Sauces, Dressings and Condiments Market Overview

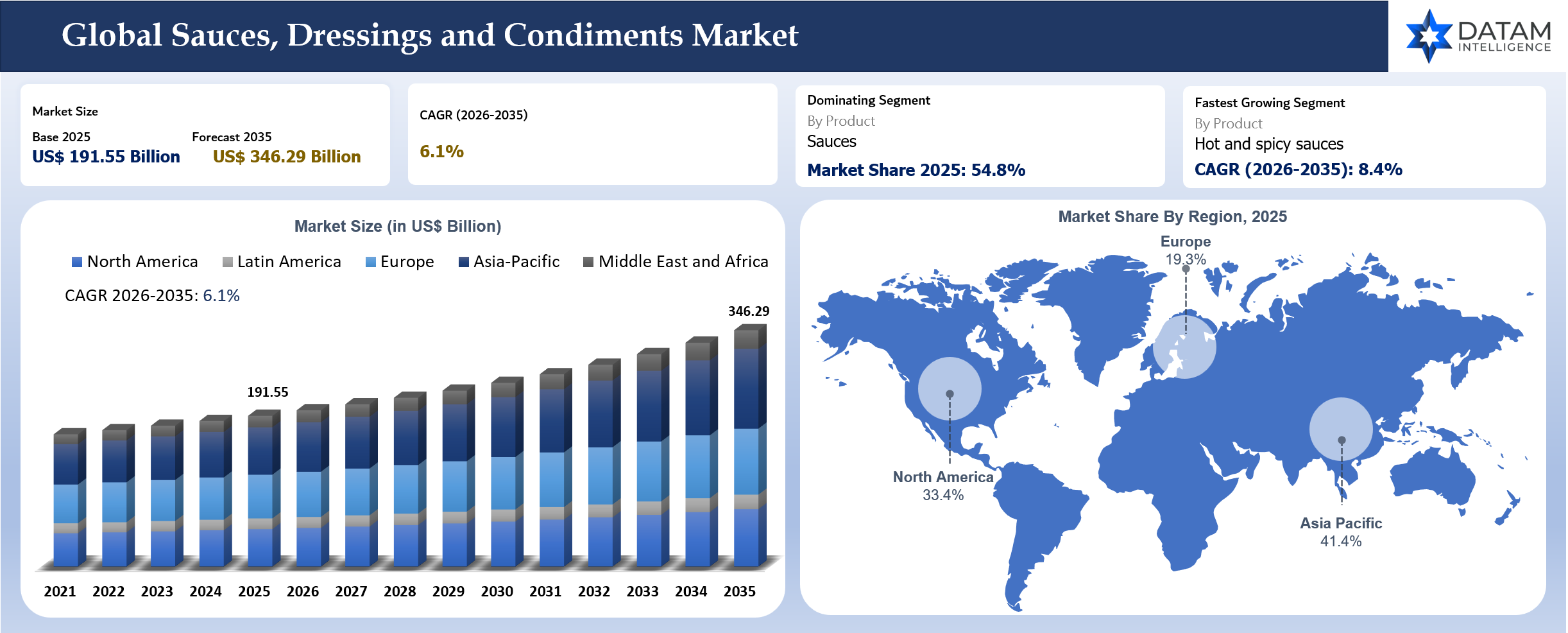

The global Sauces, Dressings And Condiments Market reached US$ 191.55 Billion in 2025 and is expected to reach US$ 346.29 Billion by 2035, growing at a CAGR of 6.1% during 2026-2035. The market is moving beyond traditional table sauces and becoming a broader flavor platform across retail, foodservice and packaged food manufacturing. Consumers are using condiments to add global flavors, heat, creaminess, convenience and personalization to everyday meals. Brand owners are responding with premium pasta sauces, hot sauces, squeeze formats, globally inspired blends, clean-label recipes and foodservice packs that support both at-home cooking and away-from-home dining. Value growth is being led by premiumization, spicy flavor adoption, ethnic cuisine penetration, restaurant-style home cooking and wider use of sauces in ready meals, snacks, sandwiches, bowls, protein dishes and frozen foods.

Large-scale food companies are treating sauces, dressings and condiments as strategic assets because the category offers repeat purchases, brand loyalty, strong household penetration and attractive extension opportunities. McCormick’s planned combination with Unilever’s Foods business shows how leading companies are consolidating flavor assets across herbs, spices, seasonings, sauces, condiments, cooking aids and foodservice solutions. Campbell’s acquisition of Sovos Brands also demonstrates the value of premium sauce brands, especially Rao’s, where ingredient quality, brand trust, distribution expansion, and innovation have turned a once regional pasta sauce into a billion-dollar portfolio. The category is therefore becoming more competitive, more premium and more dependent on strong retail execution.

Growth is not uniform across all products. Ketchup, mayonnaise and mustard remain high-penetration staples in mature markets, but faster growth is coming from hot sauces, pasta sauces, cooking sauces, dips, premium dressings and international flavor formats. Foodservice demand is also changing because restaurant chains, quick-service operators, cloud kitchens and casual dining brands increasingly use signature sauces to differentiate menus and simplify kitchen operations. Retailers are expanding private label sauces and dressings, while premium brands defend share through taste, ingredient credibility, pack design and innovation speed. The strongest suppliers will be those that can serve retail households, foodservice kitchens and industrial customers with consistent quality, flexible packaging and strong flavor development.

