.

ReRadiussing and Radius Correction Support Higher Value Repairs When Tool Geometry Directly Controls Part Quality

Re radiussing sits close to relapping but carries a different commercial logic. Relapping refreshes the cutting edge while reradiussing corrects radius geometry when wear or customer requirements change the tool profile. Contour states that diamond reradiussing can be done when needed. Such service matters when a customer must maintain a target lens form, mold groove, freeform feature or controlled optical profile. A recovered edge without correct radius can still fail the part.

High value work appears in optics, IOL, contact lens mold, IR lens, watch component and precision engraving applications. Small radius deviations can change product form or surface quality. Customers, therefore, pay for metrology-backed correction rather than a basic polish. Service providers that can document radius, included angle, clearance and waviness are better positioned to win repeat work from regulated or export-oriented manufacturers.

Reradiussing is less frequent than routine relap but more attractive from a margin perspective. The service requires skilled diamond shaping, polishing and measurement. It can also trigger a customer discussion about tool redesign, new radius specification or a replacement recommendation. Providers that pair repair with engineering advice can convert service cases into new tool orders.

Retipping, Resetting and Rebrazing Create Replacement Deferral Revenue When Diamond Loss or Bond Failure Occurs

Retipping, resetting and rebrazing address more severe tool damage than routine relap. Contour notes that brazing services are available when a diamond becomes dislodged from the shank or insert base. Such services move the market closer to refurbishment because the provider may need to restore the diamond seat, replace the stone or rebuild tool integrity. Customers choose the service when tool holder value, lead time or geometry history justifies repair over replacement.

It is especially relevant for custom tools, large radius tools, controlled waviness tools and special holders. A standard low complexity tool may be replaced faster, while a custom geometry with proven process data may merit resetting. Aerospace, defense, optics and specialist labs often value continuity because a known tool body can shorten requalification. High repair value also appears when imported tool lead times are long or when local supply is uncertain.

Commercial value depends on provider's capability. Basic relapping shops may not offer reliable resetting or brazing. OEM toolmakers and advanced independent providers hold stronger positions because they understand shank design, diamond orientation and thermal effects. Service providers that publish full restoration capability, such as SINJIN and Gold Technic, can capture repair work beyond the first relap pass.

Geographical Penetration

U.S. SCD Diamond Cutting Tools Relapping Market Trends

The U.S. market is driven by defense optics, aerospace optical systems, IR imaging, precision medical devices, national lab work and advanced manufacturing job shops. NIST links diamond turning to single-crystal diamond tools for metal optics and NASA lesson material highlights precision diamond turning for aerospace optical systems. Such applications create a strong need for relapping because a tool edge can determine mirror finish, form accuracy and repeatability in non-ferrous optical materials.

U.S. customers place a high value on documentation and traceability. Aerospace and defense suppliers often need tool condition records, inspection support and process consistency. Contour has a North American presence through its service network, while K and Y Diamond in Canada supports customers with rapid relapping and any manufacturer repair capability. Micro LAM adds a U.S. technology layer by combining diamond tools with process development and laser-assisted machining expertise.

Machining investment also provides a demand backdrop. AMT reports U.S. manufacturing technology orders through the USMTO program and its 2025 releases point to continued investment interest around automation and machine tool demand. More five-axis precision machining, diamond turning and specialized optics work increases the installed base that needs tool recovery. Service providers can win by offering emergency turnaround, tool design advice and inspection packages tied to production uptime.

U.S. buyers are less likely to select the lowest price when tool failure threatens qualification loss. Defense optics, medical micro parts and scientific instrumentation often carry small batch sizes with high part value. Service providers, therefore, need to sell risk reduction. The most attractive customer groups are optics manufacturers, national lab suppliers, aerospace component shops, IR lens makers and diamond turning service bureaus using mixed tool brands.

Japan Specialist Diamond Tool Servicing Market Outlook

Japan has a strong fit for this market because its manufacturing base values precision, repeatability and supplier trust. JMTBA identifies itself as the nonprofit trade association for metal cutting machine tool builders and publishes monthly machine tool order data. METI’s FY2025 vision for machine parts and tooling emphasizes digital technologies and managerial resources to strengthen Japan’s manufacturing foundation. Such policy direction supports high-accuracy tooling services around machine parts, optics and equipment manufacturing.

Japanese demand is linked to optics, cameras, semiconductor equipment, precision molds, watch components, automotive sensors and advanced machinery. Japan’s production culture favors long-term supplier relationships and documented quality. Tool recovery fits that behavior because tool recovery can become a scheduled maintenance program rather than spot repair. Diamond turning tools used for aspheric lenses, IR components and mold inserts need repeat edge quality across production cycles.

Local Japanese toolmakers and machine tool firms also influence customer expectations. Buyers tend to prefer technically deep suppliers that can discuss radius change, clearance, surface finish and process stability. Service providers entering Japan need more than price competitiveness. Strong documentation, inspection proof, Japanese language technical support and compatibility with domestic diamond turning machines matter.

Semiconductor and optical equipment investment can lift service demand indirectly. METI published OT security guidelines for semiconductor device factories in 2025, which reflect continuing attention to fab operations and process resilience. Precision parts and optical subsystems used around semiconductor equipment still require tight machining and finishing. Tool servicing demand will likely remain specialized and relationship-driven rather than broad commodity repair.

Asia-Pacific Service Capability and India-Led Localization

Asia-Pacific holds the broadest growth pool because China, India, Japan, South Korea, Singapore and Malaysia combine optics, electronics, ophthalmic, semiconductor equipment, jewelry, automotive precision and contract manufacturing. USGS states that China led synthetic industrial diamond production in 2025 and synthetic diamond represented more than 99% of global industrial diamond output. Supply-side strength in diamond materials creates a base for toolmaking while customer clusters create recurring servicing demand.

India deserves specific attention because local suppliers are becoming more visible. Hardten Precision Technologies publishes single-crystal tooling, tool relaping, technical reports and diamond tool consultancy. The company lists industries such as ophthalmic, electro optics, roto gravure, automotive, space and defense and watch and jewelry. Reliance Diamond Tools adds natural diamond, PCD and CBN tooling relevance while Solar Diamond Tools and Kamala Engineering support broader diamond tool manufacturing and export capabilities. Such ecosystem depth can reduce import dependence for routine service work.

Singapore has a specialist service role due to high precision engineering and regional logistics. Gold Technic publishes diamond tool relapping and polishing, with repairs handled in its Singapore facility and a 5 to 7 day restoration cycle. Such positioning is valuable for Southeast Asian optics, electronics and precision mold customers that need regional turnaround without sending tools to Europe or North America.

South Korea and China are important through optical parts, electronics, semiconductor equipment and superhard tooling capabilities. SINJIN Diamond lists ultra-precision cutting tools and repair services, including regrinding, relapping and resharpening. Chinese superhard material firms also publish single-crystal diamond cutting tools for ultra-smooth mirror surfaces and nanometer-level waviness control. Competitive pressure from Asia-Pacific will increase as more providers publish service tolerances and quality records.

Europe Precision Tooling and Optics Service Base

Europe remains important through Germany, Switzerland, UK, France, Netherlands and Italy because the region contains high-value optical, watch, medical, aerospace and precision machining clusters. DIATEC in Germany presents monocrystalline and polycrystalline diamond tools for turning and milling and states that monocrystalline diamond is thermally and chemically stable up to 650 degrees Celsius. Apex Diamond Products in the UK states that it manufactures tools using natural, single-crystal and MCD diamond and serves contact lens, IOL, ophthalmic, electro-optical and optical sectors.

European customers often demand application engineering and documented reliability. Precision optics, watchmaking, medical components and defense suppliers need edge consistency and traceability. Service providers can differentiate through controlled waviness, special profiles and fast regional repair. The market is less about volume compared with China or India and more about premium jobs with high inspection requirements.

Germany and Switzerland are likely premium pockets due to optics, advanced machine tools, precision engineering and watch-related tooling. UK demand has a stronger link to optics, defense, aerospace and academic labs. European service providers may also receive tools from customers in Middle East, Africa and Latin America, where local relapping capability is thinner.

Competitive pressure will rise from Asian providers for standard work, yet Europe should hold premium controlled geometry and specialist optical tool cases. Providers that combine toolmaking, repair and process consulting can protect margins. Service records, lead time reliability and ability to handle non-standard geometries will be critical.

Competitive Landscape

- The market remains fragmented because diamond tool servicing depends on specialist skill, precision lapping equipment and customer trust rather than large-scale distribution.

- Contour Fine Tooling, K and Y Diamond, Micro LAM, DIATEC, Apex Diamond Products, Gold Technic, SINJIN Diamond and Hardten Precision Technologies represent relevant named competitors with visible single-crystal or diamond tool service evidence.