Key Takeaways

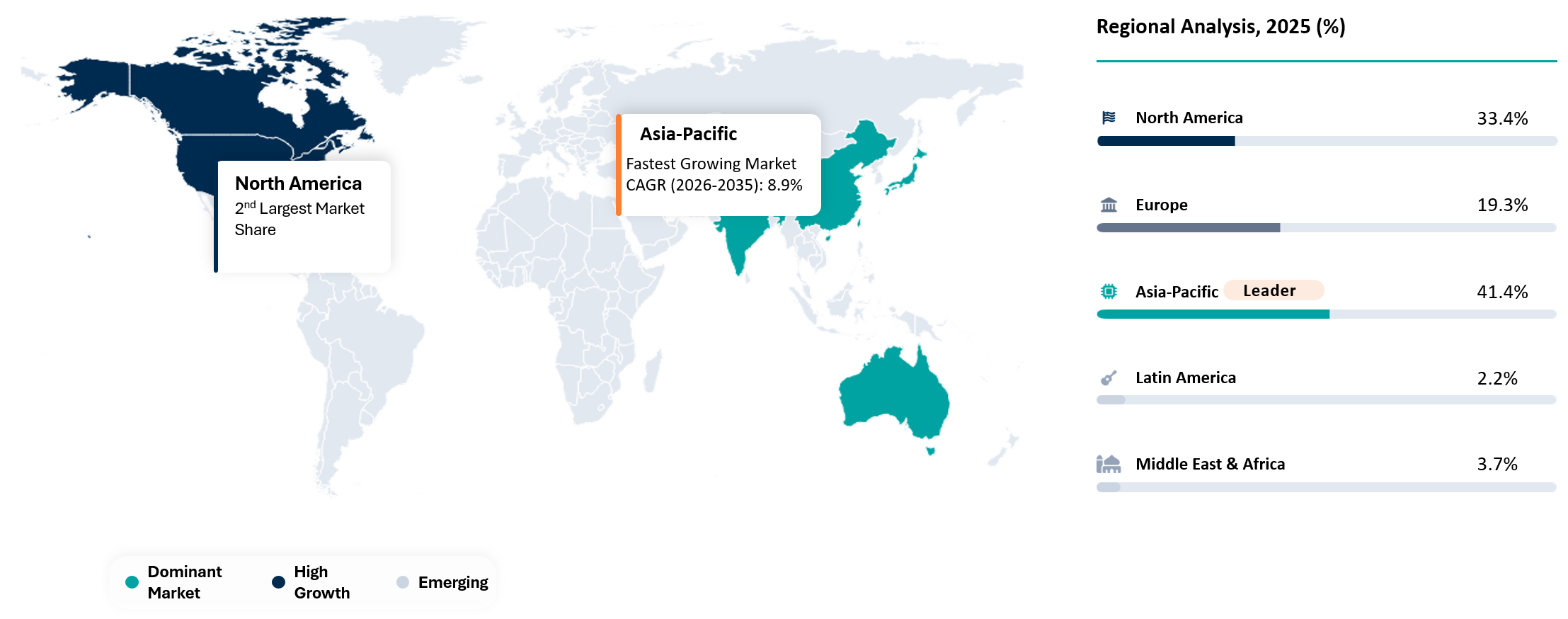

- Asia-Pacific dominated the global sauces, dressings and condiments market with 41.4% share in 2025, supported by high commercial penetration of ketchup, mayonnaise, dressings, hot sauces, barbecue sauces and premium pasta sauces.

- Asia-Pacific is also the fastest-growing region with a projected CAGR of 7.6% during 2026-2035, driven by urban foodservice expansion, rising packaged food consumption, strong demand for chili sauces, soy-based sauces, curry sauces and premium international flavors.

- Sauces dominated with 54.8% share in 2025 because pasta sauces, hot sauces, cooking sauces, barbecue sauces, soy sauces, chili sauces and table sauces are used across retail, foodservice and packaged meal applications.

- Hot and spicy sauces are expected to be the fastest-growing product group during 2026-2035 with 8.4% CAGR, supported by younger consumers, global flavor exploration, chicken-wing occasions, street-food-inspired menus, and spicy convenience foods.

- Retail and household consumption led the market with 61.7% share in 2025 because sauces and dressings are high-frequency pantry items used for daily meals, snacks, sandwiches, salads, pasta, grilled foods, and prepared meals.

- Foodservice is the fastest-growing sales channel because quick-service restaurants, casual dining chains, delivery kitchens and institutional kitchens use sauces to build recognizable menu signatures with limited preparation complexity.

- Premium pasta sauces are gaining share as consumers trade up from basic tomato sauces to slow-cooked, ingredient-led and restaurant-origin brands that support affordable at-home meal upgrades.

- Supplier differentiation is moving toward flavor innovation, ingredient transparency, clean-label positioning, packaging convenience, foodservice pack flexibility, private label defense, distribution depth and the ability to scale regional taste profiles globally.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 191.55 Billion | |

| 2035 Projected Market Size | US$ 346.29 Billion | |

| CAGR (2026-2035) | 6.1% | |

| Largest Market | Asia-Pacific, 41.4% Share in 2025 | |

| Fastest Growing Market | Hot and Spicy Sauces, 8.4% CAGR During 2026-2035 | |

| Dominating Sales Channel | Retail and Household Consumption, 61.7% Share in 2025 | |

| Dominating Product | Sauces, 54.8% share in 2025 | |

| By Product | Sauces, Dressings, Condiments, Dips and Spreads | |

| By Packaging Type | Bottles, Jars, Pouches, Sachets, Tubes, Cups and Bulk Packs | |

| By Ingredient Base | Tomato-Based, Chili-Based, Soy-Based, Vinegar-Based, Oil-Based, Dairy-Based, Fruit-Based, Herb and Spice-Based and Others | |

| By Sales Channel | Retail, Foodservice, Industrial and Institutional | |

| By End-User | Household, Quick-Service Restaurants, Full-Service Restaurants, Hotels, Catering, Food Manufacturers and Institutional Kitchens | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Why This Report Matters in 2026

Sauces, dressings and condiments have become one of the most important value-creation areas in packaged food because consumers want more flavor without adding cooking complexity. Inflation changed meal behavior in several developed markets, encouraging consumers to recreate restaurant-style meals at home. At the same time, younger consumers are experimenting with spicy, global and fusion flavors more often than previous generations. Brand owners are therefore competing to own meal occasions rather than only shelf space. Ketchup, mayonnaise and mustard remain important, but growth is increasingly influenced by hot sauces, premium pasta sauces, dipping sauces, wing sauces, salad dressings and globally inspired cooking sauces.

The decisive 2026 shift is consolidation around flavor platforms. McCormick’s agreement to combine with Unilever’s Foods business would unite McCormick, French’s, Frank’s RedHot, Cholula, Stubb’s, OLD BAY, Lawry’s, Hellmann’s and Knorr under one flavor-focused company. Campbell’s progress with Rao’s shows another direction, where premium Italian sauces can scale nationally while protecting quality perception. These moves show that large food companies are not treating sauces as small add-ons. They are treating them as strategic portfolios that can support retail, foodservice and industrial flavor demand.

Buyers need a report that separates mature staple condiments from premium and faster-growth flavor platforms. A supermarket category manager, a foodservice distributor, a private label manufacturer and a strategic investor will not evaluate this market in the same way. Pricing power depends on brand trust, flavor intensity, packaging format, ingredient claims, channel reach and promotional discipline. Procurement also depends on tomato paste, peppers, vinegar, oils, sugar, eggs, spices, packaging and logistics. A useful market view must connect consumer taste shifts with manufacturing economics and channel execution.

Strategic Indicators For Sauces, Dressings and Condiments

High Regulation Impact

Food safety, traceability, allergen disclosure, nutrition labeling and claims management are becoming more important for sauce and condiment manufacturers. Products may include eggs, mustard, sesame, soy, dairy, fish, gluten, sulfites or spice blends that require strong ingredient control and clear labeling. The FDA Food Traceability Final Rule also raises the importance of lot-level tracking and supply-chain records for selected foods and ingredients, even though enforcement timing has been extended. Regulatory exposure is especially relevant for dressings, mayonnaise, fresh dips, refrigerated sauces and foodservice products where contamination, allergens or incorrect labels can trigger recalls and customer penalties.

High Investment Activity

Investment is concentrating in premium sauces, hot sauces, Latin flavors, Asian sauces, foodservice packs, clean-label dressings and high-growth brands with strong household repeat purchase. McCormick’s agreement with Unilever’s Foods business is the clearest signal that global flavor portfolios are becoming more valuable. Campbell’s acquisition of Sovos Brands and continued push behind Rao’s also shows that premium sauce brands can attract large strategic buyers when distribution expansion, brand equity and pricing power are visible. Investment is also moving into packaging convenience, squeeze formats, digital commerce and foodservice innovation kitchens.

Supply Chain Disruption

Supply-chain pressure is concentrated around tomatoes, peppers, edible oils, eggs, mustard seed, vinegar, glass jars, plastic bottles, flexible pouches, caps and cartons. Weather issues can affect tomato and chili pepper supply, while edible oil and egg costs can influence mayonnaise and dressing margins. Packaging shortages or freight delays can disrupt promotional windows because sauces and condiments are often tied to grilling season, holidays, sports events and summer eating occasions. Manufacturers with multi-region ingredient sourcing, strong co-manufacturing networks and flexible packaging options can protect service levels better than single-source suppliers.

Pricing Volatility

Pricing volatility is visible across both branded and private label products. Premium brands can pass through more cost when they have strong quality cues, recognizable ingredients and loyal shoppers. Value brands and private label products face tighter price gaps, especially when retailers push for lower shelf prices. Tomato paste, oils, eggs, vinegar, sweeteners, peppers and spices can create cost swings across product lines. Packaging format also matters because glass jars, squeeze bottles and single-serve packets have different cost structures. Strong category managers track gross margin by product format rather than averaging across all sauces.

Procurement Pressure

Procurement teams are being asked to protect margins without weakening taste, consistency or food safety. Ingredient substitutions can damage brand trust quickly because consumers notice changes in texture, acidity, heat, sweetness and mouthfeel. Foodservice buyers face additional pressure because a sauce must perform consistently across restaurants, delivery kitchens and reheating conditions. Large customers increasingly evaluate suppliers on fill-rate, allergen control, packaging flexibility, innovation support and ability to provide custom formats. Procurement advantage is shifting toward suppliers that can manage both commodity exposure and flavor integrity.

New Technology Adoption

Technology adoption is strongest in flavor analytics, sensory testing, automated batching, traceability systems, packaging automation and demand forecasting. Sauce producers need repeatable viscosity, pH, color, heat level and emulsion stability. Digital quality controls help reduce batch variation, while AI-enabled flavor analysis can identify emerging combinations from restaurant menus, social media and retail velocity data. Foodservice suppliers are also using data from limited-time offers to decide which sauces deserve permanent rollout. Technology matters most when it protects taste consistency and shortens the time from insight to shelf.

Company Coverage Preview

McCormick is positioned as one of the most influential companies in this market because it combines retail brands, foodservice offerings and flavor solutions for manufacturers. The company’s portfolio includes McCormick, French’s, Frank’s RedHot, Cholula, Stubb’s, OLD BAY, Lawry’s and other brands that directly participate in condiments, sauces, seasonings and foodservice flavor systems. The planned combination with Unilever’s Foods business would add Hellmann’s, Knorr and several regional food brands, creating a broader global flavor platform with stronger reach across retail, foodservice and industrial customers. McCormick’s competitive advantage comes from flavor science, brand building, distribution, foodservice access and experience integrating acquired brands.

The Campbell’s Company has strengthened its position through Rao’s, Prego and Pace. Rao’s has become particularly important because it gives Campbell a premium sauce platform with strong brand credibility and pricing power. The company has stated that Rao’s has grown into a billion-dollar portfolio spanning Italian sauces, soups, pasta and frozen meals. The brand also reached number one sauce-brand status across all U.S. regions and introduced Creamy Marinara as a leading innovation in the Italian category. Campbell’s advantage is different from McCormick’s because it is centered on meals, pasta sauces and pantry solutions rather than broad flavor systems.

Kraft Heinz remains important through Heinz, HP Sauce, A.1., Grey Poupon, Bull’s-Eye, Lea and Perrins, Primal Kitchen and other condiment assets. Heinz remains one of the most recognizable ketchup and condiment brands worldwide, while Primal Kitchen gives the company a cleaner-label and premium wellness-oriented platform. The company’s opportunity is to defend legacy categories while moving into globally inspired sauces, reduced-sugar recipes, spicy formats and retail packs that appeal to younger consumers. The strongest near-term challenge for large legacy brands is not awareness. The challenge is keeping flavor innovation fast enough while defending shelf space against private label and challenger brands.

AI Impact Analysis

AI is becoming useful in sauces, dressings and condiments because flavor innovation is increasingly data-driven. Manufacturers can analyze restaurant menus, food delivery platforms, social media recipes, retail scan data and foodservice customer feedback to identify emerging flavor combinations before they become mainstream. Hot honey, chili crisp, Korean barbecue, street corn, truffle, spicy ranch, smoky chipotle and creamy pesto all show how fast flavor signals can move from restaurants into retail bottles. AI can help brand teams decide which combinations are worth pilot production and which are only short-lived online trends.

AI can also support recipe optimization, quality control and demand planning. Sauce production depends on balancing acidity, sweetness, heat level, texture, color and shelf stability. Advanced analytics can help detect when ingredient variation may affect batch quality. Demand planning is equally important because sauces can be seasonal, promotional and event-driven. Grilling sauces, wing sauces, salad dressings and holiday cooking products often create short demand spikes, making forecast accuracy valuable for service levels and working capital management.