- Regional Indian players such as Reliance Diamond Tools, Solar Diamond Tools and Kamala Engineering strengthen adjacent competitive coverage for natural diamond, PCD, CBN and diamond tool repair ecosystem requirements.

- OEM toolmakers compete through original geometry knowledge, tool design capability and inspection certificates, while independent providers compete through any manufacturer repair, local access and faster turnaround.

- Competitive differentiation is shifting toward tool history portals, documented waviness, emergency service, engineering support and relap repeatability rather than basic polishing skill.

Customers in aerospace, defense optics, ophthalmic and semiconductor equipment prefer providers that can preserve radius, rake, clearance and surface finish performance across multiple service cycles.

MAJOR PAIN POINTS

- Low Visibility on Relap Demand by Application: Providers often know their internal job count but lack a structured view of demand by ophthalmic, optics, defense, electronics or rotogravure customers. A market study can benchmark service frequency and identify pockets with higher repeat pass potential.

- Difficulty Proving Service Quality to New Customers: Many buyers hesitate to send high-value diamond tools to unfamiliar providers. Certification templates, sample inspection reports and documented turnaround benchmarks help reduce trust barriers.

- Pricing Pressure from Local Workshops: Regional workshops can undercut standard relap pricing. Providers need segmented pricing by geometry difficulty, turnaround urgency and certificate level to protect margins.

- Limited Public Data for Market Sizing: Service volumes, rejection rates and average ticket values are rarely published. Primary interviews and installed base triangulation are needed to build a credible market model.

- Dependence on Skilled Polishers: Service quality depends heavily on trained technicians. Providers need capacity planning, training roadmaps and process standardization to scale without quality drift.

- Mixed Brand Tool Repair Complexity: Customers often own tools from several brands. Service providers must decide which third-party tools to accept and when to refuse repair based on geometry risk.

- Long International Logistics for Urgent Repairs: Cross-border shipping can delay tool return and create customs risk. Regional service hubs and local partners can improve customer retention.

Unclear Replacement Versus Repair Decision Rules: Customers may over-repair worn tools or replace tools too early. A structured service decision matrix can improve customer economics and supplier credibility.

KEY DEVELOPMENTS

- October 2025: Precitech and TRIOPTICS announced that TRIOPTICS’ OptiCentric measurement system and ATS software can integrate with Precitech diamond turning machines. The development is relevant because on-machine and near-machine lens centering strengthens precision optics manufacturing workflows where SCD tool edge quality, geometry control and relapping consistency directly affect output quality.

- July 2025: OSG highlighted its expanded diamond tool platform after the earlier acquisition of Precision Tools Holding B.V., which includes Contour Fine Tooling. The update positioned OSG more strongly in micro-precision machining through single-crystal diamond inserts, single-crystal diamond bites, fly-cutting inserts and single-crystal diamond ball end mills. Use this only as a strategic portfolio update, not as a second acquisition development.

- December 2024: Nissin Diamond Co., Ltd. changed its company name to OSG Diamond Tools Co., Ltd. The name change followed OSG’s diamond tooling expansion and is relevant because it consolidated the company’s identity around SCD ultra-precision tools, PCD tools and CBN tools.

- August 2024: Nissin Diamond, an OSG Group company, announced the acquisition of Micro Diamond Corporation’s business. Micro Diamond specializes in ultra-small diameter monocrystalline ball end mills, making the development relevant to micro-machining and high-precision SCD tool lifecycle requirements.

- July 2024: OSG Europe S.A., a subsidiary of OSG Corporation, acquired Precision Tools Holding B.V., the parent company of Contour Fine Tooling and Technodiamant. The acquisition expanded OSG’s access to ultra-precision diamond point cutting tools, diamond tool grinding technology and optical application customers across spectacles, contact lenses, intraocular lenses and electro-optics.

ANALYST VIEW / OPINION

- DMI opinion is that the most valuable part of this market is not the visible number of repair shops. The real opportunity lies in converting tool wear into a managed service cycle. Customers in optics, ophthalmic, defense, electronics and rotogravure want fewer production interruptions and better tool traceability. Providers that can prove geometry recovery, turnaround performance and repeat tool life will control pricing better than providers selling generic polishing.

- DataM would view service passes as the correct volume anchor because the unit is countable, repeatable and directly tied to revenue. A strong study should estimate number of diamond tools serviced per year by application area and region. Revenue can then be layered by standard relap, premium controlled geometry relap, reradiussing, recone and major refurbishment. Such a structure gives clients an actionable model rather than a broad aftermarket estimate.