Adoption will remain practical rather than fully automated. Human sensory panels, culinary teams and food scientists will still decide whether a flavor is credible, craveable and scalable. AI can narrow the field of ideas, predict regional demand and improve manufacturing consistency, but it cannot replace taste judgment. Companies that combine culinary expertise with better data will move faster than companies relying only on annual innovation calendars.

Disruption Analysis

Disruption in this market is coming from premiumization, private label pressure, global flavor migration and foodservice retail crossover. Premium sauce brands are proving that consumers will pay more when the product feels closer to restaurant quality. Rao’s is a strong example because its premium ingredient story and slower-cooked positioning helped it expand from a regional pasta sauce into a billion-dollar portfolio. At the same time, private label is gaining shelf space in mature categories such as ketchup, mayonnaise and basic dressings, forcing branded suppliers to defend through innovation and promotional discipline.

Global flavor migration is changing product development. Consumers are using sauces to explore international cuisines without learning complex recipes. Korean barbecue, Thai sweet chili, Mexican street corn, Japanese teriyaki, peri peri, harissa, sriracha, gochujang and chili crisp-inspired products are becoming retail and foodservice opportunities. The fastest growth is not always in traditional table condiments. Growth is often coming from sauces that turn simple proteins, vegetables, sandwiches, rice bowls and snacks into more flavorful meals.

Foodservice is also shaping retail innovation. Restaurant chains use sauces to create signature menu identity, while retail brands launch bottles that help households recreate restaurant-style dishes. Wing sauces, burger sauces, sandwich sauces and dipping sauces are benefiting from this crossover. Packaging is part of the disruption because squeeze bottles, single-serve cups, pouches and foodservice jugs each support different occasions. Suppliers that can move ideas across foodservice and retail formats will capture more of the category’s growth.

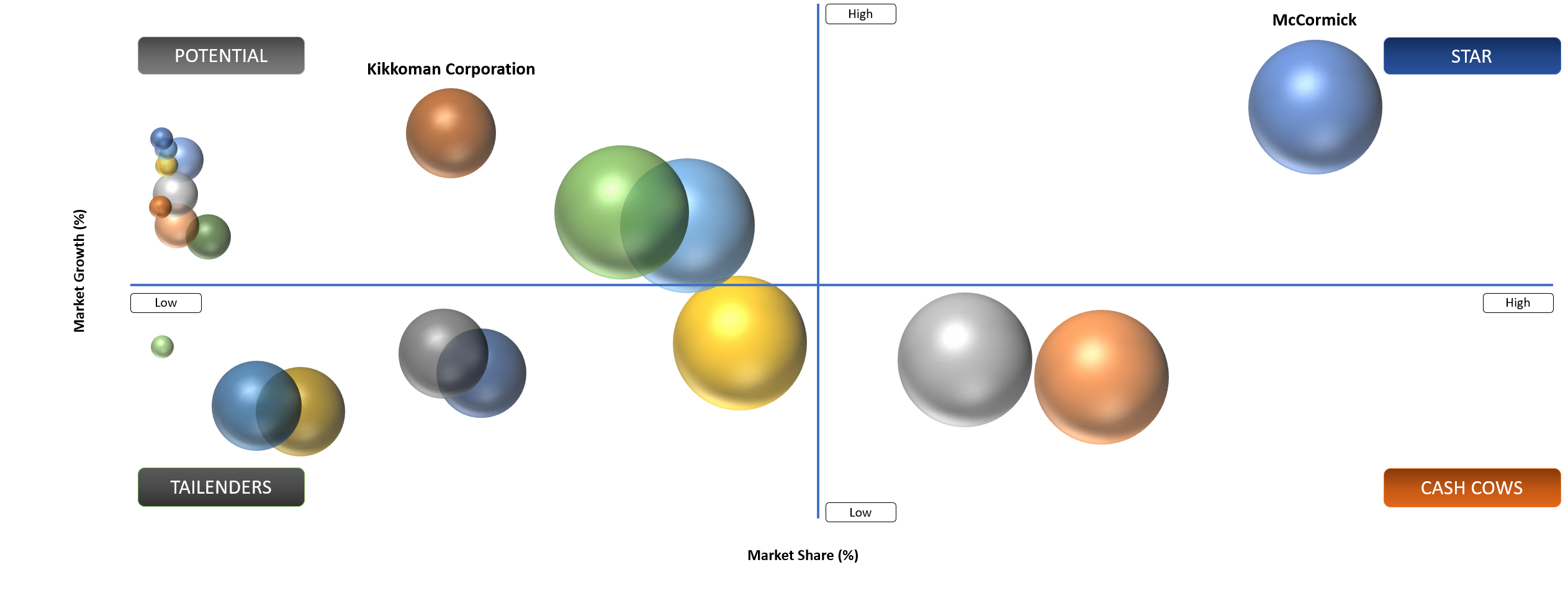

BCG Matrix: Company Evaluation

STAR

Star players include McCormick, Unilever Foods, The Campbell’s Company, Kraft Heinz, Kikkoman, Nestlé, Hormel Foods, Kewpie Corporation and Ajinomoto Co., Inc. Strong players combine high household penetration, trusted brands, foodservice relationships, flavor development capabilities, manufacturing scale and distribution reach. McCormick’s flavor portfolio and planned combination with Unilever Foods would create a broader global platform across condiments, cooking aids and sauces. Campbell’s gains strength from Rao’s premium growth, while Kraft Heinz remains a major global condiment leader through Heinz and related brands.

POTENTIAL

Potential players include premium pasta sauce brands, hot sauce challengers, clean-label dressing makers, regional ethnic sauce companies and foodservice-focused sauce developers. Smaller brands can scale quickly when they own a distinctive flavor profile, strong ingredient story or loyal community. Growth potential is strongest where brands can expand from one hero product into adjacent meal occasions without diluting quality perception. Challenger brands face a harder route once they enter mass retail because trade spending, slotting, promotion and supply reliability become as important as product taste.

Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact | Demand Concentration | Impacted Use Case | Strategic Impact |

| Consumers recreate restaurant-style meals at home | High | U.S., Canada, UK, India, Japan and Australia | Pasta sauces, wing sauces, burger sauces, dipping sauces and dressings | Supports premium retail sauces and meal-enhancing condiments |

| Spicy and global flavor adoption expands sauce usage | High | North America, Asia-Pacific and Europe | Hot sauces, chili sauces, Korean barbecue sauces, teriyaki sauces and street-food inspired sauces | Accelerates innovation and premium pack launches |

| Foodservice chains use sauces as menu identity tools | Medium To High | U.S., China, India, Japan and Middle East | Signature sauces, wing sauces, dips and bulk condiment packs | Strengthens custom sauce and foodservice sales |

| Premium sauce brands gain shelf space | Medium To High | U.S., Western Europe and urban Asia-Pacific | Pasta sauces, dressings and clean-label condiments | Supports higher unit pricing and strategic acquisitions |

Restaurant-Style Home Cooking Is Expanding Retail Sauce Demand

Consumers are using sauces to make home meals feel more complete without adding long preparation time. Pasta sauces, stir-fry sauces, wing sauces, burger sauces and salad dressings help households change the flavor of repeat proteins, vegetables, sandwiches, pasta and rice dishes. The behavior supports higher purchase frequency because one sauce can serve multiple meals across the week. Premium brands benefit when they position the product as an affordable restaurant-style upgrade rather than a basic pantry refill.

Retailers are also giving more space to sauces that create meal solutions. A jar of pasta sauce, a bottle of hot sauce or a dipping sauce can link to pasta, chicken, frozen snacks, salad kits, meat alternatives and prepared foods. Cross-merchandising has become more important because sauce brands can influence the full basket. Strong suppliers are helping retailers build meal occasions rather than only filling condiment shelves.

Foodservice influence remains strong. Wing flavors, burger sauces, spicy ranch, creamy jalapeño, Korean barbecue and hot honey first gained traction through restaurants, delivery menus and social media before entering retail. Brands that monitor foodservice adoption can move faster into shelf-stable or refrigerated formats. The commercial opportunity is strongest where the product solves a daily meal need and also carries a recognizable flavor identity.

Restraint Impact Analysis

| Restraint | Drag On Market Growth | Primary Impact Area | Impacted Use Case | Strategic Impact |

| Commodity cost swings pressure margins | High | Tomatoes, peppers, oils, eggs, sugar, vinegar and packaging | Mayonnaise, dressings, pasta sauces and ketchup | Raises need for pricing discipline and hedging |

| Private label expansion limits branded pricing power | Medium To High | Mature retail shelves | Ketchup, mustard, mayonnaise and basic dressings | Forces sharper brand differentiation |

| Sugar, sodium and additive concerns influence formulation | Medium | Developed markets | Ketchup, barbecue sauces, dressings and dips | Supports cleaner-label and reformulated products |

| Retail shelf competition slows small brand scale | Medium | Grocery and mass retail | Premium sauces and challenger condiments | Increases trade spend and distribution costs |

Input Cost and Private Label Pressure Restrain Margin Expansion

Sauce and condiment manufacturers remain exposed to cost swings across agricultural ingredients and packaging. Tomatoes, peppers, eggs, edible oils, sweeteners and spices can each effect product economics depending on the recipe. Packaging also plays a major role because glass jars, PET bottles, caps, labels and pouches account for a meaningful share of finished goods cost. Premium brands can manage cost increases more effectively when consumers see quality value, but mass-market staples face stronger resistance when price gaps widen.

Private label is a serious restraint in mature categories because retailers can offer lower-priced alternatives in ketchup, mustard, mayonnaise, dressings and pasta sauces. Branded companies must therefore defend value through flavor, packaging, advertising, innovation and foodservice credibility. Price promotions may protect volume in the short term, but heavy promotion can weaken category profitability if not managed carefully.

Health perception is another constraint. Consumers still want strong flavor, but they are more aware of sugar, sodium, oils, preservatives and artificial ingredients. Brands cannot reformulate aggressively without risking taste rejection. The best operators are using gradual recipe improvements, cleaner ingredient positioning and portion-control formats rather than removing the flavor characteristics that made the product successful.

Segment Analysis

Sauces Will Continue To Dominate Product Demand

Sauces will continue to dominate because they cover the widest range of meal occasions across retail, foodservice and industrial use. Pasta sauces, soy sauces, chili sauces, hot sauces, barbecue sauces, teriyaki sauces, curry sauces and cooking sauces each serve distinct usage occasions. Compared with dressings or classic condiments, sauces are more closely connected to meal preparation, protein flavoring, snacking, dipping and global cuisine exploration. The product group accounted for 54.8% share in 2025 and remains the core revenue base for most large suppliers.

Premium pasta sauces are one of the strongest value pools within sauces. Rao’s has shown how a premium ingredient story, restaurant heritage and expanded retail distribution can create strong pricing power. Campbell’s highlighted Rao’s growth into a billion-dollar portfolio across Italian sauces, soups, pasta and frozen meals. The brand also identified Creamy Marinara as a major Italian-category innovation, showing how premium sauce brands can extend without leaving their core meal occasion.

Hot and spicy sauces are the leading growth engine because heat has moved from niche preference to mainstream flavor behavior. Consumers are no longer choosing only one hot sauce. They are buying multiple heat and flavor profiles for wings, tacos, burgers, noodles, rice bowls and snacks. Frank’s RedHot, Cholula, sriracha-style sauces, Korean barbecue, mango habanero and spicy ranch formats show how heat is being blended with sweetness, creaminess, acidity and global flavor cues.

Pasta Sauces

Pasta sauces are shifting from value red sauce toward premium, ingredient-led and creamy formats. Rao’s has become a key benchmark for premium growth because it uses a quality-led brand story, strong distribution and innovation while keeping the core recipe promise clear. Campbell’s acquisition of Sovos Brands gave the company a premium sauce asset with high household repeats potential and category expansion options. Pasta sauce also benefits from meal affordability because consumers can build a full dinner around pasta, sauce and a protein at a lower cost than restaurant dining.

Creamy and specialty pasta sauces are gaining attention because consumers want variation beyond basic marinara. Creamy marinara, pesto, vodka sauce, arrabbiata and truffle-inspired sauces serve households looking for indulgence without complicated cooking. Strong brands can use these formats to increase basket value and encourage repeat purchase. Shelf-stable jars remain important, but refrigerated and premium imported-style sauces can capture higher unit prices where shoppers associate the product with restaurant quality.