- DMI opinion is that India deserves more attention than typical market reports provide. Hardten’s published relaping service and single-crystal positioning show that local capability is emerging beyond standard PCD or dresser tools. Reliance Diamond Tools, Solar Diamond Tools and Kamala Engineering add adjacent tooling ecosystem depth. A client evaluating Asia-Pacific should not look only at China, Japan and South Korea. India can become a practical service hub for cost-sensitive and mid-precision applications while premium geometry work gradually builds.

TARGET AUDIENCE

| INDUSTRY | WHO SHOULD BUY THIS REPORT? | REASON TO BUY THIS REPORT |

| Single-Crystal Diamond Tool Manufacturers | Owners, Product Heads and Sales Leaders | Benchmark service scope, regional demand pockets and high-margin repair opportunities. |

| Independent Service Service Providers | Business Owners and Operations Managers | Understand which service types and applications can be quantified and priced more profitably. |

| Optics Manufacturers | Manufacturing Heads, Tool Room Managers and Quality Teams | Evaluate service partners for diamond turned optics, IR lenses, aspheres and freeform components. |

| Ophthalmic Lens and IOL Producers | Production Heads and Procurement Teams | Track relap cycles, radius control needs and local repair options for lens mold tooling. |

| Aerospace and Defense Suppliers | Precision Manufacturing Teams and Strategic Sourcing Heads | Assess qualified tool servicing routes for defense optics, mirrors, sensors and high-value components. |

| Electronics and Semiconductor Equipment Suppliers | Advanced Manufacturing and Supplier Development Teams | Identify service capability for diamond turned parts, substrates and precision non-ferrous components. |

| Roto Gravure Cylinder Manufacturers | Tool Room Heads and Plant Managers | Study stylus and engraving tool service requirements and regional support options. |

| Ultra Precision Job Shops | Founders, Workshop Managers and CNC Leads | Compare repair versus replacement economics for mixed-brand single-crystal tool inventories. |

| Diamond Turning Machine Suppliers | Product Strategy and Aftermarket Teams | Identify service partnerships that can improve customer uptime and machine utilization. |

| Industrial Distributors | Category Managers and Regional Sales Teams | Evaluate whether services can be bundled with diamond tooling and precision machining support. |

| Investors and Private Equity Firms | Industrial Investors and Deal Teams | Assess specialist aftermarket revenue, service defensibility and regional consolidation opportunities. |

| Consulting and Advisory Firms | Market Intelligence Teams and Strategy Consultants | Support market entry, competitive benchmarking, pricing strategy and customer targeting projects. |

| Cutting Tool & Insert Manufacturers | Product Innovation Teams, Competitive Intelligence Departments, Sales Strategy Teams | Benchmark competitor offerings, coating technologies and material advancements |

WHY CHOOSE DATAM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

WHAT DATAM UNIQUELY PROVIDES

- A verified relapping provider map that separates confirmed SCD relapping companies from adjacent diamond tool manufacturers with no clear relap service evidence.

- A service revenue model built around real commercial drivers such as service type, tool condition, turnaround time, certificate requirement and provider type.

- A regional downtime and service hub assessment covering North America, Europe, Japan, Singapore, South Korea and emerging India based service capability.

- A procurement ready supplier scorecard covering relap capability, re radiusing, recone, retipping, inspection documentation, tool history and emergency turnaround support.

- A pricing intelligence layer that distinguishes standard relap, express relap, geometry correction, retipping and tool management programs instead of treating the market as a broad diamond tool aftermarket.

- An import export proxy view using HS 820790 and diamond tool related sub codes only as supporting evidence while keeping the core market sizing focused on service revenue.

QUESTIONS THIS REPORT ANSWERS

- What is the addressable service value for specialist diamond tool service and related repair services through 2035?

- Which service types, such as service passes, reradiussing, recone, retipping or inspection certificates, offer the strongest revenue potential?

- How many diamond tools can be modeled as serviced or serviced per year by region and application area?

- Which companies provide OEM-led versus independent edge recovery services across North America, Europe and Asia-Pacific?

- How do ophthalmic, optics, roto gravure, aerospace, defense and electronics customers differ in repair frequency and documentation needs?

- What is the best repair versus replacement decision framework for customers using high-value diamond tools?

- Which countries offer the strongest opportunity for regional service hubs and local partnership models?