Food manufacturers and foodservice operators also use pasta sauces as bases for ready meals, frozen meals and prepared entrees. The commercial value extends beyond grocery shelves because sauces support branded meal extensions. A premium pasta sauce brand can scale into pasta, soups, frozen meals and meal kits when consumers trust the taste profile. Rao’s expansion across sauces, soups, pasta and frozen meals shows why premium sauce platforms are attractive to strategic buyers.

Hot and Spicy Sauces

Hot and spicy sauces are expected to grow at 8.4% CAGR during 2026-2035 because heat is increasingly tied to flavor discovery rather than only spice intensity. Younger consumers often treat hot sauces as collectibles, rotating between chili, smoky, tangy, fruity, fermented and creamy formats. Foodservice has accelerated this behavior by adding limited-time sauces and spicy menu platforms that shoppers later look for in retail.

Brand extensions are becoming more specific. Wing sauces, squeeze sauces, dipping sauces, hot honey, Korean barbecue, mango habanero and spicy ranch each meet different eating occasions. A household may use one sauce for wings, another for burgers and another for rice bowls. This multi-bottle behavior supports volume and value growth even in mature households.

Foodservice demand is equally important. Quick-service and casual dining chains use spicy sauces to create recognizable menu items without changing core ingredients. Chicken, fries, sandwiches, tacos and burgers can all be refreshed with a new sauce. Suppliers that can provide both retail bottles and foodservice packs have stronger innovation leverage because the same flavor idea can move across channels.

Geographical Penetration

U.S. Sauces, Dressings and Condiments Market Trends

The U.S. remains the most important country market for branded sauces, dressings and condiments because household penetration is high and the category has deep links with everyday meals. Ketchup, mayonnaise, mustard, barbecue sauce, ranch dressing, hot sauce, pasta sauce and dipping sauces are all heavily embedded in home cooking, snacking and foodservice meals. Retail demand is supported by a strong supermarket, mass retail, club store and e-commerce structure, while foodservice demand is supported by quick-service chains, sports bars, casual dining, delivery kitchens and institutional cafeterias. Large suppliers use the U.S. as a launch market for spicy flavors, global sauce formats and premium meal solutions because consumer feedback and retail scan data are available quickly.

Premiumization is one of the most important U.S. dynamics. Rao’s has become a strong example because it moved from a niche premium pasta sauce into a billion-dollar portfolio after expanding distribution and brand visibility. Campbells has stated that Rao’s is now the number one sauce brand in all U.S. regions, which indicates that premium pasta sauce can scale nationally when quality perception and retail execution align. This creates pressure on mainstream pasta sauce brands to defend against both premium brands and private label alternatives.

Hot sauce and dipping sauce demand is also strong in the U.S. because sports viewing, chicken wings, burgers, tacos, snacks and delivery meals support frequent usage. Frank’s RedHot, Cholula, Tabasco, sriracha-style sauces and many challenger brands compete across heat levels and flavor formats. The category is no longer only about the hottest sauce. Consumers increasingly look for heat balanced with ranch, garlic, honey, fruit, barbecue, lime, smoke or fermented chili flavor. Foodservice chains influence these preferences quickly because limited-time sauces can become retail opportunities.

Regulation and traceability are becoming more visible in the U.S. because sauces and dressings can involve allergen, acidified food, refrigerated product and ingredient-origin complexity. FDA traceability requirements and food safety expectations increase pressure on manufacturers to maintain stronger lot records, supplier controls and recall readiness. Retailers and foodservice operators also want suppliers that can provide documentation, consistent labeling and reliable fulfilment. Competitive advantage therefore depends on more than brand strength. Operational discipline, food safety systems and supply-chain transparency are becoming part of the buying decision.

India Sauces, Dressings and Condiments Market Landscape

India is one of the most attractive long-term growth markets because urban consumers are using packaged sauces across snacks, street-food inspired meals, sandwiches, noodles, pasta, rolls, momos, pizzas, grilled foods and home cooking. Ketchup remains a high-penetration product, but faster growth is coming from chili sauces, mayonnaise, sandwich spreads, pasta sauces, peri peri sauces, schezwan sauces, dips and quick-cooking gravies. Young consumers are particularly open to spicy, tangy and fusion flavors that fit both Indian snacks and international fast-food formats. Quick-service restaurants and cloud kitchens are helping packaged sauces become more familiar across households.

Foodservice expansion is a major driver in India. Quick-service restaurants, cafés, bakery chains, pizza brands, burger outlets and delivery kitchens use sauces to maintain consistency across locations. A sauce can define the flavor of a burger, wrap, sandwich, roll or fried snack without requiring complex kitchen preparation. This creates opportunities for bulk packs, sachets, pouches and foodservice jars. Local manufacturers are strong in value formats, while multinational brands compete through quality perception, safety, imported flavors and modern retail availability.

Retail growth is supported by modern trade, quick commerce and e-commerce. Small packs are important because shoppers often trial new sauces before moving to larger bottles. Sachets and smaller jars also help brands enter price-sensitive households. Quick commerce is changing discovery because consumers can add sauces to snack, frozen food, pasta or instant food orders. Brands that win search visibility and bundle sauces with meal occasions can grow faster than brands relying only on traditional shelf visibility.

India also has a strong local taste requirement. Western sauces rarely scale without adaptation to Indian heat, sweetness, tanginess and vegetarian preferences. Mayonnaise and spreads often need eggless options, while pasta sauces and dips may require spicier profiles. Strong companies localize formats without losing brand identity. Growth will favor suppliers that can combine affordable packs, regional taste understanding, foodservice reach and consistent quality across hot climate distribution.

Japan Sauces, Dressings and Condiments Market Outlook

Japan is a mature but highly valuable market because consumers expect quality, consistency, convenient packaging and refined taste balance. Soy sauce, ponzu, mayonnaise, salad dressings, dipping sauces, yakiniku sauces, tonkatsu sauce, teriyaki sauce and pasta sauces serve daily meal occasions across households and foodservice. Packaging design and portion control matter because Japanese households often value neat dispensing, freshness and compact storage. Premium sauce demand is supported by consumers who pay for quality ingredients, balanced taste and brand trust.

Convenience retail strongly influences sauce and condiment demand in Japan. Bento meals, salads, ready-to-eat foods, fried snacks, noodles and rice dishes often use small packs, dressings and dipping sauces. Manufacturers must support portion-control formats and stable flavor quality across prepared-food channels. Foodservice also demands reliable sauces for ramen, grilled meats, fried foods, rice bowls and western-style meals. Japanese buyers are highly sensitive to texture, salt balance, aroma and aftertaste, which makes product development more demanding than simple flavor translation.

Kikkoman and Kewpie are important domestic players because they have deep category trust and strong expertise in soy-based sauces, mayonnaise, dressings and seasonings. Japanese sauce innovation often focuses on subtle flavor variation, healthier claims, reduced salt, premium ingredients and easy-use packaging. International brands can enter premium or global cuisine niches, but mass adoption usually requires local taste adaptation. Consumers may accept global flavors, but the execution must match Japanese quality expectations.

Japan also provides export influence because soy sauce, teriyaki, Japanese mayonnaise and dipping sauces have global appeal. International demand for Japanese cuisine supports overseas growth for Japanese sauce companies. Suppliers with strong manufacturing discipline and brand authenticity can benefit from both domestic stability and global cuisine adoption. Growth will be moderate in volume but attractive in value where premiumization, convenience and overseas brand expansion intersect.

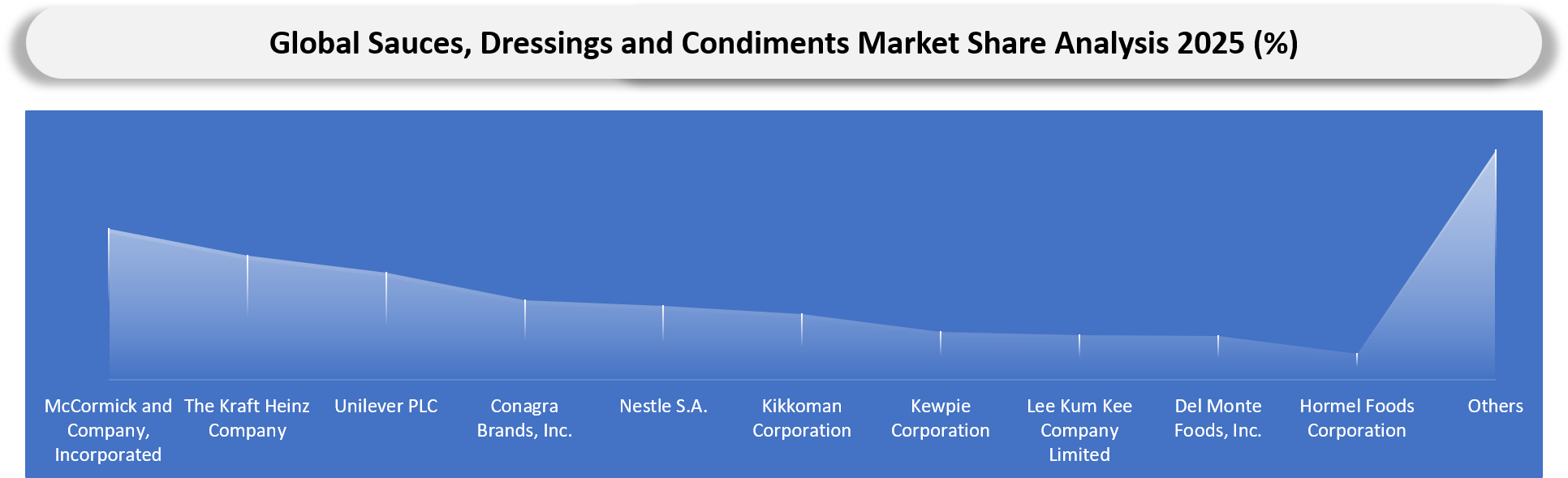

Competitive Landscape

Competition is split between global branded food companies, regional sauce specialists, ethnic cuisine leaders, private label manufacturers, foodservice sauce developers and industrial flavor suppliers. Market share should be viewed by product family because ketchup, pasta sauce, hot sauce, mayonnaise, salad dressing, soy sauce and cooking sauces have different leaders and different pricing structures.

Global companies compete on distribution depth, brand trust, advertising scale, foodservice access and ability to launch innovations across multiple countries. McCormick, Kraft Heinz, Unilever Foods, Campbell’s, Kikkoman, Kewpie, Nestlé and Ajinomoto each have different category strengths, making direct comparison useful only when product focus and channel mix are defined.

Private label suppliers compete on value, retailer relationships and fast replication of mainstream flavors. Premium brands compete through ingredient quality, culinary credibility, packaging and household loyalty. Challenger hot sauce and ethnic sauce brands compete through authenticity, stronger flavor identity and social media-driven trial.

Foodservice and industrial suppliers compete on custom formulation, pack size, margin support, kitchen performance, stability, allergen control and delivery reliability. Competitive benchmarking should track retail velocity, foodservice wins, product launches, private label exposure, premium pricing power, distribution expansion, ingredient sourcing and ability to move flavors from restaurant trends into retail products.

Major Pain Points

- Mature categories such as ketchup, mayonnaise and basic dressings face private label pressure that limits branded pricing power.

- Tomato, egg, edible oil, chili pepper, vinegar, mustard seed, sweetener and packaging cost volatility creates margin pressure across core products.

- Retail shelf space is crowded, making new brand entry expensive and increasing the need for promotional support.

- Foodservice customers need custom flavors, stable supply and bulk formats, creating complexity for manufacturers built mainly around retail packs.

- Health-conscious consumers want lower sugar, lower sodium and cleaner ingredients, but taste rejection can occur when reformulation moves too quickly.

- Premium brands must protect quality perception while scaling distribution into mass retail and club channels.

- Regional taste differences make global launches difficult because heat, sweetness, acidity, texture and usage occasions vary widely.

- Allergen control, traceability and labeling accuracy are becoming more important as recipes include eggs, mustard, sesame, soy, dairy and complex spice blends.

Recent Developments

- March 2026: McCormick and Unilever entered into an agreement to combine McCormick with Unilever’s Foods business excluding India and other excluded businesses. The transaction valued Unilever Foods at approximately US$ 44.8 billion and would create a flavor-focused company with around US$ 20 billion in combined fiscal 2025 revenue.

- March 2026: The Campbell’s Company highlighted that Rao’s had grown into a US$ 1 billion portfolio across Italian sauces, soups, pasta and frozen meals. Campbells also identified Rao’s Creamy Marinara as the number one innovation in the Italian category and stated that Rao’s is now the number one sauce brand in all U.S. regions.

- January 2026: McCormick completed the acquisition of an additional 25% ownership interest in McCormick de Mexico from Grupo Herdez for US$ 750 million, increasing McCormick’s ownership to 75% and strengthening its platform for Mexico and Latin America expansion.

- January 2026: Frank’s RedHot launched four new wing and dipping sauces - Garlic Parmesan Wing Sauce and Dip, Spicy Maple Wing Sauce and Dip, Pineapple Hawaiian Wing Sauce and Dip and Ghost Pepper Ranch Sauce - to strengthen its restaurant-style wings and at-home dipping portfolio ahead of the Super Bowl season.

- April 2025: Frank’s RedHot launched six new sauces across three product lines, including Burger Squeeze Sauce, Korean BBQ Squeeze Sauce, Secret Chicken Dip’n Sauce, Sweet N’ Sour Dip’n Sauce, General Tso Wings Sauce and Mango Habanero Wings Sauce, expanding its squeeze, dipping and wing sauce portfolio for retail consumers.

- May 2024: Frank’s RedHot launched Mini Squeeze Sauces in Sriracha and Creamy Buffalo flavors in portable 1.7-ounce bottles at Walmart, targeting on-the-go usage and trial-size hot sauce consumption.

- March 2024: Campbell completed the acquisition of Sovos Brands for US$ 23 per share in an all-cash transaction with an enterprise value of approximately US$ 2.7 billion. The deal added Rao’s, Michael Angelo’s and noosa to Campbell’s portfolio and strengthened the company’s premium meals and sauces position.

- March 2024: Frank’s RedHot launched two new sauce lines, including Buffalo Ranch Dip’n Sauce, Roasted Garlic Dip’n Sauce, Sweet and Tangy Golden Dip’n Sauce, Sriracha Squeeze Sauce, Hot Honey Squeeze Sauce and Creamy Buffalo Squeeze Sauce, expanding the brand from classic hot sauce into thicker dipping and controlled-drizzle squeeze formats.

Key Procurement Priorities and Buyer Evaluation Criteria

- Retailers evaluate suppliers on shelf velocity, margin contribution, promotional support, pack design, assortment role, private label exposure and ability to create incremental meal occasions.

- Foodservice buyers prioritize consistency, bulk packaging, kitchen performance, custom formulation, allergen management, supply reliability and ability to support limited-time menu launches.

- Manufacturers evaluate co-packers and ingredient suppliers on tomato paste quality, chili pepper consistency, oil supply, vinegar quality, emulsion stability, packaging availability and food safety documentation.

- Premium brands prioritize ingredient integrity, recipe protection, sensory consistency, distribution discipline and quality control because scaling too quickly can damage consumer trust.

- Preferred suppliers provide innovation support, pack flexibility, traceability systems, retail execution, foodservice technical support and clear cost visibility across ingredients and packaging.

Analyst View and Opinion

- Premium sauce brands will keep attracting strategic buyers because they combine high repeat purchase with clear quality cues and stronger pricing power than commodity condiments.

- Hot and spicy sauces will remain one of the most attractive growth pockets because heat is becoming a flavor language rather than a niche preference.

- Foodservice will continue shaping retail innovation as restaurant sauces, wing flavors and sandwich sauces move into grocery shelves faster than traditional product development cycles.

- Private label will put continued pressure on basic ketchup, mustard, mayonnaise and dressings, forcing branded players to defend through flavor extensions, packaging and premium claims.

- Pasta sauces will remain a high-value category because they support affordable home meals and offer room for premium positioning through ingredients, cooking style and restaurant heritage.

- Global flavor consolidation will intensify as large companies look for portfolios that connect retail brands, foodservice solutions and industrial flavor systems.

- Sauce packaging will become a stronger differentiator, especially squeeze bottles, single-serve cups, pouches, club packs and foodservice jugs.

- Reformulation will remain difficult because consumers want healthier labels but still reject products that lose familiar taste, texture or mouthfeel.

- Regional taste adaptation will decide international success because sweetness, heat level, acidity and usage occasions differ sharply between the U.S., India, Japan, Europe and Latin America.

- Data-led innovation will become more important as companies use restaurant menus, e-commerce search, social media and retail scan data to identify flavors before competitors move.

Target Audience

| Industry | Who Should Buy This Report? | Reason To Buy This Report |

| Food Manufacturers | Strategy Teams, Product Managers, Innovation Leaders | Identify high-growth product groups, flavor trends, packaging shifts and premiumization opportunities |

| Retailers and Category Managers | Grocery Buyers, Private Label Teams, Merchandising Heads | Benchmark category structure, shelf-space priorities, pricing and brand positioning |

| Foodservice Operators | QSR Teams, Casual Dining Chains, Cloud Kitchen Operators | Evaluate sauce-led menu differentiation, custom formulation and bulk pack demand |

| Ingredient Suppliers | Tomato Paste, Chili Pepper, Oil, Vinegar and Spice Suppliers | Track demand outlook By Product and application |

| Packaging Companies | Bottle, Jar, Pouch, Sachet and Cup Suppliers | Identify growth in convenience packaging, single-serve formats and foodservice packs |

| Investors | Private Equity Teams, Strategic Investors, Mergers and Acquisitions Teams | Assess premium sauce brands, foodservice platforms and consolidation opportunities |

| Co-Packers | Contract Manufacturers, Quality Teams, Commercial Heads | Understand outsourcing demand, formulation needs and quality expectations |

| Consulting Firms | Food and Beverage Strategy Teams, Procurement Advisors | Support market entry, partner screening, pricing analysis and category strategy |

What DataM Uniquely Provides

- Client-ready views that connect product, flavor platform, packaging, region, channel, end-use and supplier capability.

- Bottom-up market modelling using brand portfolios, retail checks, distributor interviews, foodservice demand, import-export signals and ingredient cost tracking.

- Supplier scorecards covering innovation speed, foodservice strength, ingredient control, packaging flexibility, private label exposure and regional distribution.

- Pricing intelligence covering tomato paste, oils, eggs, peppers, vinegar, packaging formats, branded price premiums and private label pressure.

- Flavor opportunity mapping across hot sauces, pasta sauces, dressings, dips, global sauces, clean-label condiments and restaurant-inspired retail products.

- Procurement risk assessment covering ingredient volatility, allergen control, traceability, formulation change risk and co-manufacturing capacity.